- Food Ingredients & Additives

- Specialty Food Ingredients Market

Specialty Food Ingredients Market Size, Share, and Growth Forecast 2026 - 2033

Specialty Food Ingredients Market is segmented by Nature (Organic, Conventional), by Product Type (Antioxidants, Colorants, Emulsifiers, Enzymes, Others), Application (Bakery, Confectionery, Convenience Foods, Dairy Products, Others), Distribution Channel, and Regional Analysis for 2026 - 2033

Specialty Food Ingredients Market Share and Trends Analysis

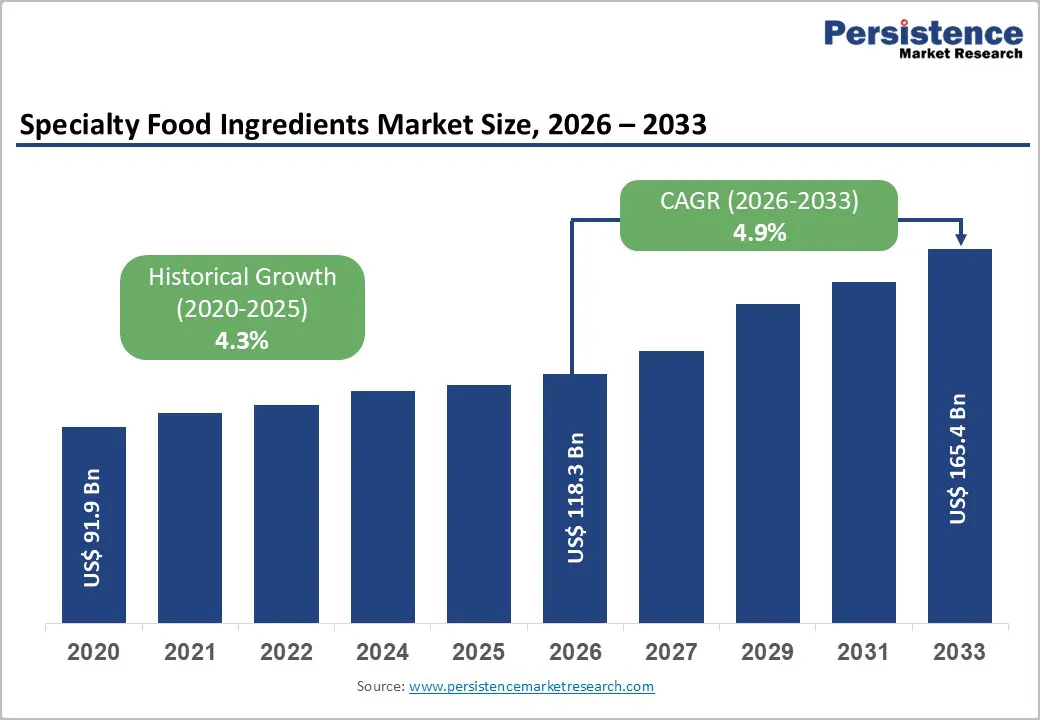

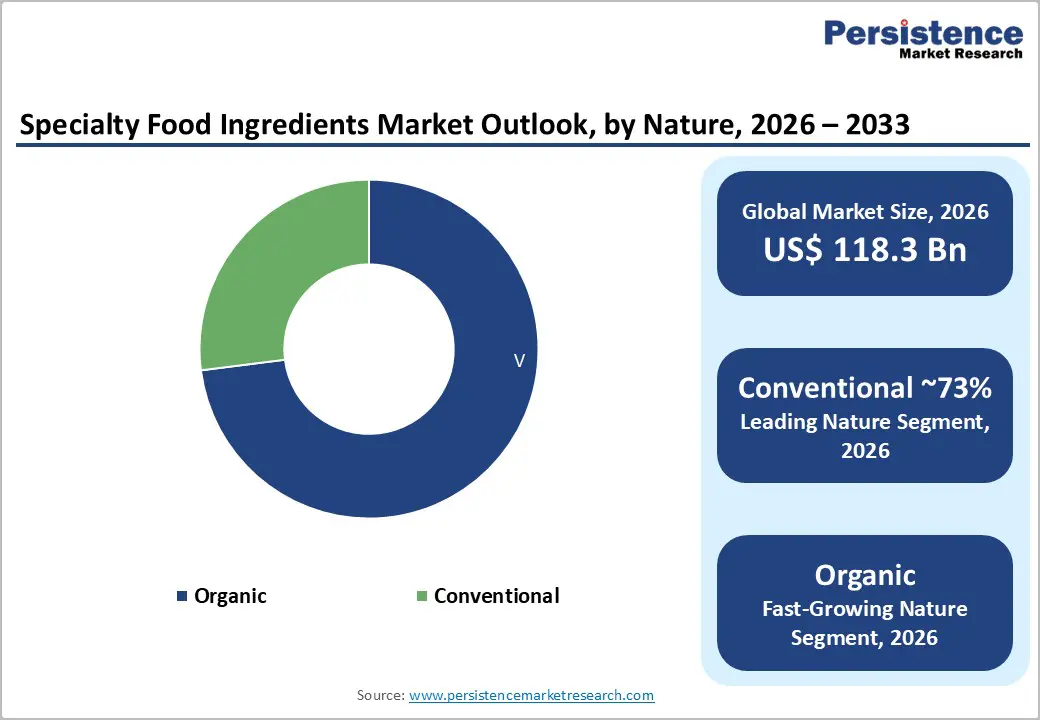

The global specialty food ingredients market size is expected to be valued at US$ 118.3 billion in 2026 and is projected to reach US$ 165.4 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

These ingredients, including emulsifiers, enzymes, antioxidants, flavors, and natural colorants, are widely used to improve texture, stability, shelf life, and nutritional value. Growing urbanization, evolving dietary habits, and rising demand for packaged and convenience foods are supporting steady market expansion across both developed and emerging economies. Current market trends highlight a strong shift toward clean-label, natural, and functional ingredients, driven by increasing consumer awareness of health and wellness. Manufacturers are focusing on plant-based, organic, and minimally processed formulations while investing in innovation to balance performance with label transparency. This trend is reshaping product development strategies and driving long-term growth.

Key Industry Highlights:

- Leading Region: North America leads the global specialty food ingredients market, supported by a highly developed food processing industry, strong demand for functional and clean-label foods, advanced formulation capabilities, and strict food safety and labelling regulations.

- Fastest Growing Region: Asia-Pacific is the fastest-growing region, driven by rapid urbanization, expanding middle-class populations, increasing consumption of packaged foods, rising disposable incomes, and growing investments in food manufacturing infrastructure.

- Leading Nature: Conventional specialty food ingredients dominate the market due to their cost efficiency, large-scale availability, stable supply chains, and widespread usage across bakery, dairy, and convenience food applications.

- Fastest Growing Nature Segment: Organic specialty food ingredients represent the fastest-growing segment, fueled by rising consumer preference for natural, minimally processed, and sustainably sourced food components.

| Key Insights | Details |

|---|---|

| Specialty Food Ingredients Market Size (2026E) | US$ 118.3 billion |

| Market Value Forecast (2033F) | US$ 165.4 billion |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 4.3% |

Market Dynamics

Driver - Rising Consumption of Processed and Convenience Foods

The rising global consumption of processed and convenience foods remains a core structural driver for the specialty food ingredients market. Rapid urbanization, longer working hours, and increasing participation of women in the workforce have significantly altered eating habits, leading to higher demand for ready-to-eat, frozen, and packaged food products. These food formats require specialty ingredients to maintain consistency, stability, and shelf life during large-scale manufacturing, transportation, and storage. Emulsifiers, enzymes, stabilizers, and antioxidants are essential for preserving texture, flavor, and visual appeal, especially in bakery, dairy, and convenience food categories.

As food manufacturers expand product portfolios to address evolving consumer preferences, the reliance on specialty ingredients continues to grow. Product differentiation through improved mouthfeel, extended freshness, and consistent quality has become a competitive necessity rather than an option. This trend is evident across both developed and emerging economies, where rising disposable incomes and urban lifestyles are driving packaged food penetration. Consequently, sustained growth in processed food consumption continues to reinforce long-term demand for specialty food ingredients.

Growing Focus on Functional, Fortified, and Clean-Label Foods

Increasing consumer awareness of health, nutrition, and preventive wellness is accelerating demand for functional and fortified foods, directly supporting specialty ingredient adoption. Consumers are actively seeking food products that offer added health benefits such as improved digestion, immunity support, and nutrient enrichment. To meet these expectations, food manufacturers are incorporating specialty ingredients, including antioxidants, enzymes, fibers, and natural colorants that enhance nutritional profiles without compromising taste or texture.

At the same time, clean-label reformulation has emerged as a strategic priority, particularly in premium and health-oriented food categories. Shoppers increasingly scrutinize ingredient lists and prefer recognizable, minimally processed components. Specialty food ingredients play a critical role in achieving this balance by delivering functionality while enabling label transparency. Manufacturers are reformulating existing products and launching new clean-label alternatives to maintain consumer trust and brand differentiation. This shift toward value-added, health-focused food product is strengthening long-term market growth and driving continuous innovation in ingredient sourcing, processing, and formulation technologies.

Restraints - Volatility in Raw Material Prices

Volatility in raw material prices remains a significant challenge for the specialty food ingredients market. Many specialty ingredients are derived from agricultural commodities that are highly sensitive to climate change, weather variability, seasonal yield fluctuations, and geopolitical disruptions. Events such as droughts, floods, or trade restrictions can quickly affect supply availability, leading to sharp price movements and procurement uncertainty for ingredient manufacturers.

Fluctuating input costs directly impact production economics, profit margins, and pricing strategies, particularly for small and mid-sized players with limited sourcing flexibility. These challenges can disrupt long-term supply agreements with food manufacturers and complicate cost forecasting. In some cases, manufacturers are forced to pass increased costs downstream, potentially affecting demand from price-sensitive customers. Persistent raw material volatility therefore introduces operational risk, limits pricing stability, and constrains overall market predictability, especially in highly competitive food ingredient segments.

Stringent Regulatory and Compliance Requirements

Strict regulatory and compliance requirements pose another major restraint for the specialty food ingredients market. Food safety authorities enforce rigorous standards related to ingredient approval, permissible usage levels, labeling accuracy, and toxicological safety. Meeting these requirements involves extensive documentation, testing, and validation, which increases development timelines and operational costs for ingredient manufacturers.

Regulatory complexity can slow innovation, particularly for novel ingredients, natural extracts, and bio-based additives that require additional safety assessments. Smaller companies often face greater challenges due to limited regulatory expertise and financial resources. Differences in regulatory frameworks across regions further complicate global product launches, as formulations may need modification to comply with local standards. These regulatory hurdles can delay commercialization, restrict market entry, and reduce innovation speed, limiting the ability of manufacturers to respond quickly to changing consumer preferences.

Opportunity - Rapid Growth of Organic and Clean-Label Ingredients

The accelerating shift toward organic and clean-label food products presents a compelling growth opportunity for specialty food ingredient manufacturers. Consumers increasingly demand transparency, traceability, and natural sourcing, driving food brands to reformulate products using organic-certified and minimally processed ingredients. This trend is particularly strong in bakery, dairy, infant nutrition, and premium packaged food categories, where clean-label positioning enhances brand value.

Improvements in organic farming practices, supply chain traceability, and certification frameworks are expanding the availability of organic raw materials, enabling broader adoption across food applications. Manufacturers investing in sustainable sourcing, organic certification, and natural ingredient innovation are well-positioned to capture premium pricing and long-term customer loyalty. As regulatory support for organic labeling strengthens and consumer trust continues to grow, organic and clean-label specialty ingredients are expected to emerge as a key revenue driver and competitive differentiator over the forecast period.

Category-wise Analysis

Nature Insights

The conventional nature segment remains the dominant force in the specialty food ingredients market, accounting for a leading 73% market share in 2025. This market leadership is fundamentally supported by the cost-effectiveness and established industrial-scale availability of conventional ingredients, which are essential for high-volume processed food manufacturing. While the Organic segment is the fastest-growing due to the heightening "clean-label" sentiment, conventional ingredients continue to provide the functional backbone for global food security. The versatility of conventional specialty ingredients, ranging from high-fructose corn syrups to synthetic antioxidants, allows for consistent shelf-life and taste profiles that are critical for mass-market retail and foodservice operations. However, the gap is narrowing as conventional manufacturers integrate more "natural-identical" components to satisfy regulatory bodies like the European Commission, which is increasingly vetting conventional additives for environmental and health impacts.

Distribution Channel Insights

The B2B (Business-to-Business) distribution channel is the dominant conduit for specialty food ingredients, as most of these value-added components are sold directly to food and beverage manufacturers. This segment's leadership is anchored by the technical complexity of the ingredients, which requires "collaborative co-creation" and significant technical support from the supplier. For instance, Ingredion’s Idea Labs® innovation centers serve as a B2B hub where the company partners with manufacturers to solve texture and sweetness challenges using their specialty portfolio. While B2C and Online Retailers are seeing an uptick in the sale of "health-focused" ingredients like protein powders or probiotics directly to consumers, the high-volume industrial demand for enzymes, emulsifiers, and stabilizers in processed foods ensures that the B2B channel remains the bedrock of the industry’s revenue stream.

Regional Insights

North America Specialty Food Ingredients Market Trends

North America maintained its leadership position in the specialty food ingredients market, accounting for approximately 34% market share in 2025, supported by a highly mature and technologically advanced food processing ecosystem. The region has a strong concentration of large-scale food and beverage manufacturers that actively invest in value-added formulations, including functional, fortified, and clean-label products. High consumer awareness regarding nutrition, ingredient transparency, and food safety has accelerated the adoption of specialty ingredients such as emulsifiers, enzymes, and natural colorants. In addition, stringent regulatory oversight by food safety authorities ensures consistent quality standards, encouraging manufacturers to rely on specialized ingredients that meet compliance requirements while enhancing product performance.

The U.S. remains the dominant contributor within North America due to its robust innovation environment and strong collaboration between ingredient suppliers and food manufacturers. Advanced research and development capabilities enable continuous improvement in ingredient functionality, shelf-life extension, and sensory enhancement. High consumer spending power and demand for premium, organic, and plant-based food products further support market expansion. Moreover, well-established distribution networks and strong B2B procurement channels allow efficient large-volume ingredient sourcing, reinforcing North America’s sustained leadership in the global specialty food ingredients market.

Asia Pacific Specialty Food Ingredients Market Trends

Asia Pacific represents the fastest-growing regional market for specialty food ingredients, driven by rapid urbanization, changing dietary habits, and rising consumption of packaged and convenience foods. Expanding urban populations and increasingly busy lifestyles have boosted demand for processed foods that require specialty ingredients to ensure stability, taste consistency, and extended shelf life. Countries such as China, India, and several Southeast Asian nations are experiencing strong growth in bakery, dairy, and ready-to-eat food segments, directly increasing demand for emulsifiers, enzymes, and antioxidants across food manufacturing applications.

The region also benefits from cost-competitive manufacturing capabilities, improving supply chain infrastructure, and rising disposable incomes among middle-class consumers. Governments across the Asia Pacific are actively promoting food processing industries through policy support, infrastructure investments, and export-oriented manufacturing initiatives. These factors encourage both domestic production and foreign investment in specialty ingredient manufacturing. In addition, the growing presence of multinational food brands and increasing adoption of Western-style packaged foods further accelerate demand. Collectively, these dynamics position Asia-Pacific as a critical growth engine for the global specialty food ingredients market over the forecast period.

Competitive Landscape

The specialty food ingredients market is moderately fragmented, with multinational players and regional specialists competing across diverse product categories. Leading companies focus on product innovation, clean-label reformulation, sustainability initiatives, and capacity expansion in emerging markets. Strategic partnerships with food manufacturers, investments in R&D, and supply chain optimization remain key competitive strategies. Emerging players are increasingly targeting niche applications and organic segments to enhance differentiation and market penetration.

Key Industry Developments:

- In October 2025, EU Specialty Food Ingredients launched a digital guide titled “Behind the Evidence: How to Interpret Scientific Research,” aimed at helping stakeholders better understand and critically evaluate scientific studies related to food ingredients.

- In May 2025, Arla Foods Ingredients expanded its distribution partnership with the Brenntag Group. Brenntag will distribute Arla Foods Ingredients' protein ingredients in Vietnam, Thailand, and Indonesia, covering health foods, infant nutrition, sports nutrition, and functional solutions for dairy and bakery applications.

Companies Covered in Specialty Food Ingredients Market

- Evonik

- Archer Daniels Midland Company

- PPG Industries

- KF Specialty Ingredients

- Koninklijke DSM N.V.

- Specialty Commodities Inc.

- Ingredion Incorporated

- Prinova Group LLC

- Naturex

- Kerry Group Plc

- Tate & Lyle Plc

- Cargill Inc.

- Frutarom

- Woodland Foods Inc.

- Others

Frequently Asked Questions

The specialty food ingredients market is estimated to be valued at US$ 118.3 Bn in 2026.

Rising consumption of processed foods, increasing demand for functional and clean-label products, and continuous innovation in food formulation technologies.

The global market is expected to witness a CAGR of 4.9% between 2026 and 2033.

Major players include Ingredion Incorporated, Cargill Inc., Kerry Group Plc, Tate & Lyle Plc, Archer Daniels Midland Company, and others.

North America is the leading region in the global specialty food ingredients market.