- Energy Storage Solutions

- Stationary Battery Storage Market

Stationary Battery Storage Market Size, Share, and Growth Forecast 2026 - 2033

Stationary Battery Storage Market by Battery Type (Lithium-Ion Batteries, Lead-Acid Batteries, Sodium-Sulfur Batteries, Flow Batteries, Solid-State Batteries, Others), Application (Grid Services (Frequency Regulation, Peak Shaving, Load Shifting, Renewable Integration), Behind-the-Meter (BTM), Off-Grid / Remote Systems), Energy Capacity (Up to 250 kWh, 251 kWh-1 MWh, 1.1-10 MWh, Above 10-20 MWh), and Regional Analysis for 2026 - 2033

Stationary Battery Storage Market Size and Trend Analysis

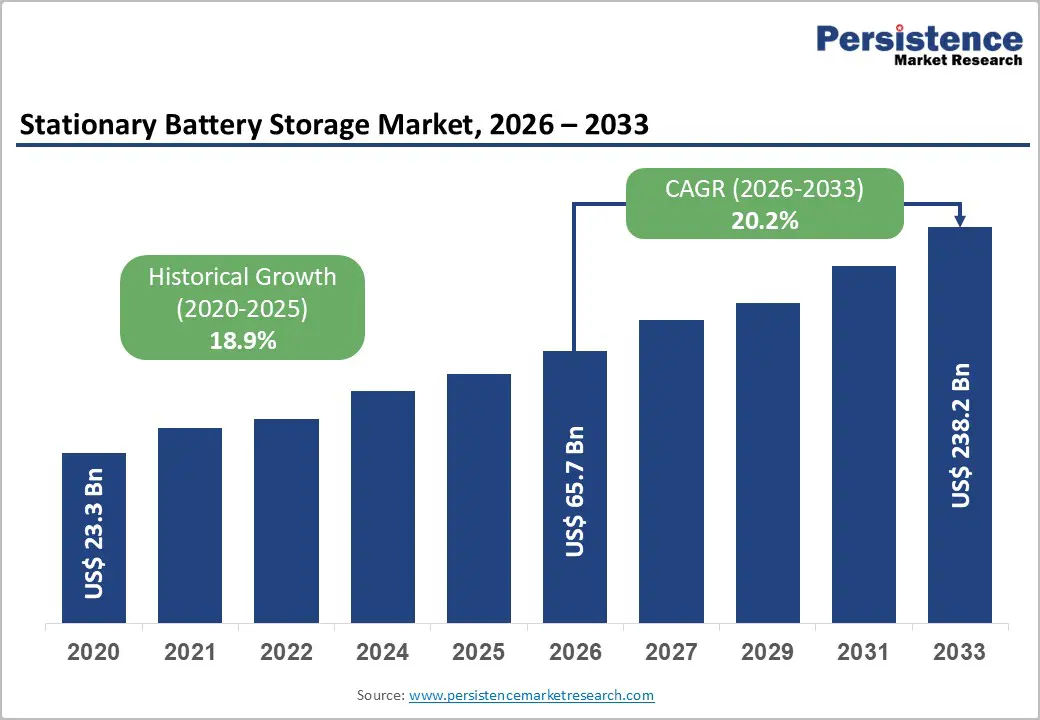

The global stationary battery storage market size is valued at US$ 65.7 Bn in 2026 and is projected to reach US$ 238.2 Bn by 2033, growing at a CAGR of 20.2% between 2026 and 2033.

This exceptional trajectory is driven by the convergence of mandatory renewable energy integration targets, rapidly declining battery costs, and unprecedented policy investment commitments, all of which are structurally accelerating the deployment of utility-scale and behind-the-meter battery energy storage systems (BESS) globally.

According to the International Energy Agency (IEA) Electricity 2026 report, utility-scale battery storage additions reached a record 63 GW globally in 2024, bringing total installed capacity to 124 GW, representing a 12-fold increase in power capacity between 2020 and 2024, while global average battery costs fell 58% from US$ 511 per kWh in 2019 to approximately US$ 213 per kWh in 2024, making BESS deployment economically compelling across virtually all grid and behind-the-meter applications.

Key Industry Highlights:

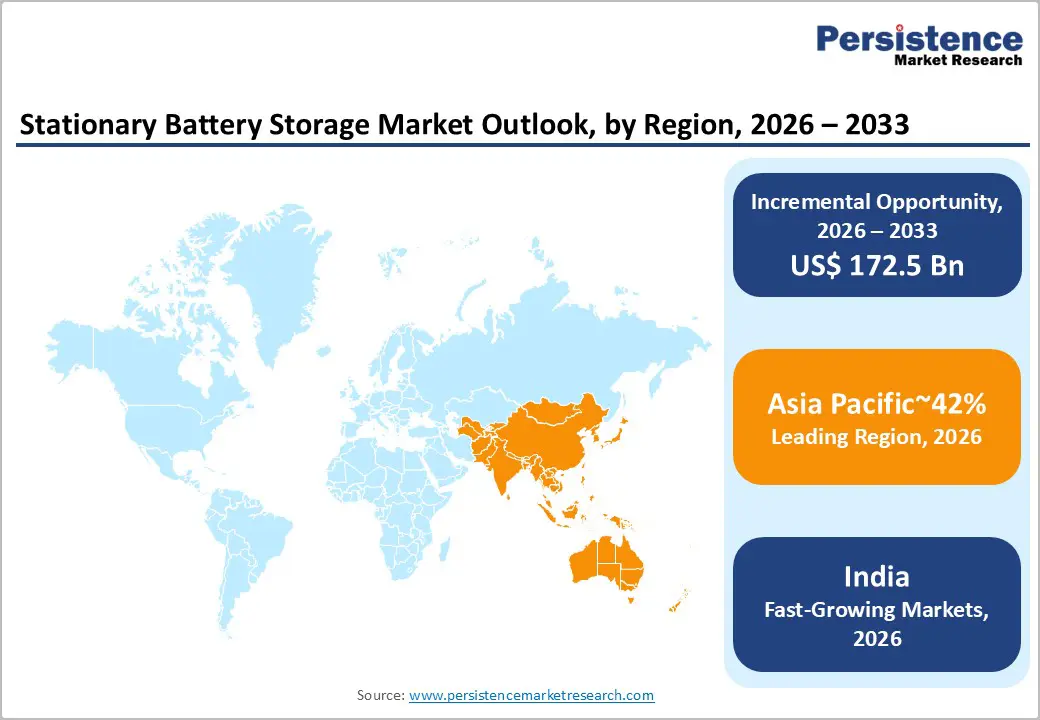

- Leading Region: Asia Pacific, led by China's CATL commanding 40% global market share and India's 92 GWh BESS pipeline, is the world's dominant stationary battery storage region, with the largest installed capacity base and highest concentration of new manufacturing investment through 2033.

- Fastest Growing Region: India is the fastest-growing sub-regional market, with its BESS project pipeline growing from 19 GWh in 2024 to 92 GWh in early 2025, supported by the government's Viability Gap Funding program and Ember Energy's analysis confirming solar-plus-storage competitiveness for 90% of national electricity demand.

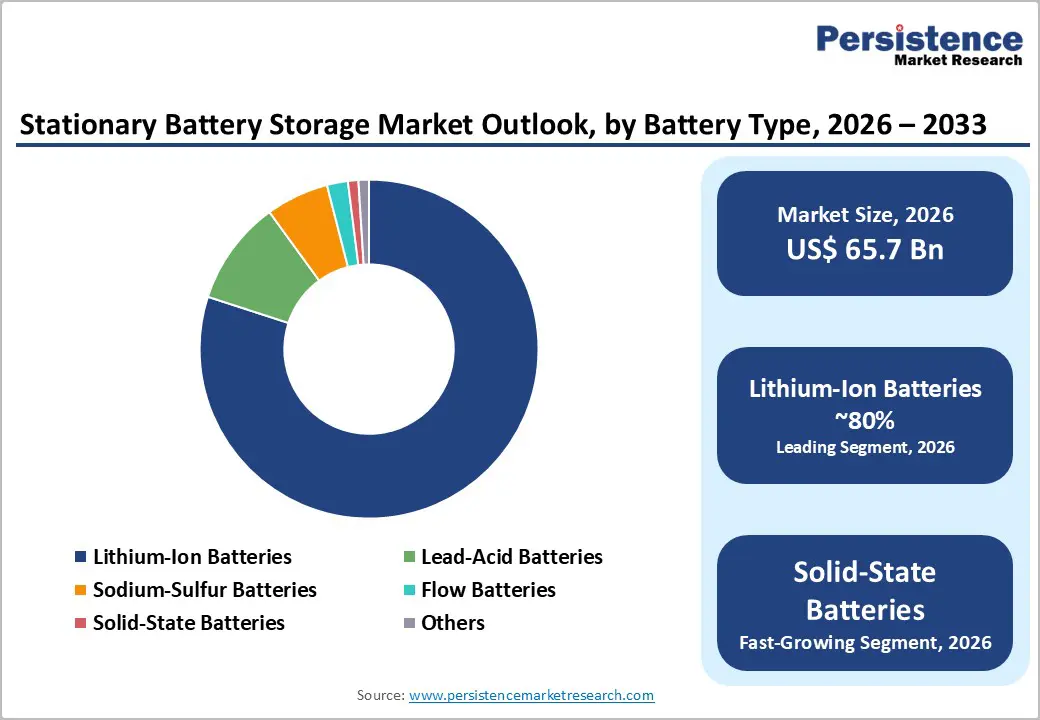

- Dominant Segment: Lithium-Ion Batteries dominate the battery type category, accounting for approximately 80% of the global Stationary Battery Storage market revenue. They are led by LFP chemistry, delivering 4,000-6,000 cycle lifetimes, industry-leading cost competitiveness below US$ 213 per kWh, and proven scalability from residential to utility-scale grid applications.

- Fastest Growing Segment: Long-Duration Energy Storage (LDES) within the Above 10-20 MWh capacity tier is the fastest-growing sub-segment, driven by the U.S. DOE's Long-Duration Storage Shot initiative and the IEA's mandate for global storage to reach 1,500 GW by 2030, a sixfold increase from 2024, requiring multi-hour grid storage at unprecedented scale.

- Key Market Opportunity: The EU's ReFuelEU renewable integration mandate, the IRA's standalone 30% ITC, and India's Viability Gap Funding program collectively define the most accessible high-growth BESS policy opportunities, enabling companies with compliant, cost-competitive products to capture long-term, policy-guaranteed procurement contracts from utility and government buyers through 2033.

| Key Insights | Details |

|---|---|

| Stationary Battery Storage Market Size (2026E) | US$ 65.7 Bn |

| Market Value Forecast (2033F) | US$ 238.2 Bn |

| Projected Growth CAGR (2026 - 2033) | 20.2% |

| Historical Market Growth (2020 - 2025) | 18.9% |

DRO Analysis

Market Growth Drivers

Accelerating Renewable Energy Integration: Creating Compulsory BESS Demand at Grid Scale

The global transition to renewable energy, led by solar and wind generation, is the foremost structural driver of stationary battery storage demand, as intermittent generation sources require co-located or contracted storage capacity to ensure grid stability, frequency regulation, and dispatchable power supply. According to the IEA-PVPS Snapshot of Global PV Markets 2025, global cumulative solar PV capacity reached at least 2,247 GW by the end of 2024, with 554-602 GW of new capacity added in that year alone.

The IEA has set a global target of tripling renewable energy capacity by 2030, which will require global battery storage capacity to increase a further sixfold to 1,500 GW, from approximately 124 GW in 2024, creating an enormous compulsory demand pipeline for BESS deployment.

Wind and solar project developers are increasingly mandating co-located battery storage as a project bankability requirement for grid connection approval, as demonstrated by renewable energy zones in Australia, California, and the United Kingdom. This renewable integration imperative is self-reinforcing: each additional gigawatt of variable renewable energy capacity commissioned increases the economic value and operational necessity of each additional gigawatt of battery storage, creating a durable and accelerating demand cycle.

Transformational U.S. Policy Incentives Quadrupling Domestic Energy Storage Pipeline

The U.S. Inflation Reduction Act (IRA) of 2022 has fundamentally restructured the economics of stationary battery storage deployment in North America, creating a policy-backed growth wave with global repercussions. The IRA introduced a standalone Investment Tax Credit (ITC) of 30% under Section 48 for battery energy storage systems with a minimum capacity of 5 kWh, the first time U.S. energy storage qualified for standalone ITC support independent of solar co-location. Additional stackable adders push the effective ITC to as high as 70% for projects meeting domestic content and energy community requirements.

The 45X Manufacturing Production Tax Credit provides US$35 per kWh for battery cell production and US$10 per kWh for battery pack assembly, directly incentivizing domestic manufacturing scale-up. The U.S. Department of Energy (DOE) has confirmed that the energy storage pipeline quadrupled following the IRA's passage: the pre-IRA forecast of 50 GW of storage by 2040 has been revised to over 200 GW post-IRA. This regulatory transformation is drawing tens of billions in BESS manufacturing and project investment into the United States, establishing a second global growth center for stationary battery storage alongside China.

Market Restraints

Supply Chain Concentration in China Creating Geopolitical and Security Risk

The global stationary battery storage supply chain is heavily concentrated in China, which dominates lithium-ion battery cell production, key material refining, including lithium, cobalt, and manganese, and BESS system integration. The IEA Electricity 2026 report explicitly identifies this supply chain concentration as a critical risk: "Much of the world's battery supply chains are concentrated in China, creating considerable risks in terms of supply security, given the growing role batteries play across energy systems and the wider economy."

This geographic concentration exposes non-Chinese buyers to geopolitically driven supply disruptions, export control risk, and price manipulation, and is limiting BESS project bankability in markets with domestic content requirements under frameworks such as the U.S. IRA's 45X credit. Diversifying supply chains requires years of upstream investment and the development of processing capacity, constraining near-term market acceleration.

Grid Connection Delays and Permitting Bottlenecks Slowing Project Deployment

Despite unprecedented investment intent, global deployment of stationary battery storage is systematically constrained by multi-year delays in securing grid connection approvals and permitting clearances. The IEA Electricity 2026 report identifies grid connection delays as a "universal challenge" across all major markets. In Germany, grid connection requests for BESS projects surged from 300 GW to over 500 GW in a single year, vastly overwhelming transmission system operator processing capacity.

In the United States, the Federal Energy Regulatory Commission (FERC) has acknowledged a massive interconnection backlog, with over 2,600 GW of project requests pending, that imposes multi-year delays in storage commissioning. These bottlenecks translate directly into delayed revenue realization, increased financing costs, and deferred capacity additions, acting as a meaningful drag on the market's realization of its structural demand potential.

Market Opportunities

Long-Duration Energy Storage (LDES): The Next Frontier for Grid Decarbonization

Long-Duration Energy Storage (LDES), defined as battery systems capable of discharging for 8 hours or more, represents one of the most strategically important and commercially promising growth opportunities for stationary battery storage market participants over the 2026-2033 forecast horizon. As renewable energy penetration pushes beyond 50-70% of total grid generation in leading markets, the demand for storage capable of shifting energy across daily, weekly, and seasonal cycles, not merely the 2-4 hour duration window addressed by current mainstream BESS, will intensify dramatically. Flow batteries, sodium-sulfur batteries, and next-generation solid-state systems are all positioned to serve LDES applications.

According to IDTechEx, batteries with higher storage durations are seeing "the most rapid cost declines" globally, with Australian grid operators already targeting systems designed for 2.5+ hours of sustained discharge, rising from 1.5 hours in 2024. The U.S. DOE's Long-Duration Storage Shot initiative aims to reduce the cost of LDES systems by 90% within a decade, creating a policy-backed commercialization pathway. Companies that develop LDES-capable flow or hybrid battery technologies with superior levelized cost of storage (LCOS) profiles will access a high-value, differentiated market segment underserved by today's dominant lithium-ion technology stack.

India and ASEAN's Energy Storage Scale-Up: A High-Growth Emerging Market Opportunity

India and the broader ASEAN region represent a transformational emerging market opportunity for stationary battery storage manufacturers and project developers, underpinned by aggressive government procurement programs, rapidly expanding renewable capacity targets, and significant off-grid electrification demand. India's BESS deployment pipeline stood at 92 GWh as of early 2025, growing by 74 GWh in a single year from just 19 GWh in 2024, with the government's Viability Gap Funding (VGF) program allocating support for up to 4 GWh of BESS deployment as a direct capital subsidy. According to an analysis by Ember Energy, battery storage has become sufficiently affordable to enable 90% of India's electricity demand in 2024 to have been met by solar-plus-storage at a competitive cost, marking a fundamental inflection point in India's storage market economics.

ASEAN nations, particularly Vietnam, Indonesia, Thailand, and the Philippines, are simultaneously expanding solar capacity and confronting grid instability challenges that position BESS as a critical infrastructure investment. For global manufacturers including CATL, BYD, LG Energy Solution, and Samsung SDI, early market-entry partnerships, technology licensing agreements, and localized manufacturing investments in the India-ASEAN corridor represent a high-return, long-duration commercial opportunity.

Category-wise Analysis

Battery Type Insights

Lithium-Ion Batteries dominate the battery type category, commanding approximately 80% of total global Stationary Battery Storage market revenue. This overwhelming leadership is grounded in lithium-ion's unmatched combination of high energy density, cycle life exceeding 4,000-6,000 cycles for LFP (Lithium Iron Phosphate) chemistry, declining cost trajectory, and proven scalability across residential, commercial, and utility-scale BESS applications. According to IDTechEx, global lithium-ion battery deployment for stationary energy storage reached 10% of total Li-ion demand by 2023, with the stationary sector growing its share consistently as EV battery manufacturing scale drives cost reductions that accrue directly to BESS economics.

The IEA has confirmed that global Li-ion battery deployment in 2025 was six times higher than in 2020, reflecting the compound effects of manufacturing scale, chemistry optimization, and policy incentive support. The increasing dominance of LFP chemistry in lithium-ion BESSs, offering superior thermal stability, lower cost per kWh, and longer calendar life than NMC, is reinforcing the segment's technological leadership across grid-scale applications.

Application Insights

Grid Services is the dominant application segment, accounting for approximately 64% of the total global Stationary Battery Storage market revenue. Grid services, encompassing frequency regulation, peak shaving, load shifting, and renewable energy integration, represent the highest-volume and most financially scalable application for stationary battery storage, driven by utility procurement mandates, capacity market participation, and wholesale energy market monetization.

The IEA has confirmed that utility-scale battery storage additions reached a record 63 GW globally in 2024, with grid services applications comprising the dominant deployment category. Frequency regulation, where BESS provides near-instantaneous response to grid frequency deviations, commands premium pricing in markets including PJM Interconnection, ERCOT, National Grid UK, and AEMO Australia. Renewable integration, peak shaving, and transmission deferral are driving utilities to accelerate BESS procurement as coal and gas peaker plant retirements accelerate across Europe, North America, and Australia.

Energy Capacity Insights

The Above 10-20 MWh energy capacity segment leads the market, accounting for approximately 45% of total global Stationary Battery Storage market revenue. This dominance reflects the rapid scaling of utility-scale BESS projects at the grid tier, where system sizes ranging from tens of megawatt-hours to multi-hundred-megawatt-hours are the norm for frequency regulation, renewable firming, and peaker replacement applications. Large-capacity systems deliver significantly lower levelized cost of storage (LCOS) per kWh due to shared balance-of-plant infrastructure, centralized battery management systems, and volume procurement economics.

Tesla's Megapack, with individual unit capacity of 3.9 MWh and multi-unit project configurations in the hundreds of MWh, and BYD's HaoHan system, unveiled in September 2025 with approximately double the Megapack's capacity, exemplify the industry's direction toward progressively larger capacity building blocks. Grid operators across the United States, Australia, and China are exclusively specifying large-capacity configurations for new grid service contracts, reinforcing this segment's dominant commercial position.

Regional Analysis

North America Stationary Battery Storage Trends

The United States is the world's fastest-growing major national market for stationary battery storage, driven by the transformative economic incentives of the Inflation Reduction Act (IRA), record renewable energy procurement, and the retirement of thermal peaker plant capacity. The U.S. DOE confirmed that the domestic energy storage pipeline quadrupled post-IRA, with the deployment forecast for 2040 revised from 50 GW pre-IRA to over 200 GW post-IRA. The standalone 30% ITC for BESS under Section 48, extendable to 70% with domestic content and energy community adders, has attracted multi-billion-dollar manufacturing investments from CATL, Tesla, Panasonic, and LG Energy Solution. California alone, under its Resource Adequacy rules, mandates four-hour battery storage for capacity value recognition, driving the largest single-state BESS procurement pipeline globally.

Canada contributes through provincial clean energy initiatives, particularly Ontario's IESO capacity market procurement and British Columbia Hydro's grid modernization programs, and is expanding its manufacturing base for battery components with support from the Government of Canada's Clean Technology Investment Tax Credit. The U.S.-Canada shared grid interconnection and the integrated nature of the Western and Eastern Interconnections mean that BESS deployments on either side of the border contribute to mutual grid reliability, creating a North American continental BESS demand ecosystem. North America is forecast to sustain its position as the world's second-largest stationary battery storage market through 2033, behind only the Asia Pacific.

Europe Stationary Battery Storage Trends

Europe is one of the world's most dynamic and rapidly expanding stationary battery storage markets, driven by the European Union's comprehensive clean energy regulatory framework, aggressive renewable energy targets, and the structural imperative of replacing retiring nuclear and coal generation capacity with flexible battery storage resources. The EU installed a record 27.1 GWh of new battery storage capacity in 2025, a 45% year-over-year increase, with utility-scale BESS leading installations. Germany has emerged as the single largest and fastest-growing European BESS market, deploying over 3.5 GW of new capacity in 2024 alone, supported by 1.8 million residential and commercial battery storage units nationwide and over 1.8 GWh of grid-scale capacity. Grid connection requests for BESS in Germany surged from 300 GW to over 500 GW in a single year, indicating the extraordinary depth of the pipeline.

The United Kingdom operates Europe's most mature capacity market, with National Grid ESO procuring BESS through Balancing Mechanism contracts and capacity market auctions. France and Spain are accelerating BESS deployment through the EU Innovation Fund and national grid flexibility programs, in line with the REPowerEU Plan's storage deployment objectives. Europe's combined regulatory trajectory, including the EU Battery Regulation 2023/1542 (requiring lifecycle CO2 disclosure and recycled content mandates), Grid Codes harmonization under the Internal Electricity Market Directive, and the European Green Deal, is creating both the regulatory demand certainty and technical standards framework that commercial BESS investors require for long-term project financing.

Asia Pacific Stationary Battery Storage Trends

Asia Pacific is the world's dominant region for stationary battery storage, led by China, which is simultaneously the largest BESS manufacturer and the fastest-growing deployment market globally. CATL has ranked first globally in energy storage battery deliveries since 2021, with energy storage battery sales growing from 12.5% of its business in 2021 to 17.6% in 2023, while storage deliveries surged 46.8% in 2023 to 69 GWh. BYD's energy storage battery deliveries surged by 57% in 2023, significantly outpacing its EV battery growth.

The average duration of cumulative new-type energy storage installations in China increased from approximately 2.1 hours in 2021 to approximately 2.6 hours in 2025, reflecting the nation's progression toward longer-duration grid applications. Tesla's Megapack manufacturing facility in Shanghai, produced in partnership with CATL battery cells, is targeting 10,000 Megapacks annually, totaling 40 GWh in storage capacity for global export.

Japan contributes through advanced battery R&D, led by Panasonic, Toshiba, and GS Yuasa, and grid modernization investments under METI's (Ministry of Economy, Trade and Industry) capacity market and storage support programs. India's BESS pipeline reached 92 GWh in early 2025, supported by the government's Viability Gap Funding and the Ministry of New & Renewable Energy's grid storage procurement mandates. Australia is one of the world's leading per-capita BESS deployers, with state governments in South Australia, Victoria, and New South Wales commissioning multi-hundred-megawatt battery projects within their renewable energy zone frameworks.

Competitive Landscape

The global Stationary Battery Storage market is characterized by a moderately concentrated competitive structure at the cell manufacturing tier, dominated by CATL, BYD, LG Energy Solution, and Panasonic, and a more fragmented landscape at the system integration level, where hundreds of regional integrators compete alongside global OEMs. Key competitive differentiators include battery chemistry (LFP vs. NMC vs. emerging sodium-ion), system energy density improvements, battery management system (BMS) sophistication, safety certifications, and after-sale service capabilities.

CATL and BYD are aggressively expanding into vertically integrated stationary storage system products, threatening Tesla's Megapack leadership, while European and U.S. companies are competing through regulatory compliance, domestic content, and financing partnerships. Emerging competitive models include Storage-as-a-Service (SaaS) and battery leasing platforms.

Key Market Developments

- In September 2025, BYD unveiled its HaoHan stationary energy storage system, a direct competitor to Tesla's Megapack 3 with approximately twice the capacity per unit, marking a significant escalation in Chinese battery manufacturers' push into vertically integrated utility-scale BESS products for global markets.

- In January 2025, CATL commenced supplying battery cells and packs for Tesla's Shanghai Megapack manufacturing facility, which entered production targeting 10,000 Megapacks annually (40 GWh of storage capacity), intended for global export as a landmark stationary BESS supply chain partnership.

- In March 2024, The U.S. DOE confirmed that the domestic energy storage project pipeline had grown four-fold since the passage of the Inflation Reduction Act (IRA), with the national storage deployment forecast for 2040 rising from 50 GW pre-IRA to over 200 GW post-IRA, establishing the U.S. as a dominant second growth engine for global BESS demand.

Companies Covered in Stationary Battery Storage Market

- BYD

- CATL

- Exide

- GS Yuasa

- Hitachi

- Johnson Controls

- Leclanche

- LG

- Panasonic

- Samsung

- Siemens

- SK Innovation

- Tesla

- Toshiba

- Varta

Frequently Asked Questions

The global Stationary Battery Storage market is valued at US$ 65.7 Bn in 2026 and is projected to reach US$ 238.2 Bn by 2033, growing at a CAGR of 20.2% during the forecast period. This exceptional growth is underpinned by a 12-fold increase in global utility-scale battery capacity between 2020 and 2024 per IEA Electricity 2026, and policy-driven BESS investment commitments across the U.S., EU, China, and India.

The primary demand drivers are the compulsory global push for renewable energy integration, with the IEA requiring global battery storage to grow a further sixfold to 1,500 GW by 2030, and the U.S. Inflation Reduction Act's standalone 30% ITC for BESS, which quadrupled the U.S. domestic energy storage deployment pipeline from 50 GW to over 200 GW by 2040, per the U.S. DOE.

Lithium-Ion Batteries lead the battery type category with approximately 80% of global market revenue, driven by LFP chemistry's superior thermal safety, cycle life of 4,000-6,000+ cycles, and declining cost trajectory. By 2025, global Li-ion battery deployment was six times higher than in 2020 per the IEA, with LFP-based BESS from CATL and BYD defining the industry cost benchmark for grid-scale applications.

Asia Pacific leads the global Stationary Battery Storage market, anchored by China, where CATL commands approximately 40% global market share in energy storage battery deliveries, and BYD's storage deliveries grew 57% in 2023. China's average new-type energy storage installation duration has grown from 2.1 hours in 2021 to 2.6 hours in 2025, reflecting rapid progression toward long-duration grid applications.

Long-Duration Energy Storage (LDES) is the most significant emerging opportunity. The U.S. DOE's Long-Duration Storage Shot targets a 90% cost reduction for LDES within a decade, while the IEA identifies batteries with higher storage durations as seeing "the most rapid cost declines" globally. Flow batteries, sodium-sulfur, and solid-state systems capable of 8+ hour discharge will access a differentiated, premium-priced market underserved by mainstream lithium-ion configurations.

The global Stationary Battery Storage market is led by CATL, BYD, Tesla, Inc., LG Energy Solution, Samsung SDI, Panasonic Corporation, SK Innovation (SK On), Siemens Energy, Hitachi Energy, Toshiba Corporation, GS Yuasa Corporation, VARTA AG, Fluence Energy, Sungrow Power Supply, and Exide Technologies, among others.