- Energy Storage Solutions

- UPS Battery Market

UPS Battery Market Size, Share, and Growth Forecast 2026 - 2033

UPS Battery Market by Battery Type (Lead Acid, Li-ion, Nickel Cadmium, Others), Application (Residential, Commercial, Data Centres, Industrial), Power Rating (Less than 10 kVA, 10-100 kVA, 101-250 kVA, above 250 kVA), and Regional Analysis for 2026 - 2033

UPS Battery Market Size and Trend Analysis

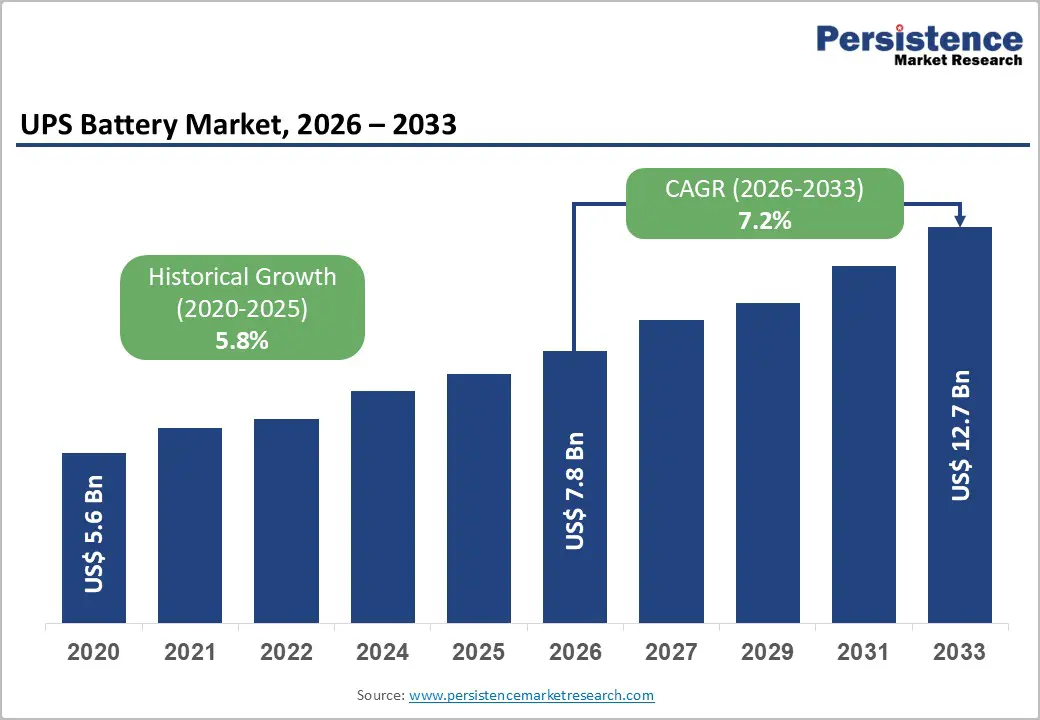

The global UPS battery market size is valued at US$ 7.8 billion in 2026 and is projected to reach US$ 12.7 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033. This robust growth is primarily fueled by the accelerating buildout of hyperscale and edge data centers, surging adoption of 5G telecommunications infrastructure, and the rapid digital transformation of industries worldwide.

Escalating power reliability requirements across healthcare, banking, and manufacturing verticals, combined with the declining cost of lithium-ion battery technology, are compelling enterprises to invest in advanced UPS solutions, reinforcing sustained demand throughout the forecast period.

Key Industry Highlights

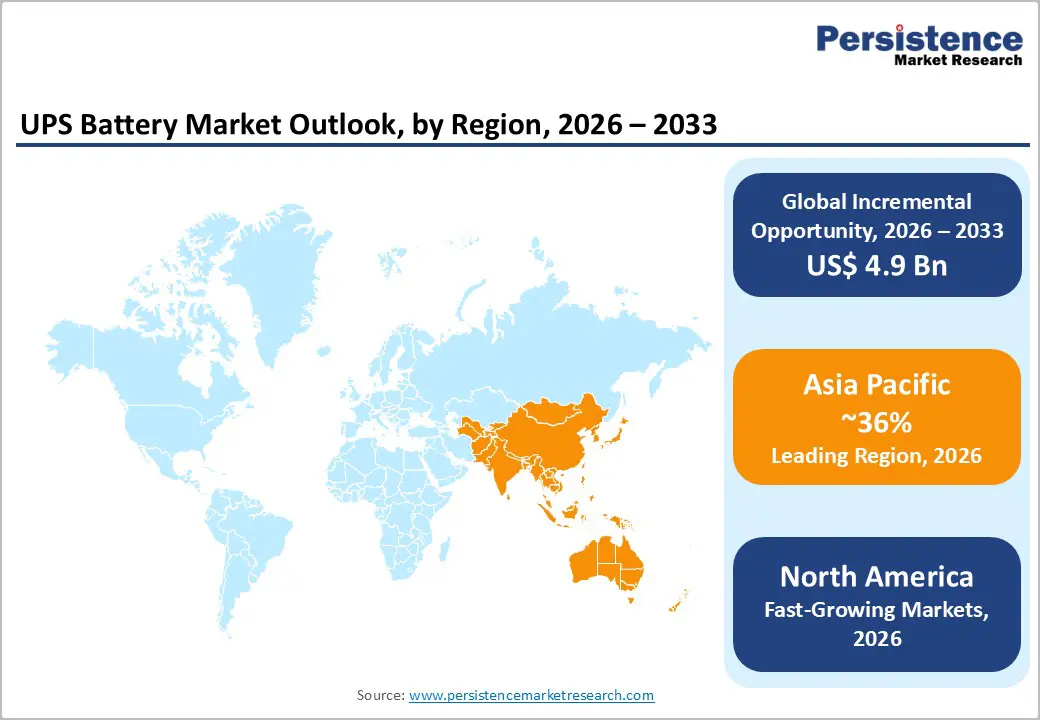

- Leading Region: The Asia Pacific UPS battery market dominated the global market with a revenue share of 36.5% in 2026 and is expected to grow at a CAGR of 13.4% from 2026 to 2033. Rapid urbanization and industrialization across countries such as China, India, Japan, and South Korea are significant drivers of growth. These nations are experiencing an increased demand for uninterrupted power supplies to support their economic progress.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, projected at the highest CAGR through 2033, fueled by China's data center expansion, India's 5G infrastructure investment, and rapid industrialization across ASEAN economies, including Malaysia, Indonesia, and Thailand.

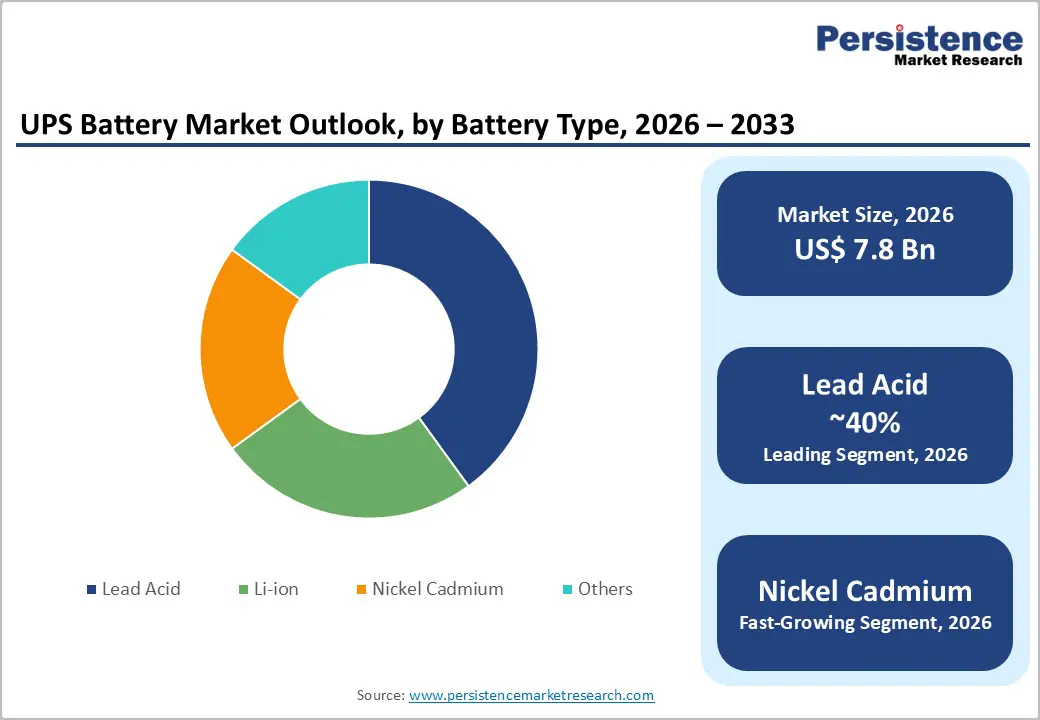

- Dominant Segment: Lead-acid batteries (VRLA) dominate the Battery Type segment, with approximately 38-40% revenue share, owing to lower upfront costs, a mature supply chain, and global recycling rates exceeding 90%, thereby retaining widespread adoption in cost-sensitive applications.

- Fastest Growing Application Segment: The data centers application segment is the fastest-growing category, driven by AI workload expansion, cloud computing growth, and hyperscale infrastructure buildout, with IEA projecting global data center electricity consumption to nearly double to 945 TWh by 2030.

- Key Opportunity: AI-enabled Battery Management Systems (BMS) and grid-interactive UPS architectures present the key market opportunity, enabling predictive maintenance, extended battery lifecycles, and demand-response participation, creating high-margin recurring service revenue streams for UPS manufacturers.

DRO Analysis

Drivers - Exponential Expansion of Data Center Infrastructure

The global proliferation of hyperscale and edge data centers stands as the single most powerful catalyst for UPS battery demand. According to the U.S. Department of Energy (DOE), data center electricity consumption in the United States reached approximately 176 TWh in 2023 and is projected to double or triple by 2028. Globally, the International Energy Agency (IEA) estimates data center electricity consumption at around 415 TWh in 2024, poised to grow at approximately 15% per year through 2030.

Since data centers require uninterrupted power to prevent costly operational downtime, high-capacity UPS batteries, particularly lithium-ion-based systems, have become indispensable. Combined capital expenditure on data centers by Amazon, Microsoft, Google, and Meta exceeded US$ 200 billion in 2024 alone, reflecting the enormous scale of infrastructure investments that directly generate sustained demand for UPS battery solutions.

Increasing Frequency of Power Disruptions and Energy Transition Imperatives

The increasing frequency and severity of extreme weather events, coupled with the ongoing transition to renewable energy sources, have heightened the strategic importance of reliable backup power systems. Governments and enterprises across the globe are investing heavily in grid modernization; however, intermittent renewable generation introduces new reliability challenges. According to the U.S. Energy Information Administration (EIA), the average American utility customer experienced approximately 8 hours of power interruption per year in 2020.

Across emerging economies in the Asia Pacific, Africa, and Latin America, power outages remain a critical operational risk, compelling industrial facilities, hospitals, and commercial establishments to adopt robust UPS battery systems. Regulatory frameworks such as the European Union's Energy Efficiency Directive and national energy resilience standards further necessitate investment in advanced power backup infrastructure, thereby substantially broadening the addressable market for UPS batteries.

Restraints - High Capital Cost of Lithium-Ion UPS Transition

Despite superior lifecycle economics, the upfront capital expenditure required to transition from traditional valve-regulated lead-acid (VRLA) batteries to lithium-ion systems remains a significant deterrent, particularly for cost-sensitive industrial users and small-to-medium enterprises (SMEs). For large data centers deploying 1 MW+ UPS banks, incremental capital expenditure for lithium-ion systems can exceed US$ 1 million, considerably lengthening payback periods.

Furthermore, lithium batteries are classified as hazardous materials for air transport, elevating shipping costs by approximately 30-40% compared to VRLA alternatives. These financial barriers continue to delay lithium-ion adoption among budget-constrained end users, limiting market penetration despite clear long-term operational expenditure (OPEX) advantages.

Stringent Environmental and Safety Regulations on Lead-Acid Batteries

Lead-acid batteries, which still account for a significant share of the UPS battery installed base, contain sulfuric acid and heavy metals, which are regulated under frameworks such as the EU RoHS Directive, the Basel Convention, and various national hazardous waste management laws. Compliance with disposal, recycling, and transportation requirements adds considerable operational cost and administrative complexity for end users and manufacturers alike.

While lead-acid batteries enjoy a high recycling rate of over 90% globally, according to the Battery Power Magazine Industry Organization, the evolving stringency of regulations across jurisdictions creates compliance uncertainty, particularly for multinational operators managing large UPS battery fleets across multiple regulatory environments. These dynamics constrain market expansion for conventional battery chemistries.

Opportunities - Lithium-Ion Adoption as a Fast-Growing Segment in Data Center UPS Applications

The accelerating shift from VRLA to lithium-ion batteries within data center UPS applications represents a substantial near-term revenue opportunity for market participants. Lithium-ion batteries captured approximately 44% of UPS battery market revenues in 2024, and their adoption is projected to expand at nearly 18% CAGR through 2030, significantly outpacing overall market growth.

As hyperscale operators demand compact, high-power-density backup solutions capable of supporting rack loads exceeding 100 kW, and as AI-optimized data center infrastructure becomes mainstream, lithium-ion UPS systems offer distinct advantages in energy density, footprint reduction, and total cost of ownership. In October 2024, Vertiv and NVIDIA jointly introduced a 132-kW liquid-cooled rack UPS specifically engineered for AI platforms, illustrating the convergence of AI infrastructure buildout with next-generation UPS battery technology.

Smart Battery Management Systems and Energy Storage Integration

The integration of Artificial Intelligence (AI)-enabled Battery Management Systems (BMS) and the growing convergence of UPS infrastructure with broader Energy Storage Systems (ESS) present transformative business model opportunities. Smart BMS technologies enable predictive maintenance, real-time performance monitoring, and extended battery lifecycle management, reducing total cost of ownership and creating recurring service revenue streams for UPS manufacturers.

Additionally, grid-interactive UPS architectures where large-scale UPS battery banks participate in demand response and frequency regulation markets are gaining commercial traction, particularly in North America and Europe. According to the IEA, the integration of renewable energy into power systems is accelerating globally, creating sustained demand for reliable backup and storage solutions.

Category-wise Analysis

Battery Type Insights

Lead-acid batteries, specifically valve-regulated lead-acid (VRLA) variants, represent the dominant battery type in the global UPS battery market, holding approximately 40% revenue share. Despite the rapid ascent of lithium-ion technology, lead-acid batteries retain their leadership owing to substantially lower upfront acquisition costs, a mature and globally distributed supply chain, and deep-rooted familiarity among system integrators and end users.

In cost-sensitive applications, including small- to mid-scale commercial facilities, telecom towers, and industrial installations, lead-acid batteries remain the default choice. According to the Battery Power Magazine Industry Organization, lead-acid batteries are the most recycled product globally, with recycling rates exceeding 90%, thereby mitigating regulatory compliance burdens.

Application Insights

Data centers dominate the UPS battery market by application, accounting for approximately 60% of global revenue in 2026. The insatiable demand for uninterrupted computing power driven by cloud adoption, AI workload proliferation, and digital transformation across industries has made data centers the largest and fastest-growing UPS battery consumption segment. According to the IEA, global data center electricity consumption stood at approximately 415 TWh in 2024 and is projected to nearly double by 2030.

The relentless expansion of hyperscale facilities by Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, combined with the emergence of colocation and edge data centers, spreads sustained, large-scale demand for high-reliability UPS battery systems. Lithium-ion batteries are particularly favored in this segment due to their compactness and ability to support high-density power architectures.

Power Rating Insights

The 10-100 kVA power rating segment leads the global UPS battery market, accounting for approximately 35% of revenue. This segment's dominance reflects its versatility across a broad spectrum of applications from mid-size commercial offices and retail establishments to small-scale data centers, telecommunications facilities, and healthcare institutions.

Systems in the 10-100 kVA range offer a compelling balance between power capacity and cost-effectiveness, making them the most widely deployed UPS configuration globally. The proliferation of edge computing nodes, regional colocation facilities, and enterprise IT environments has reinforced demand for this power rating tier. Furthermore, technological advancements enabling modular UPS architecture within this segment allow scalable capacity expansion, aligning well with the evolving power requirements of modern digital infrastructure.

Regional Analysis

North America UPS Battery Market Trends & Analysis

North America represents the largest regional market for UPS batteries, led by the United States, which hosts the densest concentration of hyperscale data center infrastructure globally. According to the U.S. Department of Energy (DOE), U.S. data centres consumed approximately 183 TWh of electricity in 2024over 4% of total national electricity consumption, and this is projected to increase by 133% to 426 TWh by 2030.

Combined capital expenditure by Amazon, Microsoft, Google, and Meta on U.S. data center infrastructure surpassed US$ 425 billion in 2025, directly translating into massive procurement of UPS batteries. The robust regulatory framework for power reliability in healthcare, financial services, and defence sectors further underpins regional demand.

U.S. UPS Battery Market Size

Estimated at approximately US$ 1.8 Bn in 2026, driven by hyperscale data center investments, stringent uptime mandates, and accelerating lithium-ion adoption. The U.S. federal government's prioritization of data center development as a national security and economic competitiveness imperative reflected in permitting incentives and defence procurement mandates creates a stable long-term demand environment.

Europe UPS Battery Market Trends, Drivers, & Insights

Europe represents a strategically significant regional market for UPS batteries, underpinned by robust regulatory harmonization and a strong sustainability imperative. The European Union's Energy Efficiency Directive and RoHS compliance frameworks drive systematic upgrades of legacy lead-acid UPS installations toward cleaner and more efficient lithium-ion alternatives.

The European Union's commitment to achieving carbon neutrality by 2050, combined with the European Green Deal, is accelerating the transition from VRLA to lithium-ion UPS batteries, which offer a lower environmental footprint and longer service life. IEA projections indicate European data center electricity consumption will grow by over 70% between 2024 and 2030, directly expanding the regional UPS battery addressable market. Regulatory harmonization through the EU Battery Regulation (2023/1542), which establishes lifecycle sustainability requirements for industrial batteries, is reshaping product development priorities for regional and global UPS battery manufacturers.

Germany UPS Battery Market Size

Estimated at approximately US$ 390 Mn in 2026, supported by industrial automation, Industrie 4.0, and data center expansion. Germany leads European demand, supported by its dense industrial base and the Industrie 4.0 digitalization initiative, which mandates high-reliability power backup for smart manufacturing environments.

U.K. UPS Battery Market Size

Estimated at approximately US$ 310 Mn in 2026, led by financial services sector demand and London-centric colocation growth. The United Kingdom is experiencing strong UPS battery demand growth, particularly in financial services and colocation data centers concentrated around London.

France UPS Battery Market Size

Estimated at approximately US$ 240 Mn in 2026, driven by national data sovereignty investments and industrial electrification. France and Spain are investing heavily in AI-ready data center infrastructure as part of national digital sovereignty strategies, creating new procurement cycles for advanced UPS batteries.

Asia Pacific UPS Battery Market Drivers & Analysis

Asia Pacific is the dominant regional market, accounting for approximately 33% of global UPS battery revenues in 2024, and it is expected to maintain the highest regional CAGR through 2033. China remains the largest country-level market, driven by its massive data center buildout, accounting for approximately 49% of overall data center investments in the region and the continued expansion of telecommunications infrastructure.

China UPS Battery Market Size

Estimated at approximately US$ 1.1 Bn in 2026, underpinned by data center expansion and telecom infrastructure investment. The Chinese government's national digitalization policies and the New Infrastructure initiative have sustained strong demand for high-capacity UPS battery systems across commercial, industrial, and public-sector applications.

India UPS Battery Market Size

Estimated at approximately US$ 420 Mn in 2026, driven by rapid data center capacity addition and 5G rollout. India is the fastest-growing country market in the region; the country's data center capacity is projected to double from approximately 950 MW in 2024 to around 1,800 MW by 2026, according to industry sources.

Japan UPS Battery Market Size

Estimated at approximately US$ 330 Mn in 2026, supported by data center modernization and disaster resilience mandates. Japan represents a mature yet steadily growing market, with demand driven by data center modernization, disaster-resilience imperatives following frequent natural disasters, and the adoption of AI-ready infrastructure.

Competitive Landscape

The global UPS battery market exhibits a moderately consolidated structure, with a handful of global integrated solution providers including Schneider Electric, Eaton Corporation, Vertiv Group Corp., and Emerson Electric Co. Commanding significant combined revenue shares through comprehensive product portfolios and established OEM relationships. These incumbents are differentiating through integrated digital power management ecosystems, AI-enabled battery monitoring platforms, and energy-as-a-service business models.

The specialized battery manufacturers such as EnerSys, East Penn Manufacturing, GS Yuasa, and Exide Industries compete primarily on chemistry innovation, supply chain scale, and lifecycle services. The market is witnessing an accelerating trend toward strategic alliances between UPS system integrators and battery technology specialists, as well as mergers aimed at securing lithium-ion supply chains and smart BMS capabilities.

Key Developments:

- In January 2026, Schneider Electric announced a USD 180 million expansion of its lithium-ion UPS module plant in Bangalore, India, targeting 500 MWh annual capacity by Q4 2027.

- In December 2025, Eaton completed the acquisition of a 60% stake in South Africa-based PowerSync, gaining secondary-life battery integration expertise.

- In November 2025, Vertiv launched the UL 9540A-certified Liebert EXM LFP UPS, with first shipments totalling 22 MWh to 14 US hospital systems.

Companies Covered in UPS Battery Market

- Schneider Electric

- Eaton Corporation

- Vertiv Group Corp.

- Emerson Electric Co.

- Delta Electronics, Inc.

- Exide Industries Limited

- GS Yuasa International Ltd.

- East Penn Manufacturing Company

- EnerSys

- Vision Group

Frequently Asked Questions

The global UPS Battery Market is valued at US$ 7.8 Bn in 2026 and is projected to reach US$ 12.7 Bn by 2033, expanding at a CAGR of 7.2% between 2026 and 2033.

The primary demand drivers include the exponential expansion of hyperscale and edge data centres, rise in digitalization of industries, growing deployment of 5G telecommunications infrastructure, and increasing frequency of grid power disruptions.

Lead-acid batteries, specifically valve-regulated lead-acid (VRLA) variants, dominate the battery type segment with approximately 40% revenue share, owing to their lower upfront cost, mature supply chains, and over 90% global recycling rate.

The Asia Pacific UPS battery market dominated the global market with revenue share of 36.5% in 2026 and is expected to grow at a CAGR of 13.4% from 2026 to 2033.

Key players in the global UPS Battery Market include Schneider Electric, Eaton Corporation, Vertiv Group Corp., Emerson Electric Co., Delta Electronics, Inc., Exide Industries Limited, GS Yuasa International Ltd., East Penn Manufacturing Company, EnerSys, and Vision Group, among others.