- Advanced Materials

- Geogrids Market

Geogrids Market Size, Share, and Growth Forecast 2026–2033

Geogrids Market by Product Type (Uniaxial, Biaxial, Multiaxial), Material (HDPE, PP, Polyester), Application (Road Construction, Railroad, Soil Reinforcement, Others), and Regional Analysis, 2026–2033

Geogrids Market Size and Trends Analysis

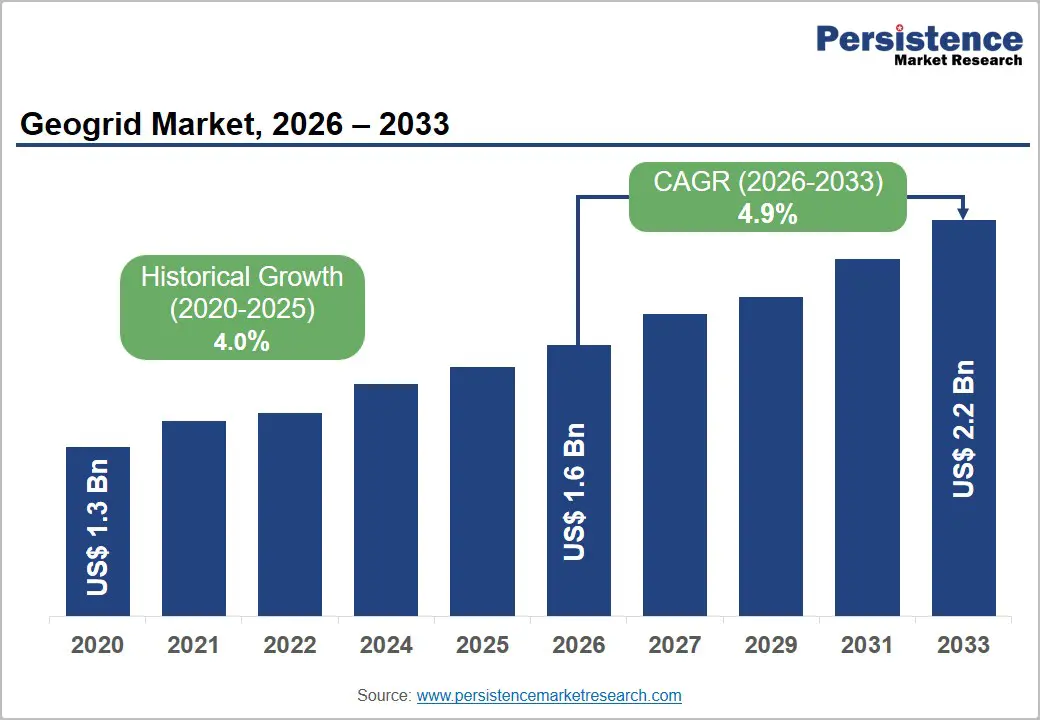

The global geogrids market size is likely to be valued at US$1.6 billion in 2026 and is projected to reach US$2.2 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by increasing investments in transportation infrastructure, urban development projects, and the growing need for cost-effective soil stabilization solutions. Geogrids are widely used in civil engineering applications to reinforce soil, improve load distribution, stabilize embankments, and enhance the durability of roads, railways, retaining walls, and other infrastructure assets. By creating a strong mechanical interlock with surrounding fill materials, geogrids efficiently transfer tensile stresses and reduce the risk of deformation or structural failure. As governments worldwide continue to prioritize infrastructure modernization and urban expansion, demand for geogrids is expected to remain closely tied to long-term construction and transportation development activities.

Key Industry Highlights:

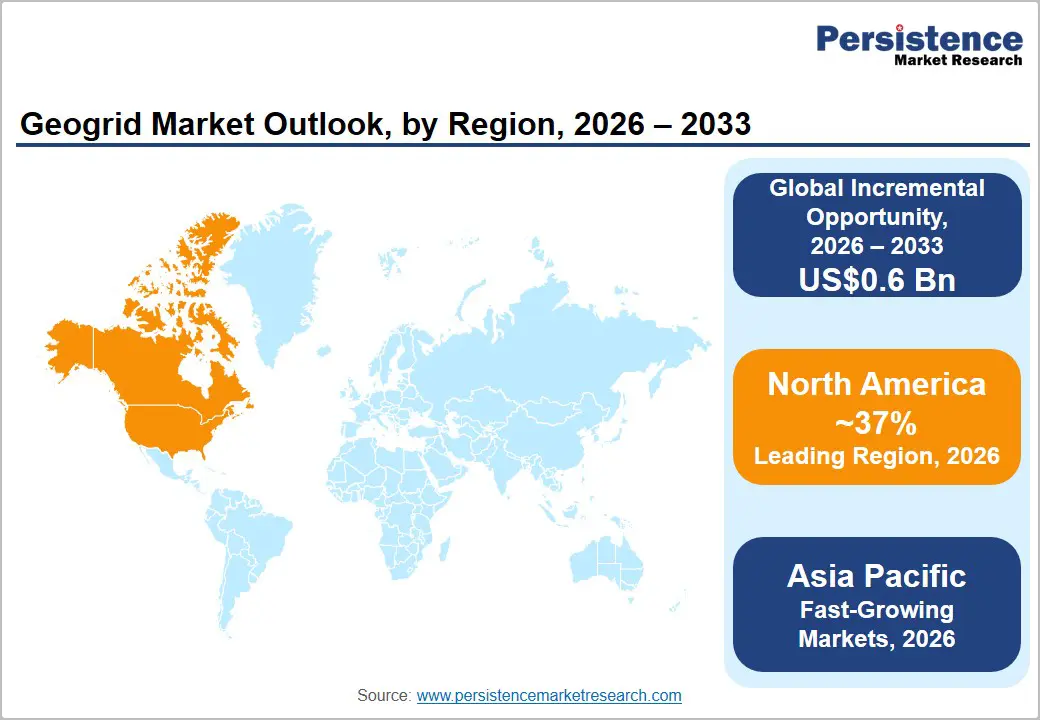

- Leading Region: North America is forecast to dominate with approximately 37% share in 2026, driven by the US$110 billion IIJA road and bridge program, FHWA Every Day Counts adoption initiative, and strong contractor familiarity with geogrid specifications.

- Fastest-growing Region: Asia Pacific is projected to grow at a CAGR of approximately 6.5% through 2033, led by India's National Infrastructure Pipeline highway programs, China's BRI export demand, and ASEAN infrastructure investment backed by ADB and World Bank.

- Dominant Product Type: Biaxial geogrids are anticipated to lead the product segment, commanding approximately 55% of the revenue share in 2026, favored for road base stabilization and pavement reinforcement due to bidirectional load distribution, established design standards, and demonstrated aggregate thickness reductions of 30–50%.

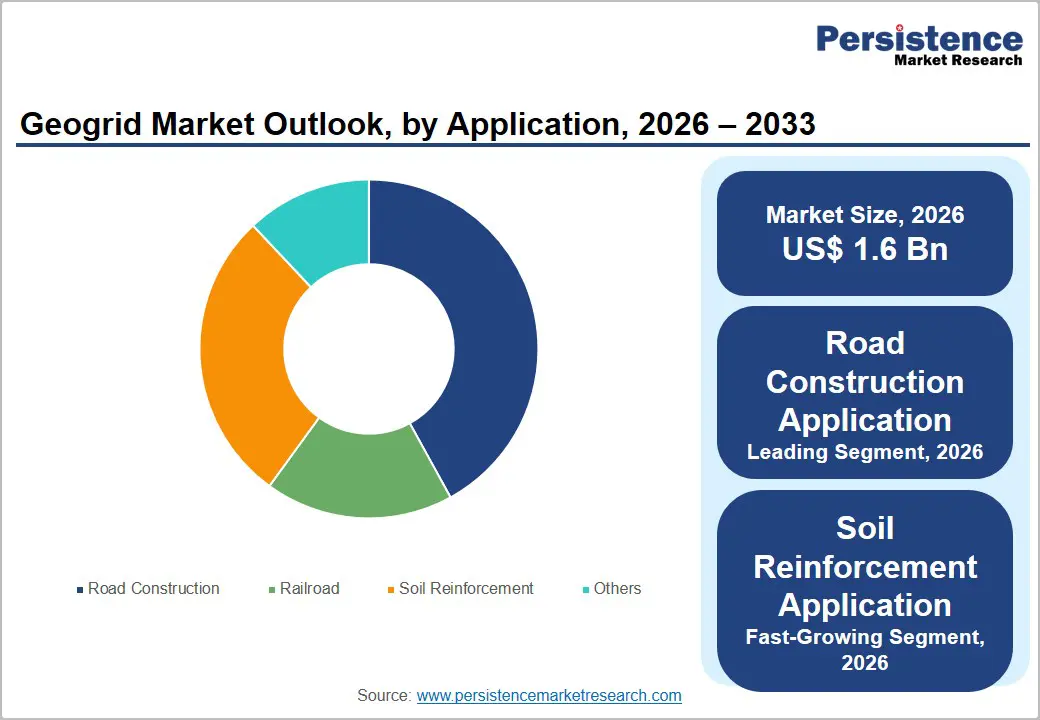

- Fastest-growing Application: Soil reinforcement applications are likely to be the fastest-growing end-use at an estimated CAGR of ~6.5% through 2033, driven by MSE retaining walls, steep slope stabilization, and the adoption of geogrids in green infrastructure projects meeting LEED and BREEAM standards.

- Key Market Opportunity: Emerging markets in Sub-Saharan Africa and Southeast Asia present the largest untapped geogrid volume opportunity, supported by AfDB PIDA and World Bank road programs targeting Africa's US$130–170 billion annual infrastructure gap, with geogrid stabilization ideally suited to challenging tropical subgrade conditions.

- Sustainability Trend: The increasing demand for recycled-content PET geogrids, driven by the EU Green Deal and public procurement Environmental Product Declaration (EPD) requirements, is creating new opportunities for product innovation. Leading manufacturers are focusing on developing geogrids with over 70% recycled polymer content and verified lifecycle carbon credentials.

DRO Analysis

Driver - Rising Global Infrastructure Investment and Road Construction Activity

Infrastructure development is the single most powerful demand driver for geogrids. The World Bank estimates that developing countries alone require over US$836 billion annually in infrastructure investment to support economic growth. In the U.S., the IIJA channels US$110 billion specifically to roads, bridges, and major infrastructure projects over five years, directly stimulating geogrid demand for road base stabilization and embankment reinforcement.

In India, the National Infrastructure Pipeline (NIP) targets US$1.4 trillion in infrastructure spending through 2025, with the Ministry of Road Transport and Highways awarding over 10,500 km of national highway contracts in FY 2023–24 alone. Geogrids used in road construction reduce aggregate thickness requirements by 30–50% per published ASTM International guidelines, delivering cost and material savings that accelerate adoption among cost-conscious infrastructure contractors globally.

Restraint - Competition from Alternative Ground Reinforcement Technologies

Geogrids face competitive substitution pressure from alternative ground improvement techniques, including geotextiles, geocells, deep soil mixing, and vibro-compaction, each suited to specific ground conditions and load requirements. The International Geosynthetics Society (IGS) has documented growing use of geotextile-geogrid composites that can partially displace standalone geogrid applications.

In soft ground conditions, deep foundation techniques may be technically preferred, reducing the geogrid addressable market in certain geologies. Lack of standardized design guidelines in some emerging markets leads engineers to default to familiar conventional methods, inhibiting geogrid adoption even where it would be economically and technically superior.

Opportunity - Expansion in Emerging Markets Driven by Urbanization and Road Network Development

Emerging economies across Sub-Saharan Africa, Southeast Asia, and Latin America represent the largest untapped volume opportunity for geogrid manufacturers. Africa's road network deficit is significant: The African Development Bank (AfDB) estimates that only 34% of Africa's rural population lives within 2 km of an all-season road, with the continent requiring over US$130–170 billion annually in infrastructure investment.

Multilateral development bank programs, including the AfDB's Programme for Infrastructure Development in Africa (PIDA) and World Bank transport projects, are channeling capital into road construction in geologies and climates where geogrid stabilization is highly effective. Companies that build local distribution partnerships and offer performance-based design support will be best positioned to capture this structural long-term opportunity in high-growth frontier markets.

Category-wise Analysis

Product Type Insights

Biaxial geogrids are projected to dominate the global product type segment, accounting for approximately 55% of the total product type in 2026. Biaxial geogrids reinforce two perpendicular directions, length and width, making them the preferred choice for road base stabilization, parking lot construction, and general ground reinforcement applications where omnidirectional load distribution is required.

Multiaxial geogrids are estimated to register the fastest-growing product type, advancing at an estimated CAGR of approximately 6% through 2033, driven by their superior aggregate interlock geometry and growing adoption in premium pavement reinforcement projects. Tensar International's TriAx® multiaxial geogrid has demonstrated 40% aggregate reduction in published field trials.

Material Insights

High-density polyethylene (HDPE) is the leading material segment, commanding approximately 48% of total material revenue in 2026. HDPE geogrids deliver exceptional resistance to chemical degradation, UV exposure, and biological attack, maintaining structural integrity across a wide temperature range, properties critical for road and rail applications in harsh climatic conditions.

Polyester (PET) geogrids are likely to be the fastest-growing material segment, growing at an estimated CAGR of approximately 5.8% through 2033, driven by their high tensile strength-to-weight ratio and suitability for steep-slope mechanically stabilized earth (MSE) wall applications where HDPE's creep characteristics may be a constraint.

Application Insights

Road construction is projected to dominate the application segment, accounting for approximately 52% of the total application share in 2026. Geogrids are routinely specified for subgrade stabilization, base reinforcement, and pavement overlay in both new highway construction and rehabilitation projects. HUESKER's Fortrac® geogrid systems have been widely deployed for steep slope stabilization, embankment reinforcement, and geosynthetic-reinforced soil (GRS) retaining structures, enabling the construction of stable slopes and retaining walls with reduced environmental impact and improved land utilization.

Soil reinforcement encompassing MSE retaining walls, steep slope stabilization, and embankment reinforcement is the fastest-growing application at an estimated CAGR of ~6.5% through 2033, driven by urban expansion into challenging topographies and the growing use of geogrids in green infrastructure and living wall systems that comply with LEED and BREEAM sustainable construction standards. In March 2025, GO Transit selected Solmax's MIRAGRID® XT geogrids for the Lakeshore West Line rail expansion project in Ontario, Canada.

Regional Insights

North America Geogrids Market Trends

North America is projected to dominate, capturing around 37% of the global market share in 2026. Growth is driven by substantial investments in highway rehabilitation, transportation infrastructure, retaining walls, and pavement reinforcement projects across the region. The widespread adoption of geosynthetic solutions to improve soil stability and extend infrastructure lifespan further supports demand.

U.S. Geogrids Market Trends

The U.S. is expected to command approximately 82% of the regional market share in 2026. Its dominance is attributed to large-scale federal and state infrastructure programs, extensive road and bridge rehabilitation activities, and high adoption of geogrids in transportation and civil engineering projects. Strong domestic manufacturing capabilities and continuous investments in resilient infrastructure further support market growth.

Canada Geogrids Market Trends

Canada is anticipated to account for 18% of the regional market share in 2026. Market growth is driven by increasing investments in transportation networks, mining infrastructure, and road construction in remote and cold-climate regions where soil stabilization is critical. Rising use of geogrids in sustainable infrastructure development and erosion control projects also contributes to demand.

Europe Geogrids Market Trends

Europe is estimated to be the second-largest regional market, accounting for approximately 27% of the global market share in 2026. The region's leadership is driven by extensive transportation infrastructure modernization, stringent sustainability regulations, and widespread adoption of geosynthetics in road, rail, and retaining wall applications. Strong engineering standards and the presence of major geogrid manufacturers further support market growth.

Germany Geogrids Market Trends

Germany is estimated to hold approximately 24% of the regional market share in 2026, making it the leading country in the region. The country's dominance is supported by continuous investments in highway rehabilitation, railway upgrades, and sustainable construction projects. Germany also benefits from the presence of leading geosynthetics manufacturers and advanced civil engineering practices that encourage geogrid adoption.

U.K. Geogrids Market Trends

The U.K. is expected to account for approximately 16% of the regional market share in 2026. Growth is driven by ongoing transportation infrastructure improvements, road maintenance programs, and increasing use of geogrids in embankment stabilization and pavement reinforcement projects. Government initiatives focused on sustainable and long-lasting infrastructure solutions continue to support market expansion.

Asia Pacific Geogrids Market Trends

Asia Pacific is likely to be the fastest-growing regional market for geogrids. The region's dominance is driven by rapid urbanization, large-scale transportation infrastructure development, expanding construction activities, and increasing investments in railways, highways, and smart cities. Rising demand for soil stabilization and ground reinforcement solutions in emerging economies further supports market growth.

China Geogrids Market Trends

China is projected to hold approximately 50% of the regional market share in 2026, making it the leader in the region. Its dominance is supported by massive investments in highways, high-speed rail networks, urban infrastructure, and land development projects. The presence of a large domestic manufacturing base and continuous government spending on infrastructure modernization further strengthens demand for geogrids.

Japan Geogrids Market Trends

Japan is projected to account for approximately 15% of the market share in 2026. The country's market is driven by extensive use of geogrids in earthquake-resilient infrastructure, slope stabilization, retaining wall construction, and transportation network maintenance. Strong engineering standards and ongoing investments in infrastructure rehabilitation continue to support geogrid adoption across the country.

Competitive Landscape

The global geogrids market is moderately consolidated, with a select group of multinational manufacturers commanding significant combined revenue share. Tensar International, TenCate Geosynthetics, Huesker, Maccaferri, and NAUE are among the global technology leaders, competing on the basis of proprietary product designs, long-term performance data, and technical design service capabilities.

Key competitive differentiators include proprietary geogrid geometries such as Tensar's TriAx® technology, engineering software tools for project-specific design optimization, and certified third-party long-term performance data that supports contractor and engineer specification confidence. Emerging trends include investments in recycled polymer geogrid product lines, digitally integrated design services, and expansion into high-growth emerging markets through local manufacturing and distribution partnerships.

Key Industry Developments:

- In February 2026, NAUE supplied approximately 150,000 square meters of Combigrid® and Secugrid® geogrids for a major port infrastructure development project linked to renewable energy expansion. The company supported large-scale ground stabilization and coastal infrastructure construction through its high-performance geogrid reinforcement systems, demonstrating the growing adoption of advanced geosynthetic solutions in critical infrastructure projects.

- In June 2025, Solmax launched its new Performance Materials platform and integrated the legacy businesses of TenCate Geosynthetics and Propex into a unified operating structure. Through this initiative, the company expanded its global footprint, strengthened its technical textiles and geosynthetics portfolio, and enhanced its ability to deliver broader product development capabilities for infrastructure and civil engineering applications.

Companies Covered in Geogrids Market

- Huesker

- TenCate Geosynthetics

- Strata Systems

- Maccaferri

- NAUE

- CLIMAX SYNTHETICS

- Veer Plastics

- Pietrucha Group

- CTM Geosynthetics

- TENAX

- BOSTD Geosynthetics

- Tensar

Frequently Asked Questions

The global geogrids market is estimated at US$1.6 billion in 2026.

The geogrids market is primarily driven by large-scale global infrastructure investments and the growing adoption of geogrids in road and rail projects due to their ability to reduce aggregate usage, lower construction costs, and enhance structural performance.

The geogrids market is forecast to grow at a CAGR of 4.9% between 2026 and 2033.

Key opportunities include expanding infrastructure projects in Sub-Saharan Africa and Southeast Asia, alongside rising demand for sustainable, recycled-content geogrids that meet environmental procurement standards and low-carbon construction requirements.

The global geogrids market is characterized by the presence of several established manufacturers specializing in geosynthetic solutions. Key market participants include Tensar International, TenCate Geosynthetics, HUESKER, Maccaferri, NAUE, and Strata Systems.