- Industrial Automation

- Thermal Scanners Market

Thermal Scanners Market Size, Share, and Growth Forecast, 2026 - 2033

Thermal Scanners Market by Product Type (Handheld, Fixed), Wavelength (Short-Wave Infrared (SWIR), Mid-Wave Infrared (MWIR), Long-Wave Infrared (LWIR)), Technology Type (Cooled, Uncooled), End Use Industry (Industrial, Commercial, Aerospace & Defense, Healthcare, Oil & Gas, Automotive, Others) and Regional Analysis for 2026 - 2033

Thermal Scanners Market Size and Trends Analysis

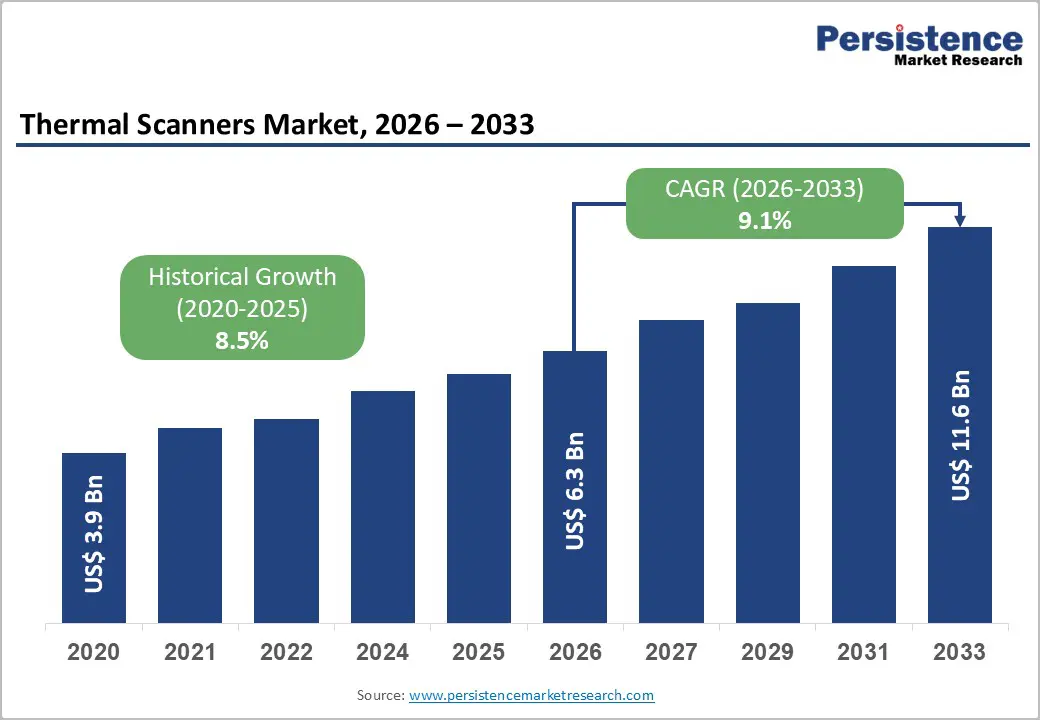

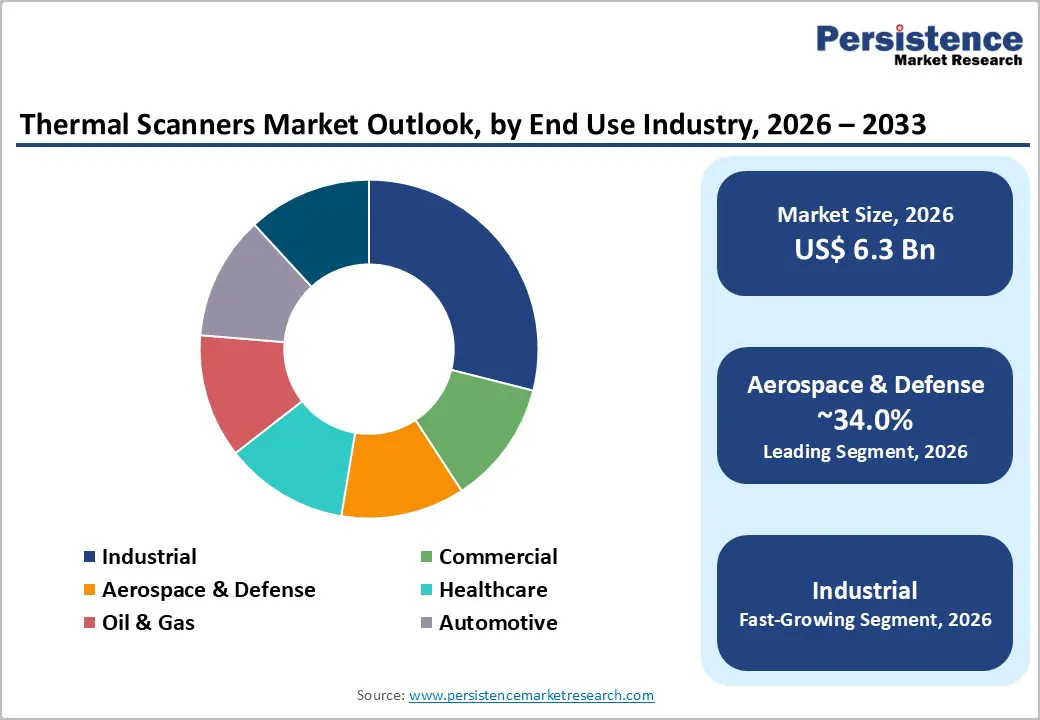

The Global Thermal Scanners Market size was valued at US$ 6.3 billion in 2026 and is projected to reach US$ 11.6 billion by 2033, growing at a CAGR of 9.1% between 2026 and 2033. This expansion reflects accelerating demand from defense modernization initiatives, industrial predictive maintenance adoption, and technological advancements enabling broader commercial applications.

The Thermal Scanners Market benefits substantially from increasing military spending across developed and emerging markets, with U.S. aerospace and defense sector generating over US$ 995 billion in business activity and European A&D contributing €325.7 billion in turnover during 2024.

Key Industry Highlights:

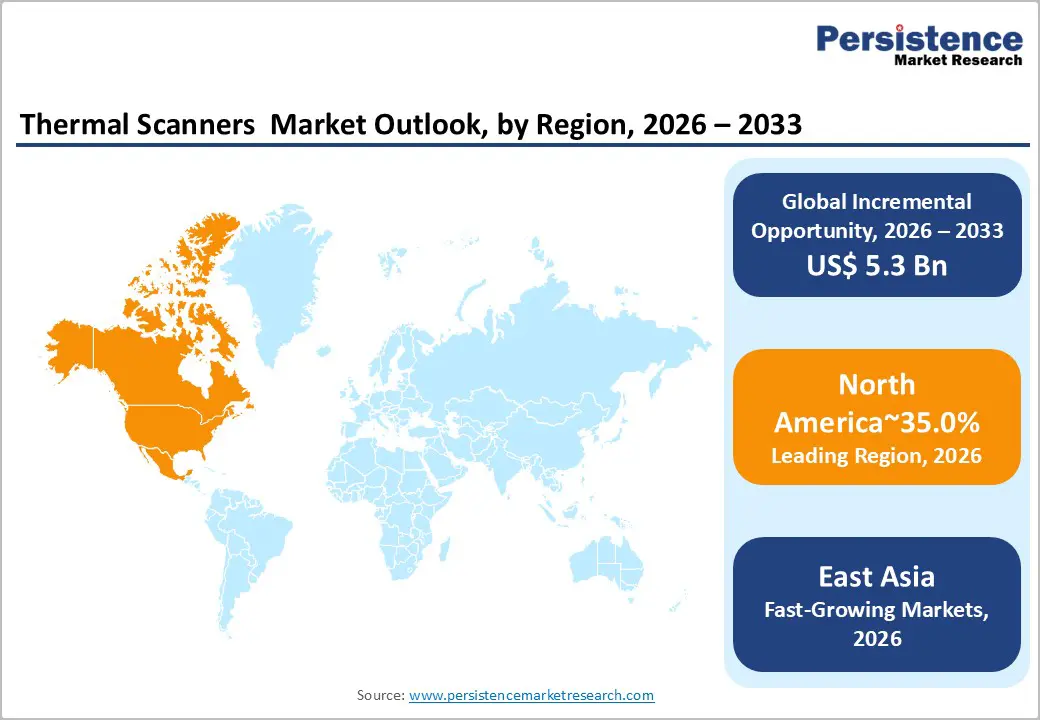

- Regional Leadership: North America leads the global Thermal Scanners market with 35% share, driven by sustained defense spending, advanced manufacturing adoption, and strong presence of leading thermal imaging manufacturer.

- Fastest-Growing Region: East Asia holds 22% market share and represents the fastest-growing region, supported by rapid industrialization, defense modernization, and cost-efficient thermal scanner manufacturing in China, Japan, and Southeast Asia.

- Strong European Presence: Europe accounts for 28% of the market, underpinned by robust aerospace & defense activity, stringent industrial safety norms, and strong demand for building energy efficiency assessments.

- Leading End-Use Segment: Aerospace & Defense dominates with 34% share, fueled by military modernization programs, large government procurement contracts, and demand for all-weather surveillance and targeting systems.

- Leading Product Type: Handheld thermal scanners command 58% market share, reflecting their flexibility, cost-effectiveness, and widespread use in industrial maintenance, electrical inspections, and building diagnostics.

| Key Insights | Details |

|---|---|

|

Thermal Scanners Market Size (2026E) |

US$ 6.3 Bn |

|

Market Value Forecast (2033F) |

US$ 11.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.5% |

Market Dynamics

Growth Drivers

Defense Modernization and Military Technology Advancement

Global defense spending has reached unprecedented levels, with geopolitical tensions and security concerns driving substantial investments in advanced surveillance and targeting capabilities. The U.S. aerospace and defense industry alone generated $995 billion in total business activity in 2024, with military-focused thermal imaging technologies representing critical modernization priorities.

The European aerospace and defense sector demonstrated particularly robust performance, with defense spending expanding 13.8% year-on-year, totaling €325.7 billion in 2024 turnover and supporting direct employment of 1,103,000 professionals. Military thermal imaging cameras enable all-weather surveillance, target acquisition, and situational awareness capabilities that conventional visible-spectrum systems cannot achieve, making them essential components of modern defense platforms including unmanned aerial vehicles, armored vehicles, and weapon-mounted systems.

The Thermal Scanners Market experiences direct benefits from military modernization programs globally. The military thermal camera segments demand driven by requirements for enhanced detection capabilities, integration with command-and-control systems, and AI-enabled target recognition.

THEON International signed a multi-year framework agreement with the German Bundeswehr in November 2025 for up to 25,000 thermal weapon-mounted clip-on sights valued at over €100 million, representing the largest EU procurement of such systems and underscoring strategic military priorities. These substantial government contracts establish sustained demand for thermal scanning capabilities across military applications

Industrial Predictive Maintenance and Condition-Based Equipment Monitoring

Industrial organizations are systematically transitioning from reactive maintenance models requiring equipment failure before intervention to proactive, condition-based maintenance strategies enabled by thermal imaging technologies. Manufacturing facilities deploying thermal scanning systems achieve maintenance cost reductions of 30-40% through early equipment failure detection, with some implementations eliminating unplanned downtime entirely through planned maintenance scheduling based on thermal condition monitoring.

The Market addresses critical industrial requirements including detection of temperature anomalies as small as 0.03°C that indicate developing equipment problems, enabling maintenance interventions weeks or months before conventional inspection methods would identify issues.

Organizations implementing comprehensive thermal imaging solutions report production downtime reduction of 35-45% through early problem detection combined with planned maintenance scheduling during predetermined shutdown windows. Industrial thermal imaging applications encompass electrical equipment monitoring, rotating machinery assessment, process furnaces, and hydraulic systems encompassing the vast majority of critical manufacturing equipment.

Advanced analytics capabilities enable trend analysis identifying gradual temperature changes that precede catastrophic failures, translating to equipment lifespan extension of 20-40% while extending operational reliability. The Market's strongest growth trajectory among industrial applications reflects economic attractiveness of predictive maintenance compared to alternative approaches, with facilities reporting elimination of up to 75% of breakdowns through comprehensive condition monitoring programs.

Market Restraining Factors

High Capital Equipment Costs and Procurement Barriers

Thermal scanning systems continue to command premium pricing despite advancing sensor technology and increasing manufacturing scale, with high equipment costs representing a significant barrier to adoption, particularly for small and medium-sized enterprises and emerging market applications. Advanced thermal cameras capable of detecting subtle temperature variations across large areas require sophisticated optics, specialized detectors, and signal processing electronics that collectively drive equipment costs substantially above commodity-priced surveillance or monitoring alternatives.

Organizations evaluating thermal imaging deployment must justify capital investments against alternative approaches, creating procurement barriers that slow adoption among price-sensitive customer segments. Additionally, specialized training requirements for accurate thermal image interpretation and proper system deployment add implementation costs beyond hardware acquisition.

Key Market Opportunities

Healthcare Diagnostics and Non-Invasive Medical Assessment Applications

The healthcare sector represents an emerging and rapidly expanding opportunity for Thermal Scanners Market technologies, driven by proven applications in non-invasive diagnostics and disease detection. COVID-19 pandemic experiences demonstrated thermal imaging capabilities for fever screening, with deployed systems achieving 90% accuracy rates in identifying elevated body temperatures across large populations at transportation hubs and healthcare facilities. Beyond pandemic response applications, medical professionals increasingly adopt thermal imaging for vascular assessment, inflammation detection, breast cancer screening, and musculoskeletal disorder diagnosis, where thermal patterns correlate with underlying pathophysiology.

Advanced thermal imaging capabilities enable early detection of circulatory problems, infection sites, and inflammatory conditions without requiring contrast agents or invasive procedures, creating value propositions particularly attractive to healthcare systems prioritizing non-invasive diagnostic approaches. The healthcare thermal imaging segment is positioned for significant expansion as evidence accumulates regarding diagnostic accuracy and clinical utility across expanding medical specialties.

Integration of AI-enabled thermal data analysis enhances diagnostic precision while reducing interpretation skill requirements, accelerating adoption across healthcare facilities worldwide. The Thermal Scanners Market opportunities in healthcare encompass both large facility-based applications (centralized screening systems) and mobile/portable platforms enabling distributed assessments across diverse clinical settings.

Building Energy Efficiency and Sustainable Infrastructure Initiatives

Government-mandated sustainability initiatives and building energy efficiency standards create substantial demand for thermal imaging solutions enabling identification of heat losses, insulation deficiencies, and inefficient envelope construction. Building diagnostics applications leverage thermal imaging to identify thermal bridges, air leakage paths, and defective insulation that compromise heating and cooling system efficiency and increase operational costs. European authorities emphasize building energy efficiency through regulatory frameworks and incentive programs, creating systematic demand for thermal survey services that identify optimization opportunities.

The Market expands as municipalities, property managers, and sustainability-focused organizations invest in comprehensive building energy assessments preceding renovation and modernization initiatives. Large-scale commercial facilities, district heating systems, and public infrastructure benefit particularly from thermal imaging analysis that quantifies energy waste and justifies capital investments in efficiency improvements.

Climate change mitigation policies supporting transition toward sustainable built environments create policy-driven demand for thermal assessment tools, while building energy codes increasingly reference thermal imaging standards for compliance verification. This opportunity encompasses both equipment sales to specialized thermography service providers and development of integrated software solutions analyzing thermal datasets to optimize building performance.

Category-wise Analysis

Product Type Insights

Handheld thermal scanners maintained 58% market share in 2026, reflecting their position as the primary form factor for field-based thermal inspections, maintenance operations, and portable diagnostic applications

Handheld devices provide flexibility for technicians to conduct on-demand inspections of distributed equipment across manufacturing facilities, electrical installations, and building envelopes without requiring installation of fixed monitoring infrastructure. The widespread adoption of handheld thermal cameras across industrial maintenance programs reflects their cost-effectiveness compared to fixed systems, ease of deployment without integration requirements, and ability to support diverse inspection routes across facility equipment.

Recent innovations in handheld thermal imaging expand addressable applications and market penetration. Fluke Corporation's September 2024 launch of the iSee Mobile Thermal Camera demonstrates smartphone-compatible form factors that leverage consumer smartphone platforms as display and processing systems, dramatically reducing standalone equipment costs while enabling broader adoption among commercial users and building professionals.

Handheld device refinement emphasizes ergonomics, user interface intuitiveness, and software capabilities that reduce interpretation expertise requirements, enabling technicians with standard maintenance backgrounds to conduct effective thermal inspections without specialized training. Market leadership in handheld products reflects their versatility across diverse applications including electrical system diagnostics, HVAC equipment maintenance, mechanical equipment assessment, and building thermal surveys.

End Use Industry Insights

The Aerospace & Defense industry maintained approximately 34% of the Thermal Scanners Market in 2026, establishing its position as the dominant end-user segment driven by military modernization priorities and stringent aircraft safety and quality control requirements.

Defense organizations worldwide are prioritizing advanced surveillance and targeting capabilities that thermal imaging technologies provide, with military applications encompassing handheld thermal sights for soldier-level threat detection, vehicle-mounted systems for armored vehicle situational awareness, airborne platforms for reconnaissance and target acquisition, and naval vessel surveillance systems. Government procurement contracts represent highly predictable, multi-year demand with substantial contract values supporting sustained manufacturer investments in technology advancement and production capacity.

The robust aerospace and defense market fundamentals reflect significant investment commitments. The U.S. aerospace and defense sector generated $443 billion in economic value contribution during 2024, representing 1.5% of national GDP, with thermal imaging technologies representing strategic capabilities supporting national security and military effectiveness.

European A&D sector demonstrated particularly strong performance with €325.7 billion in total turnover during 2024, supporting 1,103,000 direct employees and 4.2 million ecosystem jobs across supplier and service industries. THEON International's €100+ million multi-year contract with the German Bundeswehr for 25,000 thermal weapon-mounted clip-on sights exemplifies substantial military procurement commitments driving sustained Thermal Scanners Market demand.

Regional Insights and Trends

North America Market Trend

North America maintained approximately 35% of the Global Thermal Scanners Market share, establishing the region as the dominant market driven by sustained defense spending, advanced manufacturing base, and technological innovation concentration. The United States alone generated over $995 billion in aerospace and defense business activity during 2024, with military thermal imaging technologies representing strategic priorities for defense modernization and force enhancement.

U.S. military spending for thermal imaging systems and platforms remains among the highest globally, with government procurement contracts providing sustained demand supporting multiple domestic manufacturers and ensuring continued technology advancement investment.

North American industrial sectors demonstrate advanced adoption of predictive maintenance technologies, with manufacturing organizations prioritizing equipment reliability and production continuity through systematic deployment of thermal monitoring systems across critical assets.

The region benefits from presence of major thermal imaging manufacturers including Teledyne FLIR, Fluke Corporation, and LumaSense Technologies, which drive innovation through substantial research and development investment and maintain competitive advantage through technology leadership. Commercial applications in building energy efficiency assessment, HVAC system diagnostics, and electrical infrastructure maintenance demonstrate broad thermal imaging adoption across diverse customer segments. Regulatory standards including ASHRAE energy efficiency requirements and NFPA electrical safety codes mandate or strongly encourage thermal inspection methodologies for compliance verification, creating systematic demand for thermal scanning services and equipment among commercial and industrial customers.

East Asia Market Trend

East Asia accounted for approximately 22% of the Global Thermal Scanners Market share while demonstrating the fastest regional growth trajectory, driven by rapid industrialization, defense modernization programs, and cost-conscious manufacturing sector adoption. China dominates the region's thermal imaging manufacturing capacity, with substantial production of uncooled microbolometer-based systems at cost structures significantly below Western manufacturers, enabling competitive pricing that accelerates adoption across price-sensitive industrial customers and emerging market applications.

Chinese military modernization priorities emphasize advanced surveillance and targeting capabilities that thermal imaging technologies provide, with government defense spending supporting substantial domestic research institutions and commercial manufacturers.

Japanese manufacturers emphasize precision and quality characteristics aligned with automotive and electronics manufacturing requirements for non-destructive thermal inspection and quality assurance. Southeast Asian electronics manufacturing expansion creates demand for thermal monitoring in precision manufacturing processes and semiconductor inspection applications. The region's cost sensitivity drives innovation in affordable thermal solutions, enabling broader adoption among small and medium-sized enterprises while challenging Western suppliers' premium pricing models.

Europe Market Trend

Europe represented approximately 28% of the Thermal Scanners Market, characterized by stringent industrial safety standards, substantial aerospace and defense sector participation, and emphasis on building energy efficiency. European A&D sector generated €325.7 billion in turnover during 2024, with demand for thermal imaging technologies spanning civil aviation maintenance, defense platform development, and military modernization initiatives across European NATO members

Germany represents the regional leader for thermal imaging innovation and manufacturing, with companies including InfraTec GmbH hosting advanced applications conferences highlighting evolving thermography technologies and supporting growing demand for thermal scanning services in research and industrial applications.

European regulatory frameworks emphasizing building energy efficiency and sustainability create systematic demand for thermal survey services identifying heat losses and insulation deficiencies in commercial and residential properties.

Competitive Landscape

The Global Thermal Scanners Market is moderately consolidated to oligopolistic, with a few large players dominating the high-end and industrial segments. Leading companies like 3M, L3Harris Technologies, Teledyne FLIR LLC, AMETEK Land, Leonardo S.p.A., and Fluke Corporation have significant market influence due to their strong R&D capabilities, global distribution networks, and established brand reputation. These firms focus on advanced thermal imaging, defense, industrial, and healthcare applications, giving them a competitive edge.

Mid-tier players such as Opgal Optronic Industries and OMEGA Engineering compete through niche solutions and customization, keeping the market dynamic. The overall competition is shaped by technological innovation, integration with AI/IoT, and regional presence. While top players drive standards and pricing, smaller specialized companies ensure the market is not entirely concentrated. This balance makes the market highly competitive yet strategically controlled by the leading firms.

Key Industry Developments

- 3 September 2025, InfraTec GmbH (Germany): InfraTec hosted its cost-free online user conference “Thermography Compact – Enter the World of Infrared Technology”, focusing on advanced thermography applications for research, development, and industrial automation. The event highlighted evolving thermal camera technologies, software-based evaluation capabilities, and real-world measurement use cases, supporting growing demand for thermal scanning services in quality assurance and R&D.

- 26 November 2025, Theon International Plc (THEON): THEON signed a multi-year framework agreement with the German Bundeswehr for up to 25,000 thermal weapon-mounted clip-on sights, valued at over €100 million, marking the largest procurement of such thermal imaging systems in the EU. The contract strengthens THEON’s position in digital and thermal imaging technologies, supporting long-term service, integration, and lifecycle support demand for military-grade thermal scanning solutions in Europe.

Companies Covered in Thermal Scanners Market

- 3M

- AMETEK Land (Land Instruments International Ltd)

- Fluke Corporation

- HGH

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- Nippon Avionics Co. Ltd.

- OMEGA Engineering Inc.

- Opgal Optronic Industries Ltd.

- Optotherm, Inc.

- Teledyne FLIR LLC

- Tonbo Imaging

Frequently Asked Questions

The global Thermal Scanners Market is projected to be valued at US$ 6.3 Bn in 2026.

Aerospace & Defense Segment is expected to account for approximately 34.0% of the global Thermal Scanners Market by End Use Industry in 2026.

The market is expected to witness a CAGR of 9.1% from 2026 to 2033.

The Thermal Scanners Market growth is driven by rising defense modernization and military procurement of advanced thermal imaging systems, along with increasing industrial adoption of predictive maintenance and condition-based monitoring to reduce downtime, costs, and equipment failures.

Key opportunities in the Thermal Scanners Market arise from expanding healthcare adoption for non-invasive diagnostics and AI-enabled medical imaging, along with growing demand for building energy efficiency and sustainability assessments driven by regulatory and climate policies.

The key players in the Thermal Scanners Market include 3M, L3Harris Technologies, Teledyne FLIR LLC, AMETEK Land, Leonardo S.p.A., and Fluke Corporation.