- Industrial Automation

- Telescopic Handler Market

Telescopic Handler Market Size, Share, and Growth Forecast, 2026 - 2033

Telescopic Handler Market by Lift Height (5 – 15 meters, More than 15 meters, and Less than 5 meters), Lift Capacity (3 – 10 tons, More than 10 tons, and Less than 3 tons), Industry (Construction, Agriculture, Oil & Gas, Manufacturing Industry, Transport and Logistics, Power Utilities, Forestry, and Others), Propulsion Type (ICE, and Electric), Telehandler Type (Large, and Compact) and Regional Analysis for 2026 - 2033

Telescopic Handler Market Size and Trends Analysis

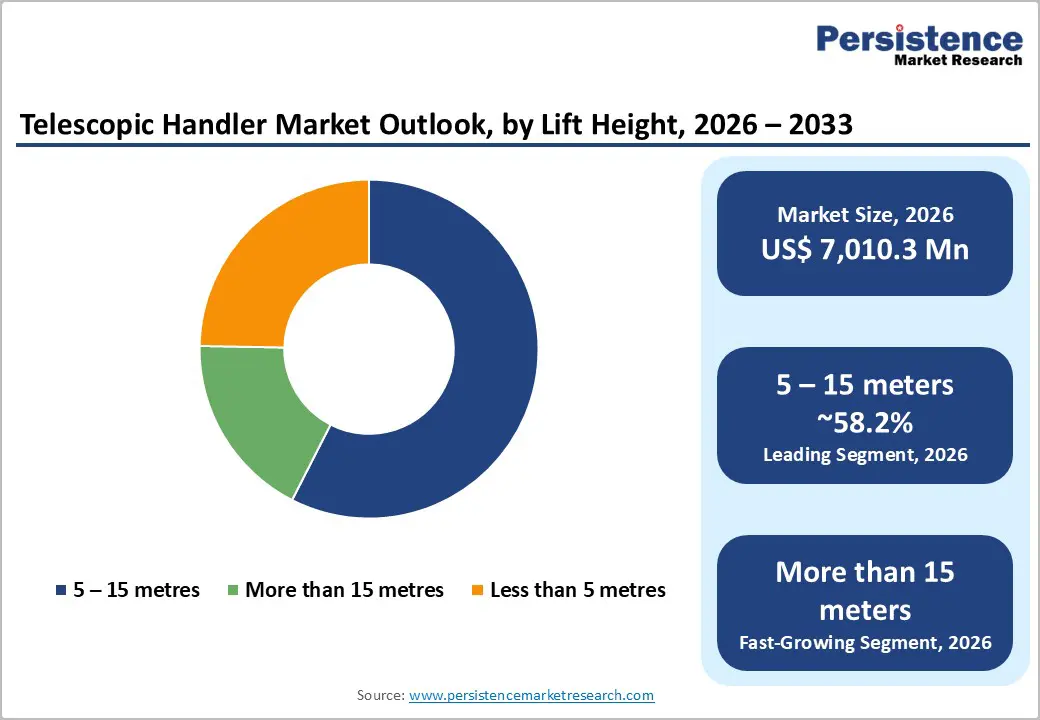

The global Telescopic Handlers market size is supposed to be valued at US$ 7.01 Bn in 2026 and is projected to reach US$ 10.33 Bn by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The sustained expansion in global construction output, projected to grow close to 4% annually to 2030, underpins robust growth and drives demand for versatile lifting and material-handling equipment on building and infrastructure projects. At the same time, rising mechanization and automation in agriculture, supported by initiatives from bodies such as the FAO to promote sustainable agricultural mechanization, are encouraging farmers and contractors to adopt multi-purpose equipment, such as telehandlers, to handle bales, feed, and bulk materials more efficiently. Robust non-residential construction spending in markets such as the United States, together with tightening safety and emissions regulations for non-road machinery, further supports fleet renewal and upgrades to more productive and compliant telehandlers.

Key Industry-Highlights:

- Sales Order: In November 2025, Ardent Hire Solutions has underlined its confidence in the UK housing & construction sector with a landmark £40 million order for more than 450 telehandlers from Manitou UK, the largest single order ever placed with Manitou UK.

- Construction Equipment Vs Telescopic Handler: The global telescopic handler market accounted for approximately 4.2% of the total construction equipment market by value and 6.3% by volume in 2025.

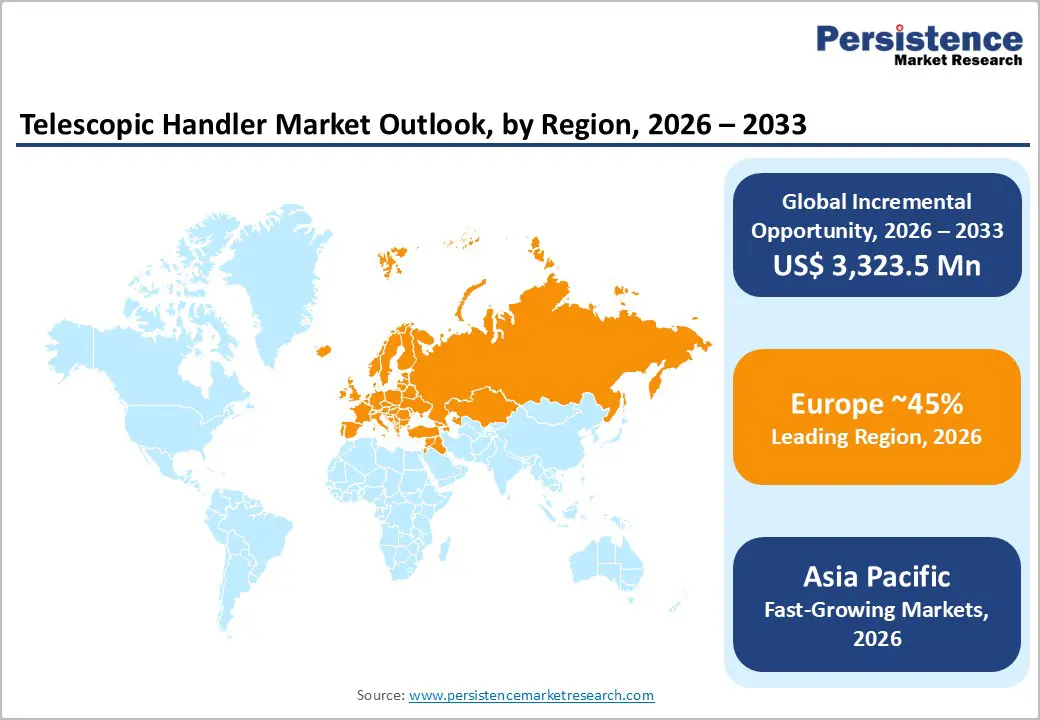

- Leading region: Europe currently leads the telehandlers market, supported by high non-residential construction spending, robust rental penetration, and strong adoption across infrastructure, industrial, and commercial building projects.

- Fastest-growing region: Asia Pacific is the fastest-growing market, benefiting from rapid urbanization, large-scale infrastructure programs such as the BRI and Smart Cities Mission, and rising mechanization in construction and agriculture.

- Dominant segment: Within product segmentation, telehandlers with 5 – 15 metres lift height and 3 – 10 tonnes capacity, primarily serving the construction industry, collectively command the largest share of installed units.

- Fastest-growing segment: Compact telehandlers and Electric propulsion options are the fastest-growing sub-segments, driven by space-constrained urban projects, rental fleet diversification, and tightening emissions regulations.

- Key market opportunity: Long-term growth is anchored in low-emission and electric telehandlers for urban construction and industrial sites, plus rising adoption in emerging markets with large infrastructure and smart-city pipelines requiring versatile, high-productivity material-handling solutions.

| Key Insights | Details |

|---|---|

|

Telescopic Handler Market Size (2026E) |

US$ 7,010.3 Mn |

|

Market Value Forecast (2033F) |

US$ 10,333.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

Market Dynamics

Drivers - Expanding Global Construction and Infrastructure Pipelines

A primary growth driver for telehandlers is the steady expansion of global construction and infrastructure spending, which is expected to reach about US$ 17.5 trillion by 2030, with China, India, and the U.S. accounting for a substantial share of incremental activity. Large non-residential programs in data centers, manufacturing, transportation, and energy are particularly material-handling intensive, requiring equipment that can lift heavy loads to height on congested and uneven sites where cranes or conventional forklifts are impractical.

In the United States, non-residential construction spending remains above US$ 1.2 trillion on an annualized basis, with data centers and manufacturing accounting for over 90% of the year-on-year increase between 2023 and 2024, directly translating into higher demand for jobsite access and lifting equipment, including telehandlers. In North America, telehandlers have become one of the fastest-growing construction machines; Off-Highway Research data cited by industry media show telehandler unit sales in the U.S. rising by more than a third to around 30,000 units in 2023, representing nearly 10% of all construction machines sold, confirming their central role on modern worksites.

Rising Agricultural Mechanization and Material-Handling Automation

A second major driver is accelerated mechanization and automation in agriculture, livestock, and rural industries, where telehandlers increasingly replace traditional loaders and tractors for intensive bulk-handling tasks. The FAO’s work on agricultural automation highlights how powered machinery significantly improves productivity, timeliness, and labor efficiency, especially as rural labor becomes scarcer and more expensive. In Europe, the agricultural machinery association CEMA represents about 1,300 manufacturers with an annual turnover of nearly €40 billion, reflecting the scale of mechanization in which agricultural telehandlers now play a key part.

Data from Axema cited by Manitou Group show that Manitou has maintained the number-one position in agricultural telehandler registrations in France, with a 31.1% market share in 2025, underlining both the maturity and continued growth of telehandlers in European farming. In Ireland, industry estimates indicate telehandler volumes of roughly 600 units a year, with around 70% sold to farming and agricultural contractors, further underscoring their role as a mainstream mechanization solution in rural economies.

Restraint - High Upfront Costs and Ownership Complexity

Telehandlers involve higher upfront acquisition costs and more complex maintenance than basic forklifts or tractors, which can discourage smaller contractors and farms from outright purchases. North American rental rankings such as the Telehandler30 index show that the 30 largest rental fleets collectively own more than 90,000 telehandlers, with year-on-year fleet growth still positive but moderating as interest rates and equipment prices climb. This underscores how many users prefer short-term rental or leasing to avoid capital commitments, indirectly limiting unit sales growth despite strong utilization. Ownership also requires operator training, regular inspections, and adherence to load charts and stability limits, which can strain smaller operators without dedicated safety and maintenance resources.

Stringent Emissions and Safety Regulations Increasing Compliance Burden

Telehandlers are subject to stringent emissions and safety regulations that increase design complexity and costs for manufacturers and owners. In the European Union, Stage V non-road mobile machinery standards (Regulation EU 2016/1628) introduce tighter particulate mass limits of 0.015 g/kWh and a particle-number cap of 1×10¹²/kWh, effectively requiring advanced aftertreatment such as diesel particulate filters on many diesel telehandler engines. At the same time, OSHA in the U.S. classifies telehandlers as rough-terrain forklifts, obliging employers to ensure formal operator certification, structured training, and regular inspections, with non-compliance subject to penalties. While these rules improve safety and environmental performance, they can increase total cost of ownership and slow adoption among price-sensitive end users, particularly in emerging markets

Opportunities - Electrification and Low-Emission Telehandlers

The transition toward low-emission and zero-emission equipment offers a powerful long-term opportunity. Stage V in Europe and tightening air-quality rules worldwide are pushing contractors and rental companies to seek quieter, emission-free equipment that can operate indoors, in tunnels, and on urban sites subject to stringent restrictions. OEMs and partners are responding: in 2024, Manitou Group and rental leader Kiloutou unveiled what they describe as the first retrofit electric telehandler, replacing the diesel engine with a full electric drivetrain while maintaining equivalent performance.

The electrified model achieved about a 25% reduction in its environmental score across 16 impact indicators and is being trialed on worksites for at least 12 months to validate range, charging, and customer acceptance. Similar developments include purpose-built electric telehandlers in the 3–4 ton and 10 metre range, targeted at indoor logistics, urban construction, and environmentally sensitive zones. As battery costs fall and charging infrastructure improves, electric telehandlers and hybrid concepts are poised to capture a growing share of new sales, particularly in Europe and parts of North America and Asia with strong green-construction agendas.

Emerging Market Infrastructure, Smart Cities, and Belt and Road Projects

Rapid urbanization and infrastructure deployment in Asia, the Middle East, and Africa create a sizeable opportunity pool for telehandlers. China’s Belt and Road Initiative (BRI) has generated cumulative engagement of about US$ 1.053 trillion over ten years, including roughly US$ 634 billion in construction contracts and US$ 419 billion in non-financial investments, much of it in transport, energy, and urban infrastructure that require extensive materials-handling capacity. Recent analysis shows over US$ 92.4 billion in BRI-related deals in 2023, an 18% increase on the previous year, with technology, manufacturing, and energy projects further widening the base of equipment demand.

In India, the Smart Cities Mission covers 100 designated cities, with an RTI response indicating that by mid-2025, about 8,067 projects, roughly 94% of the total, had been completed at a cost of INR 1.64 lakh crore, transforming urban districts with dense construction activity. These large, complex, often high-rise and brownfield projects favor versatile telehandlers that can maneuver in tight spaces, use multiple attachments, and replace several dedicated machines, positioning telehandlers as key beneficiaries of emerging-market infrastructure cycles

Category-wise Analysis

Lift Height Insights

Within Lift Height, the 5 – 15 metres segment is the leading category, accounting for close to 58% of global telehandler demand by reach range. Industry analysis indicates that telehandlers with 5–15 metre reach offer the most attractive balance between boom length, stability, and acquisition cost, making them the default choice for mid-rise building construction, warehouse yards, and agricultural tasks such as stacking bales or loading feed into intermediate-height silos.

OEM portfolios from brands like JCB, Manitou, and Wacker Neuson SE feature numerous 7–14 metre models, underlining the commercial focus on this range. In Europe, mid-height agricultural telehandlers dominate farmyards, while in North America, the same height band aligns with common residential and light commercial building heights, reinforcing the position of the 5 – 15 metres segment as the workhorse of the telehandlers market.

Lift Capacity Insights

In Lift Capacity, telehandlers rated in the 3–10 ton band make up the largest segment, with various industry estimates pointing to a share slightly above 50% of global demand. Heavy-duty telehandler market assessments show that 5–10 ton capacity models alone can represent around 35% of heavy-duty unit demand, reflecting the sweet spot for medium-heavy lifting tasks.

Machines in the 3 – 10 ton range are widely used on construction sites for palletized materials, masonry packs, rebar bundles, and prefabricated components, as well as in industrial plants and large farms for handling bulk materials. High-capacity models above 10 tons, such as 20 ton and even 50-ton heavy telehandlers, serve mining, ports, and heavy industry niches, whereas sub-3 ton units are mostly compact machines for tight spaces.space handling. This leaves the 3–10 ton capacity band as the most versatile and therefore the leading segment by share.

Industry Insights

By Industry, construction is the dominant segment, accounting for close to half of global telehandler revenues, with some analyses placing construction’s share at around 48% for core telehandler applications. Construction and infrastructure projects from residential housing and commercial buildings to bridges and industrial facilities demand continuous lifting and placement of materials at varying heights and outreach, where the crane-like reach and forklift-like load handling of telehandlers are highly valued.

Heavy-duty telehandler research further suggests that construction can account for nearly 60% of the heavy-segment demand, with agriculture around 20%, mining around 10%, and logistics and warehousing the remainder. Trade media and OEMs also highlight that telehandlers are now a staple on most large construction sites, particularly in North America and Europe, with rental fleets in these regions collectively fielding tens of thousands of units each year for general construction contractors.

Propulsion Type Insights

Under Propulsion Type, ICE (internal combustion engine, predominantly diesel) telehandlers currently dominate the installed base and new sales. Heavy-duty telehandler analysis indicates that diesel-powered units command roughly 70% of market share, reflecting their suitability for long duty cycles, high torque requirements, and remote or rough-terrain sites where refueling is easier than recharging. In Europe, Stage V requirements have pushed OEMs to adopt sophisticated aftertreatment systems. However, engine-powered telehandlers still account for the overwhelming majority upwards of 80% of units in some regional breakdowns, as contractors continue to favor range and refueling speed on large projects.

Telehandler Type Insights

By telehandler type, large telehandlers remain the leading segment by revenue, while Compact telehandlers are the fastest-growing. One global assessment suggests that compact telehandlers account for about 41% of market revenues, implying that large telehandlers capture just under 60%, reflecting their use on major construction, mining, and industrial projects where high reach and capacity are critical.

Trade data show that North American telehandler rental fleets exceed 90,000 units, with many large-frame machines deployed on infrastructure and industrial sites that require long reach and high capacity. However, industry roundtables and trade publications consistently report that demand growth is strongest in compact telehandlers smaller, more maneuverable machines used on urban and suburban sites driven by compact footprints, lower ownership costs, and the ability to perform both telehandler and light earthmoving tasks. This dynamic leaves Large telehandlers as the current volume and revenue leader, while Compact models carve out high-growth niches in dense urban and specialty applications.

Regional Insights and Trends

Europe Dominates the Global Telehandler Market With Strong Demand

Europe represents the largest and most mature regional market for telescopic handlers, supported by strong demand from both the construction and agricultural sectors. In 2025, telehandler sales in Western Europe reached approximately 32,365 units, following a record year in which regional sales surpassed 35,000 units, highlighting the region’s strong equipment demand cycle. Despite a moderate market correction expected during 2025–2026, annual volumes are projected to remain above 30,000 units, reflecting stable long-term demand for versatile lifting equipment.

The region’s dominance is largely attributed to the balanced contribution of construction and agriculture. Telehandlers are widely used in residential and commercial construction for material lifting, site logistics, and height-access tasks. At the same time, Europe has one of the most advanced agricultural machinery sectors globally, where telehandlers are commonly used for bale stacking, feed handling, and grain logistics on medium and large farms.

Europe also benefits from a strong manufacturing base, particularly in the United Kingdom, Germany, France, and Italy, which collectively account for the majority of regional production and equipment innovation. Additionally, stringent Stage V emission standards for non-road mobile machinery have accelerated the development of cleaner technologies, including electric and hybrid telehandlers.

Germany remains a key demand center due to robust infrastructure investment, while high equipment rental penetration across Europe further supports telehandler adoption across construction, agriculture, and industrial applications.

Asia Pacific Emerging as Fastest-Growing Telehandler Market Amid Infrastructure Investments

Is Asia Pacific the fastest-growing region for telehandlers, supported by rapid urbanization, infrastructure development, and industrialization Regional research indicates that the Asia Pacific telehandler market is growing at CAGRs in the 5–9% range over the medium term, outpacing more mature markets as governments in China, India, Japan, and ASEAN countries invest heavily in roads, metros, airports, industrial corridors, and logistics hubs. China’s overseas infrastructure push via the Belt and Road Initiative has led to cumulative engagements exceeding US$ 1.053 trillion, with about US$ 634 billion in construction contracts, indirectly stimulating demand for lifting equipment both domestically and in partner countries.

In India, the Smart Cities Mission has completed 8,067 projects by mid-2025 across 100 designated smart cities, totaling roughly INR 1.64 lakh crore, highlighting the scale of urban redevelopment and greenfield development that require efficient material-handling solutions. Southeast Asian nations such as Indonesia, Vietnam, and Thailand are also emerging as significant growth pockets, with rising construction and manufacturing activity and growing demand for compact and mid-size telehandlers for dense urban job sites. As sustainability expectations build, the Asia Pacific is also witnessing a gradual interest in hybrid and electric telehandlers, particularly in high-income markets and export-oriented manufacturing hubs, though ICE machines still dominate volumes in the near term.

Competitive Landscape

The global telehandlers market is moderately consolidated at the top, with a cluster of large OEMs including JCB, Manitou Group, JLG (part of Oshkosh), Caterpillar, Bobcat, Wacker Neuson SE, and others producing broad product lines, while numerous regional manufacturers and specialist brands intensify competition in specific capacity ranges and geographies. Trade sources suggest that the top five brands collectively account for a significant but not overwhelming share of global sales, leaving room for niche players and regionally leading players.

Key competitive differentiators include breadth of attachments, dealer and rental networks, total cost of ownership, compliance with evolving emissions standards, and the integration of telematics, automation, and electric drivetrains. Emerging business trends include rental-first models, retrofit electrification projects in partnership with rental companies, and digital platforms that optimize fleet utilization and predictive maintenance.

Key Industry Developments:

- In January 2026, Liebherr Group introduced the T48-8s telescopic handler, offering greater reach, lift height, and versatility. The machine provides a true 8-meter lift height and 4.8-tonne lifting capacity, supported by a 115 kW engine, advanced hydraulics, and an ergonomic operator cab, with production units now available for configuration and order.

- In November 2025, J C Bamford Excavators Ltd. (JCB) expanded its Loadall portfolio with the launch of the 546-70 and 555-70 agricultural telescopic handlers. These 7-meter machines feature enhanced lifting capacity and increased breakout force, improving productivity for agricultural material-handling and farm operations.

- In April 2025, SANY Group announced the addition of a new 7-meter telehandler model to its equipment lineup. The machine integrates modern engineering features that enhance lifting performance, maneuverability, and operational safety, strengthening SANY’s presence in the construction and material-handling equipment segment.

- In April 2025, Faresin Industries Spa unveiled the FS6.26 telehandler at Bauma, positioning it as the most compact and agile machine in its portfolio. The model replaces the FR6.26, which recorded over 2,000 units sold globally, and is designed for construction, rental, and municipal applications.

- In January 2025, Caterpillar Inc. launched its next-generation Cat® telehandler series, including the TH0642, TH0842, TH1055, and TH1255 models. These machines replace the previous TL-series telehandlers and are designed to serve both retail and rental customers with improved efficiency, productivity, and performance.

Companies Covered in Telescopic Handler Market

- J C Bamford Excavators Ltd.

- Bobcat Company

- Manitou Americas, Inc.

- Liebherr Group

- Magni Telescopic Handlers Srl

- Faresin Industries Spa

- Caterpillar Inc.

- Pettibone Traverse Lift, LLC

- JLG Industries, Inc.

- Linamar Corporation

- Terex Corporation

- Xtreme Manufacturing

- Haulotte Group

- Load Lifter Manufacturing Ltd.

- CNH Industrial N.V.

- AB Volvo

- Komatsu Ltd.

- L&T Technology Services Limited

- Oshkosh Corporation

- Wacker Neuson SE

- Other Market Players

Frequently Asked Questions

The Telescopic Handler market is estimated to be valued at US$ 7,010.3 Mn in 2026.

The key demand driver for the Telescopic Handler market is the expansion of global construction and infrastructure activities.

Rapid urbanization, rising residential and commercial construction, and large-scale infrastructure investments are increasing the demand for efficient material-handling equipment.

In 2026, the Europe region will dominate the market with an exceeding 45% revenue share in the global Telescopic Handler market.

3–10 tons lift capacity dominates the product landscape, commanding over 50% of total market revenue in 2026, driven by its wide applicability across construction, agriculture, and industrial material-handling operations. Telehandlers in this capacity range provide an optimal balance between lifting strength, machine stability, and operational flexibility, making them suitable for mid-scale construction sites, farm operations, and warehouse logistics.

Key players operating in the Telescopic Handler market include AB Volvo, Komatsu Ltd., J C Bamford Excavators Ltd., Bobcat Company, Manitou Group, Liebherr Group, Magni Telescopic Handlers Srl, Faresin Industries Spa, and Caterpillar Inc.. These companies compete through product innovation, equipment performance improvements, and expansion of telehandler portfolios across construction, agriculture, and industrial applications.