- Food Ingredients & Additives

- Starter Culture Market

Starter Culture Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Starter Culture Market by Form (Powder, Liquid), Starter Culture Type (Bacteria, Yeast, Mould), End Use-Application (Dairy Products, Meat and Sausages, Alcoholic Beverages, Bakery Products, Animal Feed, Others), and Regional Analysis from 2026 - 2033

Starter Culture Market Share and Trends Analysis

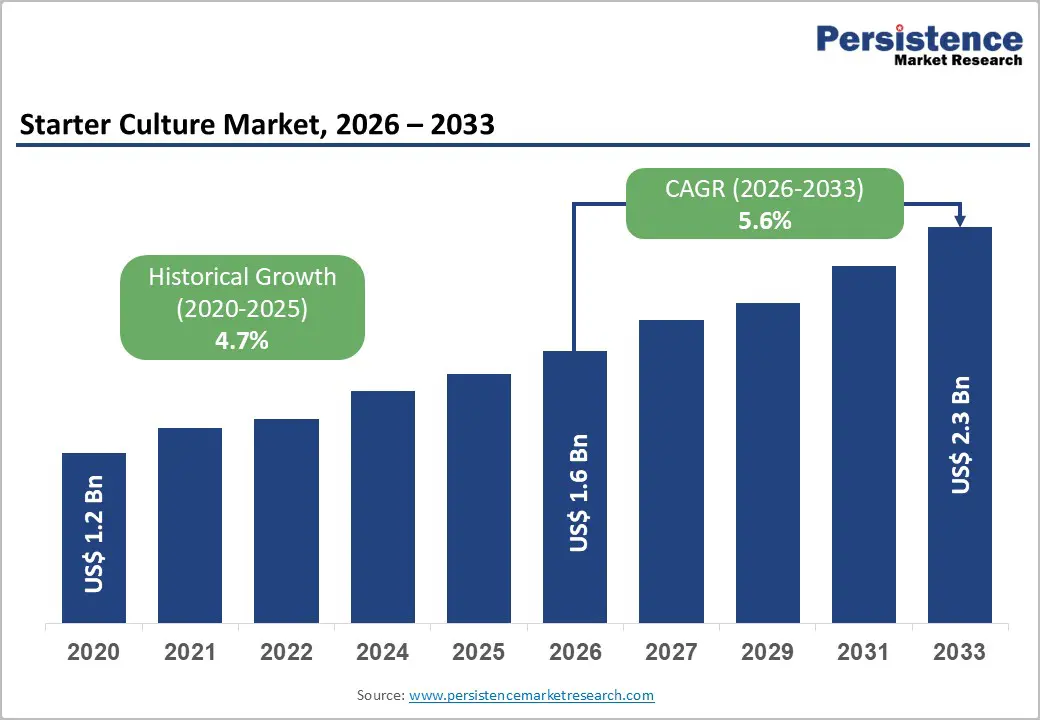

The global starter culture market is estimated to grow from US$ 1.6 billion in 2026 to US$ 2.3 billion by 2033. The market is projected to record a CAGR of 5.6% during the forecast period from 2026 to 2033.

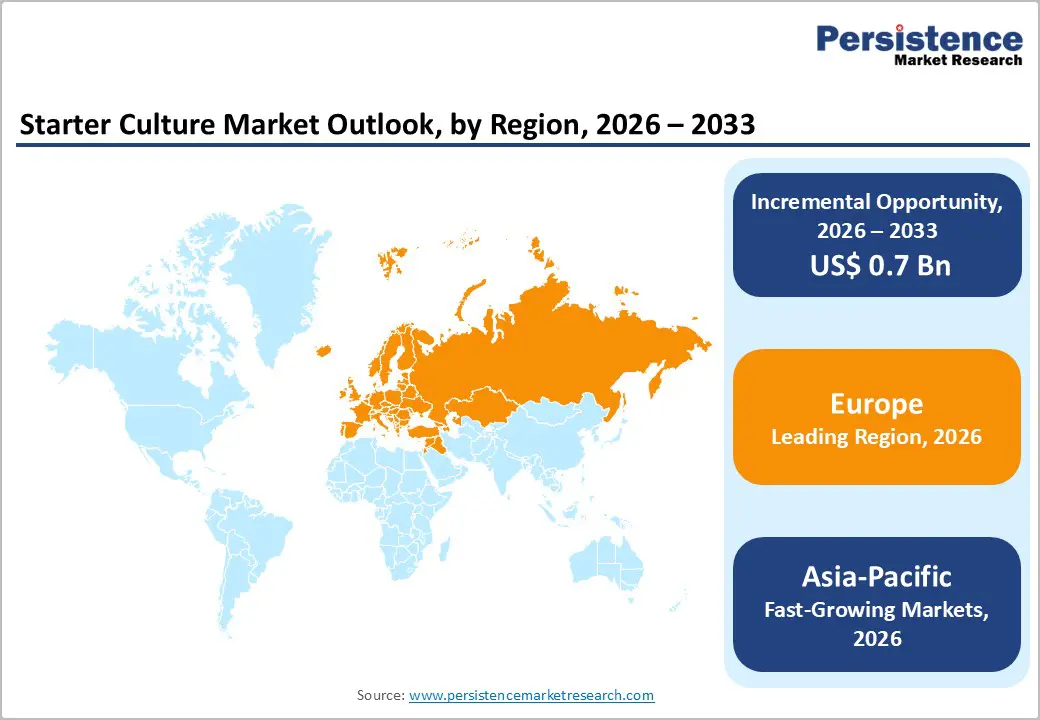

The global market is growing steadily, driven by rising demand for fermented foods, probiotics, and clean-label products. Europe dominates due to its strong dairy and cheese fermentation industry and presence of leading culture manufacturers. Asia-Pacific is the fastest-growing region, supported by expanding dairy consumption, urbanization, and increasing awareness of functional and fermented foods.

Key Industry Highlights

- Dominant Starter Culture Type: Bacteria-based starter cultures held 72.3% share in 2025, driven by extensive use in dairy products such as yogurt, cheese, and fermented milk, along with growing demand for probiotic and fermented functional foods.

- Regional Leadership: Europe led the starter culture market in 2025 with 36.1% share, supported by a strong dairy and cheese industry, long-standing fermentation traditions, and the presence of major culture manufacturers.

- Growth Indicators: Growth is driven by rising demand for fermented and probiotic foods, increasing clean-label trends, expanding dairy processing, and growing consumer awareness of gut health benefits.

- Opportunity: Opportunities exist in developing customized cultures for plant-based fermentation, functional probiotic cultures, and expanding applications in beverages, bakery, and emerging Asia-Pacific dairy markets.

| Key Insights | Details |

|---|---|

|

Global Starter Culture Market Size (2026E) |

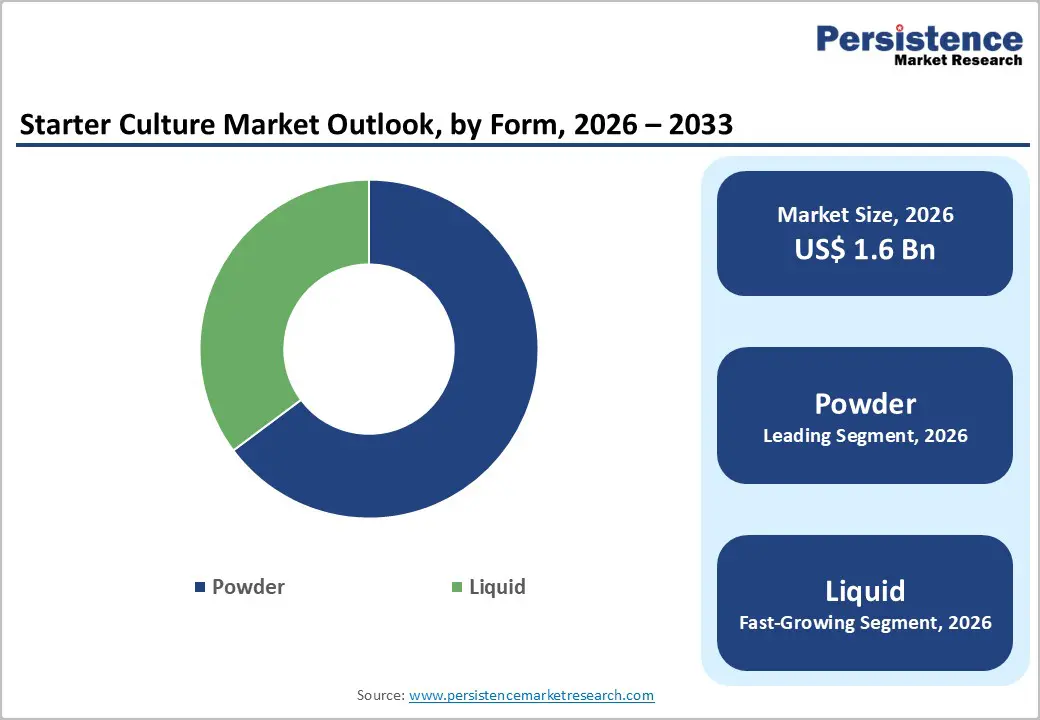

US$ 1.6 Bn |

|

Market Value Forecast (2033F) |

US$ 2.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Dynamics

Driver: Rising Global Demand for Fermented and Functional Foods

The growing global demand for fermented and functional foods is a major driver of the Starter Culture Market, as these microbial cultures are essential for producing fermented dairy, beverages, vegetables, and probiotic products. Fermented foods are widely consumed due to their digestive and immune health benefits. Additionally, more than 65% of consumers prefer fermented foods for their gut health benefits, highlighting the growing awareness of probiotics and digestive wellness worldwide.

Dairy-based fermented products such as yogurt, kefir, and cheese represent a major share of fermented food consumption, driving demand for bacterial starter cultures used in these products. The International Dairy Federation reported that global yogurt consumption reached approximately 150 million tons in 2023, demonstrating the scale of fermentation-based food production globally. As fermented dairy products dominate consumption and probiotic foods continue gaining popularity, food manufacturers increasingly rely on advanced starter cultures to maintain product quality, taste, and microbial stability. This growing consumption of fermented foods directly supports the expansion of the starter culture industry across dairy, beverage, and functional food applications.

Restraint: High Production and Storage Costs of Starter Cultures

One of the key restraints on the starter culture market is the high cost of producing, preserving, and transporting microbial cultures. Starter cultures are highly sensitive biological materials that require controlled fermentation environments, advanced bioprocessing equipment, and specialized storage systems. In many cases, cultures must be stored under strict refrigeration conditions between 2°C and 6°C to maintain microbial viability. Maintaining such cold-chain logistics significantly increases operational costs across the supply chain, particularly for small and medium-scale food processors operating in developing economies.

In addition to production costs, energy consumption and infrastructure requirements further increase manufacturers' economic burden. Temperature-controlled storage and transportation can account for about 21% of total energy expenditure in fermented food supply chains, making culture preservation and distribution costly. Furthermore, limited cold-chain infrastructure in emerging markets can result in 15–20% product loss during transportation, which discourages adoption among smaller manufacturers. These high operational costs and infrastructure challenges limit access to advanced starter cultures in some regions, thereby restraining market expansion despite growing demand for fermented and probiotic foods globally.

Opportunity: Rising Demand for Plant-Based and Dairy-Alternative Fermented Products

The increasing global shift toward plant-based diets is creating significant opportunities for the starter culture market, particularly in fermentation technologies used for dairy alternatives. Consumers are increasingly adopting vegan, vegetarian, and flexitarian diets due to health, environmental, and ethical concerns. As a result, the demand for fermented plant-based foods such as soy yogurt, almond kefir, oat-based probiotic drinks, and coconut yogurt has expanded rapidly. Studies indicate that plant-based fermented dairy alternatives already account for about 27% of fermented food consumption in some markets, demonstrating the growing acceptance of non-dairy fermentation products.

Innovation in plant-based fermentation is also accelerating the development of specialized microbial cultures tailored for non-dairy substrates. These products rely heavily on starter cultures to enhance flavor, texture, and probiotic functionality in plant-based ingredients such as soy, oats, almonds, and coconuts. As plant-based food consumption continues to rise globally, food manufacturers are increasingly investing in customized starter cultures, creating new growth opportunities for culture developers and fermentation technology providers.

Category-wise Analysis

By Product Insights

Powdered starter cultures dominate the market with 64.8% share in 2025, primarily because they provide superior stability, shelf life, and ease of transportation compared with liquid cultures. Most industrial starter cultures are produced using freeze-drying (lyophilization), a preservation process that removes water from microbial cells and keeps them metabolically inactive until rehydration. This method protects bacteria's cellular structure and allows cultures to remain viable for months or even years under proper storage conditions, which is critical for large-scale food manufacturing and global distribution.

Scientific studies also show that freeze-dried bacterial cultures maintain very high survival rates, often above 90% immediately after drying, and remain stable during long-term storage at refrigerated temperatures. Powdered cultures, therefore, reduce transportation complexity, minimize contamination risks, and allow food manufacturers to store highly concentrated microbial cultures efficiently. These advantages make powdered starter cultures the preferred format for dairy, beverage, and fermented food producers worldwide.

By Starter Culture Type Insights

Bacterial starter cultures dominate the market because most fermented foods rely on lactic acid bacteria for fermentation, particularly dairy products such as yogurt, cheese, kefir, and cultured milk. International food standards define yogurt as a product obtained through fermentation by Lactobacillus delbrueckii subsp. bulgaricus and Streptococcus thermophilus, demonstrating the central role of bacteria in fermented dairy manufacturing. These bacteria convert lactose into lactic acid, which improves flavor, texture, and microbial safety in fermented foods.

The dominance of bacterial cultures is also linked to the scale of dairy fermentation globally. According to international dairy industry statistics, global yogurt production exceeded roughly 150 million tonnes annually, making it one of the largest fermented food categories worldwide. Because bacterial cultures are essential for producing these high-volume products, they represent the most widely used starter culture type across the food processing industry, significantly driving their market dominance.

Regional Insights

Europe Starter Culture Market Trends

Europe dominates the starter culture market primarily because of its large and well-established dairy fermentation industry. The European Union produces over 160 billion liters of milk annually, and a significant portion of this milk is processed into fermented products such as cheese and yogurt that require microbial starter cultures. The region also produces more than 9 million metric tons of cheese each year, making it one of the largest cheese-producing regions in the world. These high production volumes create substantial demand for bacterial cultures used in dairy fermentation.

Another important factor is Europe’s long tradition of fermented foods and strict quality regulations. Countries such as France, Germany, and Italy produce hundreds of traditional cheese varieties that rely on specific microbial cultures for flavor and texture development. In France alone, over 350 recognized cheese varieties require unique fermentation processes. Strong regulatory frameworks, such as Protected Designation of Origin (PDO), and support from European agricultural policies also promote standardized fermentation technologies, further increasing the adoption of starter cultures in the region.

North America Starter Culture Market Trends

North America is a significant region in the starter culture market due to its large dairy processing sector and strong consumption of fermented dairy products. The United States and Canada have advanced dairy industries supported by modern processing technologies and efficient cold-chain infrastructure. High consumer demand for yogurt, cheese, and other cultured dairy foods drives the use of microbial starter cultures across food manufacturing. For example, the U.S. yogurt market alone was valued at about USD 8.1 billion, indicating the large scale of fermented dairy consumption that depends on starter cultures for fermentation and product consistency.

Health awareness and demand for probiotic foods also contribute to the region’s importance. Consumers increasingly seek products containing beneficial bacteria for digestive health, encouraging manufacturers to use specialized cultures in dairy and functional foods. In addition, government initiatives such as the U.S. Department of Agriculture’s Dairy Innovation Program support research and modernization in dairy processing technologies. These initiatives promote innovation in fermentation techniques and microbial cultures, strengthening North America’s role as a key market for starter culture development and application.

Asia-Pacific Starter Culture Market Trends

Asia-Pacific is the fastest-growing region in the starter culture market because of rapidly increasing dairy production and changing dietary patterns. Countries such as India and China have experienced strong growth in milk production and consumption of fermented dairy products. For instance, India produced about 221 million metric tons of milk in 2023, making it the world’s largest milk producer. As dairy processing expands, manufacturers increasingly adopt standardized starter cultures to produce yogurt, cheese, and fermented milk products at industrial scale.

Urbanization, rising incomes, and growing awareness of probiotic foods are also accelerating demand. As more consumers shift toward packaged and functional dairy products, yogurt and fermented beverages are increasing in consumption across major Asian economies. Government programs aimed at strengthening dairy production, such as India’s National Dairy Plan, support improvements in milk processing infrastructure and fermentation technologies. These developments encourage the adoption of commercial starter cultures in food manufacturing, making Asia-Pacific the fastest-growing regional market for fermentation ingredients and microbial cultures.

Competitive Landscape

The starter culture market is highly competitive, led by major companies such as Chr. Hansen, IFF (DuPont), DSM-Firmenich, Sacco System, and Lesaffre. These players focus on developing advanced microbial cultures, expanding fermentation solutions for dairy and plant-based foods, investing in biotechnology R&D, and strengthening global distribution to meet growing fermented food demand.

Key Industry Developments:

- In January 2026, Concerto Biosciences signed a development and commercialization agreement with Sacco System to advance next-generation microbial ingredient discovery. Through this partnership, the companies aimed to combine Concerto Biosciences’ microbial discovery platform with Sacco System’s expertise in producing and commercializing microbial cultures for the food industry.

- In September 2025, The company introduced these advanced starter cultures to support the production of semi-hard, hard, and continental-style cheeses. The new Dairy Safe™ cultures were designed to combine acidification, flavor development, and bioprotection in a single solution, helping manufacturers simplify cheese production processes while maintaining consistent product quality and safety.

Companies Covered in Starter Culture Market

- Koninklijke DSM N.V.

- Chr. Hansen

- DuPont

- Sacco System

- THT s.a.

- CSK Food Enrichment B.V.

- Dalton Biotecnologie S.r.l.

- Lesaffre

- Lallemand Inc.

- Angel Yeast Co., Ltd.

- Lactina Ltd.

- Others

Frequently Asked Questions

The global starter culture market is projected to be valued at US$ 1.6 Bn in 2026.

Rising demand for fermented foods, probiotics, dairy processing expansion, clean-label ingredients, and growing consumer gut health awareness.

The global starter culture market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Plant-based fermented products, customized microbial cultures, probiotic innovations, emerging markets expansion, and advancements in fermentation technology.