- Energy Storage Solutions

- Building Automation Energy Harvesting Market

Building Automation Energy Harvesting Market Size, Share, and Growth Forecast 2026 - 2033

Building Automation Energy Harvesting Market by Energy Source (Solar Energy, Vibration & Kinetic Energy, Thermal Energy, Radio Frequency (RF)), Component Type (Energy Harvesting Transducers, Power Management ICs (PMICs)) Deployment Type (New Buildings (Greenfield / Smart Buildings), Retrofit / Existing Buildings), Building Type (Commercial Buildings, Residential Buildings, Industrial Buildings), Regional Analysis, 2026 - 2033

Building Automation Energy Harvesting Market Size and Trend Analysis

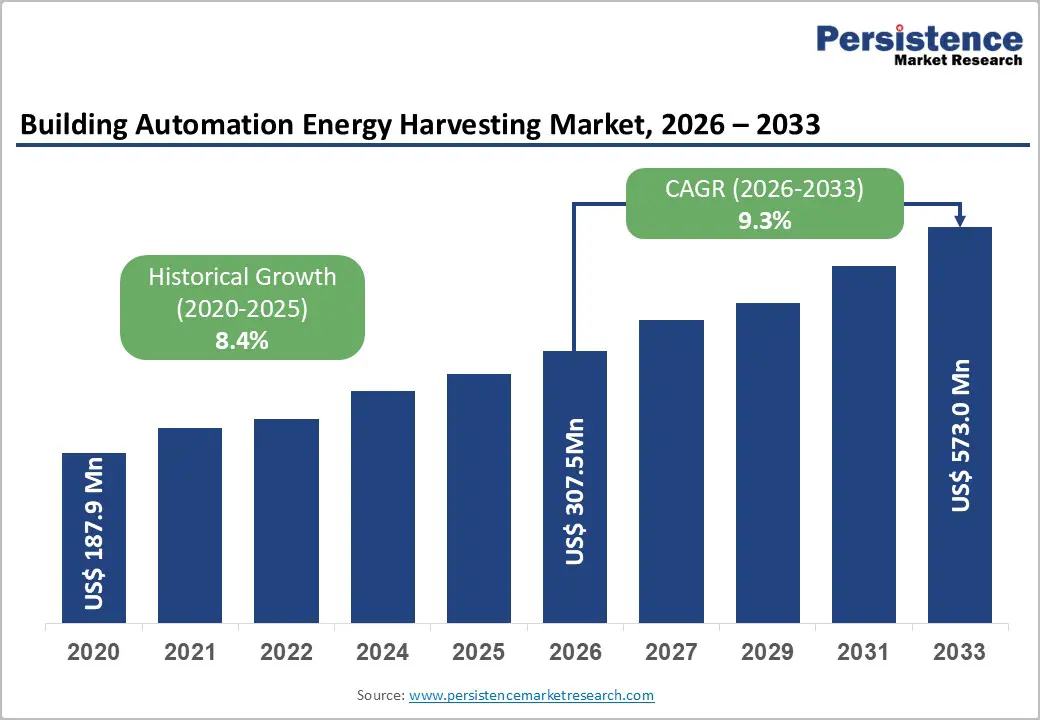

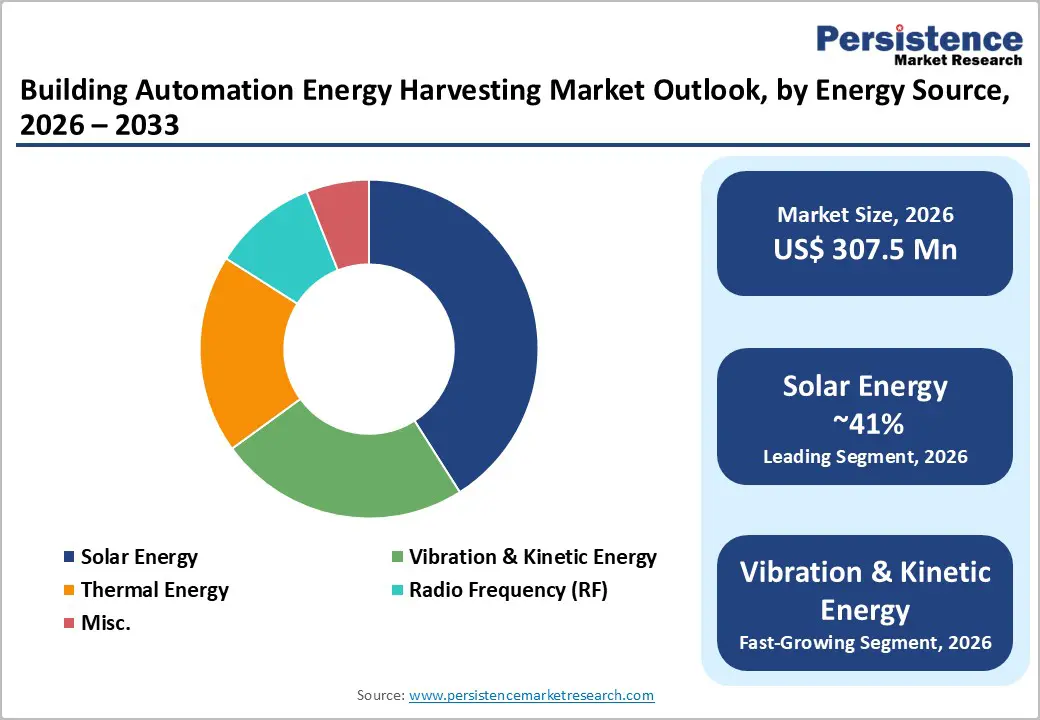

The global building automation energy harvesting market size is likely to be valued at US$ 307.5 million in 2026 and is projected to reach US$ 573.0 million by 2033, growing at a CAGR of 9.3% between 2026 and 2033 as buildings worldwide shift toward systems that generate and manage their own energy without relying on the grid.

This growth is driven by three distinct forces: policy pressure for greener buildings - carbon-reduction mandates across Europe, North America, and the Asia Pacific are pushing building owners to replace conventional energy-dependent systems with self-powered alternatives.

Falling component costs - the declining cost of solar and piezoelectric components has made energy-harvesting solutions affordable for routine commercial deployment.

Booming construction pipeline - the sheer scale of new construction, reflected in US$ 2.16 trillion in U.S. construction spending in 2024 and India's real estate market projected at US$ 5.8 trillion over the next two decades - is rapidly expanding the addressable base for these technologies.

As policy, economics, and construction activity align, energy harvesting for the building automation market is well positioned for sustained, long-term growth.

Key Industry Highlights:

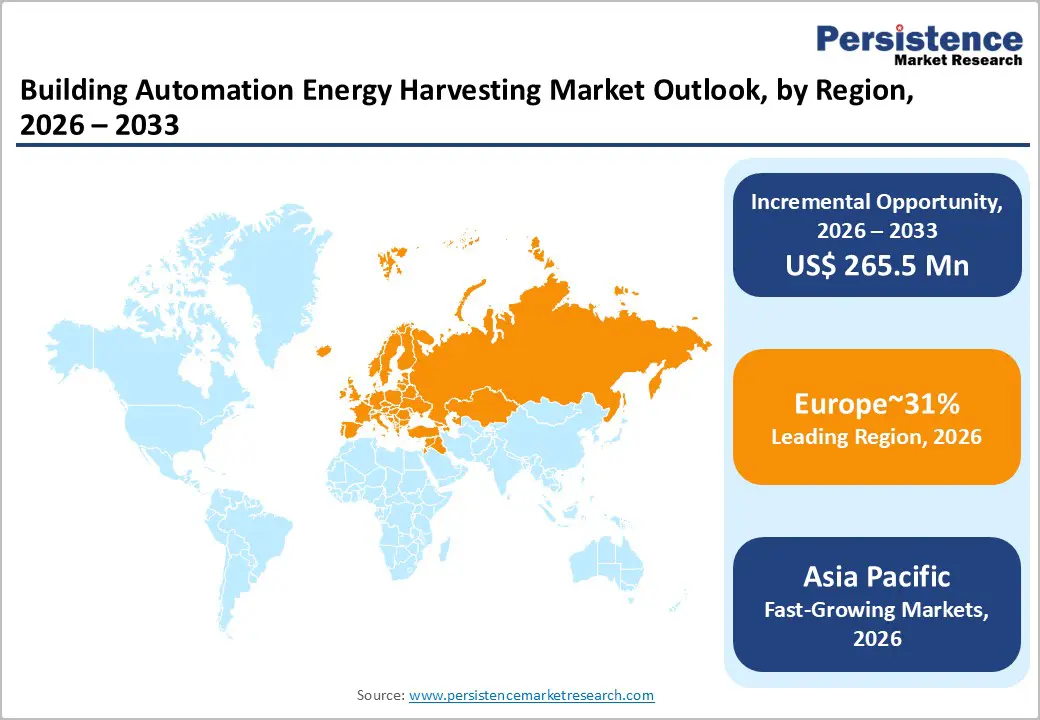

- Leading Region: Europe dominates the Building Automation Energy Harvesting Market with 31% share, driven by the EU’s Energy Performance of Buildings Directive, Renovation Wave targeting 35 million building upgrades by 2030, and strong retrofit-led smart building adoption across Germany, France, Spain, and Eastern Europe.

- Fast-growing Region: North America holds a 27% share, supported by the US$ 2.2 trillion U.S. construction market, a large-scale nonresidential building pipeline, and the rapid deployment of smart buildings integrated with energy-harvesting sensors across commercial, institutional, and industrial facilities.

- Leading Energy Source Segment: Solar Energy dominates with 41% share, supported by large-scale rooftop PV expansion (25M to 100M households by 2030), strong indoor photovoltaic adoption, and its high efficiency and maturity for powering building automation systems.

- Fastest-Growing Energy Source Segment: Vibration & Kinetic Energy is the fastest-growing segment, driven by industrial IoT expansion, smart factories, and demand for maintenance-free wireless sensors powered by machinery vibration and human movement in industrial buildings.

- Leading Deployment Type Segment: New Buildings (Greenfield / Smart Buildings) lead with 54% share, driven by mandatory integration of energy-harvesting systems in smart city megaprojects like NEOM, the high US and India construction pipelines, and rising adoption in commercial and institutional developments.

- Fastest-Growing Deployment Type Segment: Retrofit / Existing Buildings is the fastest-growing segment, driven by EU energy efficiency mandates, large-scale building modernization programs, and demand for battery-free wireless sensors enabling low-cost upgrades without structural rewiring.

DRO Analysis

Driver - Net Zero Building Mandates and Renewable Integration Targets Creating Structural Pull for the Building Automation Energy Harvesting Market

Stringent national and supranational net-zero building policy frameworks are the most consequential structural drivers of the building automation energy harvesting market, as regulators across all major economies mandate self-sufficient, low-carbon, and energy-efficient building systems that rely on harvested renewable energy rather than grid-dependent power. According to the International Energy Agency, the share of zero-carbon-ready buildings in the global building stock is projected to advance from less than 1% in 2020 to approximately 5% by 2030 and nearly 20% by 2050, each percentage point representing tens of millions of buildings requiring embedded energy harvesting infrastructure for autonomous sensor, control, and automation systems.

IEA further projects that heating and cooling energy consumption in new buildings will decline from a baseline index of 100 in 2020 to approximately 50 by 2030, driven by heat pump electrification, enhanced building envelopes, and fossil fuel heating phase-out, directly expanding the application envelope for thermal energy harvesting within building automation and HVAC control systems.

Global rooftop solar PV adoption is projected to scale from approximately 25 million installed households in 2020 to around 100 million by 2030 and nearly 240 million by 2050, providing the solar harvesting infrastructure base upon which building automation self-powering architectures are built.

Unprecedented Global Construction Activity Creating a New-Build Deployment Base

The scale and sustained momentum of global construction investment are directly expanding the addressable deployment base for the building automation energy-harvesting market, as new commercial, industrial, and institutional buildings are increasingly specified with energy-harvesting-enabled smart building automation systems from the design stage rather than retrofitted.

India's government increased capital expenditure by 11.1% to USD 133 billion in FY 2024 to 2025, equivalent to 3.4% of GDP, with the PMAY-U program sanctioning 1.18 crore housing units, generating a vast addressable market for building automation across both greenfield residential and commercial construction.

In Saudi Arabia and the UAE, Vision 2030 megaprojects, including NEOM and King Salman Park, are explicitly designed as smart city deployments, mandating battery-free, self-powered wireless sensor networks that draw directly on building automation energy harvesting technologies, with office construction averaging US$ 2,266 per square meter in Riyadh and US$ 1,334 per square meter in Dubai, providing the premium building investment context for advanced automation specification.

Global Energy Storage Investment and Grid Decentralization Accelerating Building-Level Energy Autonomy

The structural global investment shift toward distributed energy systems encompassing grid-scale and building-level battery storage, rooftop solar PV, and autonomous power management is directly strengthening the operational and economic case for energy-harvesting-based building automation by enabling buildings to function as self-contained energy micro-ecosystems rather than passive grid consumers. According to the IEA, global investment in battery energy storage exceeded USD 20 billion in 2022 and was projected to exceed USD 35 billion in 2023, with grid-scale battery storage capacity on track to expand nearly 35-fold between 2022 and 2030, reaching approximately 970 GW globally.

Restraints - High Upfront Integration Costs and Technology Maturity Barriers

Despite declining component costs, integrating energy-harvesting systems into building automation architectures remains capital-intensive relative to conventional wired or battery-powered sensor solutions, particularly in multi-protocol building management environments where interoperability engineering, system commissioning, and energy storage buffer sizing add significant project complexity.

Thermal energy harvesting and RF energy harvesting subsystems in particular remain at an early commercialization stage, with output power density and conversion efficiency parameters that restrict deployment to low-power sensor applications, limiting addressable automation use cases and constraining adoption among cost-sensitive building owners who prioritize short-term capital efficiency over long-term operational savings.

Supply Chain Concentration in Critical Materials and Semiconductor Components

The Building Automation Energy Harvesting Market faces structural supply chain vulnerabilities in critical materials and specialized semiconductor components, including piezoelectric ceramics, thermoelectric modules, and energy-harvesting microcontrollers that underpin system performance.

As the IEA has documented, supply chains for critical battery metals, including lithium, nickel, cobalt, and graphite, are heavily concentrated in a small number of geographies, with Russia's invasion of Ukraine disrupting the global supply of Class 1 nickel and cobalt in 2022, creating cascading cost and lead time pressures across adjacent energy component supply chains. Semiconductor supply constraints further limit the scale-up of specialized energy-harvesting integrated circuits, particularly low-power RF and vibration-harvesting front-end chipsets produced by a limited number of global foundries.

Opportunities - Building Retrofit and Energy Efficiency Upgrade Programmes as an Underserved Deployment Channel

The global retrofit and existing building upgrade market represents the largest structurally underserved demand channel within the building automation energy harvesting market, as billions of square meters of existing commercial, institutional, and industrial buildings require energy efficiency modernization without the disruption and cost of full rewiring or conduit installation, making battery-free, wirelessly networked energy harvesting sensors the technically optimal and economically superior retrofit automation solution.

The European Union's Energy Performance of Buildings Directive mandates near-zero energy standards for progressively broader categories of existing buildings, creating a regulatory compliance-driven retrofit automation market across all 27 member states. The EU construction sector recorded annual average output declines of 0.9% in the euro area in 2024, with Spain achieving 11.2% growth, Czechia 9.7%, and Slovakia 5.8%, reflecting divergent national retrofit and new-build activity levels that create geographically varied but collectively substantial opportunities for energy harvesting automation deployments targeted at energy performance compliance across southern and eastern European building stocks.

For market participants, developing standardized plug-and-play retrofit energy harvesting sensor kits with pre-configured EnOcean or Bluetooth Low Energy protocol stacks represents an actionable product strategy aligned directly with the compliance-driven retrofit demand pipeline.

Industrial Building Automation and Smart Manufacturing Facility Deployment

The industrial building segment represents a high-growth opportunity within the building automation energy harvesting market, driven by the convergence of Industry 4.0 digitalization, smart factory initiatives, and the requirement for dense, maintenance-free wireless sensor networks across manufacturing floors, warehouses, logistics hubs, and data center facilities where cable routing is costly, operationally disruptive, and incompatible with dynamic production floor reconfiguration.

India's warehousing market is projected to generate demand for 159 million square feet over the next two decades, offering direct deployment opportunities for vibration, thermal, and solar energy-harvesting-powered sensors to monitor temperature, humidity, equipment vibration, and occupancy parameters.

Latin America's data center and life sciences manufacturing construction pipeline, driven by nearshoring strategies across Brazil, Colombia, Chile, and Mexico, is generating new categories of industrial building automation demand, where energy-harvesting sensors can monitor precision environmental conditions, equipment performance, and security parameters without wired infrastructure.

Category-wise Analysis

Energy Source Insights

Solar energy commands 41% of the global building automation energy harvesting market by energy source, anchored by the technology's superior power density, predictable energy output in controlled indoor and outdoor building environments, and the deepest supply chain maturity of any harvesting technology, supported by declining solar PV component costs following decades of manufacturing scale-up.

IEA projections confirm that global rooftop solar PV adoption will advance from approximately 25 million households in 2020 to approximately 100 million by 2030, creating both a direct building-level harvesting deployment base and a powerful market normalization effect that accelerates specification of solar harvesting nodes in commercial building automation systems. The integration of indoor photovoltaic cells optimized for artificial-light spectra into wireless sensor nodes across commercial office, retail, and institutional buildings has further extended the applicability of solar harvesting beyond outdoor-exposed building surfaces into interior automation control points.

Vibration and kinetic energy harvesting is the fastest-growing energy source segment in the building automation energy harvesting market, driven by the rapid proliferation of industrial IoT monitoring applications that exploit ambient mechanical energy from HVAC equipment, structural vibrations, and human movement as power sources for maintenance-free wireless sensor nodes. This segment directly addresses the industrial building automation opportunity where rotating machinery, HVAC systems, and manufacturing equipment generate continuous vibration energy that can power predictive maintenance sensors without any external power supply or battery replacement logistics.

The combination of improved piezoelectric material efficiency, miniaturized power management ICs, and the cost imperative of eliminating battery maintenance in large-scale industrial sensor deployments is progressively shifting vibration harvesting from laboratory demonstrations to commercial-scale building automation deployments across manufacturing, logistics, and critical infrastructure facilities.

Development Mode Insights

New buildings (Greenfield / Smart Buildings) command 54% of the global building automation energy harvesting market by deployment type, as design-stage specification of energy harvesting automation systems in smart buildings, particularly across commercial, institutional, and mixed-use developments, delivers superior system integration, optimised sensor placement, and full building management system interoperability that maximizes energy harvesting performance and return on investment.

Saudi Arabia's Vision 2030 giga-projects NEOM, The Line, Diriyah Gate, and King Salman Park are among the highest-profile examples of new-build smart city deployments explicitly architected around battery-free, self-powered wireless building automation, while the US non-residential construction pipeline of US$ 1.25 trillion in 2024 and India's expanding smart city program collectively represent the new-build demand base underpinning segment leadership

Retrofit and existing buildings represent the fastest-growing deployment as regulatory-driven energy performance upgrade mandates, combined with the operational superiority of wireless, battery-free energy harvesting sensors for disruptive-free installation in occupied buildings, create a compelling value proposition for existing building owners seeking automation modernization without costly infrastructure works.

The EU's Energy Performance of Buildings Directive, alongside national energy efficiency programs in the United States, UK, and Japan, is generating retrofitting activity across commercial and public building stocks that directly benefits energy harvesting automation providers. In Canada, institutional and governmental construction permits surged 31.5% month-over-month in December 2025 and 24.9% year-over-year reflecting the scale of public building upgrade investment that creates retrofit energy harvesting automation opportunities across schools, hospitals, and government facilities.

Building Type Insights

Commercial buildings command approximately 52% of the building automation energy harvesting market by building type, reflecting the segment's combination of dense sensor deployment requirements, high energy management value, large average floor plate sizes creating economies of scale in wireless harvesting sensor networks, and strong sustainability certification drivers, including LEED, BREEAM, and WELL, that incentivize self-powered automation adoption. US commercial construction spending reached US$ 143.0 Mn in 2024 the highest level on record while Canada recorded a 25.8% year-over-year increase in commercial construction permits in December 2025, reflecting the sustained capital allocation into new and upgraded commercial buildings that directly supports energy harvesting automation deployment at scale.

Industrial Buildings are the fastest-growing building type in the building automation energy harvesting market, driven by the structural shift toward smart manufacturing, logistics automation, and data centre proliferation that demands dense, maintenance-free wireless sensor networks capable of operating continuously in harsh electromagnetic and thermal environments where battery replacement is operationally impractical and costly.

India's warehousing demand of 159 million square feet by 2047 and Latin America's expanding data center and life sciences manufacturing construction pipeline, including high-specification projects across Brazil, Colombia, and Chile, represent the most dynamic industrial building energy harvesting growth markets outside the established North American and European geographies.

Regional Insights

Asia Pacific Building Automation Energy Harvesting Market Trends and Insights

Asia Pacific holds 26% of the global building automation energy harvesting market, led by China at US$ 30.4 Mn and India at US$ 11.2 Mn, the region's two contrasting market archetypes of scale-led deployment and high-velocity greenfield growth, respectively. China's dominance is anchored in its unmatched smart building construction pipeline, having accounted for 60% of global new renewable capacity additions in 2023, and with solar PV generation projected to exceed total U.S. electricity demand by the early 2030s, creating a building-level solar harvesting deployment density unmatched globally.

China's November 2025 energy storage data revealed 39.5 GW of cumulative user-side energy storage installations, a 28% year-on-year advance, with Fujian province emerging as the top contributor, driven by energy-intensive industries including steel and chemicals, where building automation energy harvesting sensors for environmental and equipment monitoring represent a direct operational efficiency investment.

India, as the region's fastest-scaling market at US$ 11.2 Mn, is driven by the government's USD 133 billion capital expenditure commitment, PMAY-U housing programme, and the real estate market trajectory toward US$ 5.8 trillion by 2047 with sustainable construction practices including green buildings and energy-efficient technologies explicitly identified as strategic investment priorities by Indian government agencies.

North America Building Automation Energy Harvesting Market Trends and Insights

North America holds 27% of the global building automation energy harvesting market, with the United States at US$ 69.7 Mn representing the region's anchor market driven by the intersection of the world's largest non-residential construction pipeline, the most advanced grid-scale energy storage deployment program, and federal policy incentives that systematically reduce the relative cost of self-powered building automation relative to conventional grid-connected sensor architectures.

The U.S. construction sector recorded total annual spending of US$ 2.2 trillion in 2024, employing over 8.2 million people across 3.7 million construction businesses. The structural scale of this industry provides an unmatched greenfield deployment channel for energy harvesting and building automation across new commercial, institutional, and industrial buildings.

The preservation of the Investment Tax Credit under the One Big Beautiful Bill Act, combined with utility-scale storage capacity projections reaching 98 GW by 2030, is driving a distributed energy autonomy transition that directly elevates the strategic and economic appeal of energy harvesting building automation to commercial building owners and REITs managing large multi-site portfolios. Canada complements U.S. demand with institutional building permits up 24.9% year-over-year in December 2025 as school, hospital, and government facility upgrade programmes incorporate wireless, battery-free sensor networks for energy performance monitoring and compliance reporting under national sustainability building codes.

Europe Building Automation Energy Harvesting Market Trends and Insights

Europe holds the highest regional share at 31% of the Global Building Automation Energy Harvesting Market, anchored by the most stringent regulatory framework for building energy performance globally, the EU's Energy Performance of Buildings Directive, nearly-zero energy building mandates, and the Renovation Wave strategy targeting 35 million building renovations by 2030.

EU construction output in December 2024 showed 0.4% month-on-month growth in the EU, with Spain recording an exceptional 11.2% annual output advance, Czechia at 9.7%, and Slovakia at 5.8%, reflecting geographically divergent but collectively robust building investment activity that sustains energy harvesting automation deployment demand across both new construction and retrofit channels.

Poland, Czechia, and Portugal recorded the strongest monthly construction output gains in December 2024 at 5.7%, 4.6%, and 3.6%, respectively, identifying Eastern and Southern Europe as the region's highest-activity building construction markets, where energy-harvesting automation specifications are progressively embedded in smart building project documentation requirements. IEA projections confirm that solar thermal and geothermal system adoption in buildings will advance from 2% in 2020 to approximately 8% by 2030, creating a thermal-harvesting adoption tailwind that is structurally stronger in Europe than in any other region due to its advanced regulatory and incentive environment.

Competitive Landscape

The global building automation energy harvesting market exhibits a fragmented competitive structure, with no single player commanding dominant market concentration across all energy harvesting modalities, building types, and geographies. Leading players, including EnOcean GmbH, ABB, Honeywell International, STMicroelectronics, and Texas Instruments, hold the highest technology recognition and system integration capability but collectively serve different sub-segments: EnOcean in wireless sensor protocol, ABB and Honeywell in integrated building management systems, and STMicroelectronics and Texas Instruments in energy harvesting semiconductor components.

Competitive positioning is primarily differentiated by harvesting technology breadth, building protocol interoperability, certified partner ecosystem depth, and demonstrated project reference base across commercial and industrial deployments.

Leading players in the Building Automation Energy Harvesting Market pursue technology platform integration, certified partner ecosystem development, and performance contracting business models as their dominant strategic themes. Key differentiators include multi-source harvesting IC integration, open-protocol sensor interoperability, and regulatory compliance documentation support for LEED and BREEAM certification. Subscription-based building energy monitoring services combining energy harvesting sensor networks with cloud-based analytics are emerging as the primary business model evolution, converting hardware sales into recurring managed service revenue streams.

Key Developments:

- In January 2024, EnOcean GmbH introduced the PTM 216B Bluetooth® energy harvesting module featuring an advanced kinetic energy harvester and enhanced wireless range, enabling battery-free, flexible lighting control and building automation applications, thereby strengthening the adoption of maintenance-free energy harvesting solutions in ambient IoT environments.

- In April 2020, EnOcean GmbH launched the STM 550 solar-powered multisensor integrating temperature, humidity, light, motion, and magnetic sensing in a single battery-free device, enabling maintenance-free, wireless building automation solutions and accelerating adoption of energy harvesting technologies in smart and IoT-enabled buildings.

Companies Covered in Building Automation Energy Harvesting Market

- EnOcean GmbH

- Honeywell International Inc.

- STMicroelectronics NV

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- ZF Friedrichshafen AG

- Fujitsu Limited

- Cedrat Technologies

- Laird Connectivity

- Powercast Corporation

- Mide Technology Corporation

- Perpetua Power

- Advanced Linear Devices, Inc.

Frequently Asked Questions

The global building automation energy harvesting market is projected to be valued at US$ 307.5 Mn in 2026.

Solar Energy leads by energy source at 41% share, driven by IEA-projected solar thermal and geothermal building adoption reaching 8% of global building stock by 2030; Vibration and Kinetic Energy is the fastest-growing source, propelled by industrial IoT predictive maintenance sensor demand across manufacturing and logistics buildings.

Commercial buildings command approximately 52% by building type, supported by US commercial construction spending reaching a record US$ 143.0 Bn in 2024; Industrial Buildings are the fastest-growing type, driven by India's 159 million square feet warehousing demand pipeline and Latin America's data centre and life sciences manufacturing construction expansion.

The building automation energy harvesting market is expected to witness a CAGR of 9.3% from 2026 to 2033.

The building automation energy harvesting market growth is driven by stringent global net-zero building mandates, rapid expansion of smart and energy-efficient construction, and increasing adoption of distributed renewable energy systems and storage that enable self-powered, autonomous building automation infrastructure.

The key opportunities in the building automation energy harvesting market are driven by large-scale building retrofit and energy efficiency upgrade programmes, rapid growth in industrial and smart manufacturing facilities requiring wireless sensor networks, and the expansion of solar thermal and geothermal-integrated buildings enabling advanced thermal energy harvesting applications in automation systems.

Key players in the Building Automation Energy Harvesting Market include EnOcean GmbH, ABB, Honeywell International, STMicroelectronics, and Texas Instruments.