- Electric Mobility

- Wireless Car Charging Market

Wireless Car Charging Market Size, Share, and Growth Forecast for 2025 - 2032

Wireless Car Charging Market by Charging Type (Static Wireless Car Charging, Dynamic Wireless Car Charging), Propulsion (Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs)), Power Supply Range (Up To 3.7 Kw, 3.8- 7.7 Kw, 7.8- 11 Kw, Above 11Kw), Technology (Inductive Charging, Hybrid-Inductive Resonance), and Regional Analysis for 2025 - 2032

Wireless Car Charging Market Share and Trends Analysis

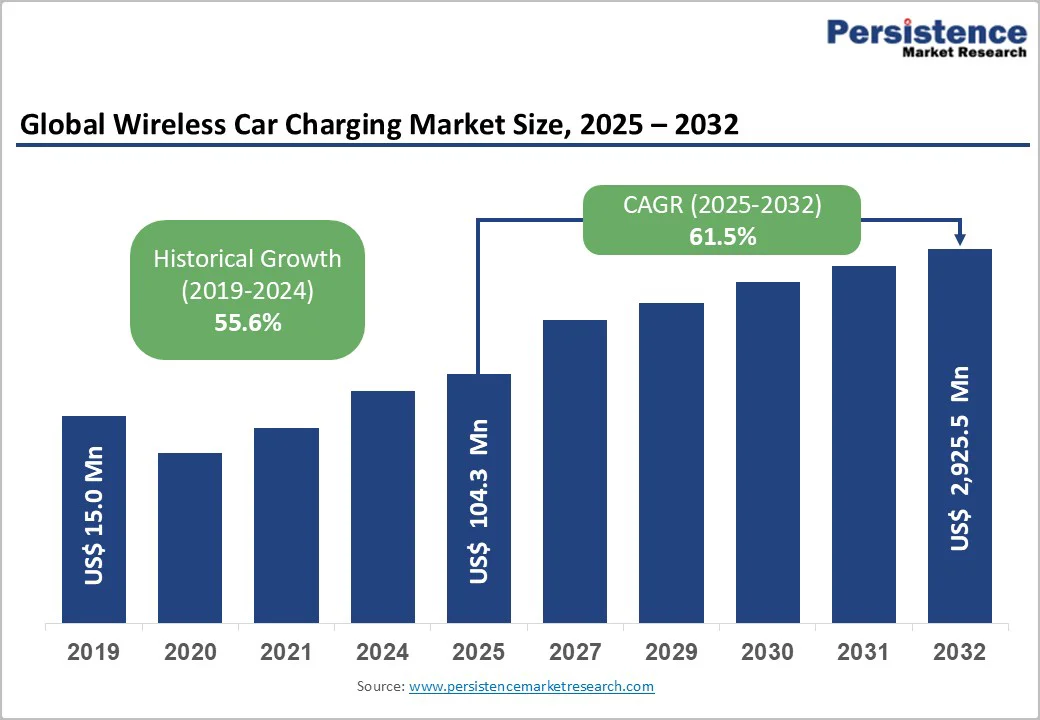

The global wireless car charging market size is likely to be valued at US$ 104.3 million in 2025, and is projected to reach US$ 2,925.5 million by 2032, growing at a CAGR of 61.5% during the forecast period 2025-2032. Tax credits for electric vehicles (EVs) under the Inflation Reduction Act are driving infrastructure expansion across residential, commercial, and public charging networks. Dynamic wireless charging pilots demonstrating in-motion vehicle charging on dedicated roadway corridors are expanding market opportunities beyond static charging.

Key Industry Highlights

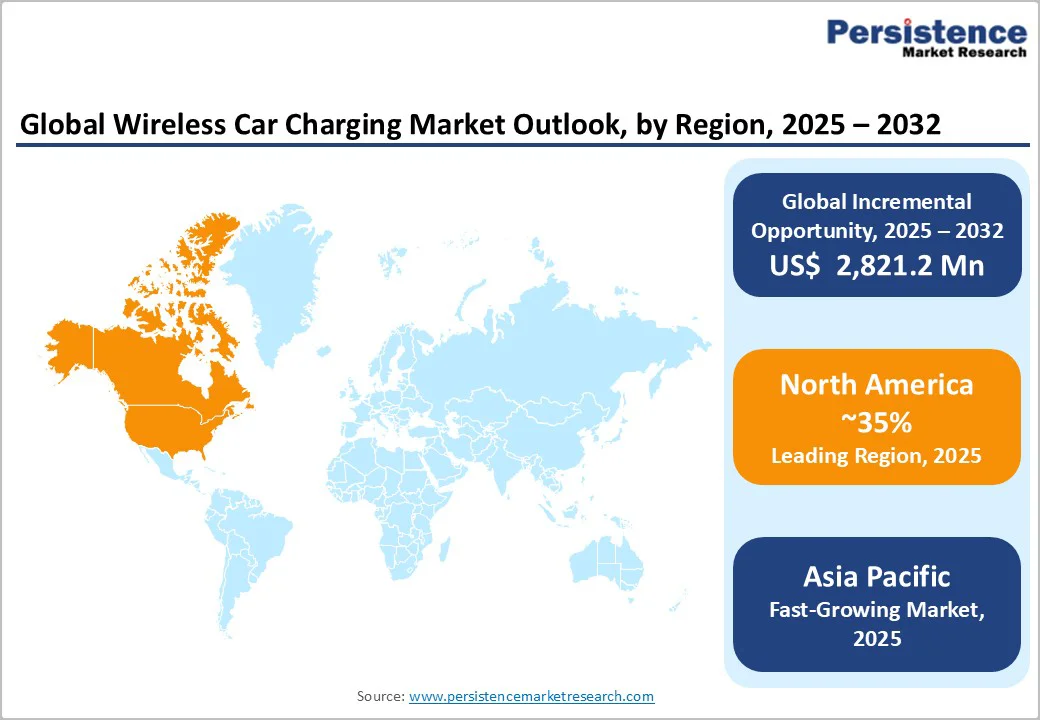

- Leading Region: North America leads with a 35% share in 2025, driven by early technology adoption, strong original equipment manufacturer (OEM) collaborations, and extensive EV infrastructure expansion across the U.S. and Canada.

- Fastest-growing Regional Market: Asia Pacific is the fastest-growing market, expanding at an exceptional 57.2% CAGR through 2032, fueled by China’s aggressive EV adoption policies.

- Dominant Charging Type: Static wireless charging dominates with a 65% market share in 2025, owing to its proven efficiency and deployment readiness.

- Leading Vehicle Type: Battery electric vehicles (BEVs) command 70% of market share, supported by global manufacturing priorities, zero-emission targets, and subsidy programs promoting long-range EVs.

- Fastest-growing Vehicle Type: Plug-in hybrid electric vehicles (PHEVs) grow at 16.3% CAGR through 2032, as they combine electric convenience with internal combustion reliability.

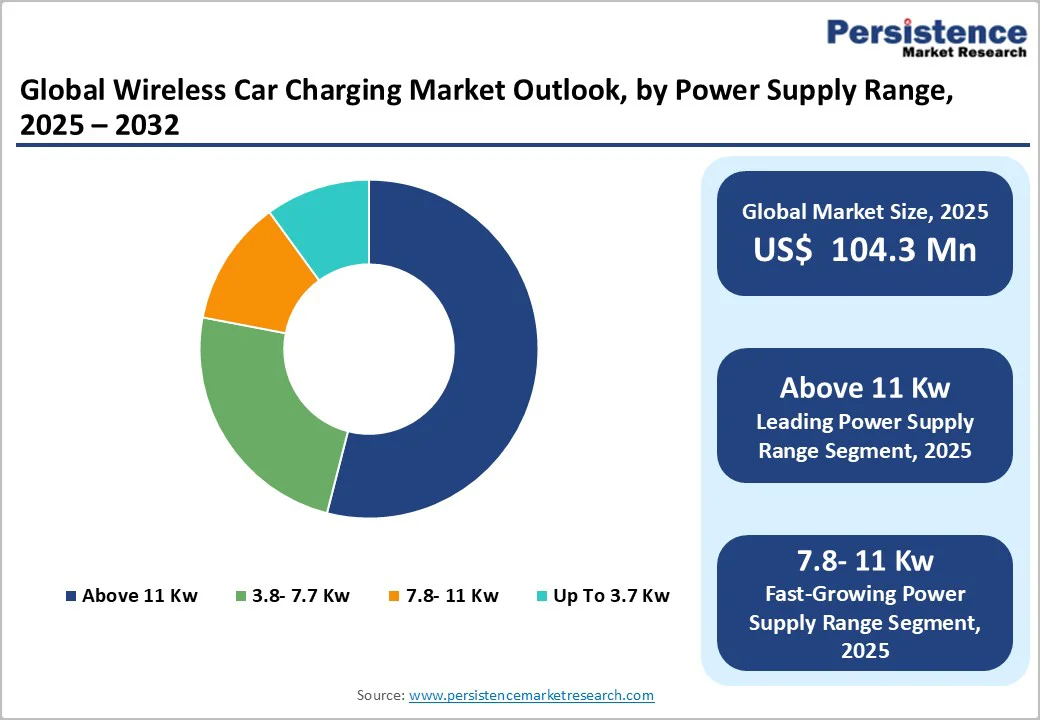

- Leading Power Supply Range: Systems rated above 11 kW hold 47.5% share, addressing commercial and fast-charging applications requiring higher energy throughput.

- Competitive Landscape: WiTricity leads with a strong patent portfolio acquired from Qualcomm Halo, while Tesla’s acquisition of Wiferion marks strategic entry into autonomous vehicle wireless charging.

| Key Insights | Details |

|---|---|

|

Wireless Car Charging Market Size (2025E) |

US$ 104.3 Mn |

|

Projected Market Value (2032F) |

US$ 2,925.5 Mn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

61.5% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

55.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Electric Vehicle Market Expansion and Government Incentives

EV adoption accelerating globally creates fundamental demand for convenient charging infrastructure, with wireless technology addressing critical usability barriers that drive adoption among hesitant consumers. Global EV sales surpassed 17 million units in 2024, representing nearly 20% of total vehicle sales, according to the International Energy Agency (IEA). For example, the U.S. Department of Energy earmarked US$ 7.5 billion specifically for national EV charging expansion including wireless infrastructure development. This policy-driven infrastructure expansion, combined with consumer demand for convenient charging solutions, establishes the foundation for wireless car charging market growth across automotive segments.

The publication of the SAE J2954 standardization framework for wireless power transfer has eliminated critical commercialization barriers by establishing comprehensive technical specifications and automated alignment methodologies that facilitate interoperability between diverse manufacturer platforms. This regulatory clarity has accelerated automotive manufacturer product development timelines, with leading brands announcing factory-equipped wireless charging models for near-term market entry. Global standards development initiatives through multiple international organizations provide regulatory confidence for infrastructure investment and supply chain optimization, enabling mass production at automotive scale while supporting both light-duty passenger vehicles and heavy-duty commercial fleet applications.

High Infrastructure Installation Costs and Capital Requirements

Dynamic wireless charging infrastructure deployment requires substantial capital investment that significantly exceeds traditional charging station expenses, constraining adoption in budget-constrained jurisdictions. Subsurface electromagnetic coil installation demands extensive civil engineering, electrical infrastructure upgrades, and coordination among multiple government agencies with fragmented decision-making authority. Retrofit applications converting existing roadways to wireless capability encounter substantial cost escalation due to traffic management requirements, property acquisition, and road surface replacement, making rapid geographic expansion economically challenging and limiting deployment to selective urban corridors as demonstrated by early pilot projects.

Consumer unfamiliarity with wireless charging technology and perception of it as a luxury feature rather than essential infrastructure constrains mass market adoption, particularly among price-sensitive segments that prioritize cost and speed over convenience. The limited deployment of public wireless charging infrastructure prevents most EV owners from gaining practical experience with the technology, disrupting the network effects necessary for organic adoption acceleration. Range anxiety concerns persist among consumers despite wireless charging capabilities, as insufficient infrastructure coverage fails to provide meaningful driving range extension for long-distance travel applications. Pre-standardization regulatory fragmentation across jurisdictions created market confusion regarding technology viability and future-proofing of infrastructure investments, delaying consumer confidence and market development.

Autonomous Vehicle Market Development and Robotaxi Deployment

Autonomous vehicle deployment models requiring hands-free operation without human drivers create unique demand for wireless charging infrastructure unavailable through traditional wired systems. Commercial autonomous shuttle services in airports, corporate campuses, and controlled environments require reliable wireless charging to enable continuous operational availability without human intervention, establishing a critical market segment distinct from conventional passenger vehicle applications. Vehicle-to-grid (V2G) integration enables autonomous EV fleets to provide grid stabilization services during peak demand periods, creating additional revenue streams that justify wireless infrastructure investment and enhance economic viability.

The rapidly urbanizing economies of China, India, and Southeast Asia are constructing new automotive infrastructure without legacy wired charging constraints, positioning wireless technology as the primary charging architecture. Large-scale provincial and municipal investment initiatives across these regions demonstrate the economic viability and strategic importance of wireless charging infrastructure at scale. Smart city initiatives across multiple municipalities globally incorporate IoT connectivity, renewable energy integration, and demand management systems that create favorable deployment environments for wireless charging infrastructure with grid optimization capabilities. Residential wireless charging adoption accelerates in emerging markets as consumer demand for convenient cable-free solutions aligns with urban apartment living patterns, enabling automated charging without resident action during off-peak hours.

Category-wise Analysis

Charging Type Insights

Static charging holds about 65% of the wireless car charging market revenue share in 2025, as a result of residential and workplace applications where vehicles remain parked for long durations. Supported by the SAE J2954 standard, this charging technology delivers more than 90% efficiency, matching wired Level 2 performance. Home garages and office parking lots increasingly adopt static systems for convenience and automated energy management aligned with electricity pricing.

On the other hand, dynamic wireless charging is the fastest-growing segment, expected to register an estimated 61.5% CAGR through 2032. Projects in Detroit, Tel Aviv, and Trondheim demonstrating in-motion charging viability are propelling the growth of this segment. Advances such as Chiba University’s AI alignment system and DOE–Oak Ridge’s 200 kW prototypes accelerate commercialization. Dynamic charging reduces battery size needs, extends range, and enables continuous charging for fleets, buses, and autonomous vehicles.

Propulsion Type Insights

BEVs dominate the wireless charging market with a 70% revenue share, supported by surging global EV sales surpassing 17 million units in 2024 and projected to reach 39 million by 2030. Major automakers such as Tesla, BMW, Volkswagen, and Audi integrate factory-installed wireless systems in next-generation BEV platforms, enabling automated, cable-free recharging ideal for autonomous mobility. Growing environmental awareness, government incentives, and falling battery costs further reinforce BEV leadership.

Plug-in hybrid electric vehicles represent the fastest-growing segment at 16.3% CAGR from 2025 to 2032, serving as a transition technology where charging infrastructure is developing. Luxury brands including BMW, Porsche, and Audi are adopting wireless charging for PHEVs, offering convenience, sustainability, and hybrid backup flexibility for corporate and premium consumers.

Power Supply Range Insights

The above 11 kW power supply segment dominates with a 47.5% the wireless charging market share in 2025, driven by commercial and fast-charging applications requiring rapid battery replenishment. High-power wireless solutions exceeding 50 kW cater to buses, delivery fleets, and port vehicles where downtime reduction directly improves operational efficiency. Three-phase 11 kW systems are widely adopted in Europe, offering faster charging without major infrastructure upgrades. Emerging 22+ kW systems enable 50% battery recharge within 10 minutes, addressing public charging limitations.

The 7.8–11 kW range is the fastest-growing segment, providing an optimal balance between charging speed and infrastructure cost. Ideal for residential, workplace, and light commercial use, this range benefits from SAE J2954 standardization and widespread OEM integration of 11 kW onboard chargers.

Regional Insights

North America Wireless Car Charging Market Trends

North America commands the dominant position in the wireless EV charging market, supported by accelerated growth rates that reflect strong government funding commitments, policy incentives, and a mature automotive technology ecosystem. In the U.S., the region's primary growth engine, the market benefits from strategic government support including substantial Department of Energy infrastructure funding earmarked specifically for wireless charging deployment. This financial backing combines with federal and state incentive programs, notably the Inflation Reduction Act's EV tax credits, building a comprehensive policy framework that encourages both infrastructure investment and consumer EV adoption.

Early-stage pilot projects across major metropolitan areas, particularly Detroit's wireless electric road initiative and California's planned urban corridors, validate technology feasibility and demonstrate government commitment to wireless infrastructure deployment. These projects serve as proof-of-concept installations that reduce regulatory uncertainty and provide operational experience to guide scaling efforts. Leading automotive manufacturers including Tesla, General Motors, and Ford are aggressively advancing wireless integration into production vehicles, with strategic acquisitions and partnerships accelerating development timelines. The establishment of the SAE J2954 standardization framework has also been instrumental in accelerating commercialization by enabling interoperability across diverse manufacturer platforms and reducing procurement complexity.

Europe Wireless Car Charging Market Trends

Europe is emerging as the second-largest regional market for wireless EV charging, attributable to stringent emissions regulations and comprehensive green mobility initiatives that prioritize environmental sustainability. The regional market growth reflects a distinct competitive advantage centered on premium automotive engineering capabilities, with luxury brands leading technology integration into next-generation vehicle platforms. European regulatory frameworks, particularly European Union (EU) sustainability mandates, create consistent policy pressure across member states to adopt eco-friendly transport infrastructure, establishing uniform technical requirements that encourage wireless charging deployment as part of broader decarbonization strategies.

Germany anchors the Europe wireless car charging market through its advanced automotive engineering ecosystem and strategic deployment of major urban and highway wireless charging initiatives. The country's engineering expertise and automotive supply chain depth position it as the regional innovation center, supporting both infrastructure development and vehicle integration efforts. The U.K. has also accelerated charging infrastructure expansion through collaborative research projects that advance dynamic on-road charging capabilities, with pilot installations such as Coventry's Dynacov project testing technology feasibility in real-world conditions. France and Spain are extending wireless charging adoption through their commitment to EU sustainability mandates, integrating wireless infrastructure into broader urban mobility strategies. These regional demonstrations validate wireless charging utility across diverse vehicle types and operational environments, supporting market expansion beyond private passenger vehicles.

Asia Pacific Wireless Car Charging Market Trends

Asia Pacific has emerged as the fastest-growing wireless EV charging regional market. Charting the growth trajectory of the market is the accelerating EV adoption rates across the region, policies prioritizing electrification and sustainability, and significant manufacturing scale advantages that enable cost-competitive production and deployment. These structural advantages position Asia Pacific as the leading market for wireless charging innovation, infrastructure investment, and technology commercialization. China commands market leadership, fueled by aggressive national EV targets and comprehensive infrastructure expansion initiatives. The country's strategic commitment to electrification, supported by extensive provincial infrastructure programs across Sichuan, Guangdong, and other major regions, establishes wireless charging as a core component of urban mobility infrastructure.

Japan is also contributing to the growth momentum of the regional market through its strengths in wireless charging technology innovation and export-oriented production capabilities. The country's advanced automotive engineering ecosystem and supply chain sophistication position Japanese manufacturers as key technology providers supporting regional and global wireless charging commercialization. At the same time, India has widened EV adoption through national electrification missions and smart infrastructure development programs that integrate wireless charging into broader urban development strategies.

Competitive Landscape

The global wireless car charging market structure is moderately consolidated, with a few global technology leaders setting core standards and controlling key intellectual property (IP), while a long tail of regional specialists and startups competes in niche applications. Large providers leverage extensive patent portfolios, deep OEM relationships, and proven deployments to anchor major passenger vehicle and commercial fleet programs, shaping technology roadmaps and influencing interoperability and standardization trends across the industry.

Alongside these leaders, companies focused on specific use cases, such as high-power depot and fleet charging, dynamic road systems, or region-specific integrations, are gaining ground by offering tailored solutions and flexible business models. This mix of dominant IP holders and agile innovators is driving rapid technical refinement, expanding from premium passenger cars into buses, logistics fleets, and smart city projects, while also intensifying competition around licensing, ecosystem partnerships, and long-term platform control in the global EV charging landscape.

Key Industry Developments

- In November 2025, WiTricity introduced advanced wireless EV charging solutions designed to modernize airport ground operations and improve fleet electrification. Their MR/1 900W wireless charging system supports a range of airport ground support equipment, providing safety by eliminating cable hazards, automatic charging for maximum uptime, all-weather reliability, and reduced maintenance due to no moving parts. The system is quick to install and charges vehicles as “fast” or “faster”, allowing airports to enhance operational efficiency, safety, and reduce total cost of ownership for their electric fleets.

- In September 2025, Porsche unveiled an optional wireless charging system for its all-new 2026 Cayenne Electric, making it the first vehicle in its lineup to offer inductive charging. The system delivers up to 11 kW of power with over 90% efficiency and starts charging automatically once the vehicle is parked above a floor plate in the garage. Integrated with the My Porsche app, it guides drivers to the optimal parking position using ultra-wideband technology and includes convenient features such as charging timers and preconditioning.

- In June 2025, WirelessCar, Blink Charging, and ChargeHub launched a Seamless Charging pilot program across the U.S. and Canada aimed at simplifying the EV charging experience. The initiative allows drivers to access Blink chargers with a single app registration via ChargeHub, eliminating the need for multiple apps or accounts. Using connected vehicle data, the system automatically starts charging and notifies drivers, creating a more convenient and frictionless public charging experience, especially for those without home charging access.

Companies Covered in Wireless Car Charging Market

- Qualcomm Technologies Inc.

- Evatran LLC

- WiTricity Corporation

- Momentum Dynamics Corp

- Toshiba Corporation

- Mojo Mobility Inc.

- HEVO Inc.

- Bombardier Inc

- TDK Corporation

- Denso Corporation

- ZTE Corporation

Frequently Asked Questions

The global wireless car charging market is projected to reach US$ 104.3 million in 2025.

Rising adoption of electric vehicles worldwide, combined with the growing need for convenient, automated, and cable-free charging solutions that enhance user experience and support autonomous mobility, is driving the market.

The market is poised to witness a CAGR of 61.5% from 2025 to 2032.

Tax credits for EVs, dedicated governmental funding for charging infrastructure, and dynamic wireless charging pilots demonstrating in-motion vehicle charging on roadway corridors are expanding market opportunities.

Qualcomm Technologies Inc., Evatran LLC, WiTricity Corporation, and Momentum Dynamics Corp are some of the key market players.