- Food Ingredients & Additives

- Pulse Flour Market

Pulse Flour Market Size, Share, and Growth Forecast, 2026 – 2033

Pulse Flour Market by Nature (Organic, Conventional), Pulse Type (Chickpea, Beans, Lentil, Peas, Others), Application (Bakery and Snacks, Beverages, Dairy Alternatives, Meat Substitutes, Animal Feed, Nutritional Supplements), and Regional Analysis for 2026-2033

Pulse Flour Market Share and Trends Analysis

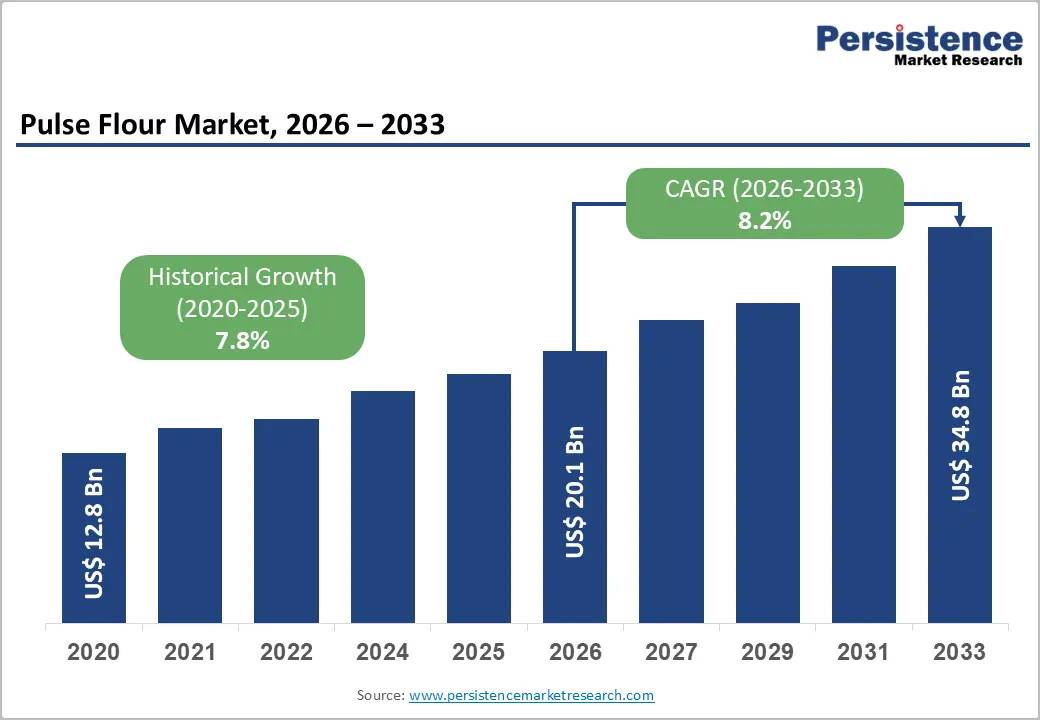

The global pulse flour market size is likely to be valued at US$ 20.1 billion in 2026 and is estimated to reach US$ 34.8 billion by 2033, growing at a CAGR of 8.2% during the forecast period 2026−2033, driven by rising demand for plant-based nutrition and functional food ingredients, supported by urbanization and evolving dietary patterns that increase consumption of protein-rich alternatives.

Growing clinical awareness of metabolic health boosts demand for low-glycemic, fiber-rich formulations. Food manufacturers incorporate pulse flour into processed foods to enhance nutrition and label transparency, while advancements in milling technologies and improving food processing infrastructure across emerging economies strengthen supply chains and support sustained growth.

Key Industry Highlights:

- Leading Pulse Type: Chickpea pulse type is set to hold around 35% revenue share in 2026, supported by versatility and cultural acceptance.

- Fastest-Growing Pulse Type: Pea pulse type is projected to be the fastest-growing segment, driven by superior functional properties in alternative proteins.

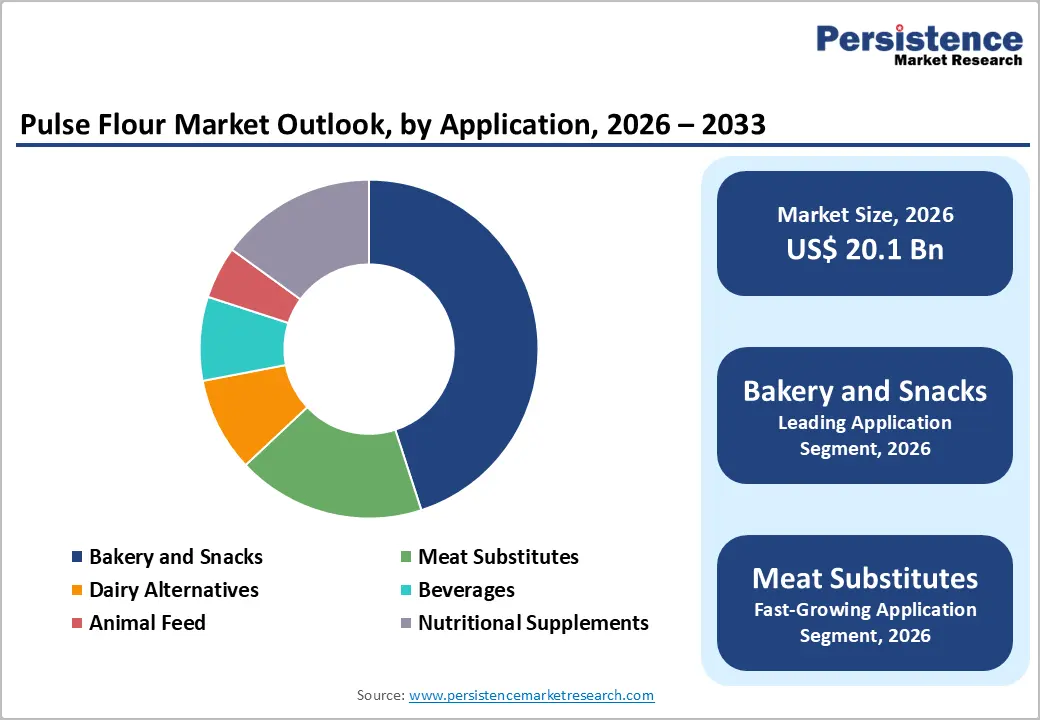

- Leading Application: Bakery and snacks are estimated to hold roughly 45% revenue share in 2026, driven by functionality, fortification, cost efficiency, and United States Department of Agriculture-supported sourcing.

- Fastest-Growing Application: Meat substitutes are forecast to record the fastest growth, driven by texture, efficiency, and extrusion in products such as lentil burgers and chickpea nuggets.

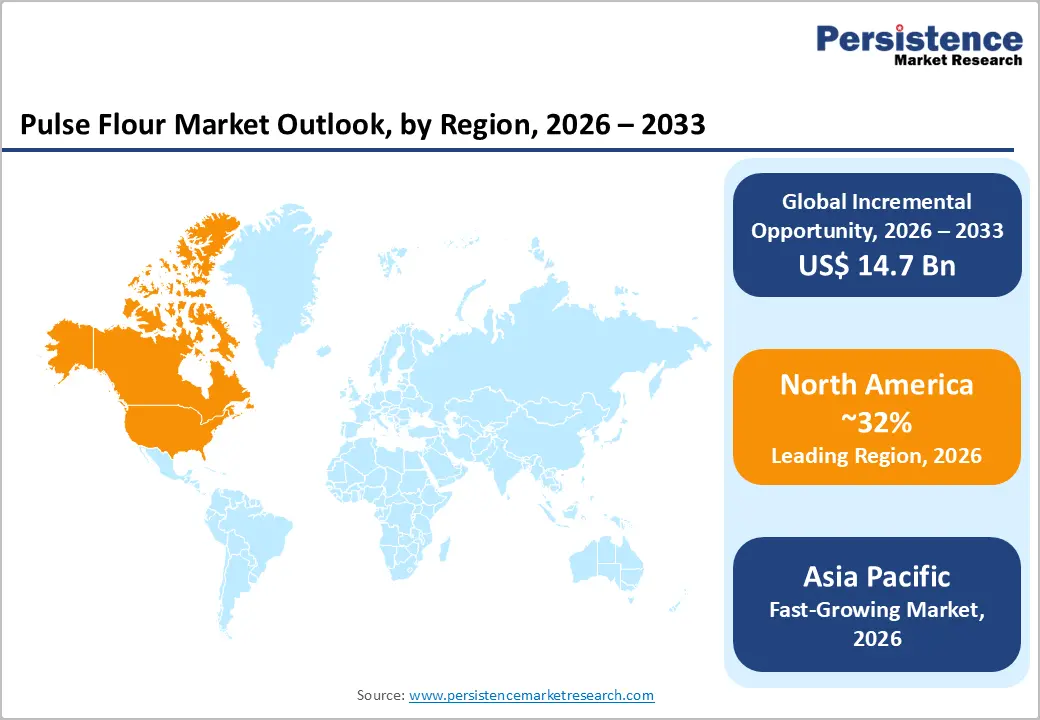

- Regional Leadership: North America is projected to capture roughly 32% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth, stimulated by rapid urbanization and rising protein demand.

DRO Analysis

Driver - Rising Demand for Plant-Based Protein Sources

Plant-based protein demand is tightening the link between consumer diets and ingredient choices, pushing food manufacturers to reformulate around high-protein, plant-derived components. Pulse flour delivers dense protein, fiber, and micronutrients while meeting gluten-free and clean-label requirements, which aligns directly with these shifting priorities. As consumers treat protein intake as a core nutritional metric, brands increasingly replace or blend conventional wheat flour with pulse-based alternatives across baked goods, snacks, and ready-to-eat meals to capture this structural demand.

This protein-driven shift also improves unit economics and supply resilience for food producers. Pulse crops generally require less synthetic input and fit well into crop-rotation systems, lowering long-term input costs and supporting sustainability commitments. U.S. Department of Agriculture data for 2025 indicate rising pulse acreage and output, reflecting how policy and farm-level incentives are reinforcing the supply base for pulse flour. With stronger, more efficient supply chains and higher-value protein content, the ingredient is positioned to expand further into mass-market and institutional channels.

Restraint - Supply Chain Volatility and Agricultural Dependency

Weather-dependent pulse farming creates recurring spikes in raw-material costs and availability, which directly compresses processor margins and complicates long-term planning. Many major pulse-producing regions rely on rain-fed agriculture and limited irrigation infrastructure, leaving supply highly exposed to drought, heatwaves, and shifting precipitation patterns. U.S. Department of Agriculture data for 2025 show that domestic pulse output fell short of early projections, underscoring how easily forecasted supply can unravel under adverse conditions.

This agricultural dependency also amplifies supply-chain complexity for finished-goods manufacturers. Fluctuating pulse yields force buyers to switch suppliers or geographies, increasing freight, certification, and quality-control costs. Regional concentration of production further raises counterparty risk, as simultaneous shortfalls in key exporting basins can trigger global price volatility. Under these conditions, pulse-based formulations become harder to standardize and price-stabilize, limiting the speed and scale of commercial rollout.

Opportunity - Innovation in Gluten-Free and Functional Food Segments

Gluten-free and functional food innovation is reshaping ingredient portfolios, creating a structural opening for pulse flour to move beyond niche applications. Manufacturers seeking clean-label, high-protein, and allergen-friendly formulations increasingly pair pulse flour with alternative starches to improve texture and nutritional density. This shift supports premiumization across snacks, bakery, and on-the-go products, where protein-fortified gluten-free formats command higher margins and stronger repeat purchase behavior.

Pulse flour also enhances operational efficiency in formulations that require multiple functional ingredients. Replacing synthetic additives with pulse-derived gum-like properties reduces complexity in supply-chain management and labeling. Data from the U.S. Department of Agriculture for 2025 show steady growth in domestic pulse production, indicating a scalable, cost-efficient base for further expansion into gluten-free and functional categories. This combination of technical versatility and favorable supply-side dynamics positions pulse flour as a core building block for next-generation product development.

Category-wise Analysis

Nature Insights

The conventional segment is anticipated to secure around 70% of the pulse flour market share in 2026, reflecting established supply chains, economies of scale, and broad compatibility with large-volume food manufacturing. Processors leverage cost advantages to serve bakery and snack producers that prioritize price stability, using standard chickpea flour in tortilla lines and lentil flour in extruded snacks. Bulk distribution networks align with industrial procurement cycles, while yield-focused innovation sustains preference among cost-conscious manufacturers.

The organic segment is expected to be the fastest-growing segment, propelled by consumer demand for certified sustainable ingredients and stricter residue standards. Health professionals increasingly endorse organic pulse flour for allergen-sensitive groups, and dedicated segregation protocols preserve nutritional integrity. Examples include organic chickpea flour in gluten-free crackers and organic pea flour in clean-label protein bars. E-commerce platforms expand accessibility, while government data show rising organic pulse acreage signaling supply-side readiness.

Pulse Type Insights

Chickpea pulse type is poised to dominate with a projected market share of over 35% in 2026, powered by versatile functionality in both sweet and savory applications and widespread cultural familiarity. Consumer trust stems from long-established use in dishes such as hummus, falafel, and Indian curries. Examples include besan in pakoras and bakery items, and garbanzo flour in pasta and Mediterranean snacks. Retail penetration benefits from shelf-stable formats and recognizable packaging. The United States Department of Agriculture data indicate stable chickpea output, supporting steady commercial availability and consistent supply chains.

Pea pulse type is estimated to be the fastest-growing segment, fueled by neutral flavor and superior emulsification that suit modern plant-based formulations. Consumer trust builds through clean-label positioning in protein-rich bars, shakes, and dairy-free alternatives. Examples include yellow pea flour in gluten-free bread and plant-based burgers, and pea protein blends in ready-to-drink shakes. Government statistics show rising pea cultivation yields, while innovation in deflavored variants removes taste barriers and expands adoption among sensitive consumers.

Application Insights

The bakery and snacks segment is likely to be the leading segment with a projected 45% of the pulse flour market share in 2026, due to functional advantages in texture development and nutritional fortification of everyday products. Clinical credibility stems from measurable improvements in protein and fiber in items such as pulse-fortified crackers, high-protein muffins, and multigrain breads. Manufacturer adoption increase as food technologists validate performance on high-volume lines. Accessibility improves through standardized particle sizes, while cost-efficiency arises from partial wheat replacement that maintains yield. The United States Department of Agriculture data on pulse availability underpin reliable sourcing for this category.

The meat substitutes segment is anticipated to be the fastest-growing segment, fueled by demand for texturized proteins that replicate mouthfeel in plant-based analogs. Clinical credibility strengthens through alignment with dietary guidelines that elevate pulses in protein food groups. Examples include lentil-based burger patties, chickpea-ortified nuggets, and pea-flour meatballs. Provider referrals grow as formulators integrate pulse flours for binding and moisture retention. Digitalization enables rapid prototyping, while cost efficiency arises from lower raw-material intensity versus isolates. Technology-enabled service delivery incorporates high-shear extrusion to enhance texture and functionality.

Regional Insights

North America Pulse Flour Market Trends

North America is expected to lead with an estimated 32% of the pulse flour market share in 2026, supported by advanced processing infrastructure and stable raw material pipelines across the U.S. and Canada. Large-scale milling and fractionation capacity operated by Archer Daniels Midland and Ingredion Incorporated ensures consistent quality and functional standardization. The United States Department of Agriculture reports stable chickpea and pea output, reinforcing supply continuity and supporting high-volume industrial utilization.

Demand intensity is reinforced by the rapid expansion of plant-based portfolios led by Beyond Meat and Impossible Foods. Food manufacturers prioritize pulse ingredients for protein enrichment and clean-label positioning across mainstream retail. Investment in extrusion and protein isolation technologies strengthens functionality in meat analogs and dairy alternatives. Established logistics networks and contract farming systems improve procurement efficiency, while private-label expansion by Walmart and Kroger increases shelf penetration.

Europe Pulse Flour Market Trends

Europe is emerging as a core hub for value-added pulse flour applications, with strong adoption in gluten-free bakery, plant-based snacks, and functional foods. Major Food-processing clusters in Germany, France, and the Netherlands integrate pea, chickpea, and fava flours into industrial baking lines, leveraging existing milling infrastructure and distribution networks. Regulatory frameworks that favor whole-pulse ingredients over isolates support long-term formulation stability, enabling established brands to embed pulse flours into mainstream Stock Keeping Units (SKUs) rather than niche products.

European producers, such as Vicent Foods, Avena Foods, and local millers, are investing in fractionation and deflavoring technologies to improve functionality and sensory performance in premium formats. Digital recipe platforms and predictive modeling tools shorten innovation cycles, helping bakeries and snack manufacturers launch new pulse-fortified products faster. E-commerce growth and private-label expansion further amplify reach, positioning Europe as a structurally important node in the global pulse flour value chain.

Asia Pacific Pulse Flour Market Trends

Asia Pacific is forecast to be the fastest-growing market for the pulse flour market, stimulated by rapid urbanization, rising protein demand, and policy support in key economies. China is expanding pulse-fortified bakery and snack lines, with companies, such as Sino-Grain and local millers, integrating chickpea and pea flours into mass-market products. India is scaling up pulse-based staples and packaged foods, supported by domestic producers such as Samex and Adani Wilmar that leverage large-scale lentil and chickpea processing.

Japan and South Korea are embedding pulse flours into health-oriented bakery, noodle, and convenience formats, with players such as Nissin Foods and CJ CheilJedang deploying pea and lentil flours for clean-label positioning. Modernized milling clusters in Vietnam and Thailand, backed by investments from firms such as Buhler and local processors, improve flour consistency and throughput. E-commerce platforms such as Alibaba and regional grocery-tech players accelerate the distribution of premium pulse-based SKUs, creating a dense, high-velocity channel network that underpins faster growth than slower-expanding mature markets.

Competitive Landscape

The global pulse flour market remains moderately fragmented with the presence of regional and global players. Leading companies such as Archer Daniels Midland Company, Ingredion Incorporated, and AGT Food and Ingredients Inc. account for a notable share through large-scale production and advanced processing capabilities. Competitive positioning is shaped by consistent product quality, integrated sourcing networks, and expanding applications across bakery, snacks, and plant-based categories.

Mid-sized and emerging participants such as Avena Foods Limited and Tate & Lyle PLC focus on specialty formulations and functional ingredient innovation. Smaller companies strengthen regional presence through targeted offerings and flexible supply models. Differentiation is driven by clean-label positioning, customized blends, and responsiveness to evolving food manufacturing requirements across diverse end-use segments.

Key Industry Developments:

- In April 2026, the Karnataka government announced plans to boost kharif pulse production by improving yields to around 845 kg per hectare through targeted agricultural initiatives, strengthening raw material availability for pulse flour processing, and supporting supply chain stability.

- In February 2025, Uganda-based Yellow Star, in collaboration with CGIAR partners, introduced a nutrient-dense bean-based composite pulse flour designed to address malnutrition by improving protein and iron intake and food security among vulnerable populations.

Companies Covered in Pulse Flour Market

- Archer Daniels Midland Company

- Ingredion Incorporated

- AGT Food and Ingredients Inc.

- Avena Foods Limited

- Tate & Lyle PLC

- Bob’s Red Mill Natural Foods

- Roquette Frères

- Buhler Holding AG

- Anchor Ingredients Co. LLC

- Ganesh Consumer Products Limited

- Tata Consumer Products

- Ardent Mills

- The Scoular Company

- Best Cooking Pulses

- Parakh Agro Industries

Frequently Asked Questions

The global pulse flour market is projected to reach US$20.1 billion in 2026.

Rising demand for plant-based protein, clean-label ingredients, and fiber-rich formulations in processed and functional foods drives the pulse flour market.

The pulse flour market is poised to witness a CAGR of 8.2% from 2026 to 2033.

Expansion of plant-based foods, gluten-free product innovation, and growing use of pulse ingredients in high-protein snacks and meat alternatives create key market opportunities.

Some of the key market players include Archer Daniels Midland Company, Ingredion Incorporated, AGT Food and Ingredients Inc., Avena Foods Limited, and Tate & Lyle PLC.