- Industrial Goods & Service

- Transformer Market

Transformer Market Size, Share, and Growth Forecast 2026 - 2033

Transformer Market by Product Type (Distribution Transformer, Power Transformer, Instrument Transformer, Misc.), Cooling Type (Air-cooled, Oil-cooled), Voltage Type (Low, Medium, High), Phase (Single-phase, Three-phase), End-user (Residential & Commercial, Industrial), Regional Analysis, 2026 - 2033

Transformer Market Size and Trend Analysis

The global transformer market size is expected to be valued at US$ 65.7 billion in 2026 and projected to reach US$ 96.8 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

Robust expansion of the global transformer market is underpinned by accelerating grid modernization investments and surging electricity demand worldwide. The International Energy Agency (IEA) projects global electricity demand to grow at 3.3% in 2025 and 3.7% in 2026, one of the fastest sustained rates in more than a decade, driven by the electrification of industry, data centers, and electric vehicles.

Simultaneously, approximately US$ 400 billion is now spent annually on grid infrastructure worldwide, and the IEA warns this must rise substantially to meet evolving power demands. Renewable energy integration, aging infrastructure replacement, and the proliferation of smart grid deployments are reinforcing strong demand for advanced transformer technologies across all major regions.

Key Industry Highlights

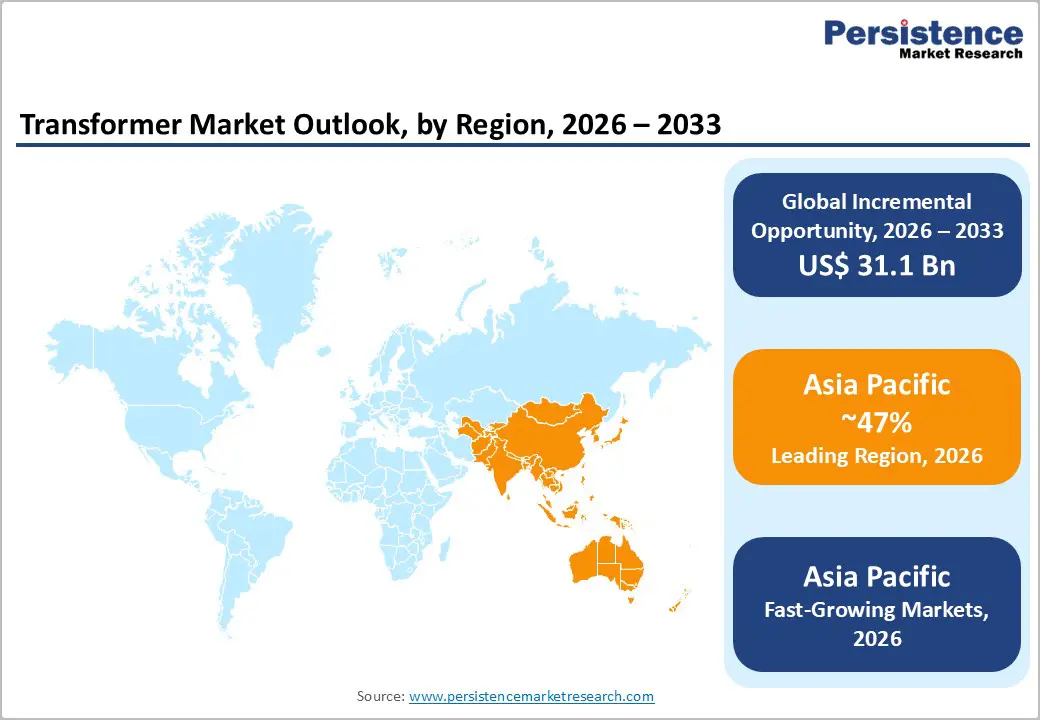

- Leading Region: Asia Pacific dominated the global transformer market with approximately 47% share in 2025, driven by China's UHV grid expansions, India's national transmission plan, and strong regional industrialization, which is driving extensive transformer procurement.

- Fastest Growing Region: Asia Pacific is also the fastest-growing region through 2033, fueled by ASEAN electrification programs, rising renewable energy capacity additions, and sustained government investment in grid infrastructure across India and Southeast Asia.

- Dominant Segment: Power transformers hold the dominant product type position, with approximately 90% market share in 2025, driven by the expansion of high-voltage transmission infrastructure, renewable energy grid integration, and the global rollout of UHV projects.

- Fastest Growing Segment: Distribution transformers are the fastest-growing product type through 2033, propelled by last-mile electrification, smart grid deployments, EV charging infrastructure rollout, and rising residential electricity consumption across the Asia Pacific and Africa.

- Key Market Opportunity: The rapid expansion of AI-driven data center infrastructure and smart grid deployments presents a high-growth opportunity, with demand for high-efficiency transformers expected to double by 2035 as hyperscale computing and grid digitalization become the primary drivers of demand.

| Key Insights | Details |

|---|---|

| Transformer Market Size (2026E) | US$ 65.7 Billion |

| Market Value Forecast (2033F) | US$ 96.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 5.2% |

DRO Analysis

Drivers - Accelerating Global Grid Modernization and Electrification

One of the foremost growth drivers of the transformer market is the unprecedented wave of grid modernization investment sweeping across the globe. The IEA's World Energy Investment report highlights that each year approximately US$ 400 billion is now deployed in global grid infrastructure, yet this needs to increase rapidly to meet surging electricity demand.

Under current policy scenarios, transmission spending must exceed US$ 200 billion per year by the mid-2030s. The European Network of Transmission System Operators for Electricity (ENTSO-E) estimates that approximately US$ 420 billion in grid investment is needed in Europe alone.

Simultaneously, the growing electrification of transportation, heating, and industrial processes is increasing the load factor on distribution and power transformers. This broad-based electrification trend, reinforced by national and supranational policy commitments, is generating structural, long-term demand for transformer products across all voltage classes and end-use segments.

Renewable Energy Integration and Expansion of Transmission Corridors

The rapid integration of renewable energy into national grids is generating sustained demand for high-capacity transformers, particularly power transformers capable of handling variable generation from wind and solar installations. The IEA has estimated that to meet national energy and climate goals, countries must add or refurbish over 80 million kilometers of grid by 2040, requiring modern, high-capacity transmission equipment, including HVDC converter transformers.

The U.S. Department of Energy (DOE) committed nearly US$ 1.5 billion under its Transmission Facilitation Program to advance approximately 1,000 miles of new lines, enabling 7.1 GW of transfer capacity. In Asia, India's National Electricity Plan maps 191,000 circuit-km of lines requiring substantial transformation capacity additions by 2032, while the State Grid Corporation of China plans investments exceeding US$ 70 billion in 2024 to expand ultra-high-voltage (UHV) projects, collectively underpinning robust global transformer procurement.

Restraints - Supply Chain Constraints and Extended Lead Times

A significant restraint facing the transformer market is the tightening of global supply chains for key components and raw materials. According to an IEA industry survey conducted in 2024, lead times for large power transformers have nearly doubled over the past two to three years. Manufacturers have reported a record backlog of transformer orders in 2024, with order values in US$ increasing by one-third in just one year.

The price of power transformers rose by approximately 75% since 2019, driven by surging demand, constrained production capacity, and rising material costs for copper, aluminum, and grain-oriented electrical steel. These supply-side pressures are delaying project timelines and inflating costs for utilities and industrial end-users, thereby moderating the global pace of transformer procurement.

High Capital Expenditure and Financing Challenges in Emerging Economies

The transformer market faces a notable restraint: high capital requirements for grid infrastructure projects, particularly in emerging and developing economies. The deployment of medium- and high-voltage transformers demands significant upfront capital investment, which can be challenging for utilities operating under constrained financial conditions.

The IEA notes that emerging markets and developing economies (excluding China) have seen grid investment decline by an average of 7% per year over recent years, despite robust electricity demand growth. The poor financial health of many utility companies in these regions, combined with lengthy permitting procedures and regulatory complexities, constrains market expansion and limits the deployment of advanced transformer technologies in high-potential yet underfunded markets.

Opportunities - Accelerating Deployment of Distribution Transformers for Last-Mile Connectivity and Smart Grids

A compelling opportunity for transformer market participants lies in the rapidly growing distribution transformer segment, particularly as governments and utilities globally prioritize last-mile electrification and smart grid infrastructure. At COP 29, nearly 60 countries committed to the Global Energy Storage and Grids Pledge, targeting 25 million kilometers of new grid infrastructure by 2030 and a doubling of global grid investment. Distribution transformers are at the heart of this effort, enabling reliable power delivery to residential and commercial end-users.

Additionally, integrating IoT-enabled sensors and predictive maintenance capabilities into next-generation distribution transformers is unlocking new revenue streams for manufacturers. Companies that invest in smart, digitally enabled distribution transformer platforms, particularly those featuring biodegradable insulating fluids and eco-friendly cooling designs, are well positioned to capture substantial demand across both developed and emerging markets through 2033.

Data Center and AI Infrastructure Expansion Driving Demand for High-Efficiency Transformers

The exponential growth of data centers and artificial intelligence (AI) computing infrastructure represents a high-growth opportunity for transformer manufacturers, particularly for dry-type and medium-voltage units. Global data center transformer demand is estimated at approximately US$ 10.5 billion in 2025 and is projected to reach US$ 20.7 billion by 2035 at a CAGR of 7.0%. Hyperscale data center providers such as Amazon Web Services (AWS) and Microsoft Azure are rapidly scaling capacity, necessitating the procurement of advanced transformers.

In June 2025, Eaton and Siemens Energy formed a strategic collaboration to deliver modular power plants for new data center campuses, integrating on-site renewable energy. Manufacturers offering AI-optimized, high-efficiency transformer solutions tailored for power-dense computing environments stand to benefit significantly from this structurally expanding end-use market.

Category-wise Analysis

Product Type Insights

Power transformers represent the dominant segment within the transformer market by product type, commanding approximately 90% of the total market share in 2025. This overwhelming dominance is driven by the critical role that power transformers play in high-voltage transmission networks, forming the backbone of national and regional electricity grids. The accelerating build-out of renewable energy generation projects-particularly large-scale wind and solar farms located in remote areas-requires power transformers to step up voltage for efficient long-distance transmission and grid interconnection.

The State Grid Corporation of China's planned investment of over US$ 70 billion in 2024 for ultra-high-voltage (UHV) expansion, India's target of 1,270 GVA of transformation capacity by 2032, and extensive grid modernization programs across North America and Europe collectively underpin sustained, large-scale procurement of power transformers. Their ability to handle extreme voltages with high operational efficiency makes them indispensable for modern grid infrastructure.

Cooling Type Insights

Oil-cooled transformers lead the transformer market by cooling type, holding approximately 52% of the market share in 2025. Their dominance is attributed to superior thermal stability, higher load-handling capacity, and proven reliability in high-voltage and heavy-duty applications such as utility-scale power transmission and large industrial operations. Oil-cooled systems are widely preferred by utilities and grid operators for their ability to manage variable load conditions over extended periods, maintaining dielectric strength and extending equipment lifespan. T

he widespread integration of renewable energy into grids has further accelerated adoption, as oil-cooled transformers demonstrate the thermal management capability required for large, fluctuating power flows. Advances in biodegradable and ester-based insulating oils are enhancing the sustainability profile of oil-cooled transformers, aligning them with increasingly stringent environmental regulations in Europe and North America and reinforcing their continued market leadership.

Voltage Type Insights

Medium voltage transformers dominate the transformer market's voltage type segmentation, accounting for approximately 55% of market share in 2025. Medium voltage units-typically operating in the range of 1 kV to 35 kV-serve as the critical interface between high-voltage transmission networks and end-user distribution systems, making them essential across industrial, commercial, and utility applications.

The growth of renewable energy integration at the distribution level, industrial facility expansions, and the deployment of electric vehicle (EV) charging infrastructure are all driving incremental demand for medium-voltage transformers. Furthermore, rapid urbanization in Asia-Pacific nations, along with government-mandated grid upgrades in Europe and North America, is driving the replacement of aging medium-voltage equipment with energy-efficient, digitally enabled units. The segment's versatility across diverse end-use applications solidifies its leadership position within the broader transformer market.

Phase Insights

Three-phase transformers hold the largest share of the transformer market by phase configuration, accounting for approximately 56% of the total market in 2025. Three-phase units are the standard choice for industrial facilities, large commercial complexes, data centers, and utility grid networks, where a high-capacity, continuous power supply with balanced load distribution is essential. Their efficiency advantages-including reduced transmission losses, improved voltage regulation, and smoother operation of heavy machinery-make them preferable to single-phase units for most high-demand applications.

The rapid growth of energy-intensive industries, including manufacturing, mining, and digital infrastructure, alongside the global expansion of electrified transportation networks, is driving demand for three-phase transformers. Countries like China, India, and Germany are particularly significant markets for three-phase transformer procurement, driven by industrial policy and grid development programs.

End-user Insights

The residential & commercial segment leads among end-users in the transformer market, capturing approximately 53% of market share in 2025. This dominance reflects the massive scale of global urbanization and the consequent growth in electricity consumption across housing developments, retail infrastructure, office complexes, and hospitality establishments. The IEA projects that global electricity demand growth will continue to accelerate through 2030, with a rising share driven by residential adoption of heat pumps, smart appliances, and rooftop solar systems-all of which require distribution transformers for grid integration.

The proliferation of EV charging infrastructure in commercial and residential zones is adding new load requirements on distribution transformers in urban and suburban areas. Government-backed smart city initiatives across Asia Pacific, Europe, and North America are further driving demand in this segment, as utilities undertake large-scale grid modernization to reliably serve growing populations.

Regional Insights

North America Transformer Market Trends and Insights

North America is a strategically important market for the transformer industry, driven by extensive grid modernization programs, rising electricity demand from data centers and EV infrastructure, and aggressive domestic manufacturing expansion. The U.S. Department of Energy (DOE) committed nearly US$ 1.5 billion under its Transmission Facilitation Program to develop approximately 1,000 miles of new transmission lines, enabling 7.1 GW of transfer capacity. The National Infrastructure Advisory Council (NIAC) has underscored a critical shortage of large power and distribution transformers in the region, prompting policy action and domestic investment.

In response, leading companies are rapidly expanding U.S. production capacity. ABB invested US$ 120 million in March 2025 to scale transformer output in Tennessee and Mississippi, while Siemens Energy announced plans for its first U.S. power transformer manufacturing facility, valued at US$ 150 million. Eaton also established a new three-phase transformer plant in South Carolina in February 2025. These investments reflect the region's strategic emphasis on supply chain resilience and are expected to ease chronic lead-time pressures through the forecast period.

Europe Transformer Market Trends and Insights

Europe represents a mature but rapidly evolving transformer market, shaped by aggressive decarbonization policies, offshore wind expansion, and cross-border grid interconnection targets. The European Commission's Grid Action Plan projects electricity consumption rising approximately 60% by 2030 and calls for over US$ 680 billion of grid investment this decade, including doubling cross-border transmission capacity and accommodating up to 317 GW of offshore renewables. Germany, France, and the United Kingdom are at the forefront, collectively driving procurement of high-voltage and HVDC converter transformers.

Regulatory harmonization under the EU Electricity Market Reform and the push toward sustainable, eco-design-compliant transformer specifications are shaping procurement decisions. Siemens Energy announced a EUR 220 million investment in September 2025 to expand its transformer production site in Nuremberg, Germany. In July 2024, TenneT and Siemens Energy partnered on an initiative to manufacture 100% recycled-copper transformers, targeting 52 units by 2030. Spain and Italy are also investing in transmission upgrades, with Italy's TSO Terna acquiring high-voltage grid assets to strengthen national grid resilience.

Asia Pacific Transformer Market Trends and Insights

Asia Pacific is the leading and fastest-growing region in the global transformer market, commanding approximately 47% of the global market share in 2025. This dominance is driven by rapid industrialization, urbanization, and massive grid expansion programs in China, India, Japan, and the ASEAN region. The State Grid Corporation of China planned investments exceeding US$ 70 billion in 2024 for UHV projects and intelligent distribution systems, representing one of the world's largest single-market sources of transformer demand. India's National Electricity Plan maps 191,000 circuit-km of new transmission lines by 2032, generating massive procurement activity.

In Japan, Toshiba is expanding transformer manufacturing capacity by 50% with a US$ 60 million investment by 2027 to serve both domestic and export markets. Schneider Electric Infrastructure Ltd. is investing approximately INR 13.6 crore to expand medium power transformer manufacturing at its Vadodara plant in India, adding 1,500 MVA of annual capacity.

ASEAN nations are reporting consistent electricity demand growth as noted by the Association of Southeast Asian Nations (ASEAN) secretariat, further broadening the regional market base. Asia Pacific's combination of large-scale government investment, manufacturing competitiveness, and growing domestic consumption positions it as the defining growth engine of the global transformer market through 2033.

Competitive Landscape

The global transformer market is moderately consolidated, with a few multinational players holding significant market share, supported by extensive manufacturing capabilities and global supply networks, while numerous regional manufacturers cater to localized demand and cost-sensitive segments. This dual structure fosters both scale-driven competition and regional specialization.

Strategically, leading companies are focusing on digitalization through IoT-enabled monitoring systems and predictive maintenance solutions to enhance asset reliability and lifecycle performance. Sustainability is also emerging as a key differentiator, with increasing investments in eco-friendly insulating materials and energy-efficient designs.

Capacity expansion and localization of production are being prioritized to address supply chain risks and rising demand. Additionally, long-term supply agreements with utilities and grid operators are strengthening revenue visibility. Meanwhile, emerging manufacturers are expanding export capabilities, intensifying competition in high-voltage and infrastructure-driven segments globally.

Key Developments:

- November 2025: SolarEdge Technologies collaborated with Infineon Technologies to advance high-efficiency power infrastructure for AI and hyperscale data centers, jointly developing modular solid-state transformer technology leveraging silicon carbide semiconductors to achieve over 99% efficiency and enable scalable DC-based power architectures.

- October 2025: Waaree Transpower unveiled next-generation inverter-duty transformers designed for utility-scale solar power projects, offering enhanced efficiency, high-capacity performance, and compatibility with renewable energy systems, targeting solar developers, industrial users, and smart grid applications.

- September 2025: Siemens Energy announced a EUR 220 million investment to expand its transformer production facility in Nuremberg, Germany, reinforcing European supply chain capacity amid rising demand for grid modernization.

- February 2025: Eaton Corporation established a new dedicated three-phase transformer manufacturing facility in South Carolina, its third such U.S. plant, targeting growing demand from the utility and data center sectors.

Companies Covered in Transformer Market

- ABB Ltd.

- Schneider Electric

- Siemens Energy

- Mitsubishi Electric Corporation

- Toshiba Corporation

- TBEA Co., Ltd.

- General Electric (GE Vernova)

- Hyundai Heavy Industries

- Eaton Corporation

- Hyosung Heavy Industries Co., Ltd.

- Kirloskar Electric Company

- Hitachi Energy Ltd.

- WEG S.A.

- LS Electric Co., Ltd.

- CG Power and Industrial Solutions

- Waaree Transpower

- SolarEdge Technologies

Frequently Asked Questions

The market is expected to reach US$ 65.7 billion in 2026 and grow to US$ 96.8 billion by 2033 at a CAGR of 5.7%.

Growth is driven by grid modernization, renewable energy integration, rising electricity demand, EV charging infrastructure, and expanding data centers.

Asia Pacific leads the market with around 47% share, supported by large-scale grid expansion and industrialization.

Opportunities lie in AI-driven data centers, smart transformers, and increasing global investments in grid infrastructure.

Key players include ABB, Siemens Energy, Schneider Electric, Mitsubishi Electric, Toshiba, GE Vernova, Eaton, and others.