- Advanced Materials

- Advanced Phase Change Material Market

Advanced Phase Change Material Market Size, Share, and Growth Forecast, 2025 - 2032

Advanced Phase Change Material Market By Product Type (Organic PCMs, Inorganic PCMs, Others), Form (Encapsulated PCM, Non-encapsulated PCM), Application (Building & Construction, HVAC, Cold Chain & Refrigeration, Others), and Regional Analysis for 2025 - 2032

Advanced Phase Change Material Market Share and Trends Analysis

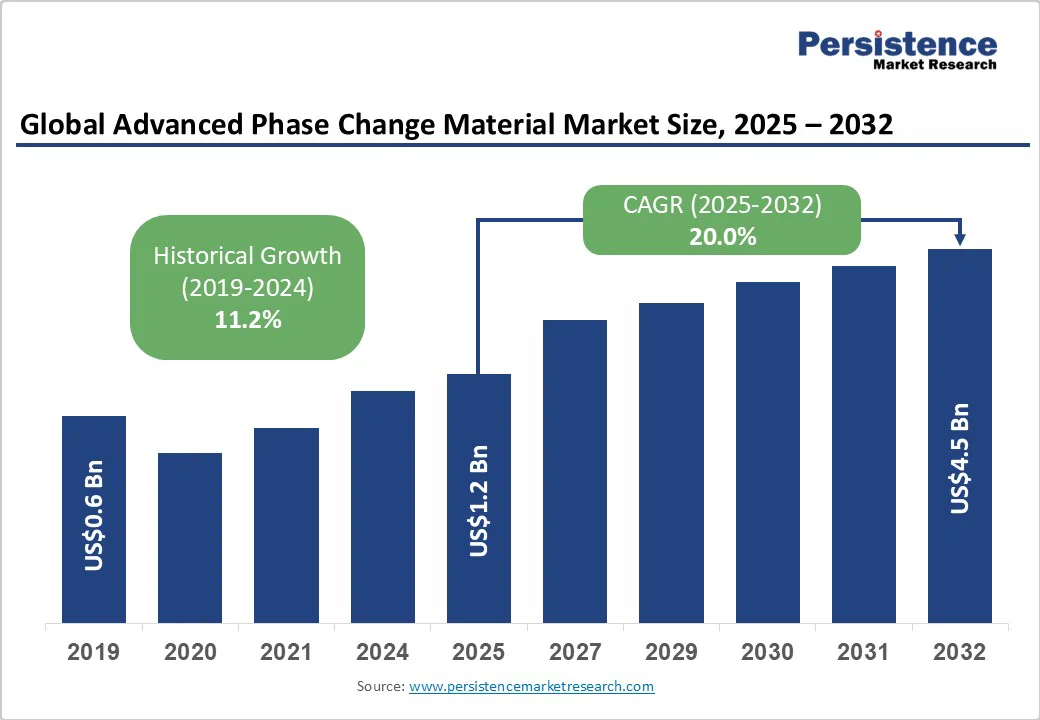

The global advanced phase change material (APCM) market size is likely to be valued at US$1.2 Billion in 2025 and is estimated to reach US$4.5 Billion by 2032, growing at a CAGR of 20.0% during the forecast period 2025 - 2032, driven by rising demand for energy-efficient thermal management solutions across key industries such as construction and electronics.

Key growth drivers include stringent regulations such as the EU’s Energy Performance of Buildings Directive, which mandates lower energy use, and advancements in encapsulation technologies that boost material stability and flexibility. These factors, alongside rising investments in renewable energy storage and green building initiatives, are accelerating market adoption.

Key Industry Highlights

- Leading Product Type: Organic APCMs are expected to lead with an estimated 53.9% market share in 2025, reflecting their superior thermal stability and widespread use in sustainable solutions.

- Fastest-growing Product Types: The bio-based APCM segment is set to register the fastest growth in the vicinity of 19.0% CAGR from 2025 to 2032, fueled by environmental regulations and innovation in renewable materials.

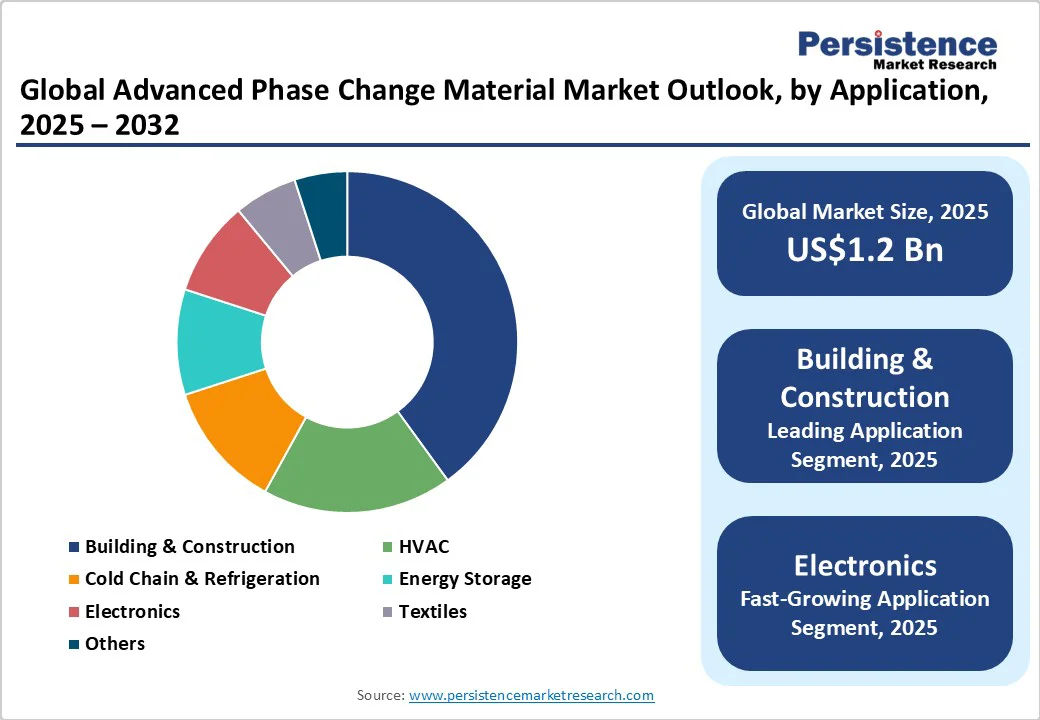

- Leading & Fastest-growing Applications: Building and construction applications are likely to dominate with 35.8% APCM market revenue share in 2025, while electronics are slated to advance at a 17.5% CAGR through 2032 due to a huge demand for efficient cooling.

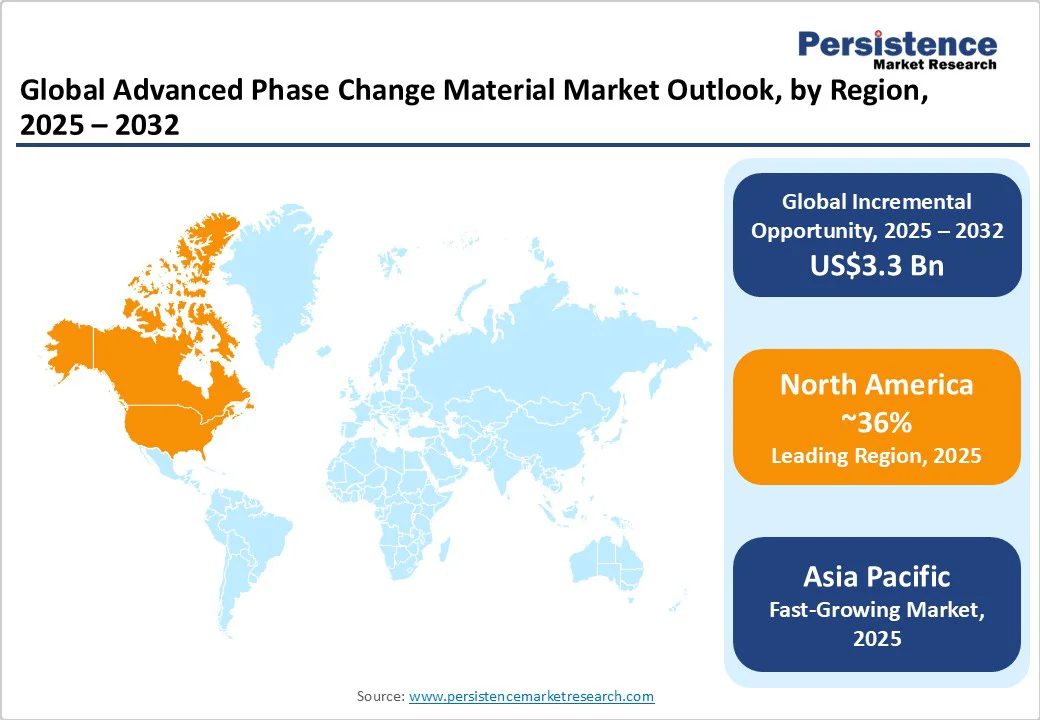

- Dominant Region: North America is anticipated to hold a commanding 36.0% share in 2025, underpinned by strong regulatory support and innovation in the U.S.

- Fastest-growing Region: Asia Pacific will emerge as the fastest-growing regional market with approximately 22.0% CAGR from 2025 to 2032, driven by rapid urbanization and strong manufacturing bases in China and India.

- July 2025: A new pilot under the IFC TechEmerge Sustainable Cooling Innovation program, in partnership with SPAR and IMI, deployed APCM technology to modernize Nigeria’s cold chain logistics, boosting efficiency and sustainability in refrigerated transport.

| Key Insights | Details |

|---|---|

| Advanced Phase Change Material Market Size (2025E) | US$1.2 Bn |

| Market Value Forecast (2032F) | US$4.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 20.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 11.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Regulatory Emphasis on Energy Efficiency and Carbon Reduction

Governments worldwide are tightening regulations to curb greenhouse gas emissions, driving the adoption of advanced phase change materials (APCMs) in energy-intensive sectors. The EU’s Green Deal mandates thermal storage in new buildings to support climate neutrality by 2050, boosting APCM demand in construction. Organic paraffins, for example, can cut heating and cooling loads by 20%-40%, according to the European Commission.

In the U.S., the Department of Energy estimates APCM-enhanced insulation could save up to 1.5 quadrillion BTUs annually by 2030, equating to US$15 Billion in energy savings. Technological advances such as nano-enhanced encapsulation, endorsed by IRENA, have improved the thermal conductivity of inorganic APCMs by 25%. These trends present strategic opportunities for businesses to align products with sustainability mandates, potentially gaining 10%-15% market share.

Material science innovations are accelerating APCM use in electric vehicles (EVs) and smart grids. Bio-based APCMs in EVs can extend range by up to 15% by regulating battery temperature, as noted by UNEP. Urbanization, projected to reach 68% of the global population by 2050, is also fueling demand for APCM-integrated smart buildings. Organizations such as ASHRAE advocate APCMs for HVAC efficiency, potentially lowering operational costs by 25%, making APCMs central to future-ready, sustainable infrastructure.

High Production and Integration Costs amid Supply Chain Vulnerabilities

APCMs face significant cost and structural barriers, limiting adoption in emerging markets where initial costs exceed traditional options by 30%-50%, according to the IMF. Raw material price volatility, especially paraffin, with up to 20% fluctuations per EIA data, coupled with geopolitical supply chain disruptions, can delay projects by 6-12 months and raise ownership costs by 15% (WTO). These challenges intensify competition from low-cost substitutes, urging firms to hedge through ISO-certified supplier contracts and scenario-based risk modeling.

Regulatory hurdles further impact scalability. The U.S. EPA mandates stringent toxicity testing for inorganic APCMs, increasing development costs by 10%-20%. Non-compliant imports, comprising 15% of global discrepancies (WCO), exacerbate market pressures. Limited bio-based feedstock availability, due to biodiversity regulations from the CBD, threatens up to 25% of production capacity. Proactive regulatory engagement with bodies such as ECHA and integrating compliance audits into strategy are vital to ensuring operational resilience and accelerating market readiness.

Policy-driven Incentives in Emerging Markets

Emerging economies are unlocking significant opportunities for APCMs, driven by policy incentives promoting sustainable infrastructure. Market projections estimate a US$1.5 Billion revenue boost by 2032 from regions such as Southeast Asia.

The Asian Development Bank highlights India’s Smart Cities Mission, with US$100 Billion allocated for urban upgrades, where APCMs can enhance thermal comfort and potentially capture 20% of the construction materials market through local manufacturing integration. Technological convergence with IoT-enabled infrastructure is further driving demand, with the International Telecommunication Union forecasting a 25% rise in smart device adoption, amplifying APCM use in energy storage systems.

APCMs are gaining traction in renewable energy integration, projected to form a US$2 Billion market segment by 2032. IRENA reports that APCMs improve energy storage efficiency by 30%, addressing intermittency in off-grid applications, particularly in Africa, where the African Union targets 300 GW of renewables by 2030.

In the U.S., the Inflation Reduction Act’s US$369 billion clean energy incentives are spurring investments in bio-based APCMs for microgrids. R&D partnerships with organizations, including the World Bank, could drive 18% growth in emerging markets, especially where low-maintenance, resilient solutions are needed. Stakeholders are advised to prioritize scalable pilot projects to validate technologies and ensure long-term profitability.

Category-wise Analysis

Product Type Insights

Organic PCMs are maintaining leadership in the advanced phase change materials market, slated to command an estimated 53.9% share in 2025, bolstered by their versatility in applications requiring stable thermal cycling, such as in building insulation, where they reduce energy demands by up to 25.0%, as supported by U.S. Department of Energy benchmarks. This dominance is attributed to cost-effectiveness and compatibility with existing manufacturing processes, with organic phase change materials finding sustained preference amid regulatory pushes for low-toxicity materials.

Bio-based PCMs are emerging as the fastest-growing segment, projected to achieve a CAGR of nearly 19.0% from 2025 to 2032, owing to the escalating sustainability demands and innovations in renewable sourcing that align with global net-zero goals, per Expert Market Research data.

Underlying drivers include demographic shifts toward eco-conscious consumers and policy incentives from bodies such as the UNEP, enabling actionable strategies for businesses to differentiate through biodegradable formulations and capture premium pricing in high-growth niches such as textiles.

Application Insights

Building & construction is set to retain its position as the leading segment in the advanced phase change materials market revenue share at an estimated 35.8% in 2025, facilitated by widespread integration in energy-efficient structures that comply with international standards, such as those from the International Code Council, where APCMs mitigate peak loads by 20.0%-30.0%. This leadership is reinforced by urbanization trends documented by the UN, emphasizing thermal regulation in high-density environments.

Electronics is advancing as the fastest-growing segment from 2025 to 2032, propelled by demands for thermal management in devices amid rising data center expansions, as highlighted by IRENA reports on energy-efficient computing. Key drivers encompass technological convergence with 5G and AI, offering consultative opportunities for suppliers to innovate hybrid solutions that address overheating risks and enhance product longevity in competitive landscapes.

Form Insights

Encapsulated forms are dominating the advanced phase change materials market, expected to secure approximately 60.0% share in 2025, on account of their enhanced durability and leak prevention that suit demanding applications such as HVAC systems, where they improve efficiency significantly, according to ASHRAE guidelines. This leading status is supported by encapsulation technologies that prevent phase separation, aligning with industry standards from ISO.

Non-encapsulated forms are the fastest-growing segment from 2025 to 2032, fueled by cost advantages and ease of integration in bulk applications such as construction composites, driven by macroeconomic trends in affordable housing as per World Bank analyses. Actionable insights suggest leveraging this growth through customized formulations that balance performance with economic viability, particularly in emerging markets seeking scalable thermal solutions.

Regional Insights

North America Advanced Phase Change Material Market Trends

North America is predicted to dominate with around 36.0% of the advanced phase change material market share in 2025, with projections indicating a CAGR of 10.5% through 2032. The spotlight in the regional market is on the U.S., which contributes over 65.0%, driven by robust performance in green building certifications under LEED standards, where APCM adoption has surged 20.0% annually. Primary growth factors encompass regulatory frameworks such as the EPA's energy efficiency mandates, innovation ecosystems fostered by DOE-funded R&D hubs, and macroeconomic trends in EV integration.

The regulatory environment, emphasizing carbon credits and incentives via the Inflation Reduction Act, is positively impacting adoption by reducing implementation barriers. Competitive landscape features consolidated players focusing on patented technologies, with investment trends leaning toward venture capital in startups, including Phase Change Energy Solutions, presenting opportunities in thermal storage for data centers and healthcare, offering stakeholders strong returns via strategic alliances.

Europe Advanced Phase Change Material Market Trends

Europe is set to secure about 35.0% of the APCM market share in 2025, positioning the region for a valuation approaching US$1.4 Billion. Performance metrics highlight Germany topping regional contribution through advanced manufacturing, the U.K. coming in second with its sustainability initiatives, France in renewable integration, and Spain with its construction upgrades.

Growth drivers include regulatory harmonization under the EU's REPowerEU plan targeting 45.0% renewable energy by 2030, technological advancements in microencapsulation, and demographic shifts toward urban retrofits. The regulatory environment, with policies such as the Energy Efficiency Directive, is accelerating harmonized standards that facilitate cross-border trade.

Competitive characteristics show a moderately consolidated landscape with emphasis on collaborative R&D, while investment trends favor public-private partnerships, offering actionable opportunities in net-zero buildings and textiles, potentially yielding a sizeable ROI for investors navigating policy-aligned expansions.

Asia Pacific Advanced Phase Change Material Market Trends

Asia Pacific is anticipated to attain an estimated 25.0% market share in 2025, and register the highest CAGR through 2032, driving the regional market size to surpass US$2.0 Billion. China will lead the pack via its mass production prowess, while Japan occupies a central position due to its innovations in electronics. In India, the regional market is expected to gain from smart city projects, and in ASEAN nations, through improvements in manufacturing efficiencies.

Other favorable factors for the Asia Pacific APCM market include manufacturing advantages such as low-cost labor and supply chains, policy changes under China's 14th Five-Year Plan for carbon peaking, and rapid urbanization as per ADB reports.

Regulatory impacts from bodies such as ASEAN's energy cooperation framework are promoting harmonized efficiency standards. The competitive landscape is fragmented yet innovative, with trends toward foreign direct investment in joint ventures, unlocking opportunities in EV thermal management and cold chain logistics.

Competitive Landscape

The global advanced phase change material market exhibits a moderately consolidated structure, with the top five players commanding approximately 45.0% of the market share, fostering an environment where innovation and scale dictate competitive positioning. Leading entities include BASF SE, Honeywell International Inc., and Croda International Plc, leveraging their extensive R&D capabilities to dominate in organic and encapsulated segments.

Market concentration analysis reveals that IP protection in encapsulation technologies creates barriers to entry via intellectual property (IP) in encapsulation technologies, yet fragmentation persists among niche bio-based providers. Competitive positioning overview highlights differentiation through sustainability certifications, with leaders such as Outlast Technologies, which focuses on application-specific solutions.

This structure advises inchoate players to pursue strategic niches in high-growth areas such as renewables, while investors should evaluate consolidation risks, potentially through M&A, to enhance supply chain resilience and achieve economies of scale.

Key Industry Developments

- In August 2025, researchers at Universidad de Santiago de Chile, led by Dr. Diego Vasco, launched a Fondecyt Regular project to boost solar energy use through thermal storage systems. The project uses organic PCMs, such as vegetable oils enhanced with nanoparticles, to improve heat conductivity and efficiency, aiming to cut energy use in buildings and industry.

- In August 2025, researchers from UC Davis and the University of Washington developed a photonic in-memory computing system using 3D-integrated electronic-photonic circuits with PCMs such as Sb?S?. Achieving over 12-bit precision and scalability for a million+ operations, the system combines PCM-AlGaAs resonators with silicon photonics for ultra-low power, high-efficiency performance, ideal for autonomous systems and fluid dynamics.

- In May 2025, a Scientific Reports study revealed that cotton fabrics treated with bio-organic PCMs, gelatin combined with coconut oil or octadecanol, show improved thermal regulation by forming a stable, heat-retaining film. Using the pad-dry-cure method, researchers found pre-dyed fabrics performed better, with coconut oil-based composites offering higher latent heat storage and thermal conductivity than octadecanol.

Companies Covered in Advanced Phase Change Material Market

- BASF SE

- Honeywell International Inc.

- Croda International Plc

- Outlast Technologies LLC

- Rubitherm Technologies GmbH

- Phase Change Energy Solutions

- Cryopak

- Climator Sweden AB

- Dow Building Solutions

- Entropy Solutions Inc.

- Pluss Advanced Technologies Pvt. Ltd.

- PCM Products, Inc.

- PureTemp LLC

- Salca BV

- Advansa B.V.

Frequently Asked Questions

The advanced phase change material (APCM) market is projected to reach US$4.5 Billion in 2025.

The heightening demand for energy-efficient thermal management solutions across key industries, such as construction and electronics, and stringent regulatory frameworks promoting sustainability, are driving the market.

The advanced phase change material market is poised to witness a CAGR of 20.0% from 2025 to 2032.

Key market opportunities include advancements in encapsulation technologies that improve material stability and application versatility, along with growing investments in renewable energy storage and green building initiatives, driving demand for advanced phase change materials.

BASF SE, Honeywell International Inc., and Croda International Plc are some of the key players in the advanced phase change material (APCM) market.