- Energy Storage Solutions

- Energy Storage as a Service Market

Energy Storage as a Service Market Size, Share, and Growth Forecast 2026 - 2033

Energy Storage as a Service Market by Service Type (Bulk Energy Services, Ancillary Services, Transmission Infrastructure Services, Distribution Infrastructure Services, Customer Energy Management Services, Others), Deployment (On-grid, Off-grid), Application (Peak Shaving, Load Shifting, Renewable Energy Integration, Microgrid Support, Power Backup), End-user (Utility, Commercial & Industrial, Residential), by Regional Analysis, 2026 - 2033

Energy Storage as a Service Market Size and Trend Analysis

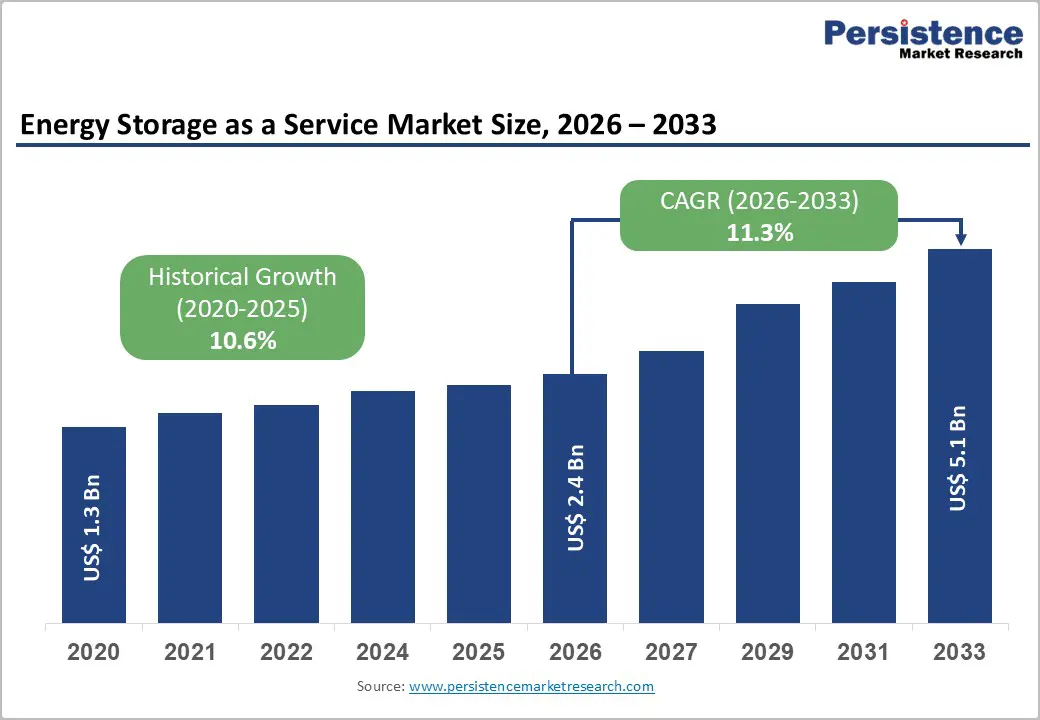

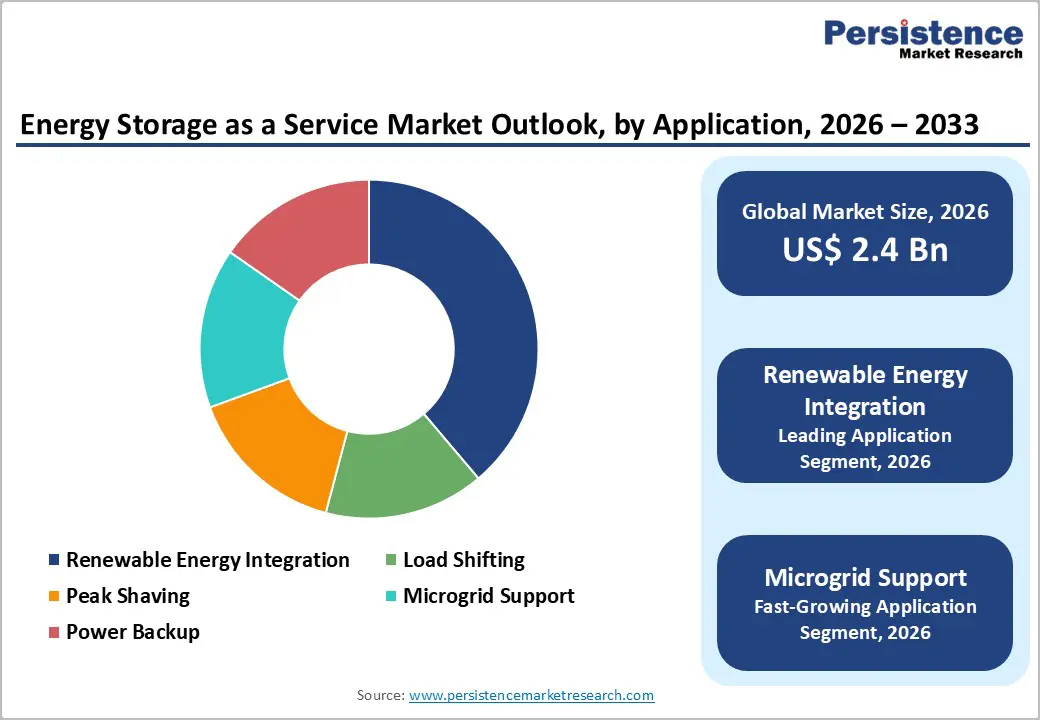

The global Energy Storage as a Service (ESaaS) market size is expected to be valued at US$ 2.4 billion in 2026 and is projected to reach US$ 5.1 billion by 2033, growing at a CAGR of 11.3% between 2026 and 2033.

The ESaaS model is rapidly displacing capital-intensive ownership models by offering businesses and utilities subscription-based, OpEx-friendly access to battery energy storage systems (BESS), advanced energy management platforms, and grid services, making energy flexibility accessible without upfront hardware costs. According to the Solar Energy Industries Association (SEIA), the U.S. alone installed a record 57.6 GWh of new battery storage capacity in 2025, a 29% year-on-year increase, underscoring the scale of infrastructure being created that underpins ESaaS contracts. Supporting evidence includes surging renewable energy penetration, escalating electricity price volatility, and mandates from regulatory bodies such as the U.S. Federal Energy Regulatory Commission (FERC) and the European Commission's Clean Energy for All Europeans Package, which collectively compel utilities and commercial users to deploy smart, dispatchable storage solutions.

Key Industry Highlights

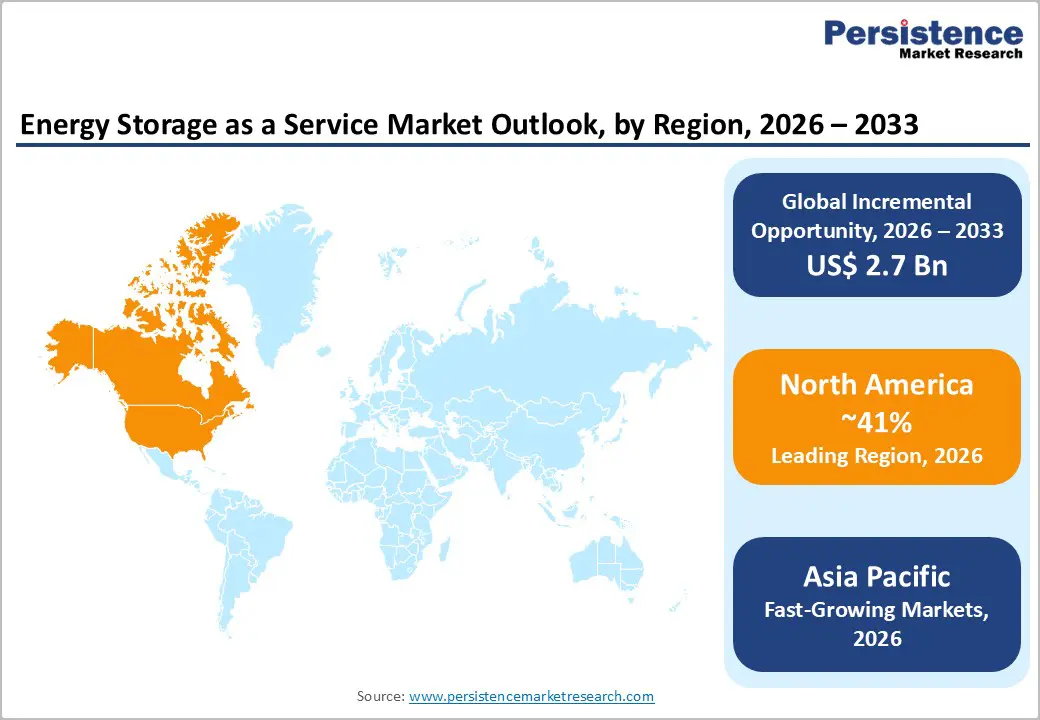

- Leading Region: North America leads the global ESaaS market with ~41% share in 2025, underpinned by the IRA's standalone storage investment tax credit, FERC Order 2222, and record U.S. BESS installations of 57.6 GWh in 2025, an annual record.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, powered by China's NEA co-location mandates, India's US$ 1.02 billion solar grid budget, and Japan's Green Growth Strategy, driving accelerating utility-scale ESaaS contract volumes through 2033.

- Dominant Segment rvices: Customer Energy Management Services holds ~33% of ESaaS service-type share in 2025, driven by AI-powered platforms, performance-contract demand from C&I customers, and demand charge reduction mandates.

- Fastest Growing Segment: Off-grid ESaaS deployments are the fastest-growing application segment, as the IEA identifies mini-grids as the optimal electrification pathway for nearly 490 million people, unlocking recurring subscription revenues in emerging markets.

- Key Market Opportunity: Vehicle-to-Grid integration and VPP aggregation represent a transformative opportunity, the DOE projects 80–160 GW of aggregated DER capacity by 2030, with ESaaS providers positioned as the operational backbone and monetization engine.

| Key Insights | Details |

|---|---|

|

Energy Storage as a Service Market Size (2026E) |

US$ 2.4 Billion |

|

Market Value Forecast (2033F) |

US$ 5.1 Billion |

|

Projected Growth CAGR (2026–2033) |

11.3% |

|

Historical Market Growth (2020–2025) |

10.6% |

Market Dynamics

Drivers - Accelerating Renewable Integration Driving Grid-Level Storage Demand

The surging global deployment of intermittent renewable energy is creating an acute structural need for dispatchable storage services. BloombergNEF forecasts global energy storage additions of 92 GW / 247 GWh in 2025, a 23% increase over 2024, and expects cumulative capacity to reach 2 terawatts (7.3 TWh) by 2035. The ESaaS model is uniquely positioned to absorb this capital demand: by transferring ownership, maintenance, and performance risk to service providers, it dramatically lowers the barrier for utilities, municipalities, and industrial users to deploy storage at scale.

The U.S. Inflation Reduction Act (IRA), 2022 introduced a standalone investment tax credit under Section 48 and 48E for energy storage facilities, directly improving the economics of ESaaS business models by reducing the provider's asset cost basis. The International Renewable Energy Agency (IRENA) estimates that over 1,500 GW of flexible storage capacity will be required globally by 2030 to support high-penetration renewable grids, a scale that only subscription-based service models can realistically achieve.

Rising Electricity Price Volatility and Corporate Decarbonization Mandates

Escalating energy costs and mandatory corporate sustainability reporting are driving Commercial & Industrial (C&I) customers to adopt ESaaS solutions as both a cost-management and compliance tool. Peak demand charges, which can represent up to 30–40% of commercial electricity bills in markets such as California, New York, and the United Kingdom, are a primary financial driver for subscribing to peak shaving and load-shifting storage services. According to the U.S. Department of Energy (DOE), virtual power plants (VPPs) leveraging aggregated storage assets could deliver 80–160 GW of flexible capacity by 2030, with ESaaS providers acting as critical aggregators. Simultaneously, the EU Corporate Sustainability Reporting Directive (CSRD) mandates that large European enterprises report and reduce their Scope 2 emissions from electricity consumption, making energy storage a critical tool for time-shifting renewable energy consumption and improving on-site carbon accounting.

Restraints - High Upfront Technology and Infrastructure Deployment Costs for Providers

Although ESaaS eliminates capital expenditure for end users, service providers must bear substantial upfront costs for battery systems, power electronics, monitoring software, and site integration. BloombergNEF estimates that U.S. four-hour turnkey battery system costs spiked to approximately US$ 266 per kilowatt-hour in 2025 following tariff increases on Chinese battery imports, a 30% inflation compared to pre-tariff baseline levels. For ESaaS providers, this erodes unit economics and lengthens payback periods, constraining the ability to offer highly competitive subscription pricing without adversely affecting project returns.

Regulatory Fragmentation and Grid Interconnection Complexity

A lack of standardized regulatory frameworks across states, regions, and countries creates significant friction for ESaaS market expansion. In the United States alone, interconnection rules vary by Independent System Operator (ISO), with projects in CAISO, ERCOT, and PJM facing structurally different market participation requirements. The U.S. FERC Order 2222, while enabling distributed energy resource aggregation, is still being implemented unevenly across ISOs, delaying revenue certainty for ESaaS aggregators. In Europe, similar fragmentation persists across member states' balancing markets, creating contract complexity for pan-European service providers.

Opportunity - Microgrid and Off-Grid Deployments in Emerging and Remote Markets

The rapid expansion of microgrids in remote industrial installations, island communities, and underserved emerging markets presents a substantial incremental revenue opportunity for ESaaS providers. Off-grid and edge-of-grid deployments, where reliability of supply is paramount and utility grid extension is economically impractical, are natural fits for the ESaaS contract model. The International Energy Agency (IEA) estimates that over 775 million people remain without access to electricity globally, with mini-grids and microgrids identified as the most cost-effective electrification pathway for more than 490 million of them.

In India, the Ministry of New and Renewable Energy (MNRE) contracted the country's largest BESS project through the Solar Energy Corporation of India (SECI) in February 2024, demonstrating government appetite for large-scale storage deployment. ESaaS providers offering bundled microgrid-as-a-service solutions, including solar, storage, and energy management software under a single service contract, stand to unlock recurring revenue streams in the fastest-growing geographies through 2033.

Vehicle-to-Grid (V2G) Integration and Virtual Power Plant Aggregation

The proliferation of electric vehicles presents a transformative opportunity for ESaaS providers to expand their managed asset base without proportional hardware investment, by integrating Vehicle-to-Grid (V2G) technology into their service platforms. The 2.1 million battery electric vehicles on U.S. roads already represent approximately 126 GWh of latent storage capacity.

The global automotive V2X (vehicle-to-everything) market is projected to expand dramatically through the next decade, creating a new class of distributed storage asset that ESaaS operators can aggregate into virtual power plants. The U.S. DOE Virtual Power Plants 2025 Update charts a pathway toward 80–160 GW of aggregated distributed energy resource (DER) capacity by 2030, with ESaaS aggregators positioned as the operational backbone. Providers that invest in AI-driven dispatch software, open-standard APIs, and utility-grade cybersecurity infrastructure will capture the highest value positions in this emerging segment.

Category-wise Analysis

Service Type Insights

Customer Energy Management Services (CEMS) is the leading segment within the service type category, commanding approximately 33% of global ESaaS market share in 2025. CEMS encompasses real-time monitoring, demand response management, peak shaving automation, and AI-driven load optimization, services that deliver measurable, billable value to commercial and industrial customers through quantifiable reductions in electricity expenditure and demand charges. The segment's dominance reflects the priorities of C&I buyers who increasingly demand performance-based contracts with guaranteed savings, rather than pure infrastructure provision. Johnson Controls reported US$ 8.4 billion in customer savings created through performance contracts, underscoring the commercial scale of managed energy services. IoT-enabled monitoring, edge analytics, and AI-driven dispatch algorithms embedded in CEMS platforms have reduced demand response times by up to 92%, further reinforcing their value proposition for large energy consumers.

Deployment Insights

On-grid deployment is the dominant segment in the ESaaS market, accounting for approximately 72% of market share in 2025. On-grid ESaaS systems are integrated directly with utility transmission and distribution networks, enabling revenue generation through multiple stacked value streams: frequency regulation, voltage support, energy arbitrage, capacity market participation, and demand charge management. The SEIA reported that the utility-scale, on-grid battery storage segment accounted for just under 50 GWh / 16 GW of U.S. installations in 2025 alone, comprising the dominant share of total capacity additions. The U.S. IRA's Section 48 standalone storage ITC and the EU's Net-Zero Industry Act specifically target grid-connected storage deployment, providing structural financial incentives that disproportionately benefit on-grid ESaaS business models. Grid-connected systems also benefit from established metering, interconnection, and settlement infrastructure, reducing complexity for service providers.

Application Analysis

Renewable Energy Integration is the leading application segment in the global ESaaS market, accounting for approximately 38% of market share in 2025. As solar and wind generation penetration rises, the need for dispatchable storage to absorb excess generation during off-peak hours and dispatch it during peak demand periods is becoming non-negotiable for grid operators. The energy storage system market renewable integration will grow at a CAGR of 25% through 2032, with utility-scale projects dominating this demand. In California, CAISO has already mandated integrated resource plans (IRPs) that require utilities to procure significant storage capacity, while China's National Energy Administration requires new utility-scale wind and solar projects to include co-located storage, a policy directly expanding the renewable integration ESaaS application pipeline across the world's largest energy storage market.

End-user Insights

The utility is the dominant end-user category in the global market representing approximately 41% of market share in 2025. Utilities are adopting ESaaS solutions at scale to meet grid balancing obligations, defer costly transmission and distribution (T&D) infrastructure upgrades, and fulfill regulatory mandates for energy storage procurement. The constant imperative to maintain stable, reliable grids, especially as variable renewable energy penetration accelerates, makes storage services a mission-critical utility spend category.

In the U.S., utilities invested US$ 320 billion in grid upgrades in 2023, including US$ 50.9 billion for distribution assets, investments that increasingly require smart storage management services. In China, the National Energy Administration (NEA) has established regional mandates requiring new renewable energy projects to include co-located storage, with utilities as the primary procurement and service-management entities.

Regional Insights

North America Energy Storage as a Service Market Trends and Insights

North America is the undisputed leading region in the global ESaaS market, holding approximately 41% of global market share in 2025. The United States is the primary growth engine, driven by the landmark Inflation Reduction Act (IRA) which introduced the standalone energy storage investment tax credit under Section 48 and 48E, directly improving ESaaS provider economics. The SEIA confirmed that the U.S. installed a record 57.6 GWh of new battery storage in 2025, up 29% year-on-year, with utility-scale deployments in California, Texas, and Arizona leading adoption. FERC Order 2222 enables ESaaS providers to participate in organized wholesale markets as aggregators of distributed energy resources, unlocking new revenue streams.

The U.S. innovation ecosystem is unmatched, with companies such as Honeywell International, Siemens Energy, Johnson Controls, and Customized Energy Solutions offering differentiated software-defined ESaaS platforms. The U.S. is projected to install approximately 500 GWh of additional storage capacity between 2026 and 2031, representing a 250% increase versus the prior five-year period. Canada is emerging as an important secondary market, with NRStor Inc. and Hydrostor advancing grid-scale compressed air and battery ESaaS projects, supported by federal clean energy investment programs.

Europe Energy Storage as a Service Market Trends and Insights

Europe represents the second-largest and fastest-evolving regional market for ESaaS, driven by the European Union's REPowerEU Plan and Fit for 55 package, which mandate a 45% renewable energy share by 2030 and create structural demand for grid-scale storage services. The United Kingdom has introduced a cap-and-floor regime for Long-Duration Energy Storage (LDES) investment, administered by energy regulator Ofgem, providing guaranteed minimum income floors that make LDES-based ESaaS contracts bankable. Germany's Energiewende policy has driven battery storage capacity additions to record levels, with commercial and industrial users adopting ESaaS solutions to manage escalating balancing costs.

France's regulated energy market and Spain's solar-heavy grid are both driving demand for ancillary services and peak-shaving ESaaS contracts. Veolia expanded its energy-from-waste and storage services in France in November 2024, supplying electricity to around 3,000 homes in Corrèze. ENGIE is targeting 10 GW of battery capacity globally by 2030, with its European grid services business a core component. Regulatory harmonization through the EU Internal Electricity Market Directive is progressively creating a pan-European framework for ancillary services markets, directly expanding the addressable ESaaS revenue pool.

Asia Pacific Energy Storage as a Service Market Trends and Insights

Asia Pacific is the fastest-growing regional market for ESaaS, propelled by China's dominant position in global storage deployment and the expanding policy ambitions of India, Japan, and ASEAN nations. China alone accounts for over 50% of global annual energy storage additions in gigawatts. The National Energy Administration (NEA) mandates co-located storage with new utility-scale renewable projects, generating a pipeline of ESaaS contract opportunities at unprecedented scale. In India, the India Brand Equity Foundation (IBEF) confirmed that approximately US$ 1.02 billion was allocated for solar power grid infrastructure in the 2024–2025 interim budget.

Japan's Green Growth Strategy and Fifth Strategic Energy Plan target storage deployment as a core enabler of its 2050 carbon neutrality commitment. South Korea has enacted a renewable portfolio standard with storage mandates. Manufacturing cost advantages in the region, anchored by CATL, BYD, and other Chinese battery producers, are keeping lithium iron phosphate (LFP) battery costs at globally competitive levels, enabling ESaaS providers in the region to offer highly price-competitive subscription contracts to utilities, C&I customers, and emerging market microgrids. Hydrostor advanced a 1.6 GWh compressed air ESaaS project in Australia, securing US$ 55 million in financing from Export Development Canada.

Competitive Landscape

The global Energy Storage as a Service (ESaaS) market exhibits a moderately fragmented structure, characterized by the presence of diversified energy conglomerates, industrial technology providers, and specialized storage developers. Market participation is shaped by varying capabilities across project development, financing, software integration, and asset management, with no single player dominating the landscape. Entry barriers remain moderate, driven by capital requirements, technology integration complexity, and the need for strong customer relationships, particularly in the commercial and utility segments.

Competition is increasingly centered on advanced energy management platforms and the ability to stack multiple revenue streams, including demand charge reduction, ancillary services, and capacity market participation. Providers are shifting toward outcome-based and subscription-driven models that guarantee cost savings and operational performance. Strategic focus areas include virtual power plant aggregation, microgrid-as-a-service offerings, and integration with distributed energy resources. Additionally, investments in AI-enabled optimization, long-duration storage solutions, and vehicle-to-grid capabilities are emerging as key differentiators.

Key Developments:

- March 2026: Canadian Solar Inc. announced its e-STORAGE division will deliver 420 MWh battery energy storage systems to Drax Group across two UK projects, including long-term operational services to support grid flexibility and renewable integration.

- November 2025: Adani Group announced its strategic entry into the battery energy storage sector with a 1,126 MW / 3,530 MWh BESS project in Gujarat, targeting commissioning by March 2026 and supporting grid stability and renewable integration.

- May 2025: ABB announced the launch of its Battery Energy Storage Systems-as-a-Service (BESS-as-a-Service), a zero-CapEx, subscription-based solution enabling businesses to deploy storage with full lifecycle management and performance guarantees.

Companies Covered in Energy Storage as a Service Market

- Siemens Energy

- Honeywell International Inc.

- ENGIE Storage Services NA LLC

- Veolia Environnement S.A.

- NRStor Inc.

- YSG Solar

- Suntuity

- Hydrostor Inc.

- Customized Energy Solutions Inc.

- Johnson Controls International PLC

- Schneider Electric SE

- Tesla, Inc.

- ABB Ltd.

- Duke Energy Corporation

- Ameresco, Inc.

- NextEra Energy Resources LLC

- Centrica plc

Frequently Asked Questions

The global ESaaS market is valued at US$ 2.4 billion in 2026 and is projected to reach US$ 5.1 billion by 2033 at a CAGR of 11.3%.

Key drivers include rising renewable energy adoption, increasing electricity costs, demand charge optimization, and supportive regulatory policies.

North America leads the market with around 41% share, driven by strong policy support and large-scale storage deployments in the United States.

A major opportunity lies in Vehicle-to-Grid (V2G) integration and Virtual Power Plant (VPP) aggregation.

Major players include Siemens Energy, Honeywell, Johnson Controls, ENGIE, Veolia, Hydrostor, NRStor, Schneider Electric, Tesla, ABB, Ameresco, and NextEra Energy Resources.