- Medical Devices

- Emergency Hospital Beds Market

Emergency Hospital Beds Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Emergency hospital beds market by Bed Type (Manual Beds, Semi-Electric Beds, Electric Beds), End-user (Blanched, Natural), by End-use (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and Regional Analysis from 2025 to 2032

Emergency Hospital Beds Market Share and Trends Analysis

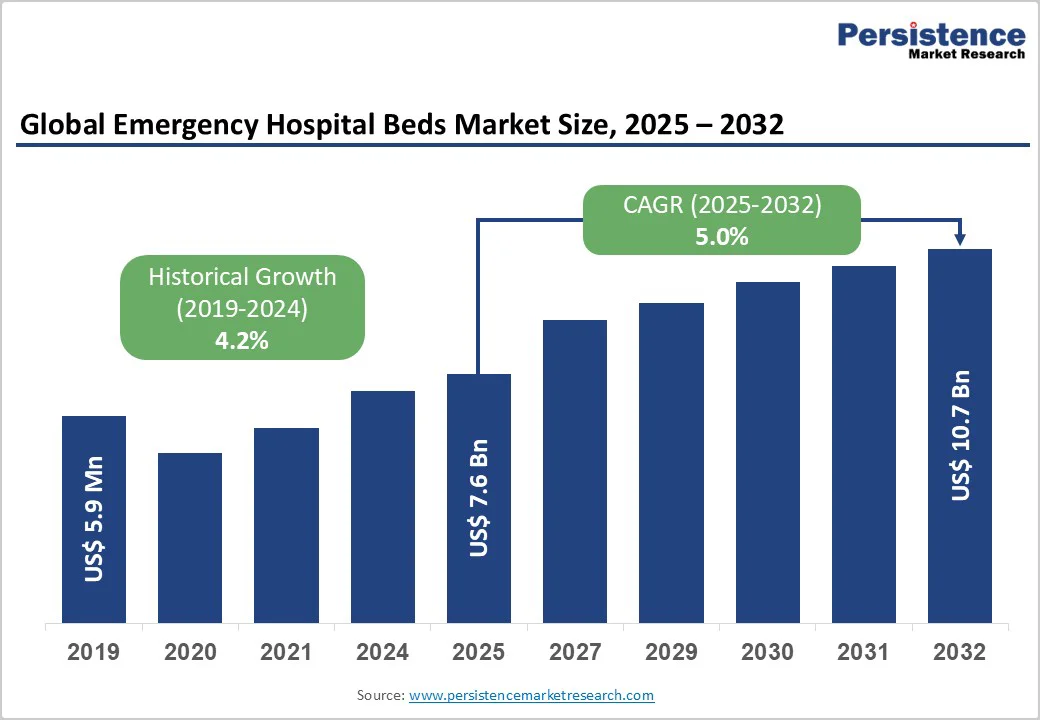

The global emergency hospital beds market size is valued at US$7.6 billion in 2025 and projected to reach US$10.7 billion at a CAGR of 5.0% during the forecast period from 2025 to 2032.

The global emergency hospital beds market is experiencing steady growth, driven by rising emergency and critical-care admissions, increasing hospital infrastructure development, and a growing preference for electrically actuated and smart beds with integrated monitoring systems.

Hospitals are investing in advanced beds to enhance patient care, improve workflow efficiency, and meet the needs of trauma and ICU units. The market includes manual, semi-electric, and fully electric beds, catering to different clinical settings such as ICUs, general wards, and emergency departments.

Key Industry Highlights:

- The emergency hospital beds market is projected to grow steadily, driven by increasing hospital admissions, aging populations, and rising critical-care needs.

- Hospitals (public and private) constitute the largest end-user segment, followed by specialty clinics and ambulatory surgical centers.

- Smart beds with integrated patient monitoring, IoT sensors, and automated adjustments are gaining traction.

- Electric beds offer automated adjustments for height, backrest, and leg positions, improving patient comfort and safety.

| Key Insights | Details |

|---|---|

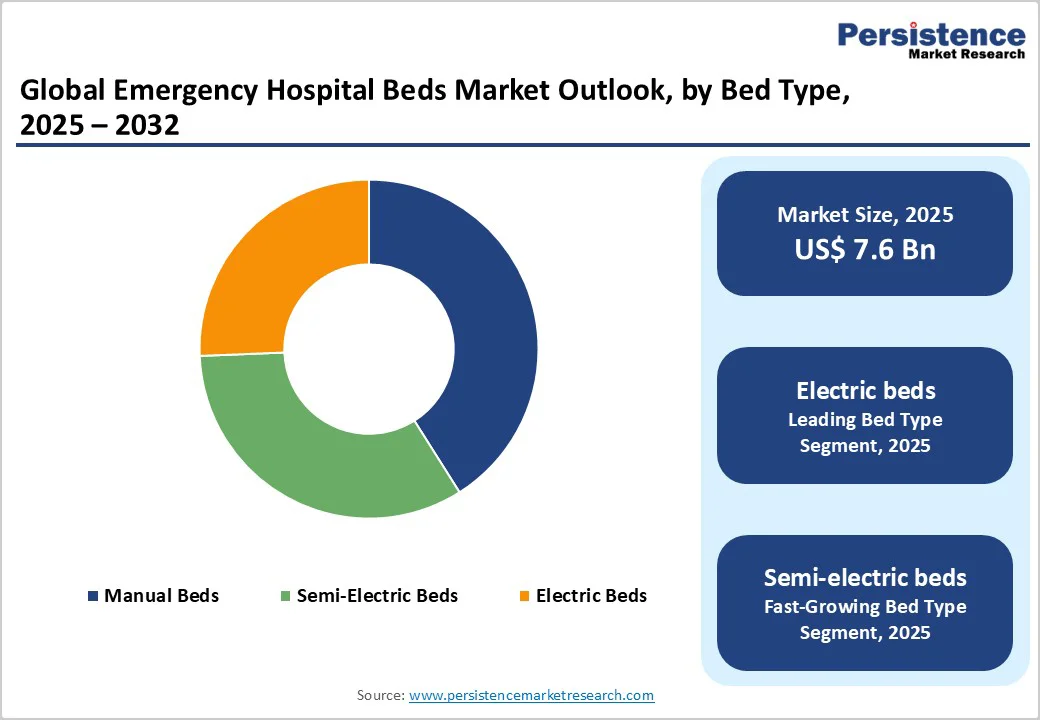

| Emergency Hospital Beds Market Size (2025E) | US$7.6 Bn |

| Market Value Forecast (2032F) | US$10.7Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.2% |

Market Dynamics

Driver - Rising Emergency & Trauma Cases

Rising emergency and trauma cases are a significant driver for the emergency hospital beds market. With rapid urbanization, increasing vehicle traffic, and expanding industrial activities, the incidence of road accidents and workplace injuries has surged globally. Natural disasters such as floods, earthquakes, and cyclones further strain emergency healthcare infrastructure, creating an urgent need for rapid patient care.

Hospitals and trauma centers require specialized emergency beds and stretchers capable of accommodating critically injured patients while ensuring safety, mobility, and ease of handling. These beds often feature adjustable positions, enhanced durability, and integration with monitoring systems to support immediate medical interventions.

Consequently, rising trauma cases are directly fueling investment in advanced emergency hospital bed solutions, particularly in high-density urban and disaster-prone regions.

Restraints - High Initial Capital Investment

High Initial Capital Investment: The adoption of advanced electric and smart emergency hospital beds is often hindered by their substantial upfront cost, making it challenging for smaller hospitals, rural healthcare centers, and budget-constrained facilities to invest.

Unlike manual beds, these technologically enhanced beds incorporate automated features, motorized adjustments, integrated patient monitoring systems, and IoT-enabled functionalities, which significantly increase procurement expenses. Beyond purchase costs, hospitals must also consider installation, calibration, and maintenance expenditures, adding to the financial burden.

For facilities operating under tight budgetary constraints, these cumulative costs can outweigh perceived benefits, leading to slower adoption rates. Consequently, despite their clear advantages in patient care and workflow efficiency, high-cost barriers remain a significant restraint for widespread market penetration.

Opportunity - Smart & Connected Beds

Smart & Connected Beds represent a transformative opportunity in the emergency hospital beds market. These beds are equipped with advanced sensors and IoT connectivity that continuously monitor patient vitals, including heart rate, blood pressure, oxygen saturation, and movement patterns. AI-driven algorithms can detect early signs of deterioration, alerting nurses or physicians in real time, thereby preventing falls, pressure ulcers, or other complications.

Integration with hospital information systems allows seamless data sharing, enhancing clinical decision-making and patient management. Automated adjustments for posture, height, and bed angles improve patient comfort while reducing caregiver workload. With rising adoption in ICUs, emergency departments, and high-acuity care units, smart beds offer both operational efficiency and enhanced patient safety, making them a critical focus for modern hospitals.

Category-wise Analysis

By Bed Type Insights

Electric beds account for the highest market share in the emergency hospital beds market due to their advanced functionality and adaptability in critical care settings. They allow automated adjustments of height, backrest, and leg positions, improving patient comfort, safety, and mobility. Integration with monitoring systems in ICUs and emergency departments enables efficient patient management and reduces caregiver workload.

Hospitals increasingly prefer electric beds for trauma, surgical recovery, and high-acuity care because they enhance workflow efficiency and clinical outcomes. Rising demand for smart, automated solutions, coupled with better durability and versatility compared to manual and semi-electric beds, solidifies their leading market position.

By End-user Insights

Hospitals account for the highest share in the emergency hospital beds market because they represent the largest and most diverse healthcare infrastructure requiring beds across multiple departments. From intensive care units and emergency departments to general wards and trauma centers, hospitals demand a wide range of bed types, including manual, semi-electric, and electric, often with integrated monitoring features.

The high patient volume, critical-care needs, and emphasis on patient safety drive hospitals to invest in advanced, durable, and feature-rich beds. Additionally, hospitals’ ongoing modernization, replacement cycles, and expansion of emergency and critical-care services reinforce their dominance as the primary end-user segment.

Region-wise Insights

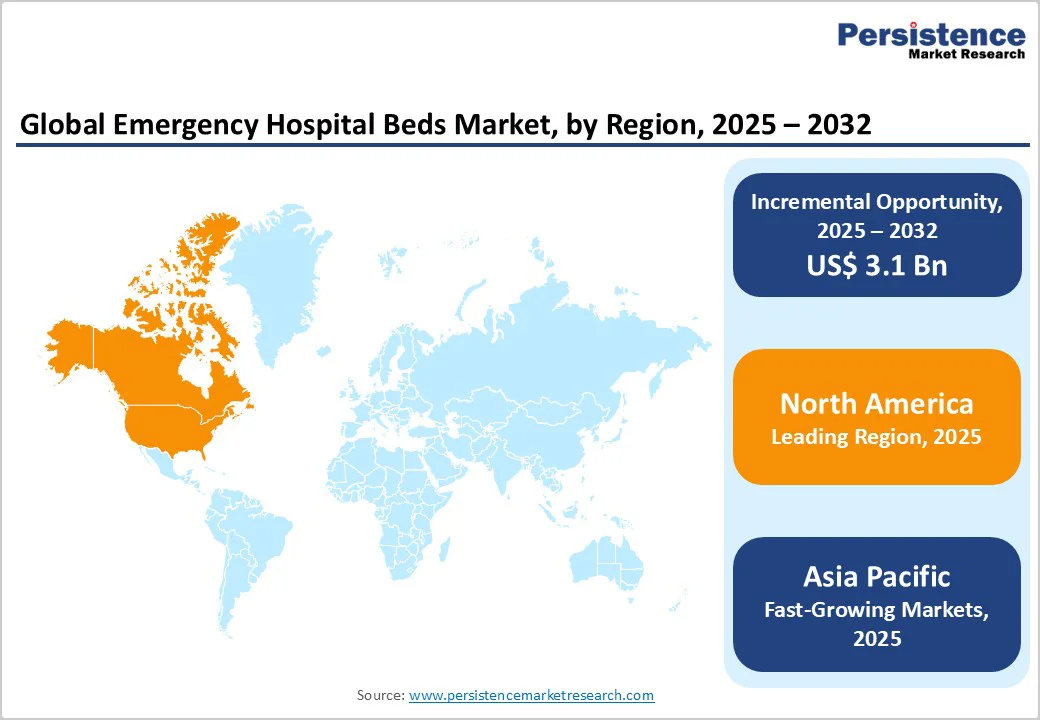

North America Emergency Hospital Beds Trends

North America leads the emergency hospital beds market, driven by advanced healthcare infrastructure, high adoption of technology, and stringent patient safety standards. Hospitals in the U.S. and Canada increasingly invest in electric and smart beds equipped with IoT sensors, automated adjustments, and integrated monitoring systems to enhance critical-care efficiency. Rising demand in trauma centers, emergency departments, and ICUs supports continuous market growth.

Additionally, favorable reimbursement policies, regular bed replacement cycles, and a focus on improving patient outcomes contribute to North America’s dominance. The region also serves as a testing ground for innovative bed designs, influencing global market trends and technological adoption.

Asia Pacific Emergency Hospital Beds Market Trends

The Asia-Pacific emergency hospital beds market is rapidly emerging, driven by expanding healthcare infrastructure, rising patient volumes, and increasing government investment in hospital modernization. Countries like India, China, and Southeast Asia are witnessing growing demand for ICU, trauma, and emergency department beds, including electric and semi-electric models.

Urbanization, rising accidents, and higher prevalence of chronic diseases are fueling the need for advanced beds with patient-monitoring capabilities. Additionally, the region’s private hospitals are adopting smart and connected beds to improve care quality. Affordable, modular, and portable beds are gaining traction, making Asia-Pacific a high-growth and strategically significant market for manufacturers.

Competitive Landscape

The emergency hospital beds market competitive landscape is highly dynamic, driven by innovation, product differentiation, and technological advancements. Key players focus on developing electric, semi-electric, and smart beds with integrated patient monitoring systems to enhance critical-care efficiency.

Competition is shaped by features such as modularity, portability, durability, and automation, catering to ICUs, trauma units, and emergency departments. Companies also prioritize customized solutions, after-sales services, and cost-effective offerings for emerging markets. Strategic initiatives like partnerships, product launches, and digital integration help maintain market presence.

Key Industry Developments:

- In April 2025, Wanaka-based property investment company Roa announced a joint venture partnership with Central Otago mana whenua interests for its proposed Wanaka Health Precinct. Roa had unveiled plans for a $300 million privately funded project, which was set to include a five-level hospital featuring four operating theatres, advanced imaging services, a 24-hour emergency department, and more than 70 beds spanning inpatient, emergency, and post-anaesthetic care.

Companies Covered in Emergency Hospital Beds Market

- Invacare Corporation

- Hill-Rom Holdings Inc.

- Stryker Corporation

- LINET

- Arjo

- PARAMOUNT BED CO., LTD.

- Howard Wright Limited

- Midmark Corp

- Joson-Care Enterprise Co., Ltd.

- Stiegelmeyer GmbH & Co.KG

- NOA Medical Industries Inc.

- Novum Medical Products

- Amico Corporation

- Other

Frequently Asked Questions

The global emergency hospital beds market is projected to be valued at US$7.6 Bn in 2025.

Increasing trauma cases, accidents, and critical illnesses create a high demand for emergency and ICU beds.

The global emergency hospital beds market is poised to witness a CAGR of 5.0% between 2025 and 2032.

Rapid-deployment and foldable beds for emergency, disaster, and mobile healthcare settings.

Invacare Corporation, Hill-Rom Holdings Inc., Stryker Corporation, LINET, and others.