- Smart Packaging

- Tote Bag Market

Tote Bag Market Size, Share, and Growth Forecast, 2026 - 2033

Tote Bag Market by Material (Canvas, Fabric, Others), Application (Daily Use/Casual Wear, Fashion & Luxury, Others), Distribution Channel, and Regional Analysis for 2026 - 2033

Tote Bag Market Size and Trends Analysis

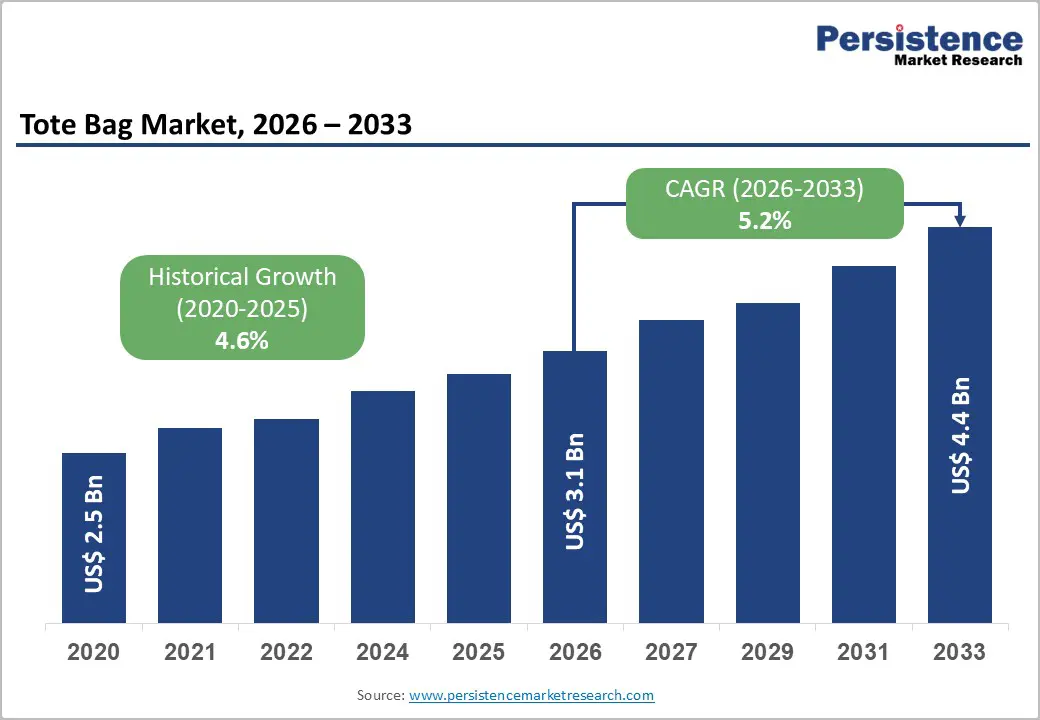

The global tote bag market size is likely to be valued at US$ 3.1 billion in 2026 and is expected to reach US$4.4 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033, driven by the regulatory substitution of single-use plastic bags, rising consumer preference for reusable and sustainable accessories, and the rapid growth of e-commerce channels that enable direct-to-consumer (D2C) brands.

Tote bags have transitioned from functional shopping carriers to lifestyle and fashion statements, strengthening value realization across both premium and mass segments. While raw material volatility and pricing pressure from low-cost producers present structural risks, companies that invest in sustainable materials, brand positioning, and omnichannel distribution are positioned to capture long-term value.

Key Industry Highlights:

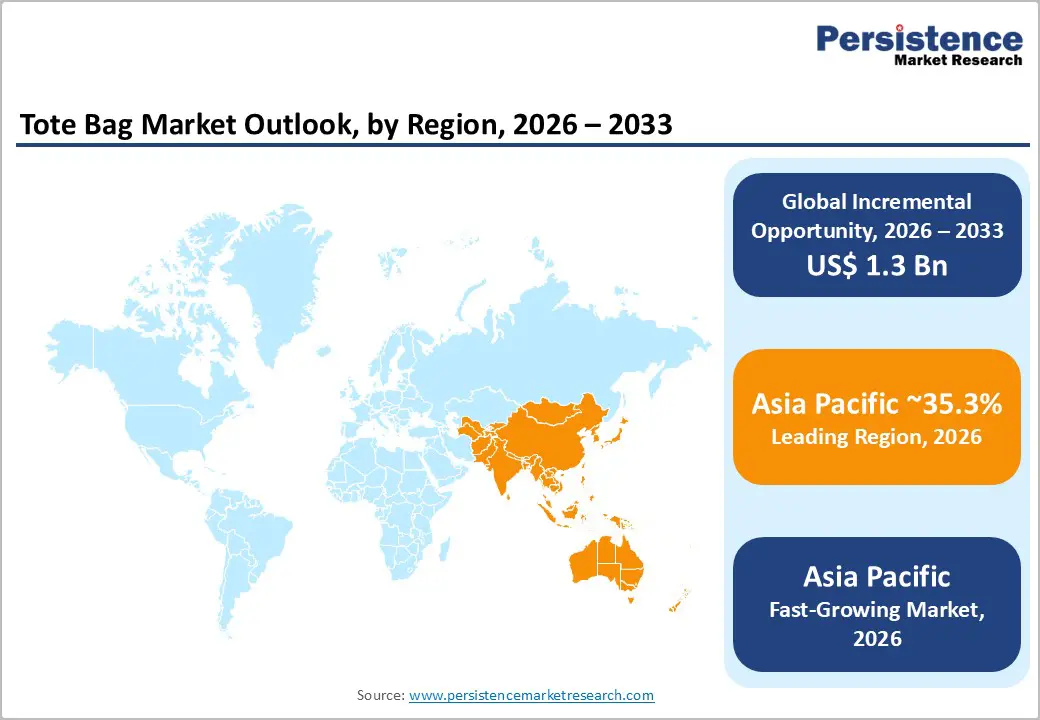

- Leading Region: Asia Pacific is projected to account for 35.3% of market share, supported by large-scale manufacturing capacity and rising domestic consumption in China, India, and Japan.

- Fastest-growing Region: Asia Pacific is projected to outpace other regions through 2033, driven by e-commerce expansion and export competitiveness.

- Investment Plans: Focus on recycled textile processing, certified sustainable material sourcing, and D2C e-commerce infrastructure to improve margins and compliance readiness.

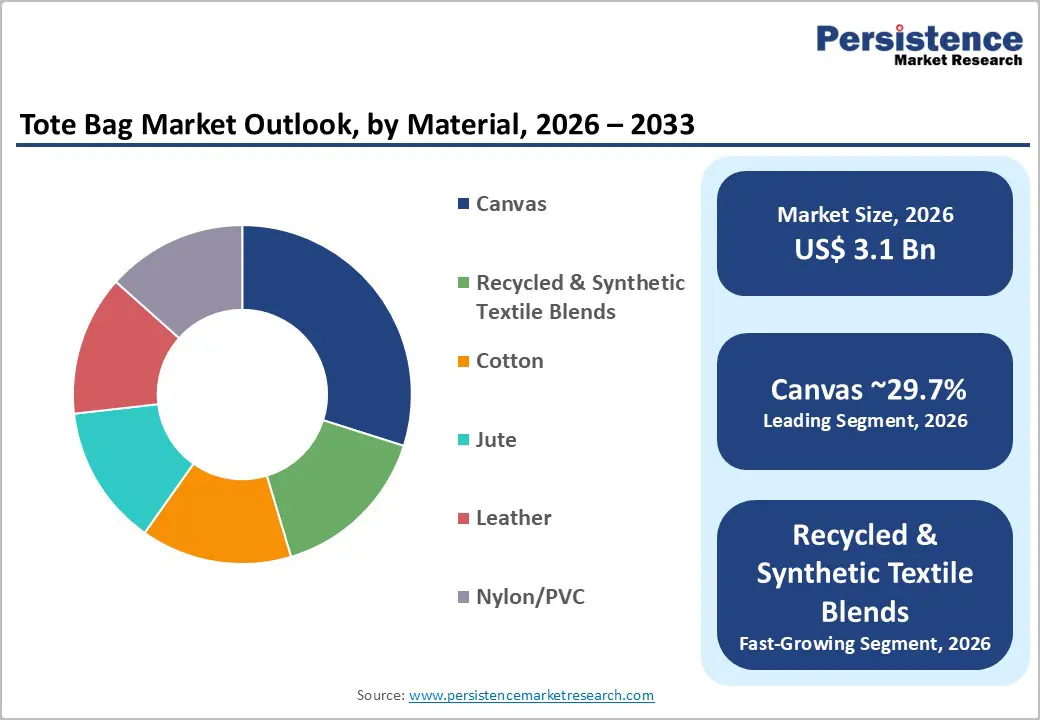

- Dominant Material: Canvas is anticipated to hold 29.7% of the market share, maintaining leadership due to durability, printability, and a broad application range.

- Leading Application: Daily Use/Casual Wear is estimated to hold 46.2% market share, supported by high replacement frequency, cross-demographic adoption, and strong demand from grocery shoppers, students, and urban commuters.

| Key Insights | Details |

|---|---|

| Tote Bag Market Size (2026E) | US$3.1 Bn |

| Market Value Forecast (2033F) | US$4.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Substitution and Plastic Reduction Policies

Government-led restrictions on single-use plastics have structurally altered consumer purchasing behavior. Federal, state, and municipal authorities across North America, Europe, and parts of Asia Pacific have implemented plastic bag bans, levies, or extended producer responsibility frameworks. These regulatory actions directly increase demand for reusable alternatives such as tote bags. Retailers respond by expanding branded reusable tote assortments, while institutional buyers procure totes for compliance and sustainability positioning. The impact is measurable: regions with active plastic reduction mandates demonstrate higher reusable bag penetration rates. Regulations create predictable baseline demand, particularly in grocery and retail environments, ensuring sustained volume growth for standard canvas and cotton tote categories.

Sustainability Positioning and ESG Differentiation

Consumers increasingly evaluate products based on environmental credentials. Tote bags serve as visible symbols of sustainable consumption, encouraging brands to adopt certified organic cotton, recycled polyester, jute, and other traceable materials. Corporate ESG commitments amplify this effect, as companies procure reusable totes for promotional events and corporate gifting aligned with sustainability policies. Products incorporating recycled content often command price premiums due to verified sourcing and life-cycle documentation. Value growth outpaces volume growth in premium and certified segments, enabling margin expansion for brands investing in traceability, material innovation, and transparent sourcing frameworks.

E-Commerce Expansion and Customization Capabilities

Digital commerce has transformed tote bag distribution. Online marketplaces and D2C brands leverage print-on-demand and small-batch manufacturing technologies to offer personalized designs and limited-edition collections. This shift reduces inventory risk and accelerates product testing cycles. Social media visibility further drives fashion-driven demand, especially in younger demographics. Online channels support faster SKU turnover, higher average selling prices (ASPs), and expanded global reach for small and mid-sized brands.

Barrier Analysis - Raw Material Price Volatility

Cotton, jute, canvas, and synthetic polymers are subject to commodity price cycles influenced by weather patterns, energy costs, and global logistics conditions. Price fluctuations directly affect production margins, particularly in commoditized segments with limited pricing power. In cost shock scenarios, margin compression of 3-6 percentage points is plausible for manufacturers lacking forward purchasing agreements or diversified sourcing strategies. Companies must prioritize supplier diversification and hedging mechanisms to stabilize cost structures.

Market Fragmentation and Low Entry Barriers

The tote bag industry has relatively low capital intensity, enabling numerous regional manufacturers to enter the market. This fragmentation increases price competition, particularly in promotional and wholesale channels. Large retail buyers frequently prioritize cost over differentiation in bulk orders, limiting ASP growth for undifferentiated suppliers. Without brand equity, material differentiation, or customization capabilities, producers face persistent margin pressure.

Opportunity Analysis - Recycled Materials and Product Innovation

Advancements in recycled textiles and blended material technologies present significant opportunities for premium product positioning within the tote bag market. Post-consumer recycled polyester (rPET), recycled cotton blends, and jute-based composites align strongly with corporate sustainability mandates and evolving regulatory expectations related to circular economy practices. These materials reduce reliance on virgin fibers while offering durability and design flexibility suitable for both promotional and retail applications. Brands capable of providing life-cycle documentation, traceable sourcing records, and certified recycled content gain measurable advantages in institutional procurement and environmentally conscious consumer segments. Strategic initiatives should include vertically integrated recycling partnerships, long-term supply agreements with fiber processors, and investment in low-impact dyeing and finishing technologies to support scalable premium product lines.

Corporate Procurement and Institutional Channels

Corporate gifting programs, university merchandise initiatives, retail promotional campaigns, and sustainability-driven procurement policies represent high-volume and recurring demand channels for tote bag manufacturers. Large organizations increasingly integrate reusable products into ESG initiatives, employee onboarding kits, conference merchandise, and customer engagement programs. Institutional buyers often require verification of environmental claims, including recycled content certifications and responsible sourcing documentation. This trend creates opportunities for producers that can meet compliance requirements while offering customization at scale. Strengthening B2B sales capabilities, establishing dedicated corporate merchandising divisions, and providing transparent sustainability documentation can help suppliers secure multi-year procurement contracts and stable revenue streams across institutional markets.

Category-wise Analysis

Material Insights

Canvas is anticipated to retain its leadership position, accounting for approximately 29.7% of the market share, supported by its durability, versatility, and strong consumer perception of quality. Its thick weave structure provides higher load-bearing capacity compared to lightweight cotton or synthetic blends, making it suitable for grocery retail, book carrying, laptop transport, and daily commuting. Retailers and lifestyle brands favor canvas due to its superior printability and structural integrity, which supports detailed screen printing, embroidery, and corporate branding. Organic and waxed canvas variants enhance water resistance and premium appeal, expanding applicability in urban fashion and outdoor segments. For example, heritage-style canvas totes offered by brands such as L.L.Bean and sustainable lifestyle collections from Patagonia demonstrate how canvas bridges utility and brand storytelling. From a cost-performance perspective, canvas maintains a favorable balance between durability and production scalability, reinforcing its dominance in both retail and promotional procurement channels.

Recycled and synthetic textile-based tote bags represent the fastest-growing material segment, driven by sustainability mandates and formal ESG procurement policies from corporations and institutions. It primarily includes post-consumer recycled polyester (rPET), recycled cotton blends, and mixed synthetic-cotton composites, distinguishing it from conventional canvas or virgin cotton products. Growth is supported by rising adoption of rPET derived from plastic bottle waste, as well as mechanically recycled cotton integrated into blended yarn systems. These materials reduce reliance on virgin fibers while maintaining durability and print compatibility. Manufacturers incorporating Global Recycled Standard (GRS)-certified inputs achieve higher average selling prices and stronger margin resilience due to documented environmental benefits. Urban consumers, universities, and multinational corporations increasingly demand traceable sourcing and verified recycled content for promotional merchandise. Brands such as Everlane have introduced collections emphasizing recycled fibers and transparent sourcing disclosures, strengthening pricing power and brand credibility. As regulatory scrutiny around environmental claims intensifies, certified recycled textile blends are expected to capture a larger share of incremental market value during the forecast period..

Application Insights

The daily use/casual wear segment is anticipated to maintain its leadership position with approximately 46.2% market share, supported by high replacement frequency and broad demographic penetration. Tote bags have evolved into multifunctional everyday carriers used for commuting, shopping, work essentials, and educational purposes. Urban professionals, students, and retail shoppers prefer tote bags for their lightweight design, open-access format, and adaptability to both formal and casual attire. Mass-market fashion retailers such as H&M and global retail operators under Inditex frequently integrate tote bags into seasonal collections, reinforcing habitual consumer purchases. The segment benefits from consistent baseline demand independent of fashion cycles, ensuring volume stability even during economic slowdowns. Its broad utility profile supports steady revenue generation across price tiers.

The fashion and luxury application segment is anticipated to grow at a CAGR of 7.63%, driven by premium brand collaborations, limited-edition releases, and elevated lifestyle positioning. In this segment, tote bags function as entry-level luxury accessories that allow brands to attract new customers while maintaining aspirational value. Designer houses such as Gucci and premium French label Longchamp have successfully positioned tote bags within curated collections, leveraging craftsmanship, premium leather, and brand heritage to command higher margins. Social media visibility, influencer marketing, and exclusivity-driven capsule drops accelerate demand among affluent urban consumers. This segment delivers stronger margin expansion compared to commoditized daily-use categories, making it strategically significant for brand-driven growth.

Regional Insights

North America Tote Bag Market Trends - Plastic Ban Policies and Retail-Led Reusable Adoption Expansion

North America represents a substantial revenue contributor, with the U.S. acting as the core demand center. State-level plastic bag bans and fees, such as those implemented in California and New York, have structurally shifted consumer behavior toward reusable totes in grocery and mass retail channels. Major retailers, including Walmart and Target Corporation, have expanded private-label reusable bag assortments while phasing out single-use plastic options in several states, reinforcing category normalization. These retail-led initiatives materially increased baseline demand across supermarkets and hypermarkets.

Corporate sustainability mandates continue to strengthen bulk procurement of reusable canvas and recycled-fabric totes for conferences, trade events, and ESG-aligned promotional campaigns. Lifestyle and outdoor brands such as Patagonia emphasize recycled content and supply chain transparency, influencing broader industry standards for traceability and material disclosures. The direct-to-consumer ecosystem, accelerated by platforms such as Shopify, enables smaller sustainable brands to scale regionally without traditional retail dependence.

Investment activity is concentrated in recycled textile sourcing partnerships, warehouse automation for faster fulfillment, and personalization technologies, including digital textile printing. Strategic positioning in North America increasingly depends on combining verifiable sustainability certifications with strong brand storytelling to secure institutional and corporate contracts.

Europe Tote Bag Market Trends - EU Single-Use Plastics Directive Driving Compliance-Centric Reusable Market

Europe maintains a mature and regulation-driven reusable bag market supported by cohesive environmental directives and high consumer sustainability awareness. The European Union’s Single-Use Plastics Directive has accelerated retailer transitions toward reusable alternatives, particularly in Germany, France, and Spain. Supermarket groups such as Carrefour and Tesco have integrated reusable tote options into mainstream checkout processes, strengthening recurring purchase behavior.

Germany continues to lead in adoption due to strong environmental norms and retail participation, while the U.K. benefits from early plastic bag charge implementation. Fashion and lifestyle brands, including Stella McCartney, promote sustainable material sourcing, reinforcing consumer preference for organic and recycled textiles.

Regulatory transparency requirements across the EU require accurate labeling of recycled content and certified supply chain documentation, increasing compliance costs but enhancing consumer trust. Retailers increasingly prioritize locally sourced cotton or certified recycled polyester to align with corporate sustainability targets and Scope 3 emissions disclosures. As a result, suppliers entering Europe must ensure compliance-ready documentation and third-party certifications to remain competitive in procurement processes.

Asia Pacific Tote Bag Market Trends - Manufacturing Scale Leadership and Export-Oriented Sustainable Production Growth

Asia Pacific is projected to account for 35.3% of the market share in 2026, making it both the leading and fastest-growing regional market. China and India anchor manufacturing output due to established textile supply chains and cost efficiencies, while Japan drives premium and design-oriented demand. Large manufacturers such as Shenzhou International Group support global apparel and bag production through vertically integrated textile operations, strengthening export capacity.

Urbanization and e-commerce penetration continue to accelerate tote bag adoption, particularly among younger consumers in metropolitan areas. Platforms such as Alibaba Group and Flipkart facilitate the rapid distribution of private-label and sustainable tote brands, broadening consumer access beyond tier-one cities. In Japan, retailers, including Muji, emphasize minimalist, reusable canvas designs aligned with sustainability values, reinforcing premium positioning.

Manufacturers across China and Southeast Asia are investing in recycled fiber processing and global certification programs to meet Western import standards, enabling preferential access to North American and European institutional buyers. Strategic focus in Asia Pacific increasingly centers on export compliance, material innovation, and domestic brand development to capture both regional consumption growth and international demand.

Competitive Landscape

The global tote bag market is fragmented globally, with numerous small and medium-sized manufacturers serving commoditized segments. Premium and branded categories exhibit higher concentration levels, where established lifestyle and fashion brands capture greater margins. No single company dominates global volume, though leading brands influence pricing trends in the premium segment.

Market leaders prioritize sustainable material innovation, omnichannel retail integration, D2C branding, and cost-efficient sourcing. Premium brands focus on limited-edition releases and storytelling, while high-volume producers emphasize operational efficiency and institutional partnerships.

Key Industry Developments:

- In March 2025, Baggu introduced a collection of bags made with recycled leather scraps combined with recycled polyester and nylon, expanding its eco-friendly portfolio beyond traditional canvas and nylon totes and reinforcing its commitment to sustainable materials and design.

- In February 2025, Lotus Sustainables became the official reusable-bag partner for Expo West 2025, launching a new 100% rPET mini-tote, a strategic product rollout linking sustainability credentials with high-visibility event branding and industry participation.

Companies Covered in Tote Bag Market

- Baggu

- EcoBags

- Envirosax

- ChicoBag

- Earthwise Bag Company

- Vera Bradley

- L.L.Bean

- The Tote Bag Factory

- Bullet Line

- Custom Earth Promos

- Enviro-Tote

- H&M

- Zara

- Uniqlo

- Carrefour

- Tesco

- Walmart

- Target Corporation

Frequently Asked Questions

The global tote bag market is estimated to be valued at US$3.1 billion in 2026.

The tote bag market is projected to reach approximately US$4.4 billion by 2033.

Key trends include rising adoption of sustainable and recycled fabrics, increasing demand for customized and branded promotional totes, expansion of D2C e-commerce channels, and growing popularity of fashion-oriented and premium canvas totes among urban consumers.

By material, canvas remains the leading segment, accounting for the highest market share due to durability, printability, and wide application across retail and fashion categories.

The tote bag market is expected to grow at a CAGR of 5.2% between 2026 and 2033.

Some of the major companies include Baggu, ChicoBag, EcoBags, Envirosax, and Enviro-Tote.