- Advanced Materials

- Shotcrete/Sprayed Concrete Market

Shotcrete/Sprayed Concrete Market Size, Share, and Growth Forecast 2026 - 2033

Shotcrete/Sprayed Concrete Market by Process Type (Wet-Mix Shotcrete, Dry-Mix Shotcrete), System Type (Robotic Spraying System, Manual Spraying System), Reinforcement Type (Steel Fiber Reinforced, Synthetic Fiber Reinforced, Non-Fiber Reinforced Shotcrete), End-user (Underground Construction, Protective Coatings, Civil Constructions, Repair Works, Mining, Others), Regional Analysis, 2026 - 2033

Shotcrete/Sprayed Concrete Market Size and Trend Analysis

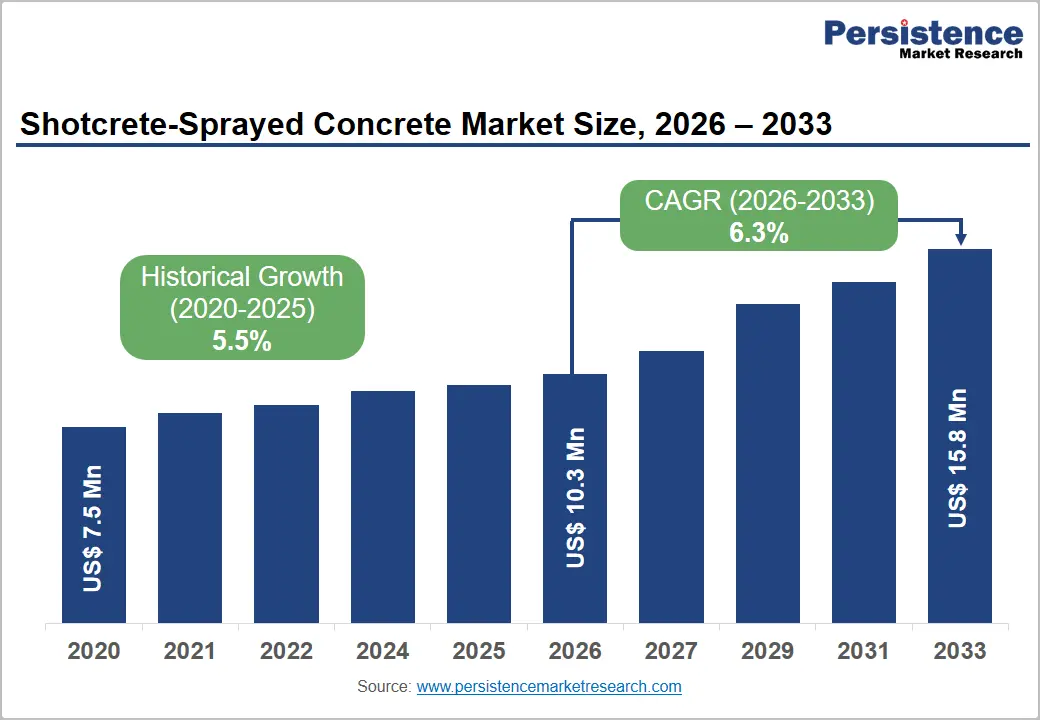

The global shotcrete/sprayed concrete market size is expected to be valued at US$ 10.3 billion in 2026 and projected to reach US$ 15.8 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033. This sustained expansion is primarily driven by accelerating investment in underground infrastructure, including metro rail tunnels, road tunnels, and underground mining, across Asia Pacific, the Middle East, and North America, where shotcrete serves as the structurally indispensable primary lining material.

Government-mandated urbanization programs, the global energy transition's demand for critical mineral extraction, and the progressive shift toward mechanized robotic application systems are collectively reinforcing demand across both emerging and mature geographies.

Key Industry Highlights:

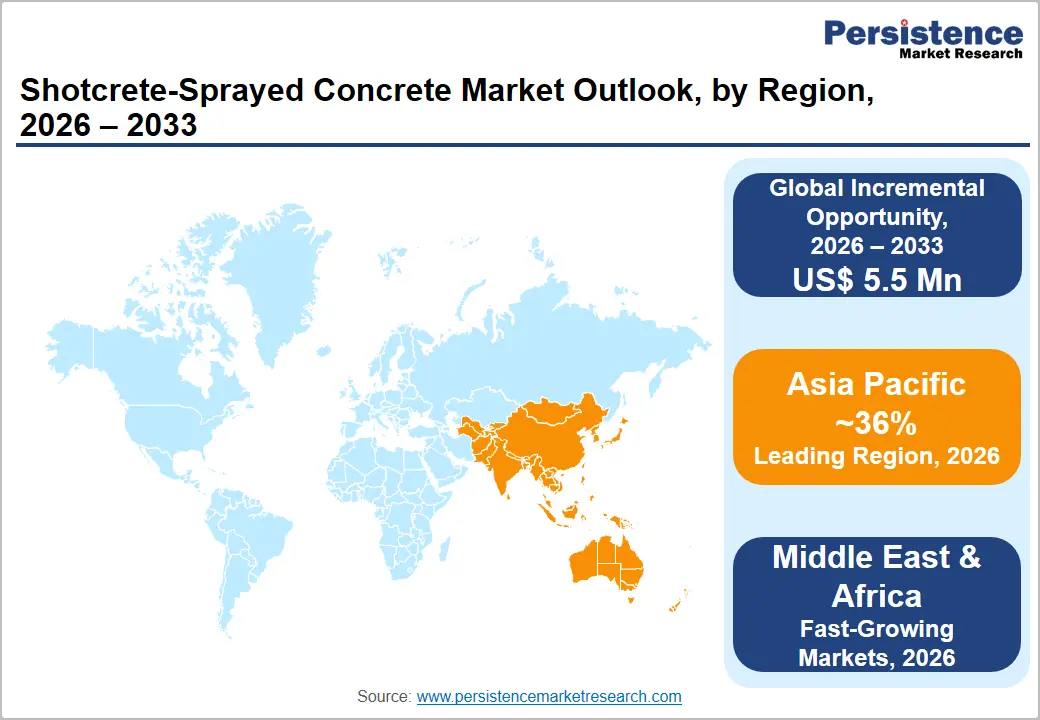

- Leading Region: Asia Pacific leads the global shotcrete/sprayed concrete market with approximately 36% share in 2026, underpinned by China's metro expansion, India's mountain tunnel buildout under the PM Gati Shakti program, and government-mandated infrastructure investment cycles across Japan and South Korea.

- Fastest Growing Region: Middle East & Africa is the fast-growing market projected to expand at a CAGR of approximately 7.8%, catalyzed by Saudi Arabia's NEOM megaproject, UAE urban tunneling programs, and critical mineral mining expansion across sub-Saharan Africa.

- Dominant Process Type: Wet-mix shotcrete dominates the process type category with approximately 62% share in 2026, driven by its superior material efficiency, lower rebound rates, and direct compatibility with robotic spraying systems specified in major infrastructure contracts globally.

- Fastest Growing System Type: Robotic spraying systems are the fastest-growing segment in the system type category, projected to expand at approximately 9.1% CAGR, propelled by safety mandates, productivity benchmarks, and increasingly automated project specifications in tunneling and underground mining.

- Key Opportunity: The integration of robotics and automation in shotcrete delivery represents the most time-sensitive opportunity for market participants, as committed global tunnel pipelines are progressively locking mechanized application into multi-year contracts that reward early movers with durable competitive positioning.

Market Dynamics

Drivers - Accelerating Global Infrastructure Investment and Tunnel Construction Activity

Large-scale infrastructure investment programs across key economies are creating structural, long-term demand for shotcrete, making this one of the most durable and contract-backed demand drivers in the market. The U.S. Infrastructure Investment and Jobs Act allocated US$ 1.2 trillion for roads, bridges, transit, and tunnels, establishing a committed federal spending pipeline that directly underpins domestic shotcrete consumption through the late 2020s.

Simultaneously, the European Union's TEN-T network expansion continues to fund cross-border tunnel and rail corridor projects in Austria, Switzerland, Italy, and Spain, all of which rely on the New Austrian Tunnelling Method (NATM), a technique architecturally dependent on shotcrete for primary ground support.

In the Asia Pacific, China's 14th Five-Year Plan prioritizes metro network expansion across more than 30 cities, each requiring hundreds of cubic meters of shotcrete per kilometer of tunnel constructed. For market participants, this pipeline of committed, government-backed projects provides multi-year demand visibility largely insulated from economic cyclicality, strengthening the investment case for capacity expansion and long-term supply agreements with major contractors.

Rising Underground Mining Activity Linked to the Global Energy Transition

The global mining sector's structural shift toward deeper, mechanized underground operations is generating a durable and technically demanding demand stream for shotcrete, particularly in fiber-reinforced ground support and drift lining applications. As surface ore deposits are progressively depleted, mining operators across Australia, Canada, Chile, and South Africa are scaling up underground extraction of copper, lithium, cobalt, and nickel, the critical minerals underpinning the energy transition.

The International Council on Mining & Metals (ICMM) has consistently documented this deepening trend, and underground operations in hard rock environments require systematic shotcrete-based ground support that is operationally non-negotiable. The Global Battery Alliance projects that global lithium demand will increase by approximately 500% by 2050, creating sustained upstream pressure on mining output, and by direct extension, on shotcrete consumption per operational mine. For suppliers of specialized fiber-reinforced and rapid-setting shotcrete formulations, this mining-linked demand stream represents a structurally protected revenue pool that favors technical differentiation over commodity price competition.

Market Restraints

High Capital Costs of Advanced Equipment Limiting Adoption Among Smaller Contractors

The high upfront investment required for advanced wet-mix and robotic shotcrete systems remains a major restraint for small and mid-sized contractors. Fully equipped robotic spraying systems can cost more than US$ 500,000, while additional expenses related to maintenance, spare parts, operator training, and logistics further increase total ownership costs. Many smaller contractors lack the financial capacity to adopt such technologies, limiting their participation in large tunnel and infrastructure projects.

The American Concrete Institute has also highlighted that poorly trained operators can generate material waste rates of 15-20% and compromise structural quality. As a result, larger contractors with stronger financial resources continue to dominate major infrastructure contracts, reinforcing market concentration and creating barriers for new entrants.

Rebound Waste and Escalating Environmental Compliance Requirements

Material rebound during shotcrete application is becoming a growing operational and environmental challenge for market participants. In dry-mix shotcrete processes, rebound waste typically ranges between 15% and 35% of applied material, according to the European Federation of National Associations of Concrete. This not only increases material costs but also creates significant waste disposal burdens, especially in tunnels and underground construction sites.

Environmental regulations across the European Union, Australia, and Canada are becoming stricter regarding construction waste management and sustainability reporting. Contractors operating under ISO 14001 environmental standards are facing higher compliance costs and tighter environmental performance expectations during project bidding. These pressures are increasing demand for low-rebound formulations and precision spraying technologies, requiring continuous R&D investment from manufacturers and suppliers.

Opportunities - Robotic and Automated Shotcrete Application as a Differentiated Commercial Platform

The growing integration of robotics, automation, and real-time monitoring technologies is creating a major commercial opportunity in the shotcrete and sprayed concrete market. Automated shotcrete systems equipped with AI-assisted nozzle positioning, remote-control operation, and real-time thickness monitoring can reduce material rebound losses by nearly 30% compared to manual application methods while significantly improving worker safety in confined underground environments.

Large tunnel and mining infrastructure projects across Scandinavia, Australia, and Southeast Asia are increasingly specifying robotic spraying systems as mandatory project requirements due to stricter safety and quality standards.

As governments accelerate tunnel construction and underground infrastructure investments globally, companies developing proprietary robotic spraying technologies and automated application platforms are expected to secure long-term contracts, premium pricing advantages, and stronger competitive differentiation in high-value infrastructure projects.

Fiber-Reinforced Shotcrete for Seismic Retrofit and Climate-Resilient Infrastructure

Increasing seismic activity, aging infrastructure, and climate-related structural stress are creating strong demand for fiber-reinforced shotcrete systems, particularly synthetic fiber-based formulations with enhanced durability and crack resistance. Regulatory frameworks such as ACI 318, Eurocode 8, and ASTM C1550 increasingly recognize fiber-reinforced sprayed concrete for tunnel rehabilitation, seismic retrofitting, and slope stabilization applications.

Countries including Japan and South Korea have introduced long-term seismic upgrade programs for underground transport and utility infrastructure, generating sustained procurement demand for advanced shotcrete materials. Fiber-reinforced formulations also provide improved corrosion resistance and post-crack ductility in harsh operating conditions, making them highly suitable for critical infrastructure projects. Suppliers with integrated portfolios covering accelerators, synthetic fibers, and technical application support are positioned to benefit most from this performance-driven infrastructure investment cycle.

Category-wise Analysis

Process Type Insights

Wet-mix shotcrete commands approximately 62% of the global market by process type in 2026, a dominant position sustained by its measurably superior material efficiency, more precise water-to-cement ratio control, and direct compatibility with the robotic and mechanized application systems that large-scale infrastructure and mining contractors now prefer. The wet-mix process enables tighter quality management over hardened concrete strength, reducing variability that would be unacceptable in structural tunnel lining applications governed by ASTM C1604 and EN 14487 standards.

The American Shotcrete Association (ASA) consistently benchmarks wet-mix processes as achieving materially lower rebound rates on high-output projects, making them the default specification in major tunneling contracts globally. Dry-mix shotcrete, while holding a smaller share in 2025, is forecast to be the fastest-growing process type through 2033, driven by its lower equipment cost, superior portability, and operational suitability for remote mining applications, repair works, and geographies where logistics constraints make wet-mix delivery systems impractical.

System Type Insights

Manual spraying systems account for approximately 58% of the global market in 2026, retaining leadership through their significantly lower capital cost, operational flexibility across project scales, and overwhelming dominance in repair, maintenance, and small-to-mid-scale construction segments in cost-sensitive markets. The installed base of manual equipment is extensive across South and Southeast Asia, Latin America, and Sub-Saharan Africa, where the majority of contractors operate without the capital or operational scale to justify robotic system investment.

Robotic spraying systems represent the fastest-growing segment in this category, expanding at an estimated CAGR of approximately 9.1% through 2033, as safety regulations in developed markets and productivity benchmarks in large tunneling and mining projects progressively establish automated application as a contract specification requirement. The International Tunnelling Association and leading global tunneling contractors are actively advancing robotic shotcrete as standard practice, a shift that will structurally reshape system type mix over the forecast period.

Reinforcement Type Insights

Steel fiber-reinforced shotcrete holds the leading position in the reinforcement type category, accounting for approximately 44% of the global share in 2026, underpinned by its long-established performance credentials in underground construction, tunnel lining, and slope stabilization applications where high tensile strength and impact energy absorption are structurally mandated. Steel fibers, typically hooked-end or corrugated profiles conforming to ASTM A820 or EN 14889-1, provide post-crack toughness and ductility that meet the structural load specifications of major tunneling and mining projects, and their endorsement by leading structural engineering consultancies has entrenched procurement patterns among large contractors.

Synthetic fiber-reinforced shotcrete is the fastest-growing reinforcement segment benefiting from a high adoption in seismic retrofit projects, marine and coastal infrastructure, where steel corrosion is structurally disqualifying, and sustainability-driven specifications that favor non-metallic reinforcement in LEED-aligned construction programs. Suppliers, including Sika AG and GCP Applied Technologies, are actively expanding synthetic fiber product lines to capture this structural shift.

End-user Insights

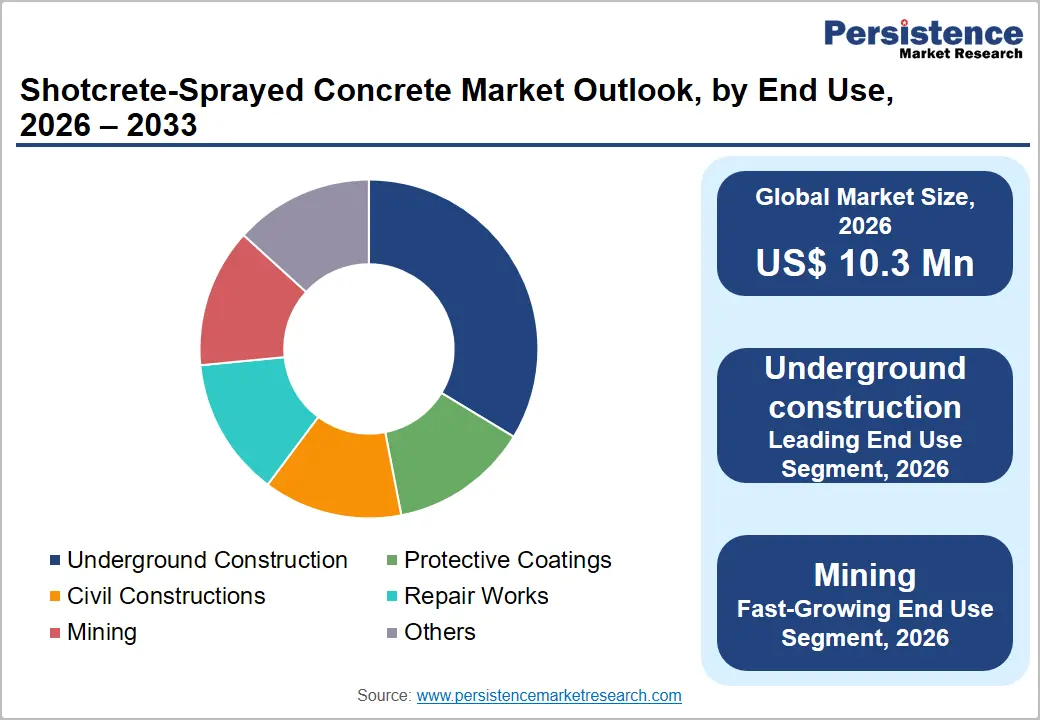

Underground construction represents the dominant end-use segment, accounting for approximately 35% of the total share in 2026, reflecting the fundamental dependency of tunnel and underground space construction on shotcrete as the primary lining and ground support material. The International Tunnelling Association (ITA) estimates that over 11,000 km of new tunnels were under active construction or advanced planning globally as of the mid-2020s, the overwhelming majority of which require shotcrete for both temporary primary support and permanent structural lining, a dual-use demand profile that maximizes volume per project.

Mining is the fastest-growing end-use segment over the 2026 - 2033 forecast period, driven by the intensification of underground critical mineral extraction that the energy transition demands. The World Mining Congress has highlighted the structural shift toward deeper underground mines where shotcrete-based ground support is operationally non-negotiable, and this demand stream is tightly linked to global decarbonization investment cycles that are politically and economically committed for decades.

Regional Insights

North America Shotcrete/Sprayed Concrete Market Trends and Insights

North America is likely to account for approximately 27% of the global shotcrete-sprayed concrete market in 2026, supported by a mature construction ecosystem, high adoption rates for automated spraying systems, and substantial federal investment in transportation and underground infrastructure. The U.S. Infrastructure Investment and Jobs Act has created a committed, multi-cycle spending program that is sustaining demand across both new tunnel construction and structural rehabilitation of aging highway and utility tunnels.

The region's regulatory environment, anchored by ACI and ASTM standards, favors technically superior, higher-margin shotcrete formulations, creating a premium pricing environment that rewards specialty chemical suppliers and integrated applicators. North America is increasingly a proving ground for robotic and digitally monitored shotcrete application, and market participants who align product and service offerings with the productivity and quality mandates of major infrastructure contractors will capture disproportionate contract value through the forecast period.

U.S. Shotcrete/Sprayed Concrete Market Size

The U.S. represents approximately 80% of North America's shotcretes-sprayed concrete market, driven by federally funded tunnel, bridge slope stabilization, and transit infrastructure programs alongside active underground mining operations in western states, including Nevada, Arizona, and Colorado. The U.S. Army Corps of Engineers and state departments of transportation are among the largest institutional procurers, specifying wet-mix shotcrete for slope reinforcement and tunnel rehabilitation contracts.

With the infrastructure bill spending cycle accelerating toward peak project execution between 2026 and 2030, the U.S. market is positioned to maintain above-regional-average growth momentum throughout the forecast period.

Europe Shotcrete/Sprayed Concrete Market Trends and Insights

Europe accounted for approximately 24% of the global shotcrete-sprayed concrete market in 2026, with activity concentrated in Germany, Austria, Norway, Switzerland, and the U.K., countries with active tunnel infrastructure programs and globally leading construction chemistry industries. The New Austrian Tunnelling Method (NATM), developed in Europe and adopted as the dominant tunneling technique worldwide, is inherently dependent on shotcrete for sequential excavation support, anchoring regional demand.

The EU Green Deal and climate resilience infrastructure programs are generating additional demand for repair-grade and low-carbon shotcrete systems as aging infrastructure assets enter mandatory rehabilitation cycles. Regulatory harmonization under Eurocode standards and EN 14487 for sprayed concrete provides consistent quality benchmarks that favor established specialty chemical suppliers with deep European market knowledge.

Germany Shotcrete/Sprayed Concrete Market Size

Germany commands the largest country-level share in Europe, representing approximately 22% of the regional market, sustained by an engineering-intensive construction sector and active tunnel and underground infrastructure programs under Deutsche Bahn and the federal Autobahn GmbH network. The country's global leadership in construction chemistry, anchored by firms including Master Builders Solutions (MBCC Group) and the European operations of Sika AG, ensures robust domestic supply innovation and continued advancement in admixture-enhanced, low-rebound shotcrete formulations.

Germany's market trajectory will remain structurally supported through 2033 as rail decarbonization investment drives new tunnel construction along strategic European freight and passenger corridors.

U.K. Shotcrete/Sprayed Concrete Market Size

UK accounts for approximately 14% of the European shotcrete market, driven significantly by the HS2 high-speed rail tunnel program and the Thames Tideway sewer tunnel, two of the largest civil shotcrete consumers in Western Europe, alongside repair demand from an aging road tunnel stock and underground utility network. The volume commitment of HS2's tunneling works through the late 2020s provides the U.K. market with a structurally supported demand floor largely insulated from short-term economic fluctuation. As HS2 construction progresses through peak excavation phases during 2026-2029, the U.K. is likely to outperform the European regional average growth rate.

France Shotcrete/Sprayed Concrete Market Size

France represents approximately 12% of the European shotcrete-sprayed concrete market, supported by tunnel maintenance requirements along the Alpine road and rail corridor, ongoing urban metro expansion under the Grand Paris Express program, the largest urban transit infrastructure project in Europe, and slope stabilization works in mountainous southern and eastern regions. The Grand Paris Express, involving over 200 km of new metro tunnels in and around Paris, has been a multi-year structural demand driver for wet-mix and fiber-reinforced shotcrete. France's market through 2033 will be characterized by growing repair and retrofit activity as infrastructure built in the mid-to-late 20th century enters its maintenance lifecycle.

Asia Pacific Shotcrete/Sprayed Concrete Market Trends and Insights

Asia Pacific dominates the global shotcrete market with approximately 36% share in 2026, powered by the world's most active construction economies, China, India, Japan, and South Korea, all of which are executing substantial underground and tunnel infrastructure programs. China accounts for the single largest country-level share within the region, driven by metro network expansion in more than 30 cities, high-speed rail tunnel construction through mountainous terrain, and hydropower project development in the Himalayan and southwestern provinces.

Asia Pacific is the fast-growing market over the forecast period, as infrastructure gaps in India, Vietnam, Indonesia, and Bangladesh create greenfield tunnel and underground construction demand at a scale and execution velocity that no other region matches. Companies scaling in Asia Pacific must navigate market fragmentation, local pricing competition, and diverse regulatory standards, but the structural demand runway is unparalleled globally.

India Shotcrete/Sprayed Concrete Market Size

India accounts for approximately 18% of the Asia Pacific shotcrete market and is among the fastest-growing country-level markets globally, driven by the PM Gati Shakti National Master Plan which prioritizes multimodal infrastructure including highways, metro rail, and strategically critical mountain tunnel corridors through the Himalayas and Western Ghats. The National Highways Authority of India (NHAI) is executing an unprecedented volume of hill tunnel projects, each requiring intensive wet-mix and fiber-reinforced shotcrete for primary support and permanent lining. India's market is expected to outpace Asia Pacific regional averages through 2033, supported by sustained government capital expenditure and a construction sector increasingly adopting technically advanced shotcrete formulations.

Japan Shotcrete/Sprayed Concrete Market Size

Japan represents approximately 15% of the Asia Pacific's shotcrete-sprayed concrete market, with demand anchored by the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) mandate for systematic seismic inspection and structural retrofitting of road and rail tunnels exceeding 30 years of age, a program covering thousands of kilometers of aging underground infrastructure.

The country's technically demanding procurement environment strongly favors premium fiber-reinforced formulations and precision robotic application equipment, creating a high-margin market niche that rewards specialist suppliers. New Shinkansen extensions and urban underground utility upgrades in Tokyo and Osaka provide additional demand alongside the repair-driven baseline, giving Japan a stable, multi-source demand profile through 2033.

South Korea Shotcrete/Sprayed Concrete Market Size

South Korea accounts for approximately 10% of the Asia Pacific shotcrete market, driven by urban underground infrastructure expansion in Seoul and its metropolitan area, alongside ongoing expressway tunnel construction in the country's mountainous central corridor. The Korean New Deal and successive infrastructure stimulus programs have accelerated underground construction project starts since 2022, and South Korea's advanced construction sector, characterized by early adoption of robotic spraying systems and digital quality management, positions the country as a regional benchmark for mechanized shotcrete application.

South Korea's technology adoption patterns have historically diffused to broader Southeast Asia, making it a strategic market indicator for regional automation uptake trends.

Competitive Landscape

The global shotcrete-sprayed concrete market demonstrates a moderately consolidated structure where competition is driven more by technical capabilities and engineering support than by production scale alone. Leading participants focus on advanced admixture formulations, fiber-reinforced systems, accelerators, and integrated application solutions tailored for complex tunnel, mining, and infrastructure projects.

Equipment manufacturers are increasingly investing in robotic spraying technologies, automated pumping systems, and materials compatibility engineering to strengthen competitive differentiation and improve operational efficiency. A major strategic trend across the market is the expansion of application engineering and technical consulting services alongside product supply, helping companies build long-term contractor relationships and higher switching costs.

Regional manufacturers compete primarily through localized production, cost competitiveness, and distribution strength in emerging infrastructure markets. However, strict certification standards, long infrastructure project qualification cycles, and rising technical performance expectations continue to create significant entry barriers for new market participants.

Key Developments

- March, 2024: Sika AG announced an expansion of its shotcrete admixture production capacity at its Swiss manufacturing facility, targeting rising demand from European and Middle Eastern tunnel and underground construction projects, reinforcing its position as the leading specialty chemicals supplier in the sprayed concrete segment.

- September, 2024: Putzmeister unveiled its next-generation robotic shotcrete spraying system featuring integrated AI-based layer thickness monitoring and remote operation capability, engineered for large-scale tunnel construction in Australia and Scandinavia.

- January, 2023: Master Builders Solutions (MBCC Group) launched a new line of low-carbon shotcrete accelerators developed in collaboration with ETH Zurich, targeting EU Green Deal-aligned infrastructure projects requiring reduced embodied carbon in sprayed concrete lining systems.

Companies Covered in Shotcrete/Sprayed Concrete Market

- Putzmeister

- Shotcrete Technologies, Inc.

- Meta Therm Furnace Pvt. Ltd

- REED

- Sika AG

- Master Builders Solutions (MBCC Group)

- Chembond Construction Chemicals Limited

- Heidelberg Materials (formerly Heidelberg Cement)

- GCP Applied Technologies

- The Euclid Chemical Company

- The QUIKRETE Companies

- CEMEX S.A.B de C.V

- Normet Group

- Mapei S.p.A

- Holcim Group

- CHRYSO Group

Frequently Asked Questions

The global shotcrete/sprayed concrete market is projected to reach US$ 10.3 billion in 2026.

The market is driven by rising tunnel infrastructure investment, expanding underground mining activity, and growing adoption of mechanized shotcrete systems.

Asia Pacific leads the market with around 36% share in 2025 due to extensive tunnel, metro, and infrastructure construction activities across China, India, Japan, and South Korea.

Robotic and automated shotcrete application systems represent the largest growth opportunity due to improved safety, reduced material rebound, and increasing use in tunnel projects.

Major companies include Sika AG, Putzmeister, Mapei S.p.A, Heidelberg Materials, and CEMEX.