- Smart Packaging

- Thermal Insulation Packaging Market

Thermal Insulation Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Thermal Insulation Packaging Market by Material Type (Expanded Polystyrene (EPS), Polyurethane Foam, Others), Packaging Format (Boxes & Containers, Bags & Pouches, Others), End-Use Industry, and Regional Analysis for 2026 - 2033

Thermal Insulation Packaging Market Size and Trends Analysis

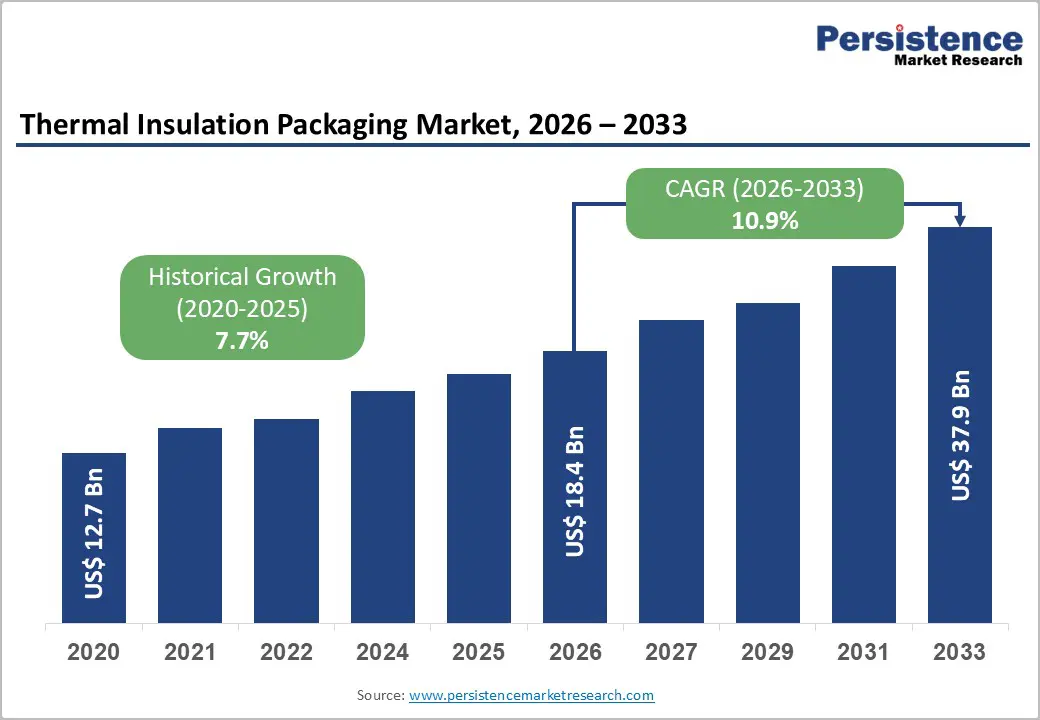

The global thermal insulation packaging market size is likely to be valued at US$18.4 billion in 2026 and is expected to reach US$37.9 billion by 2033, growing at a CAGR of 10.9% between 2026 and 2033, driven by the expansion of pharmaceutical cold-chain logistics, rising demand for temperature-sensitive e-commerce grocery fulfillment, and continuous material innovation such as phase change materials (PCMs) and vacuum insulated panels (VIPs).

While performance expectations are increasing, cost-performance tradeoffs and sustainability pressures are reshaping procurement decisions, creating differentiated growth opportunities across materials, formats, and regions.

Key Industry Highlights:

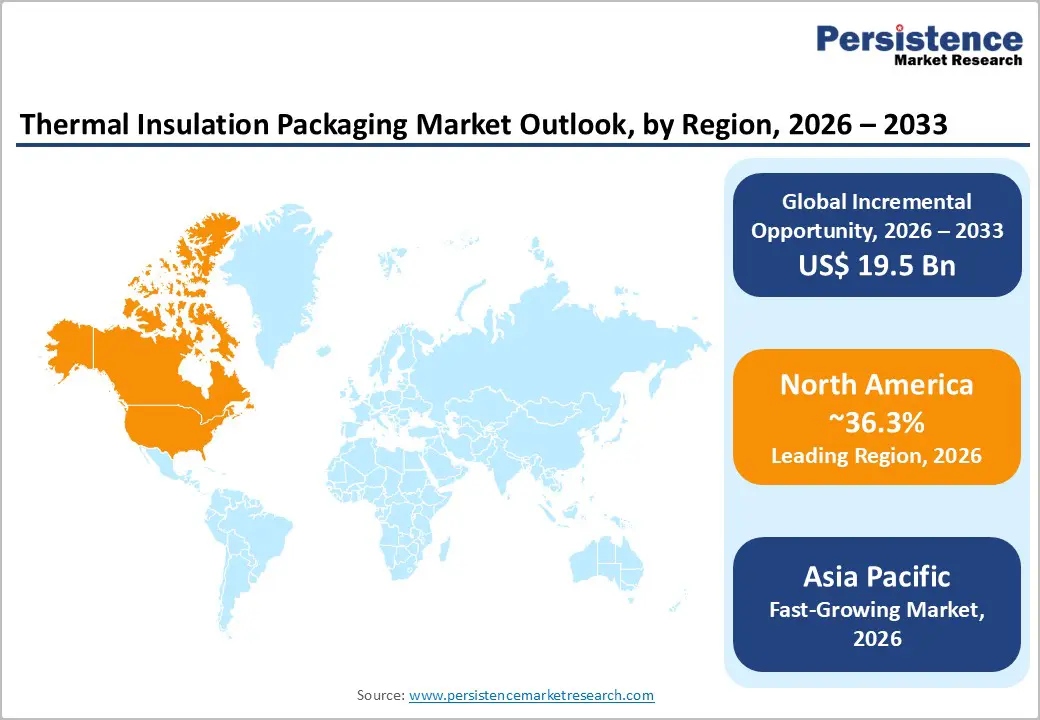

- Leading Region: North America is projected to remain the leading regional market, accounting for approximately 36.3% of market share, driven by strong pharmaceutical manufacturing, advanced cold-chain infrastructure, and strict regulatory compliance requirements.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, supported by the rapid expansion of e-commerce grocery platforms, increasing pharmaceutical exports, and significant investments in refrigerated logistics infrastructure.

- Investment Plans: Industry investment is focused on reusable shipper programs, expansion of pharmaceutical packaging production capacity, integration of IoT-enabled temperature monitoring systems, and development of recyclable and sustainable insulation materials.

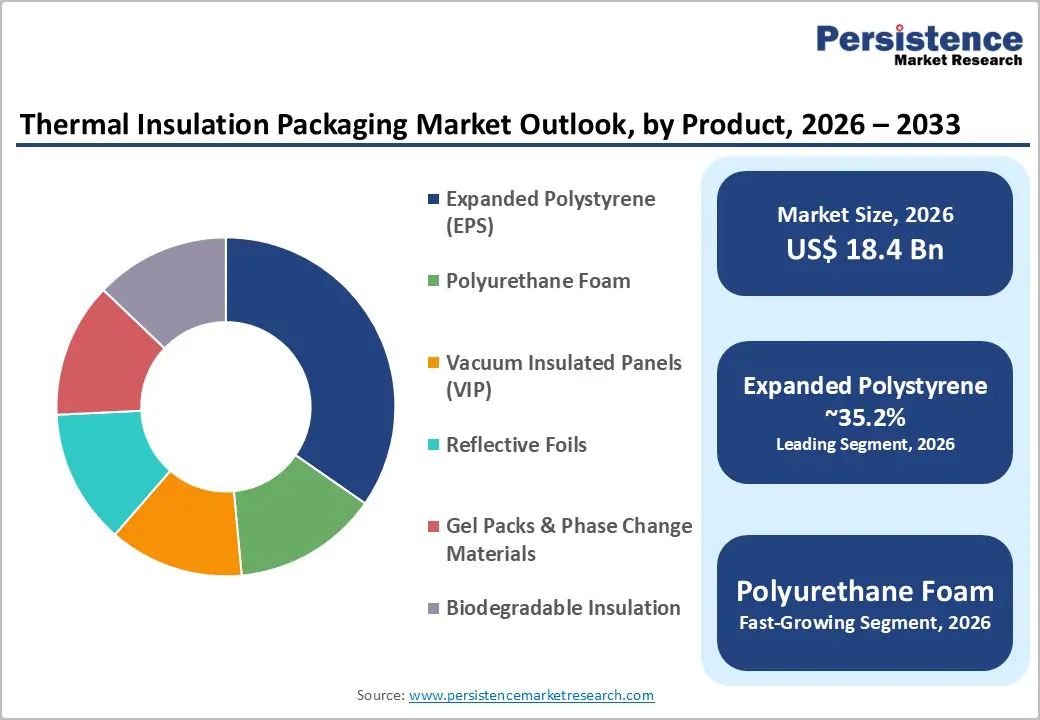

- Dominant Material Type: Expanded Polystyrene (EPS) is anticipated to lead the material segment with 35.2% of market share, supported by its cost efficiency and widespread adoption in food and domestic pharmaceutical shipments.

- Leading End-Use Industry: Pharmaceuticals & biotechnology represent the leading end-use segment with approximately 37.8% market share, driven by the growing distribution of biologics, vaccines, and specialty therapies requiring validated temperature-controlled packaging.

| Key Insights | Details |

|---|---|

| Thermal Insulation Packaging Market Size (2026E) | US$18.4 Bn |

| Market Value Forecast (2033F) | US$37.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Pharmaceutical & Biologics Cold Chain

The increasing global reliance on biologics, specialty drugs, vaccines, and advanced therapies represents a long-term structural driver for thermal insulation packaging. Biologics often require strict temperature ranges between 2°C and 8°C or controlled room temperature conditions, which necessitate validated insulated shippers and active temperature-control systems. The commercialization of temperature-sensitive therapies and expansion of global vaccine distribution programs have significantly increased the volume of regulated cold-chain shipments. Pharmaceutical companies require documented validation, temperature monitoring, and compliance with distribution standards, increasing demand for premium thermal packaging systems. Suppliers offering validated, compliance-aligned solutions command premium pricing and benefit from multi-year procurement contracts with pharmaceutical manufacturers, contract manufacturing organizations (CMOs), and contract research organizations (CROs).

E-Commerce Grocery & Last-Mile Temperature Control

Rapid growth in online grocery, direct-to-consumer (D2C) meal kits, and refrigerated parcel delivery has increased demand for lightweight and cost-efficient thermal packaging formats.Last-mile delivery requires packaging that balances insulation performance, shipping weight, and consumer convenience. Retailers and logistics providers are adopting insulated mailers, reusable thermal bags, and thin-profile polyurethane liners to reduce dimensional weight charges while maintaining temperature integrity. Rising urbanization and consumer preference for convenience further accelerate this shift. Growth strongly favors flexible and low-capex formats such as bags, pouches, envelopes, and liners. Companies capable of integrating reusable logistics loops and refurbishment systems are positioned to capture higher margins.

Material & Systems Innovation

Continuous advancements in engineered insulation materials are significantly enhancing thermal efficiency. Phase change materials (PCMs) allow controlled temperature windows, while vacuum insulated panels (VIPs) provide high thermal resistance with minimal thickness. High-R polyurethane foams further reduce packaging bulk without compromising performance. These innovations enable longer hold times, thinner packaging profiles, and reduced freight costs. They also expand use cases into high-value electronics, specialty chemicals, and long-haul pharmaceutical shipments. Material innovators can justify premium pricing where payload value is high. Conversely, traditional EPS suppliers face substitution risk in performance-sensitive segments.

Barrier Analysis - Cost & Carbon Constraints

High-performance insulation materials such as VIPs and engineered PCMs carry significantly higher unit costs than expanded polystyrene (EPS). For low-margin food and industrial shipments, cost sensitivity limits adoption despite performance benefits. Corporations also face growing pressure to reduce Scope 3 emissions and packaging waste. Regulatory requirements and retailer sustainability mandates increase compliance expenses. Premium thermal solutions may increase packaging costs by 10-25% compared to EPS, slowing procurement transitions in cost-sensitive markets.

Opportunity Analysis - Supply Chain & Certification Complexity

Thermal insulation packaging systems rely on specialized raw materials such as vacuum insulated panels (VIPs), phase change materials (PCMs), and engineered foams, along with highly controlled manufacturing and assembly processes. Fluctuations in the availability of these materials can lead to extended production lead times and pricing volatility for packaging manufacturers. In regulated sectors such as pharmaceuticals and biotechnology, customers require extensive qualification testing, thermal validation studies, and regulatory documentation before approving a packaging system for use. These validation processes are necessary to ensure product stability and regulatory compliance during transportation. As a result, qualification cycles can extend procurement timelines by 6-12 weeks, while validation and testing procedures can increase upfront implementation costs by 3-5% of the initial purchase value. Companies that can streamline validation processes, provide standardized documentation, and maintain stable supply chains gain a competitive advantage in highly regulated markets.

Reusable Systems & Circular Models

Reusable thermal packaging solutions are emerging as a major opportunity as companies seek to reduce waste, lower lifecycle costs, and improve supply chain sustainability. Returnable insulated shippers, reusable containers, and refurbishment programs allow packaging to be used multiple times before replacement, significantly lowering long-term packaging expenditure. High-frequency pharmaceutical distribution routes and e-commerce grocery delivery networks are particularly suitable for reusable systems due to predictable logistics cycles. Companies that incorporate asset tracking technologies, refurbishment services, and reverse logistics infrastructure can transform packaging from a one-time product sale into a recurring service-based revenue model. For example, reusable packaging pilots in densely populated metropolitan distribution corridors have demonstrated the ability to reduce per-shipment packaging costs by 20-30% over a period of 12-24 months, while simultaneously improving sustainability metrics and reducing packaging waste.

Lower-Cost High-Performance Materials for Emerging Markets

Rapid expansion of cold-chain infrastructure in emerging economies across Asia Pacific and Latin America is creating strong demand for cost-efficient thermal packaging solutions. Pharmaceutical distribution, vaccine logistics, and growing e-commerce grocery services require packaging systems that can deliver reliable temperature control while remaining affordable for high-volume shipments. Localizing the production of polyurethane insulation liners, gel packs, and phase change material inserts allows manufacturers to significantly reduce transportation and import costs. Collaboration with regional logistics providers and packaging converters enables faster product adaptation to local climate conditions and transportation routes. Through localized manufacturing and optimized supply chains, companies can reduce overall unit costs by 12-18%, making advanced thermal packaging more accessible while expanding their presence in rapidly developing cold-chain markets.

Smart Packaging & Data Services Integration

The integration of digital monitoring technologies is transforming thermal packaging into a connected and data-driven logistics solution. Packaging systems equipped with IoT sensors, wireless temperature loggers, and cloud-based monitoring platforms provide real-time visibility into shipment conditions throughout the supply chain. Pharmaceutical manufacturers and biotechnology companies increasingly require continuous temperature monitoring and automated compliance reporting to ensure regulatory adherence and product safety. These capabilities enable logistics managers to detect temperature deviations early and take corrective action before product loss occurs. Packaging providers that bundle hardware solutions with digital monitoring platforms and analytics services can introduce subscription-based revenue models. This combination of packaging products and data services increases customer retention, strengthens supply chain transparency, and creates long-term strategic relationships with pharmaceutical and life-science logistics providers.

Category- wise Analysis

Material Type Insights

Expanded Polystyrene (EPS) is anticipated to retain its leading position, accounting for approximately 35.2% market share in 2026. Its dominance stems from affordability, widespread availability, and proven thermal performance for short-duration and regional shipments. EPS offers reliable insulation in temperature ranges typically required for chilled food products and non-critical pharmaceutical products, making it a default choice for high-volume applications. EPS is particularly prevalent in food & beverage logistics and domestic pharmaceutical distribution networks.

For example, meal-kit providers and grocery delivery platforms commonly deploy EPS shippers paired with gel packs for 24-48-hour delivery windows. Similarly, regional vaccine distributors and diagnostic kit suppliers use molded EPS containers due to their low material cost and consistent insulation performance. Its ease of molding enables customization across various box sizes, while established converter networks allow rapid production scaling during seasonal demand peaks such as holiday food shipments or vaccination drives. Although sustainability regulations in regions such as the EU are tightening around single-use plastics, EPS continues to maintain strong adoption in cost-sensitive and performance-focused applications where cost per shipment remains a primary decision factor.

Polyurethane (PU) foam and advanced high-R-value rigid foams represent the fastest-growing material category within the market. These materials provide superior insulation efficiency in thinner wall profiles compared to EPS, reducing overall dimensional weight and helping shippers optimize freight expenses, particularly important in air cargo and express parcel logistics. PU foam solutions are increasingly deployed in pharmaceutical cold chain shipments requiring 2-8°C or controlled room temperature conditions for extended transit durations.

For instance, specialty biologics manufacturers and clinical trial logistics providers utilize high-performance PU shippers to maintain stable temperatures during cross-border distribution. Innovations in flame-retardant grades and emerging recyclable or lower-GWP formulations are improving regulatory acceptance and environmental positioning. While premium in cost compared to EPS, the enhanced thermal reliability and space optimization advantages make PU foam especially attractive for high-value biologics, cell therapies, and international shipments where failure risk carries significant financial implications.

End-use Industry Insights

The pharmaceuticals and biotechnology segment is anticipated to account for approximately 37.8% of market share in 2026, maintaining its leadership position. Growth is driven by increasing global distribution of high-value biologics, specialty injectables, vaccines, and temperature-sensitive therapies that require validated thermal packaging with documented performance. Cold chain packaging used in this sector must comply with stringent regulatory standards such as Good Distribution Practice (GDP) and validated stability protocols.

For example, mRNA vaccine distribution programs and monoclonal antibody shipments rely on insulated shippers tested for 48-120 hours of temperature control. The high cost of product loss, often thousands of dollars per shipment, makes thermal reliability and qualification testing critical purchasing criteria. Long-term supply agreements between pharmaceutical manufacturers and packaging providers further enhance demand stability, while ongoing expansion of clinical trials and personalized medicine supports sustained volume growth in validated temperature-controlled packaging solutions.

Food & beverage is projected to be the fastest-growing end-use segment, supported by rapid expansion of e-commerce grocery platforms, direct-to-consumer meal kits, specialty food exports, and last-mile chilled delivery services. Unlike pharmaceutical applications, demand in this segment centers on cost-effective, lightweight thermal solutions optimized for 24-72-hour transit.

Meal-kit companies, seafood exporters, artisanal dairy brands, and online grocery retailers commonly deploy insulated shippers combined with gel packs or PCM bricks to maintain chilled or frozen conditions. Growth in urban home delivery ecosystems and rising consumer expectations for fresh, temperature-controlled shipments are accelerating packaging consumption volumes. Sustainability is also emerging as a differentiator, prompting food brands to experiment with recyclable liners, molded fiber insulation, and compostable thermal solutions.

Regional Insights

North America Thermal Insulation Packaging Market Trends - Biopharma-Driven Demand and IoT-Enabled Cold Chain Expansion

North America represents the largest regional market, accounting for approximately 36.3% of global value, with the U.S. serving as the primary growth engine. The country’s advanced biopharmaceutical ecosystem, anchored by companies such as Pfizer, Moderna, and Johnson & Johnson, drives sustained demand for validated, temperature-controlled packaging systems. Strong biologics pipelines, expanding cell and gene therapy distribution, and strict regulatory oversight from the U.S. Food and Drug Administration (FDA) and standards from the U.S. Pharmacopeia require documented temperature control and performance validation. This regulatory intensity increases reliance on high-performance insulated shippers, data loggers, and telemetry-enabled packaging solutions.

Recent developments illustrate how the region is evolving. Sonoco ThermoSafe expanded its temperature-controlled packaging portfolio and manufacturing capabilities in North America to support biologics distribution and clinical trials, strengthening domestic production resilience. Pelican BioThermal has scaled reusable shipper programs and rental fleets for pharmaceutical clients, accelerating the shift toward circular packaging models.

Logistics providers such as UPS Healthcare continue investing in cold-chain hubs and IoT-enabled monitoring systems, integrating real-time visibility with insulated packaging solutions. E-commerce grocery growth, supported by retailers such as Amazon (Amazon Fresh) and Walmart, also sustains demand for cost-effective insulated shippers in last-mile applications. As a result, North America combines premium pharmaceutical demand with high-volume food logistics, maintaining regional leadership while driving innovation in reusable and digitally monitored thermal packaging.

Europe Thermal Insulation Packaging Market Trends - Sustainability Regulations Accelerating Recyclable and Reusable Packaging Shift

Europe holds the second-largest regional share, supported by its strong pharmaceutical manufacturing base and stringent environmental regulations. Germany leads in industrial production and high-performance insulation material adoption, with pharmaceutical exporters relying on validated solutions to comply with EU Good Distribution Practice (GDP) guidelines. The United Kingdom remains a hub for life sciences innovation and online grocery penetration, while France and Spain demonstrate expanding direct-to-consumer (D2C) food shipment volumes.

Regulatory pressure plays a defining role in shaping material preferences. The European Union’s Packaging and Packaging Waste Directive (PPWD) and circular economy initiatives are accelerating the transition away from difficult-to-recycle materials. This policy direction places pressure on conventional EPS formats while supporting fiber-based, recyclable, and reusable insulated solutions. For example, DS Smith has introduced recyclable, fiber-based temperature-controlled packaging solutions for pharmaceutical and food customers across Europe, reinforcing sustainability alignment.

va-Q-tec continues expanding its vacuum-insulated panel (VIP) container rental services across European pharma corridors, enhancing long-duration temperature control for global exports. Supermarket chains such as Tesco and Carrefour have piloted recyclable insulated liners for online grocery fulfillment, influencing packaging material shifts at scale. These combined regulatory and commercial dynamics are reshaping Europe’s competitive landscape toward reusable systems, certified recyclable materials, and lower-carbon insulation technologies.

Asia Pacific Thermal Insulation Packaging Market Trends - Rapid Cold Chain Infrastructure Growth and E-Commerce Scale-Up

Asia Pacific is the fastest-growing regional market, supported by rapid cold-chain infrastructure expansion, pharmaceutical manufacturing growth, and large-scale e-commerce grocery penetration. China leads in e-commerce scale, with platforms such as JD.com and Alibaba Group investing heavily in refrigerated distribution networks to support fresh food and healthcare delivery. Expansion of temperature-controlled warehousing and last-mile refrigerated fleets strengthens demand for insulated shipping containers across urban centers.

Japan emphasizes premium validated packaging for pharmaceutical exports, with global manufacturers requiring strict thermal compliance for biologics and specialty medicines. Companies such as Dai Nippon Printing are advancing high-performance thermal packaging formats tailored to regulated export markets. In India, pharmaceutical manufacturers, including Serum Institute of India support large-scale vaccine and biologics exports, driving demand for qualified insulated shippers. Government-backed cold-chain initiatives and Production Linked Incentive (PLI) schemes further stimulate infrastructure investment.

ASEAN countries are witnessing rising private-sector investment in refrigerated logistics, while regional manufacturers scale local production of polyurethane foam and PCM products, improving affordability and reducing import dependency. These developments collectively enhance scalability, reduce lead times, and strengthen Asia Pacific’s position as the fastest-growing market for insulated temperature-controlled packaging solutions.

Competitive Landscape

The global thermal insulation packaging market is moderately consolidated. Large packaging conglomerates compete on scale and product breadth, while niche firms focus on innovation and compliance-driven segments. Leading companies focus on validated performance, material innovation, cost optimization, reusable service models, and geographic expansion. Bundled solutions integrating telemetry and compliance reporting differentiate premium providers.

Key Industry Developments:

- In January 2025, Sonoco ThermoSafe expanded its insulated packaging product line by adding fully recyclable shuttle shippers for 2°C-8°C distribution, aiming to meet growing sustainability standards in pharmaceutical cold chain logistics.

- In February 2025, CSafe Global introduced enhanced real-time alert capabilities to its temperature monitoring platform for cold chain shipments, incorporating predictive analytics to improve biologics and vaccine shipment integrity.

Companies Covered in Thermal Insulation Packaging Market

- Sonoco ThermoSafe

- Pelican BioThermal

- va-Q-tec

- Cold Chain Technologies

- Sealed Air

- DS Smith

- Dai Nippon Printing

- Cryopak

- Intelsius

- Softbox Systems

- Envirotainer

- CSafe

- Tempack

- Insulated Products Corporation

- American Aerogel Corporation

Frequently Asked Questions

The global thermal insulation packaging market is estimated to be valued at US$18.4 billion in 2026.

The thermal insulation packaging market is projected to reach US$37.9 billion by 2033.

Key trends include rising demand for validated pharmaceutical cold-chain packaging, increasing adoption of reusable shipper systems, integration of IoT-enabled temperature monitoring devices, transition toward recyclable and fiber-based insulation materials in response to environmental regulations, and expansion of last-mile grocery delivery solutions.

By material type, expanded polystyrene (EPS) remains the leading segment, accounting for an anticipated 35.2% market share, driven by its affordability and widespread use in food and domestic pharmaceutical shipments. By end-use, pharmaceuticals & biotechnology lead with approximately 37.8% market share, supported by the growing distribution of biologics and specialty therapies.

The thermal insulation packaging market is expected to grow at a CAGR of 10.9% from 2026 to 2033.

Major players with strong product portfolios and global presence include Sonoco ThermoSafe, Pelican BioThermal, va-Q-tec, Cold Chain Technologies, and Sealed Air.