- Energy Storage Solutions

- Lithium-ion Battery Recycling Market

Lithium-ion Battery Recycling Market Size, Share, and Growth Forecast 2026 - 2033

Lithium-ion Battery Recycling Market by Battery Type (Lithium Nickel Manganese Cobalt Oxide, Lithium Iron Phosphate, Lithium Cobalt Oxide, Lithium Manganese Oxide, Others), by Recycling Process (Hydrometallurgical Process, Pyrometallurgical Process, Direct Recycling, Others), by Application, by End-Use Industry, by Regional Analysis, 2026 - 2033

Lithium-ion Battery Recycling Market Size and Trend Analysis

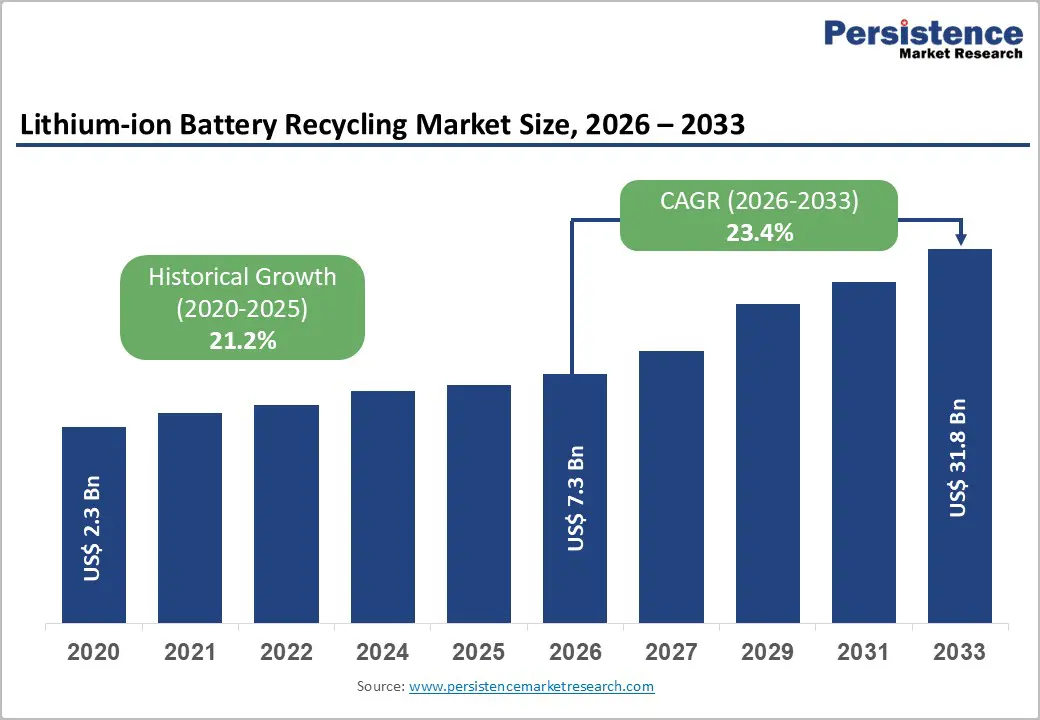

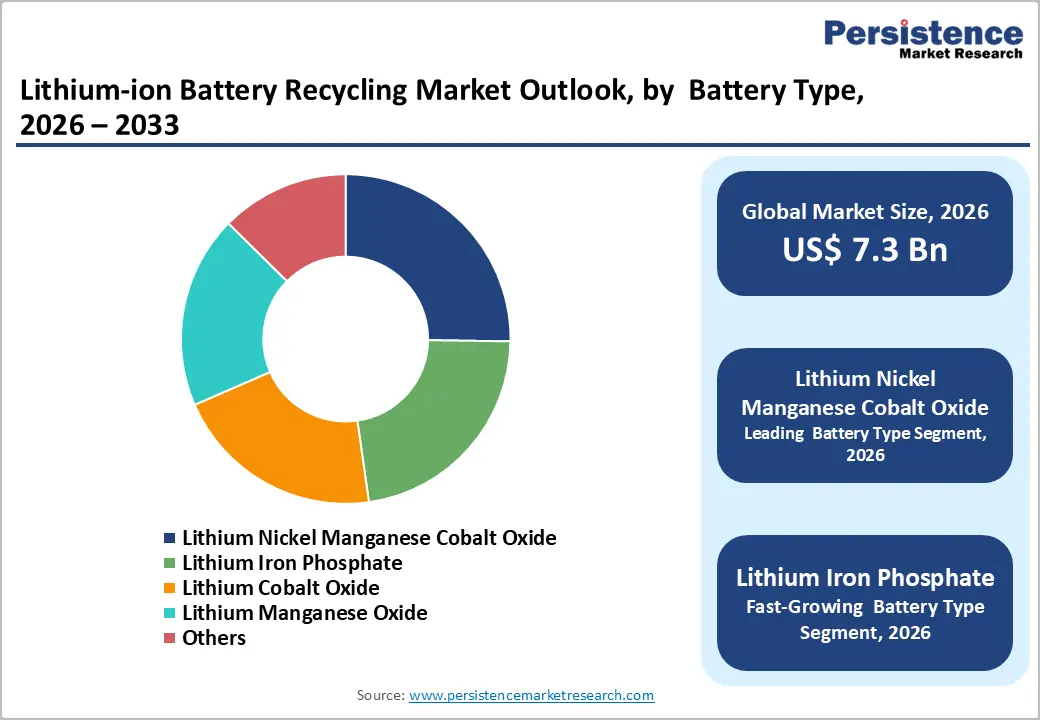

The global lithium-ion battery recycling market is expected to be valued at US$ 7.3 billion in 2026 and projected to reach US$ 31.8 billion by 2033, growing at a CAGR of 23.4% between 2026 and 2033.

Growth is fueled by accelerating electric vehicle adoption, expanding grid-scale energy storage, and tightening environmental regulations mandating efficient battery recovery. With global EV stock surpassing 40 million units and annual sales nearing 14 million, end-of-life battery volumes are rising sharply. Simultaneously, regulatory frameworks across major economies are promoting recycling efficiency and material reuse, encouraging investments in advanced technologies and strengthening circular supply chains for critical battery materials.

Key Market Highlights

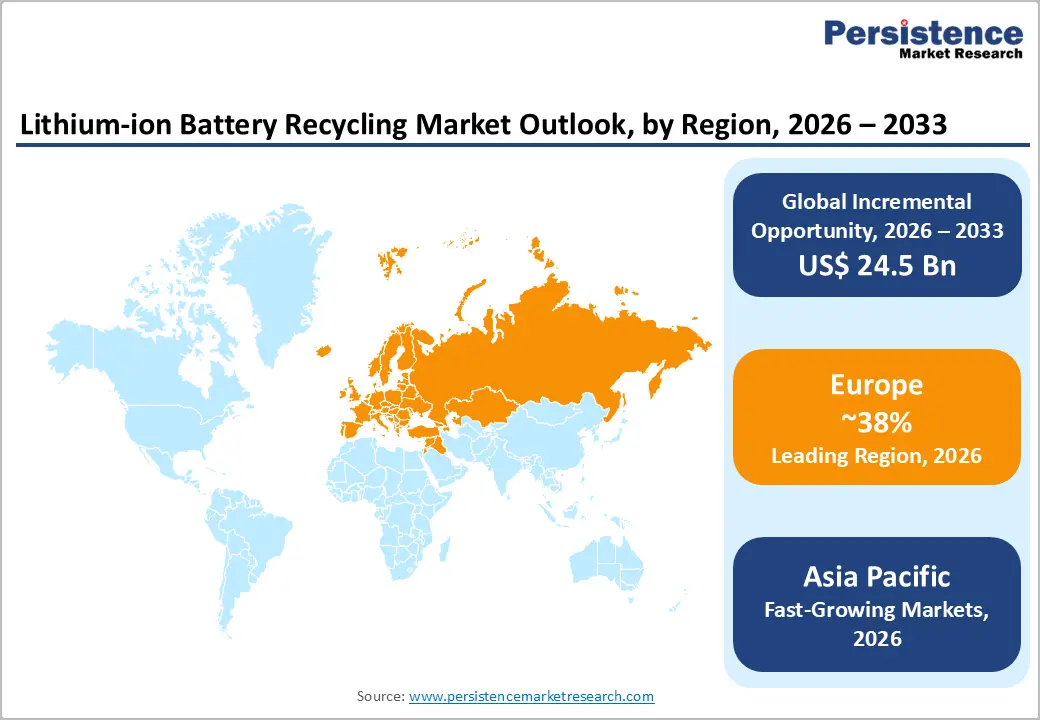

- Leading Region: Europe leads with 38% share in 2025, driven by strong regulatory frameworks and advanced recycling infrastructure.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with 33% share, supported by rapid EV adoption and expanding manufacturing ecosystems.

- Leading Application: Automotive dominates with 60% share in 2025, fueled by large volumes of end-of-life EV batteries.

- Leading Recycling Process: The hydrometallurgical process leads with 52% share, owing to high recovery efficiency and lower environmental impact.

- Key Market Opportunity: Direct recycling technologies offer 30-35% cost reductions and significant emission reductions, strengthening adoption of the circular economy.

Market Dynamics

Market Growth Drivers

Accelerating Electric Vehicle Adoption Driving Recycling Demand Growth

The rapid rise in electric vehicle adoption is a primary driver of the lithium-ion battery recycling market, as global EV stock surpasses 40 million units and annual sales momentum remains strong. This expanding installed base is generating a growing volume of end-of-life batteries, typically retired after 8-10 years, significantly increasing the need for efficient recycling infrastructure and material recovery systems.

Automakers are increasingly adopting closed-loop recycling models to secure critical materials such as lithium, cobalt, and nickel while reducing reliance on volatile mining supply chains. Strategic partnerships between OEMs and recyclers are enabling cost reductions and supporting compliance with recycled content mandates, strengthening supply chain resilience and advancing circular economy practices.

Stringent Environmental Regulations Strengthening Circular Economy Frameworks

Stringent environmental regulations across major economies are significantly accelerating the adoption of lithium-ion battery recycling practices. Policies such as the EU Battery Regulation mandate high recycling efficiency targets and introduce mechanisms, such as battery passports, that enhance traceability and encourage sustainable battery design for easier disassembly and efficient material recovery across the lifecycle.

In parallel, government initiatives in the United States and China are fostering the development of large-scale recycling ecosystems through funding programs, regulatory mandates, and production-linked recycling targets. These policy frameworks create stable demand conditions, encouraging long-term investments in advanced recycling technologies and infrastructure while supporting sustainability goals and securing critical raw material supply chains.

Market Restraints

High Capital Investment and Cost-Intensive Recycling Operations Barrier

Establishing lithium-ion battery recycling facilities requires significant upfront capital, particularly for advanced hydrometallurgical and pyrometallurgical plants. Medium- to large-scale facilities can demand investments of US$ 50-100 million, driven by complex plant design, high-throughput systems, and specialized safety infrastructure such as fire suppression, explosion-proof storage, and controlled dismantling units, thereby increasing entry barriers for new participants.

Operational challenges further increase costs due to variable battery chemistries, inconsistent feedstock quality, and strict compliance with hazardous-waste and emissions regulations. These factors increase operational expenses relative to conventional recycling, limiting participation by smaller players and resulting in a more consolidated market structure, particularly in regions lacking policy support or stable feedstock availability.

Technical Complexity and Inefficient Battery Collection Infrastructure Challenges

Handling spent lithium-ion batteries presents significant technical challenges due to diverse chemistry, formats, and proprietary designs across applications. Variations in battery composition complicate sorting, disassembly, and processing, often reducing recovery efficiency if proper pre-processing systems are not implemented, thereby affecting the quality and economic value of recovered materials.

Logistically, fragmented collection systems and the absence of standardized reverse supply chains hinder efficient battery aggregation and transportation. Many regions lack structured collection networks, labeling standards, and producer responsibility frameworks, resulting in low collection rates and safety concerns. These infrastructure gaps hinder scalability and limit the effectiveness of recycling operations despite growing volumes of battery waste.

Market Opportunities

Advancements in Direct Recycling and Material Preservation Technologies

Direct recycling technologies present a transformative opportunity by enabling the recovery of cathode materials without breaking them down into base elements. This approach preserves the crystalline structure of battery components, significantly reducing energy consumption and chemical usage compared to conventional hydrometallurgical and pyrometallurgical methods, thereby improving overall efficiency and sustainability of lithium-ion battery recycling processes.

Pilot programs have demonstrated recovery efficiencies of 90-95% for key chemistries such as NMC, while reducing material production costs by 30-35%. As these technologies scale, they can strengthen circular supply chains, support recycled-content mandates, and lower carbon footprints, with increasing government backing through R&D funding and demonstration initiatives.

Rising Energy Storage Systems Creating New Recycling Demand Streams

The rapid expansion of grid-scale energy storage and industrial battery deployments is opening new avenues for lithium-ion battery recycling. Growing renewable energy integration is driving demand for storage systems, leading to a future surge in end-of-life batteries from utilities and industrial sectors, thereby expanding the overall recycling market beyond automotive and consumer electronics applications.

Lithium iron phosphate batteries are gaining prominence in these applications due to their safety and long lifecycle, often enabling second-life usage before recycling. This extended value chain increases the potential for material recovery, while emerging regulatory frameworks across key regions are supporting structured recycling ecosystems tailored to energy storage assets.

Category-wise Insights

Battery Type Analysis

Lithium Nickel Manganese Cobalt Oxide (NMC) dominates the Lithium-ion Battery Recycling Market, accounting for approximately 45% share in 2025. Its leadership is driven by widespread use in electric vehicles and high-performance electronics, where energy density and cost efficiency are critical. The high content of valuable metals such as cobalt, nickel, and lithium enhances recycling economics, making NMC batteries the most commercially attractive segment for recyclers globally.

Lithium Iron Phosphate (LFP) is emerging as the fastest-growing battery type due to its increasing adoption in electric vehicles and energy storage systems. Its longer lifecycle, improved safety profile, and expanding deployment in large-scale applications are expected to generate a significant future stream of recyclable batteries, encouraging the development of tailored recycling technologies for lower-cobalt chemistries.

Recycling Process Analysis

The Hydrometallurgical Process dominates the recycling process segment, holding around 52% share in 2025. This leadership is attributed to its ability to recover high-purity lithium, cobalt, and nickel with recovery efficiencies exceeding 90-95%. Compared to pyrometallurgical methods, it offers lower emissions, reduced energy consumption, and improved material recovery, making it the preferred approach for modern recycling facilities.

Direct recycling is the fastest-growing process as it enables preservation of the cathode structure and reduces energy-intensive processing steps. This approach improves material value retention and aligns with circular economy goals, making it increasingly attractive for next-generation recycling systems focused on efficiency, sustainability, and integration into battery manufacturing supply chains.

Application Analysis

The Automotive segment leads the market, capturing about 60% of the market share in 2025. This dominance is driven by the rapid expansion of electric vehicles and the large volume of traction batteries reaching end-of-life. Compared to other applications, automotive batteries contribute the largest share of recyclable materials, making this segment the primary driver of recycling demand.

Energy & Utilities is emerging as the fastest-growing application segment due to the rising adoption of grid-scale energy storage systems. Increasing renewable energy integration and the need for grid stability are accelerating battery deployment, which is expected to generate a growing pipeline of end-of-life batteries for recycling in the coming years.

End-Use Industry Analysis

The Industrial segment dominates the market with approximately 55% share in 2025, supported by extensive use of lithium-ion batteries in manufacturing, logistics, telecom infrastructure, and backup power systems. These applications generate consistent and predictable battery waste streams, enabling efficient collection and processing compared to more fragmented consumer-based sources.

Municipal is the fastest-growing segment as waste management systems improve and awareness of proper battery disposal increases. Expansion of structured collection networks and regulatory initiatives is enhancing recovery rates from household and small-scale battery usage, supporting growth in formal recycling systems and strengthening overall market development.

Regional Insights

North America Lithium-ion Battery Recycling Market Trends and Insights

North America is emerging as a significant region in the lithium-ion battery recycling market, supported by strong policy frameworks and investments. The region is projected to grow at a CAGR of around 23% through the forecast period, driven by initiatives such as the Inflation Reduction Act and infrastructure funding for recycling and second-life battery projects. Increasing EV adoption and growing battery waste streams further strengthen regional demand.

The United States leads innovation with large-scale recycling facilities and advanced recovery technologies being deployed across key states. Strategic collaborations between automakers and recyclers, along with expanding collection networks and regulatory support, are enhancing scalability. These developments are creating a robust ecosystem that supports long-term growth and improves supply chain sustainability.

Europe Lithium-ion Battery Recycling Market Trends and Insights

Europe leads the lithium-ion battery recycling market, accounting for approximately 38% share in 2025. This dominance is driven by stringent regulatory frameworks, such as the EU Battery Regulation, which mandate recycling efficiency, recycled-content targets, and battery traceability systems. These policies are creating a highly structured and compliance-driven recycling ecosystem across the region.

The region continues to attract strong investments in recycling infrastructure and technology innovation. Increasing collaboration between manufacturers and recyclers, along with high collection rates and policy enforcement, is strengthening circular economy practices. Europe’s regulatory leadership and industrial alignment position it as a mature and high-value market for battery recycling.

Asia Pacific Lithium-ion Battery Recycling Market Trends and Insights

Asia Pacific accounts for around 33% share of the lithium-ion battery recycling market and is the fastest-growing region. Growth is fueled by China’s dominance in battery manufacturing, rapid adoption of electric vehicles, and strong government mandates that support recycling and resource recovery. The presence of vertically integrated players further enhances large-scale processing capabilities.

Countries such as India, Japan, and South Korea are also expanding their recycling infrastructure, supported by policy initiatives and growing energy storage deployments. Increasing investments in advanced technologies and integrated supply chains are accelerating regional growth, positioning the Asia Pacific as a key hub for future lithium-ion battery recycling activities.

Competitive Landscape

The lithium-ion battery recycling market is moderately consolidated, with large integrated players alongside emerging technology-driven recyclers. While developed regions exhibit greater consolidation due to advanced infrastructure and regulatory requirements, several countries continue to exhibit fragmented competition with numerous domestic participants. This dynamic creates a balance between scale advantages and localized operational flexibility.

Market participants are increasingly focusing on vertical integration, advanced recycling technologies, and long-term supply agreements to strengthen their competitive position. Innovations in direct recycling, automation, and traceability systems are becoming key differentiators. Additionally, evolving business models such as battery take-back programs and lifecycle management services are reshaping competition toward value-driven, circular economy-oriented strategies.

Key Market Developments

- In March 2025, Li-Cycle opens North America’s largest hydrometallurgical lithium-ion battery recycling plant in New York, capable of processing over 25,000 tons of end-of-life batteries annually. The facility is designed to produce high-purity lithium, nickel, cobalt, and manganese products that can be reintegrated into battery-cathode manufacturing, aligning with U.S. circular-economy and critical-mineral strategies.

- In July 2024, Redwood Materials secured a US$ 1 billion loan from the U.S. Department of Energy (DOE) to expand its Nevada-based recycling hub and build additional capacity for recovering lithium, cobalt, and nickel from EV batteries. The project aims to scale recovery rates above 90% while integrating direct recycling techniques into its processing flowsheet.

- In January 2025, Umicore partners with Volkswagen Group to establish a dedicated lithium-ion battery recycling hub in Germany focused on NMC-based cathode materials. The facility is intended to support Volkswagen’s closed-loop battery strategy and to meet EU-mandated recycled-content requirements by the early 2030s.

Companies Covered in Lithium-ion Battery Recycling Market

- Arrowquip

- Powder River Inc.

- Te Pari Products Ltd.

- IAE (Industrial Agricultural Engineering)

- Tarter Farm & Ranch Equipment

- Priefert Manufacturing

- Hi-Hog Farm & Ranch Equipment

- D-S Livestock Equipment

- ProWay Livestock Equipment Pty Ltd.

- Sioux Steel Company

- Patura KG

- O'Donovan Engineering Ltd.

- Jourdain SA

- Behlen Country

- WW Manufacturing

Frequently Asked Questions

The Lithium-ion Battery Recycling Market is projected to be valued at US$ 7.3 billion in 2026.

Key drivers include the global surge in electric vehicle adoption, which generates large volumes of end-of-life batteries, and the introduction of stringent environmental regulations.

Europe leads the Lithium-ion Battery Recycling Market in 2025, driven by harmonized EU-level regulations, mature collection infrastructure, and strong commitments.

A major opportunity lies in direct recycling and material-preserving technologies, which can recover high-purity battery materials with lower energy use and reduced emissions.

Key players include Li-Cycle, Redwood Materials, Umicore, Northvolt, Brunp Recycling (Gem Co., Ltd.), American Battery Technology Company, Princeton NuEnergy, and Tesla.