- Clothing, Footwear, & Accessories

- Spunlace Nonwovens Market

Spunlace Nonwovens Market Size, Share, and Growth Forecast 2026 - 2033

Spunlace Nonwovens Market by Product Type (Plain, Embossed, Apertured, Woodpulp-Based), Raw Material (Polyester, Polypropylene, Viscose/Rayon, Cotton, Blended Fibers, Specialty Fibers), Basis Weight (Lightweight, Medium Weight, Heavyweight), Application (Wipes, Medical & Healthcare, Hygiene Products, Personal Care & Cosmetics, Filtration, Apparel & Textiles, Artificial Leather, Home Care), End-userr, and Regional Analysis, 2026 - 2033

Spunlace Nonwovens Market Size and Trend Analysis

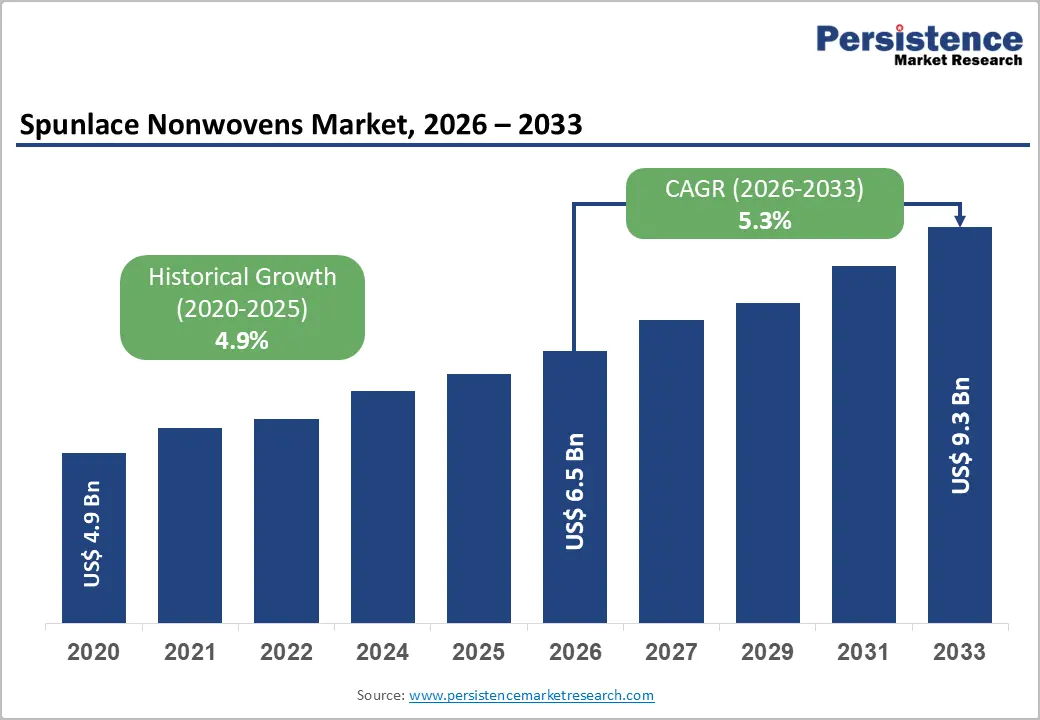

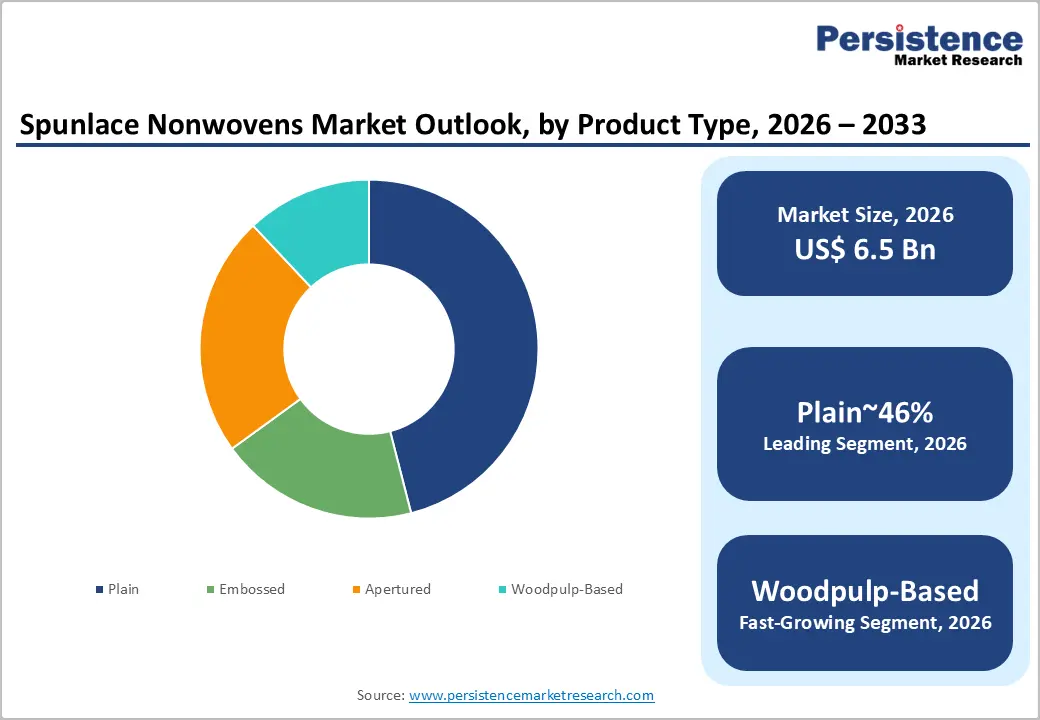

The global Spunlace Nonwovens Market size is likely to be valued at US$ 6.5 billion in 2026 and is expected to reach US$ 9.3 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033. It is driven by the expanding global demand for premium hygiene products, medical and healthcare nonwoven consumption, and the growing personal care and cosmetics industry’s adoption of soft, skin-friendly spunlace substrates for facial wipes, cleansing sheets, and cosmetic pads.

Key Industry Highlights:

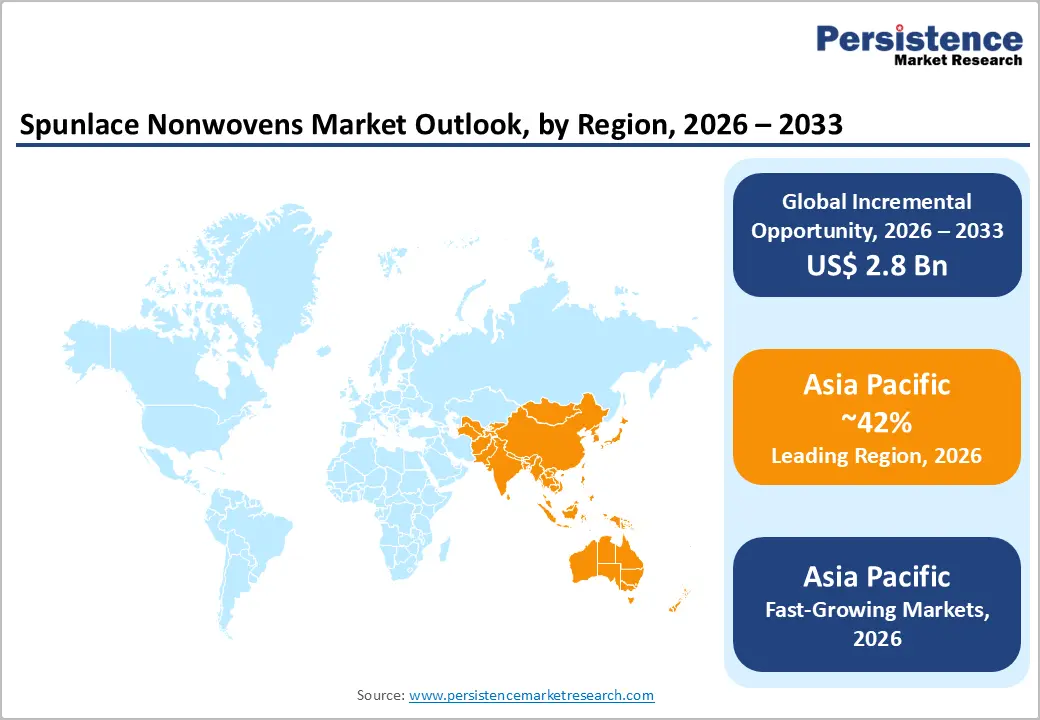

- Leading Region: Asia Pacific leads the spunlace nonwovens market as both the largest production hub and consuming region, holding 42% share, driven by China’s massive wipes manufacturing ecosystem, Japan’s premium cosmetics spunlace demand, and India’s rapidly expanding healthcare infrastructure consumption.

- Fastest Growing Region: Asia Pacific is simultaneously the fastest growing region with a CAGR of 7.1%, fueled by India’s PMJAY healthcare expansion covering 500M+ people, South Korea and China’s K-Beauty facial care culture driving premium spunlace sheet mask demand, and ASEAN’s rising personal care consumption.

- Dominant Applications: Plain spunlace nonwovens are likely to lead with approximately 46% market share, as the most versatile and widely produced fabric format serving wipe, medical, and personal care applications across global brand owner supply chains.

- Fastest Growing Application: Medical & healthcare are the fastest growing segments, driven by WHO-endorsed single-use disposable medical textile standards, aging global populations requiring more hospital procedures, and emerging market healthcare infrastructure expansion.

- Key Opportunity: EU SUP Directive-driven demand for certified biodegradable spunlace substrates using TENCEL™ lyocell, FSC-certified viscose, and cotton, enabling 15–30% premium pricing, and medical-grade spunlace expansion into India’s PMJAY-driven healthcare infrastructure represent the highest-value growth opportunities.

Market Dynamics

Drivers - Expanding Global Healthcare and Medical Nonwovens Demand

The global healthcare sector is the most technically demanding and fastest-growing end-user segment for spunlace nonwovens, driven by expanding surgical procedure volumes, increasing infection control standards, and the growth of single-use medical hygiene products. Spunlace fabrics are extensively used in surgical gowns, drapes, sterilization wraps, wound dressings, and patient hygiene wipes.

The World Health Organization (WHO) emphasizes single-use disposable medical textiles as a critical component of infection prevention in healthcare settings. Global surgical procedure volumes are increasing in parallel with aging populations: the United Nations projects that the population aged 65+ will reach 1.6 billion by 2050, driving higher rates of hospitalization and procedural intervention that directly expand medical spunlace nonwoven consumption. Government healthcare infrastructure investment programs across Asia Pacific and the Middle East are simultaneously expanding hospital capacity and creating new institutional demand centers.

Rising Personal Care and Cosmetics Sector Demand for Premium Wipe Substrates

The global personal care and cosmetics industry’s accelerating adoption of premium wipe substrates, including facial cleansing wipes, micellar cleansing pads, makeup remover sheets, and eye mask fabrics, is driving sustained, high-value demand for soft, absorbent spunlace nonwovens. Cosmetics Europe reports that the European personal care market generates over €84 billion in annual retail sales, with facial cleansing and wipes among the fastest-growing categories.

The Asia Pacific beauty market, led by South Korea, Japan, and China’s K-Beauty-influenced facial care culture, has driven particularly strong demand for ultra-soft, high-thread-count equivalent spunlace fabrics for premium sheet masks and cleansing products. Cotton-based and viscose/rayon spunlace substrates are preferred for cosmetic applications due to their natural fiber feel and skin compatibility, supporting premiumization and higher average selling prices in this dynamic segment.

Restraints - High Capital Investment in Spunlace Production Lines

Spunlace nonwoven production requires high-pressure water-jet entanglement equipment with sophisticated water management and drying systems, which represent a significantly higher capital investment than alternative nonwoven processes such as spunbond or meltblown.

A complete spunlace production line from leading equipment suppliers, including Andritz AG, Trützschler Nonwovens, and Rieter, can cost US$ 30 million or more, depending on width, speed, and automation level. For emerging market producers and smaller nonwoven manufacturers, these capital barriers constrain new capacity investment and market entry, moderating supply-side responsiveness to demand growth.

Environmental Concerns Around Synthetic Fiber Spunlace Products

A significant share of spunlace nonwovens is produced from polyester and polypropylene synthetic fibers that are not biodegradable, generating concerns about microplastic shedding during washing and end-of-life disposal.

The EU’s Single-Use Plastics Directive (SUP Directive 2019/904/EC) requires wet wipes containing plastic fibers to carry labeling disclosures, while regulatory pressure for biodegradable alternatives is intensifying across Europe and North America. These sustainability pressures are compelling manufacturers to invest in fiber substitution toward viscose, cotton, and lyocell substrates, increasing production costs and creating transition-period investment burdens.

Opportunities - Sustainable and Biodegradable Spunlace Nonwovens for Regulated Markets

The growing regulatory and consumer pressure against single-use products containing plastic is creating a significant market opportunity for producers developing certified biodegradable spunlace nonwoven substrates. The EU SUP Directive plastic labeling requirements for wipes containing synthetic fibers, combined with growing retailer and brand owner commitments to plastic-free personal care product ranges, are driving rapid product reformulation toward viscose, cotton, Lyocell, and wood pulp-based spunlace substrates.

Suominen Corporation’s BIONELLE and Ahlstrom-Munksjö’s sustainable wipe substrate portfolios represent leading commercial implementations. The global organic cotton and sustainable fiber movement, with the Textile Exchange reporting double-digit growth in preferred fiber sourcing, provides both raw material infrastructure and brand storytelling support for premium biodegradable spunlace positioning, enabling manufacturers to command 20% price premiums in eco-conscious retail channels.

Medical Spunlace Growth in Emerging Market Healthcare Infrastructure Expansion

The rapid expansion of hospital and healthcare infrastructure across Asia Pacific, Africa, and Latin America is creating large, underserved demand pools for medical-grade spunlace nonwovens used in surgical textiles, wound care, and patient hygiene applications.

The World Bank is directing billions in healthcare infrastructure financing across developing economies, and government programs, including India’s Ayushman Bharat–Pradhan Mantri Jan Arogya Yojana (PMJAY), the world’s largest government-funded health insurance scheme covering over 500 million people, are expanding formal healthcare utilization that drives disposable medical textile consumption. Manufacturers achieving ISO 13485 medical device quality management certification and EN 13795 surgical textile performance standards compliance can access premium, long-term institutional procurement contracts with rapidly expanding hospital networks across these high-growth emerging healthcare markets.

Category-wise Analysis

By Product Type Insights

Plain spunlace nonwovens are the leading product type, accounting for approximately 46% of total market share. Plain hydroentangled fabrics, with smooth, uniform surface texture, serve the broadest range of wipe, medical, and personal care applications where consistent absorbency, tensile strength, and softness are required without surface texture differentiation. Their compatibility with high-speed converting, printing, and packaging operations makes them the most commercially versatile and widely produced spunlace format.

Plain spunlace fabrics serve as the substrate for the majority of global wipe brands, including Kimberly-Clark’s Scott and Procter & Gamble’s household wipe lines. The segment benefits from the largest installed production base globally, with dedicated plain spunlace lines operating at near-continuous capacity across leading producers in Europe, North America, and the Asia Pacific.

By Raw Material Insights

Viscose/Rayon is the leading raw material segment in spunlace nonwovens, representing approximately 38% of total fiber consumption by volume. Viscose, a regenerated cellulose fiber derived from wood pulp, is the preferred fiber type for premium spunlace applications, including cosmetic wipes, baby wipes, and medical hygiene products, due to its exceptional softness, high moisture absorbency, natural feel against skin, and superior biodegradability compared to synthetic alternatives.

The fiber’s compatibility with high-speed hydroentanglement processes and its ability to produce homogeneous web structures with excellent hand feel make it functionally superior to polyester in skin-contact applications. Major viscose fiber suppliers, including Lenzing AG and Sateri Holdings, serve the global spunlace nonwovens market with certified sustainable viscose grades.

By Basis Weight Insights

Medium-weight spunlace nonwovens lead the basis-weight segment, accounting for approximately 49% of total market share. Medium-weight fabrics, typically in the 45–80 gsm range, represent the most commercially versatile basis weight category, serving the widest range of wipe, hygiene, and medical applications where the balance of strength, absorbency, and converting efficiency is optimized.

This weight range covers the majority of consumer wet wipe substrates, hospital patient care wipes, and personal care applications that constitute the core volume demand for spunlace nonwovens globally. Medium-weight fabrics provide adequate tensile strength for machine-processing through folding, cutting, and packaging lines while maintaining the softness and drape characteristics that end-consumers associate with premium wet wipe and hygiene products.

By Application Insights

Wipes are the dominant application segment, accounting for approximately 41% of the market. The wipes category, encompassing baby wipes, personal hygiene wipes, household cleaning wipes, industrial wipes, disinfecting wipes, and cosmetic cleansing wipes, represents the single largest and most diverse volume application for spunlace nonwovens globally.

The COVID-19 pandemic fundamentally expanded the disinfecting and hygiene wipes category, and INDA data confirms that post-pandemic wipe consumption has maintained a structurally higher baseline than pre-2020 levels across most markets. The Association of the Nonwoven Fabrics Industry reports that the wipes category accounts for the majority of hydroentangled nonwoven production in North America and Europe. Baby wipes alone represent a globally significant volume category, with over 140 million births worldwide per UN data, generating sustained demand from a new consumer cohort.

Regional Insights

North America Spunlace Nonwovens Market Trends & Analysis

North America remains a mature yet innovation-driven spunlace nonwovens market, led by strong demand from healthcare, hygiene wipes, and personal care sectors. Regulatory frameworks (FDA, OSHA) ensure consistent demand for medical-grade materials, while sustainability and premiumization trends drive innovation. The U.S. dominates regional consumption, supported by high per capita hygiene product usage.

- U.S. Spunlace Nonwovens Market Size

The U.S. accounts for approximately 85% of North America’s spunlace consumption, valued at around US$ 2.0 billion in 2026, and is growing steadily at a ~4.5% CAGR. Demand is fueled by disinfecting wipes, baby care, and cosmetics, alongside institutional healthcare procurement and increasing preference for biodegradable wipe substrates.

Europe Spunlace Nonwovens Market Trends, Drivers & Insights

Europe is a premium, sustainability-led spunlace market driven by strict environmental regulations such as the EU SUP Directive. Producers focus on biodegradable fibers and circular production. High demand from the medical, personal care, and cosmetics industries, along with innovation in eco-friendly materials, positions Europe as a global leader in sustainable spunlace technologies.

- Germany Spunlace Nonwovens Market Size

Germany leads Europe’s production and consumption, with an estimated market size of US$ 700 million in 2026. Strong industrial base, advanced manufacturing, and high demand for medical and hygiene applications support growth. The country also acts as a key export hub for premium nonwoven materials.

- U.K. Spunlace Nonwovens Market Size

The U.K. market is valued at approximately US$ 350 million in 2026, supported by NHS procurement and steady demand for medical and hygiene wipes. Sustainability regulations and increasing consumer preference for eco-friendly personal care products are accelerating the adoption of biodegradable spunlace substrates.

- France Spunlace Nonwovens Market Size

France’s market is estimated at US$ 300 million in 2026, driven by its strong cosmetics and luxury personal care sector. Premium facial wipes and skincare applications dominate demand, while sustainability initiatives encourage innovation in bio-based and compostable spunlace materials.

Asia Pacific Spunlace Nonwovens Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing region, driven by population scale, rising hygiene awareness, and expanding healthcare infrastructure. Cost-efficient production in China, combined with growing domestic consumption and exports, anchors regional dominance. Emerging markets like India and ASEAN are accelerating growth through healthcare expansion and urbanization.

- China Spunlace Nonwovens Market Size

China dominates globally with an estimated market size of US$ 2.8 billion in 2026, accounting for over 40% of global demand. Growth is driven by massive wipes consumption, strong export capacity, and cost-efficient production, alongside increasing domestic demand for personal hygiene and baby care products.

- India Spunlace Nonwovens Market Size

India’s market is valued at approximately US$ 550 million in 2026, expanding at a CAGR of over 6%. Growth is fueled by healthcare initiatives like PMJAY, rising disposable incomes, and increasing awareness of hygiene products. The wipes segment, especially baby and personal care, is witnessing rapid expansion.

- Japan Spunlace Nonwovens Market Size

Japan represents a high-value, technologically advanced market estimated at US$ 670 million in 2026. Demand is concentrated in premium cosmetics, medical applications, and high-performance nonwovens. Innovation, aging population needs, and preference for high-quality hygiene products sustain steady growth despite market maturity.

Competitive Landscape

The global spunlace nonwovens market is moderately consolidated, featuring a mix of large diversified nonwovens conglomerates and dedicated spunlace specialists. Companies including Suominen Corporation, Berry Global Group, Ahlstrom-Munksjö Oyj, and Jacob Holm & Sons AG hold strong market positions through advanced hydroentanglement technology, diversified fiber and product portfolios, and global manufacturing footprints. Asian producers including Toray Industries and Asahi Kasei serve premium technical segments, while Chinese producers compete on cost in standard wipe substrate grades.

Key differentiators include basis weight range, fiber blend capability, sustainable substrate certifications), medical compliance certifications, and converting-to-finished-product integration capabilities. Emerging trends include bio-based fiber development, closed-loop water recycling in production, and digital fabric surface customization for premium personal care brand partners.

Key Developments:

- March 2025: Suominen Corporation launched its BIONELLE Evolution range of 100% plant-based spunlace substrates made with FSC-certified wood pulp and lyocell fibers, targeting compliance with the EU SUP Directive for wipe manufacturers seeking certified, plastic-free substrate solutions.

- October 2024: Jacob Holm & Sons AG expanded its SoftAir spunlace fabric platform with new ultra-lightweight cosmetic-grade grades for premium facial mask and eye patch applications in the Asia Pacific K-Beauty market, featuring sub-30 gsm basis weights with exceptional softness and transparency.

- May 2024: Ahlstrom-Munksjö Oyj introduced a medical-grade spunlace nonwoven line certified to EN 13795 standards for surgical gowns and drapes, featuring enhanced fluid barrier performance and OEKO-TEX STANDARD 100 certification for healthcare facility procurement across European and Middle Eastern markets.

Global Spunlace Nonwovens Market- Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 4.9 Bn |

|

Current Market Value (2026) |

US$ 6.5 Bn |

|

Projected Market Value (2033) |

US$ 9.3 Bn |

|

CAGR (2026-2033) |

5.3% |

|

Leading Region |

Asia Pacific, 42% share |

|

Dominant Product Type |

Plain, 46% share |

|

Top-ranking End Use |

Healthcare, 32% |

|

Incremental Opportunity |

US$ 2.8 Bn |

Companies Covered in Spunlace Nonwovens Market

- Suominen Corporation

- Ahlstrom-Munksjö Oyj

- Freudenberg & Co. KG

- Berry Global Group, Inc.

- Glatfelter Corporation

- Johns Manville

- Fitesa S.A.

- Avgol Industries 1953 Ltd.

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Mitsui Chemicals, Inc.

- Jacob Holm & Sons AG

- PFNonwovens Group

- Oceancash Pacific Berhad

- Rugao Jinyi Textile Co., Ltd.

- Lenzing AG

- Sandler AG

Frequently Asked Questions

The global Spunlace Nonwovens Market is projected to reach US$ 9.3 Billion by 2033, growing from US$ 6.5 Billion in 2026 at a CAGR of 5.3% during the 2026–2033 forecast period.

The primary drivers are expanding global healthcare infrastructure requiring single-use WHO-endorsed disposable medical textiles, with the UN projecting 1.6 billion people aged 65+ by 2050 driving surgical and patient care volumes, and the Asia Pacific K-Beauty influenced personal care market generating premium viscose spunlace demand for facial wipes, sheet masks, and cosmetic cleansing products.

Viscose / Rayon leads the By Raw Material category with approximately 38% fiber consumption share, preferred for its exceptional softness, high moisture absorbency up to 3.5× its weight in water, natural skin-compatible feel, and biodegradability, making it the universal substrate choice for premium cosmetic wipes, baby wipes, and medical hygiene spunlace products globally.

Asia Pacific leads the global Spunlace Nonwovens Market as both the dominant production and consumption region, led by China’s massive wipes manufacturing base, Japan’s premium spunlace production from Toray and Asahi Kasei, Malaysia’s Oceancash Pacific Berhad, and India’s rapidly expanding healthcare and personal care consumption driving sustained regional demand growth.

The highest-value opportunities are EU SUP Directive-mandated biodegradable substrate development using TENCEL lyocell and FSC-certified viscose commanding 15–30% price premiums in eco-conscious European and North American retail channels, and medical-grade spunlace expansion into India’s PMJAY-driven healthcare infrastructure covering 500+ million people with growing hospitalization and disposable medical textile demand.