- Display Technologies

- Stretchable Electronics Market

Stretchable Electronics Market Size, Share, and Growth Forecast 2026 - 2033

Stretchable Electronics Market by Product Type (Stretchable Sensors, Stretchable Displays, Stretchable Batteries, Stretchable Circuits, Stretchable Conductors & Interconnects, Stretchable Photovoltaics, Stretchable Transistors & Logic Devices), Component, Material Type, Technology, End-user, and Regional Analysis, 2026 - 2033

Stretchable Electronics Market Size and Trend Analysis

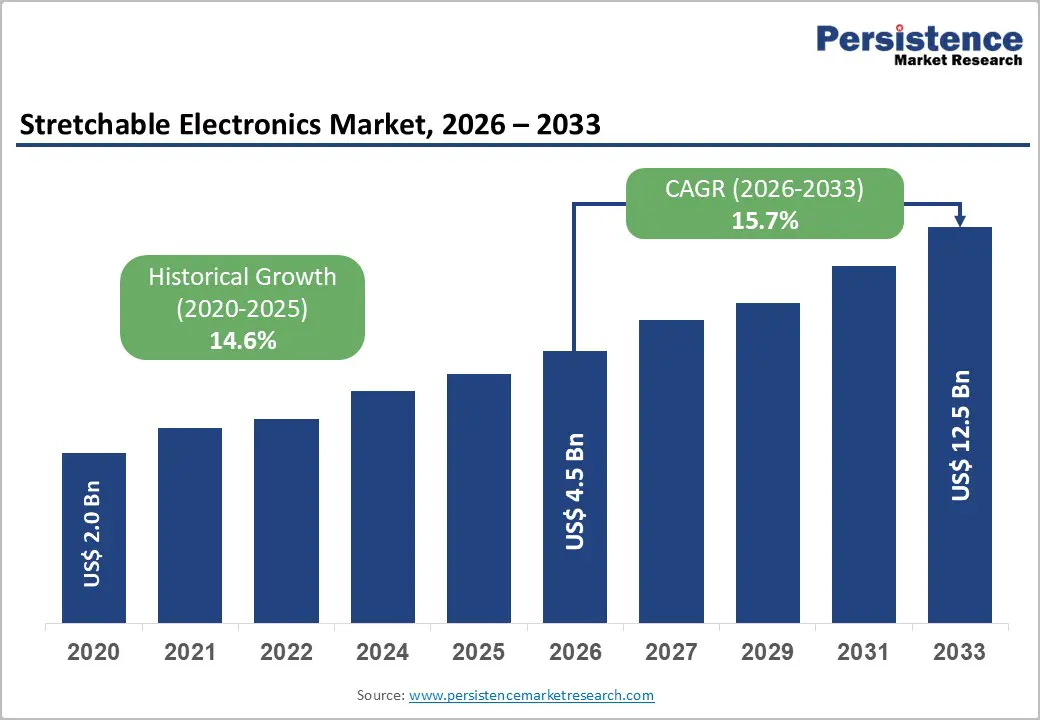

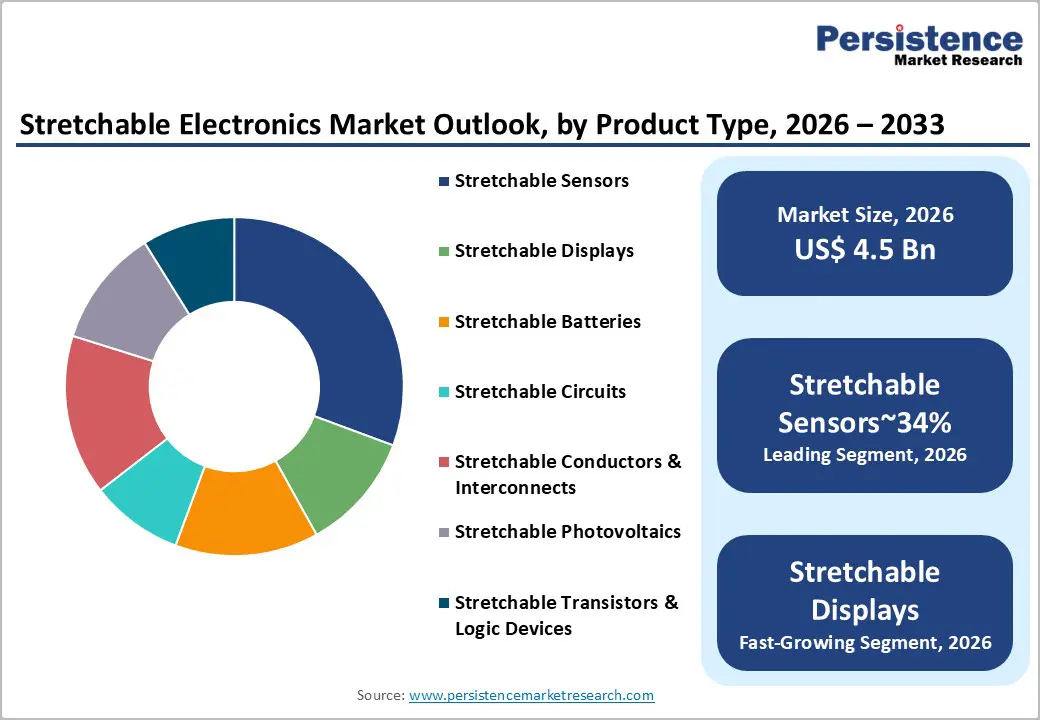

The global stretchable electronics market size is likely to be valued at US$ 4.5 billion in 2026 and is expected to reach US$ 12.5 billion by 2033, growing at a CAGR of 15.7% during the forecast period from 2026 to 2033.

The market is propelled by surging demand for body-conforming electronic devices across healthcare, consumer electronics, and wearable technology sectors. Convergence of advanced nanomaterial science with flexible substrate engineering has unlocked unprecedented device geometries that were previously unattainable using rigid electronics.

Key Market Highlights

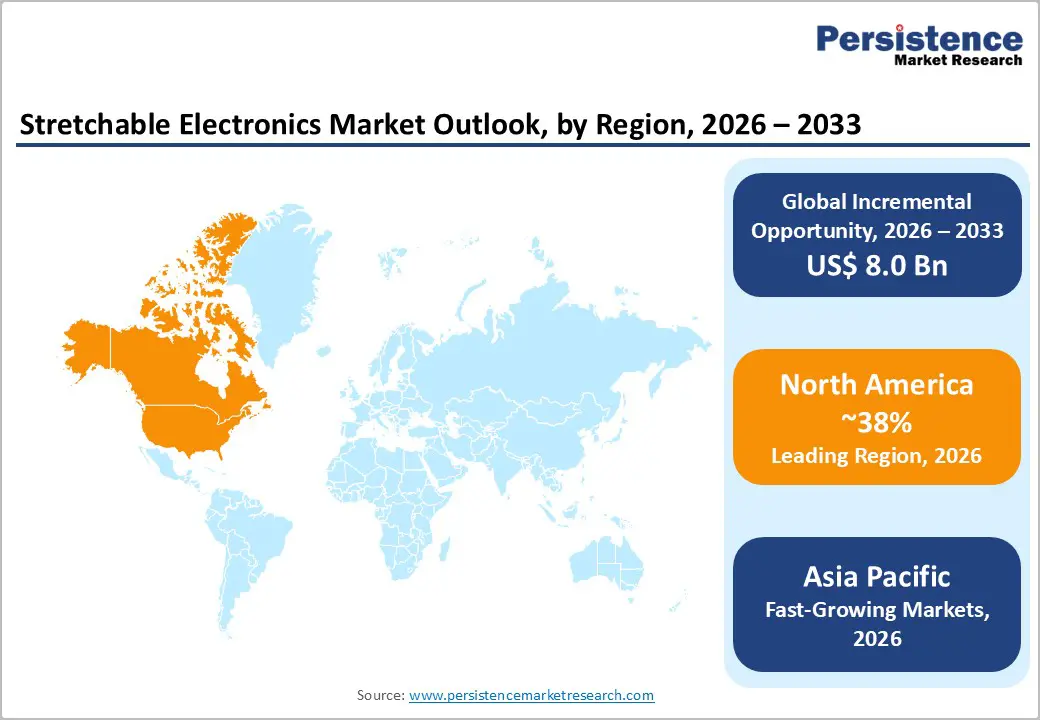

- Leading Region: North America dominates the global stretchable electronics market accounting for 38% share, driven by extensive NIH and DARPA-funded R&D programs, a vibrant deep-tech startup ecosystem, FDA digital health regulatory pathways, and strong commercial adoption across medical wearables and defense electronics sectors.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a rising CAGR of 19.9%, propelled by China's 14th Five-Year Plan investments in flexible electronics, South Korean display innovation from Samsung and LG, Japan's advanced material supply chain, and India's PLI scheme attracting electronics manufacturing investment.

- Dominant Product: Stretchable sensors lead the product type category with approximately 32% market share, driven by broad adoption in healthcare wearables, industrial robotics, and human-machine interface applications requiring skin-conformable, high-sensitivity electromechanical transduction.

- Fastest Growing Product: Stretchable displays are the fastest growing product type segment, fueled by global consumer electronics OEM investment in foldable and rollable device form factors, with patent filings in stretchable display architectures growing at over 20% annually per EPO data.

- Key Opportunity: Implantable and epidermal medical electronics represent the highest-value growth frontier, supported by over US$ 200 million in NIH funding, expanding FDA regulatory pathways, and a global implantable medical device market projected to exceed US$ 100 billion by 2028.

Market Dynamics Analysis

Drivers - Accelerating Demand for Wearable Health Monitoring Devices

The rapid adoption of continuous health monitoring wearables is a foundational driver for stretchable electronics. According to the World Health Organization (WHO), non-communicable diseases (NCDs) account for 74% of global deaths annually, amplifying the clinical value of continuous vital sign monitoring. Stretchable biosensors that conform to skin topography enable real-time, artifact-free electrophysiological measurements of ECG, EMG, and EEG signals, surpassing the performance of rigid electrode counterparts.

The U.S. Food and Drug Administration (FDA) has progressively expanded its digital health regulatory pathways under the De Novo and 510(k) frameworks, lowering barriers to clinical-grade stretchable sensor commercialization. With telehealth adoption permanently elevated post-pandemic and aging populations globally requiring chronic disease management tools, stretchable electronics are positioned to disrupt traditional medical device paradigms.

Rising Integration of Stretchable Electronics in Next-Generation Consumer Devices

Consumer electronics manufacturers are increasingly embedding stretchable components to achieve novel form factors, foldable, rollable, and skin-adherable devices, that rigid circuit boards cannot support. Samsung Electronics Co., Ltd. and LG Display Co., Ltd. have invested substantially in stretchable OLED display technologies, with patent filings in stretchable display architectures growing at over 20% annually according to the European Patent Office (EPO).

The global augmented reality (AR) and virtual reality (VR) device market, a key downstream consumer of stretchable electronics, is forecast by the Consumer Electronics Association (CTA) to sustain double-digit growth through 2030. As device manufacturers compete on ergonomics, miniaturization, and user comfort, the strategic importance of stretchable substrates, conductors, and sensors within product design roadmaps continues to intensify.

Restraints - Complex and High-Cost Manufacturing Processes

The fabrication of stretchable electronics requires specialized deposition, printing, and patterning techniques, including transfer printing, nanoimprinting, and aerosol-jet printing, that involve significantly higher capital equipment costs and lower throughput compared to conventional semiconductor manufacturing.

The absence of mature, industry-wide fabrication standards amplifies process variability and increases unit costs, particularly for low-to-medium volume production runs. These cost dynamics limit adoption to premium-priced application segments, constraining market penetration in cost-sensitive verticals such as consumer packaging and mass-market sporting goods, where price parity with conventional electronics is essential for commercial viability.

Durability, Reliability, and Standardization Challenges

Long-term electromechanical reliability of stretchable electronic systems under repeated mechanical strain cycles remains a critical technical challenge. Studies published in Advanced Materials and Nature Electronics journals have documented resistance drift and delamination of conductive traces after 10,000-50,000 stretch cycles, which is insufficient for multi-year consumer wearable lifecycles.

The lack of harmonized international standards for stretchable device testing and qualification, unlike the well-established IPC and JEDEC standards governing rigid PCBs, complicates procurement decisions for enterprise customers and regulatory clearance for medical-grade applications.

Opportunities - Stretchable Electronics for Implantable and Epidermal Medical Devices

Implantable and epidermal medical devices represent one of the most transformative commercial frontiers for stretchable electronics. The U.S. National Institutes of Health (NIH) has funded over US$ 200 million in flexible and stretchable bioelectronics research over the past five years, recognizing their potential to revolutionize brain-computer interfaces, cardiac monitoring patches, and wound-healing electronics.

Research from institutions including MIT and Stanford University has demonstrated biocompatible stretchable neural probes that maintain signal fidelity in vivo with minimal immune response. As the global implantable medical device sector is projected to exceed US$ 100 billion by 2028, stretchable electronics manufacturers developing biocompatible, FDA-cleared platforms stand to capture significant long-term value in this high-margin clinical segment.

Automotive and Aerospace Integration for Structural Health Monitoring

The automotive and aerospace industries present an emerging, high-value growth opportunity for stretchable electronics, particularly for conformable structural health monitoring (SHM) sensor networks. The Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) are progressively mandating advanced sensor-based continuous airframe monitoring systems to reduce maintenance costs and improve safety outcomes.

Stretchable piezoelectric and piezoresistive sensor arrays can be laminated directly onto complex curved fuselage and wing surfaces, eliminating heavy rigid sensor housings. Electric vehicle (EV) manufacturers are similarly exploring stretchable battery management and thermal sensing films integrated directly onto cell surfaces. Volkswagen AG and Airbus SE have both publicly disclosed pilot programs involving conformable sensing electronics, signaling an accelerating adoption trajectory that represents a compelling commercial opportunity for stretchable electronics solution providers.

Category-wise Analysis

Product Type Insights

Stretchable sensors dominate the product type segment, commanding approximately 32% of total market revenues. This leadership reflects the segment's broad applicability across healthcare wearables, industrial robotics, human-machine interfaces, and environmental monitoring, enabling conformable strain, pressure, temperature, and electrophysiological measurement.

Research published in ACS Nano and Science Advances has demonstrated skin-integrated stretchable sensor arrays achieving gauge factors exceeding 1,000 with biaxial stretchability above 30%. The proliferation of remote patient monitoring programs globally and increasing investment by consumer electronics OEMs in ergonomic health tracking devices continues to sustain robust procurement of stretchable sensor technologies, cementing the segment's top position in the product type hierarchy.

Component Insights

Conductive materials represent the leading component segment, accounting for approximately 29% of the component-level market. As the functional backbone of every stretchable electronic device, conductive materials, including silver nanowire (AgNW) networks, carbon nanotube (CNT) composites, conductive hydrogels, and liquid metal alloys such as EGaIn, determine device performance, stretchability limits, and electrical efficiency.

The Royal Society of Chemistry has published extensive reviews on AgNW percolation networks achieving sheet resistances below 10 Ω/sq at >100% strain. Continuous innovation from materials suppliers including 3M Company and Heraeus Holding GmbH in printable and screen-depositable conductive formulations is driving down costs and improving processability at scale.

Material Type Insights

Elastomers lead the material type segment with an estimated 36% share of total material consumption in stretchable electronics. Silicone-based elastomers, particularly polydimethylsiloxane (PDMS) and Ecoflex, serve as the universal substrate and encapsulant material of choice due to their exceptional mechanical compliance (Young's modulus of 0.1-3 MPa), optical transparency, biocompatibility, and well-understood surface chemistry enabling strong bonding to functional layers.

Thermoplastic elastomers (TPEs) and polyurethane-based elastomers are gaining traction as processing-friendly alternatives for roll-to-roll (R2R) manufacturing. DuPont de Nemours, Inc. and Toyobo Co., Ltd. are among the principal commercial suppliers of specialty elastomeric substrates engineered for stretchable electronics fabrication.

Technology Insights

Printed electronics technology leads the technology segment with approximately 38% revenue share, driven by its compatibility with large-area, roll-to-roll (R2R) manufacturing at relatively low capital cost. Inkjet, screen, and gravure printing of functional inks onto stretchable substrates enables scalable fabrication of sensors, interconnects, and energy harvesters without the vacuum deposition equipment required by thin-film alternatives.

The OE-A (Organic and Printed Electronics Association) estimates the printed electronics sector will maintain double-digit compound annual growth, supported by expanding printable conductive and semiconducting ink portfolios from companies such as DuPont de Nemours, Inc. and Heraeus Holding GmbH. The technology's natural alignment with high-volume, low-cost manufacturing requirements makes it the preferred fabrication route for consumer and healthcare segment applications.

End-User Insights

Healthcare & medical devices are the dominant end-use segment, contributing approximately 34% of total market revenues. The segment's primacy stems from clinical demand for skin-conformable, motion-artifact-resistant biosensors for continuous patient monitoring, wound care electronics, and rehabilitation devices. The U.S. Centers for Disease Control and Prevention (CDC) notes that over 60% of American adults have at least one chronic condition requiring ongoing health monitoring, underscoring the scale of addressable demand.

Favorable regulatory pathways for Software as a Medical Device (SaMD) and wearable biosensor platforms under FDA 21 CFR Part 820 are enabling faster product commercialization, reinforcing healthcare's dominant positioning in stretchable electronics end-use consumption.

Regional Insights

North America Stretchable Electronics Market Trends

North America dominates the stretchable electronics market, accounting for an estimated 38% global share in 2026, driven by strong R&D funding, advanced healthcare infrastructure, and early commercialization of wearable biosensors. Robust defense and medical applications, coupled with venture capital activity and regulatory support, continue to accelerate innovation and market expansion across the region.

- U.S. Stretchable Electronics Market Size

The U.S. leads the regional market with an estimated valuation of USD 2.1 billion in 2026, supported by significant investments from federal agencies and private stakeholders. The country’s leadership in wearable healthcare devices, defense-grade electronics, and startup commercialization pipelines sustains its dominant position and high double-digit growth trajectory.

- Europe Stretchable Electronics Market Trends

Europe holds approximately 25% of the global market share in 2026, driven by strong academic-industry collaboration, sustainability-focused regulations, and EU-funded R&D initiatives. Emphasis on eco-friendly materials, smart textiles, and flexible hybrid electronics is shaping innovation, while harmonized regulatory frameworks enhance product standardization and commercialization efficiency.

- Germany Stretchable Electronics Market Size

Germany leads Europe with an estimated market size of USD 550 million in 2026, supported by advanced manufacturing capabilities and strong research institutions. The country’s focus on industrial electronics, automotive integration, and high-performance materials drives consistent demand and technological leadership within the region.

- U.K. Stretchable Electronics Market Size

The U.K. market is projected at USD 250 million in 2026, fueled by innovation in organic electronics and flexible display technologies. Strong startup ecosystems and university-led research contribute to advancements in wearable and conformable electronic solutions, particularly in healthcare and consumer electronics segments.

- France Stretchable Electronics Market Size

France is expected to reach USD 280 million in 2026, supported by government-backed R&D programs and semiconductor innovation hubs. The country’s focus on next-generation electronics, including stretchable silicon architectures, positions it as a key contributor to Europe’s technological advancements in this field.

- Asia Pacific Stretchable Electronics Market Trends

Asia Pacific is the fastest-growing region, projected to capture 35% market share by 2026, driven by large-scale manufacturing, strong semiconductor ecosystems, and government-backed initiatives. Rapid adoption in consumer electronics, displays, and smart wearables, combined with cost-efficient production capabilities, positions the region as a global manufacturing and innovation hub.

- China Stretchable Electronics Market Size

China dominates the region with an estimated USD 1.5 billion market size in 2026, supported by state-led investments and expanding domestic electronics manufacturing. Strong focus on self-sufficiency in semiconductors and flexible electronics continues to drive rapid market growth and innovation.

- India Stretchable Electronics Market Size

India’s market is emerging, estimated at USD 220 million in 2026, driven by government initiatives like PLI schemes and growing electronics manufacturing capabilities. Increasing adoption in healthcare wearables and rising investments in flexible electronics production are expected to accelerate long-term growth.

- Japan Stretchable Electronics Market Size

Japan is projected to reach USD 450 million in 2026, leveraging its expertise in advanced materials and precision manufacturing. Strong presence in specialty polymers, conductive inks, and high-quality electronic components supports its role as a key supplier within the global stretchable electronics value chain.

Competitive Landscape

The global stretchable electronics market is characterized by a highly fragmented structure, encompassing multinational conglomerates, specialized material suppliers, deep-tech startups, and university spin-outs operating across different parts of the value chain. Market leaders such as Samsung Electronics Co., Ltd., DuPont de Nemours, Inc., and 3M Company leverage their scale, vertically integrated material supply chains, and extensive IP portfolios as key differentiators.

Emerging business models center on platform licensing, material-as-a-service (MaaS), and co-development partnerships with medical device OEMs and consumer electronics brands. R&D intensity remains high, with leading players allocating 8-15% of revenues to innovation pipelines targeting next-generation biocompatible substrates and ultra-stretchable conductor formulations.

Key Developments:

- February 2025: Samsung Electronics Co., Ltd. unveiled a prototype stretchable micro-LED display at the Consumer Electronics Show (CES) 2025, achieving 30% biaxial stretchability while maintaining full-color display performance, targeting next-generation wearable and foldable device form factors.

- September 2024: StretchSense Ltd. secured a strategic investment partnership with a leading athletic apparel manufacturer to mass-produce stretchable capacitive sensor-embedded sportswear for elite athlete performance analytics, with initial deployment targeting professional sports leagues.

- April 2024: Rogers Corporation launched its next-generation PORON XRD Extreme Impact Protection stretchable foam material platform, specifically engineered for integration into wearable electronics enclosures requiring simultaneous mechanical shock absorption and substrate conformability in medical and industrial applications.

Stretchable Electronics Market- Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 2.0 Bn |

| Current Market Value (2026) | US$ 4.5 Bn |

| Projected Market Value (2033) | US$ 12.5 Bn |

| CAGR (2026 - 2033) | 15.7% |

| Leading Region | North America, 38% share |

| Dominant Product Type | Stretchable Sensors, 32% share |

| Top-ranking End User | Healthcare & Medical Devices, 34% |

| Incremental Opportunity | US$ 8.0 Bn |

Companies Covered in Stretchable Electronics Market

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- DuPont de Nemours, Inc.

- 3M Company

- Panasonic Corporation

- Rogers Corporation

- StretchSense Ltd.

- MC10, Inc.

- FlexEnable Ltd.

- Royole Corporation

- Enfucell Flexible Electronics Co., Ltd.

- Pragmatic Semiconductor Ltd.

- Toyobo Co., Ltd.

- Heraeus Holding GmbH

- Imprint Energy, Inc.

- Bando Chemical Industries, Ltd.

- ISORG

- Brewer Science, Inc.

- PragmatIC Semiconductor Ltd.

- Liqtech International A/S

Frequently Asked Questions

The global Stretchable Electronics market is projected to reach US$ 12.5 Billion by 2033, up from US$ 4.5 Billion in 2026, expanding at a CAGR of 15.7% over the forecast period 2026-2033, underpinned by escalating healthcare digitalization, consumer wearable proliferation, and continuous advancement in stretchable material science and fabrication technologies.

Primary demand drivers include the global surge in wearable health monitoring devices, supported by WHO data showing NCDs account for 74% of global deaths, necessitating continuous monitoring, and intensifying consumer electronics OEM investment in stretchable display and sensor technologies for ergonomic, body-conformable next-generation device form factors.

Stretchable Sensors lead the product type segment with approximately 32% revenue share. Their dominance is driven by extensive deployment in clinical wearables, industrial robotics, and human-machine interfaces. Research in ACS Nano and Science Advances confirms their superior electromechanical performance with gauge factors exceeding 1,000 and biaxial stretchability above 30%.

North America is the dominant regional market, anchored by the United States' world-leading R&D investment through NSF, NIH, and DARPA programs, a mature venture capital ecosystem for deep-tech commercialization, FDA digital health regulatory frameworks enabling medical-grade device clearance, and strong end-user adoption across healthcare, defense, and consumer electronics sectors.

The foremost opportunity lies in implantable and epidermal medical devices, with the NIH committing over US$ 200 million to bioelectronics research and FDA pathways accelerating clearance. Automotive and aerospace structural health monitoring using conformable sensor arrays represents a secondary high-value opportunity, as FAA and EASA increasingly mandate continuous sensor-based airframe monitoring.

Key market participants include Samsung Electronics Co., Ltd., LG Display Co., Ltd., DuPont de Nemours, Inc., 3M Company, Panasonic Corporation, Rogers Corporation, StretchSense Ltd., MC10, Inc., FlexEnable Ltd., Royole Corporation, Enfucell Flexible Electronics Co., Ltd., Pragmatic Semiconductor Ltd., Toyobo Co., Ltd., Heraeus Holding GmbH, and Imprint Energy, Inc.