- Communication Infrastructure & Services

- Small Cell Networks Market

Small Cell Networks Market

Small Cell Networks Market by Component (Hardware, Software, Services), by Cell Type (Femtocell, Picocell, Microcell), Deployment (Indoor, Outdoor), End-user (Residential, Enterprises, Telecom Operators, Industrial, Public Infrastructure, Others), and Regional Analysis, 2026 - 2033

Small Cell Networks Market Size and Trend Analysis

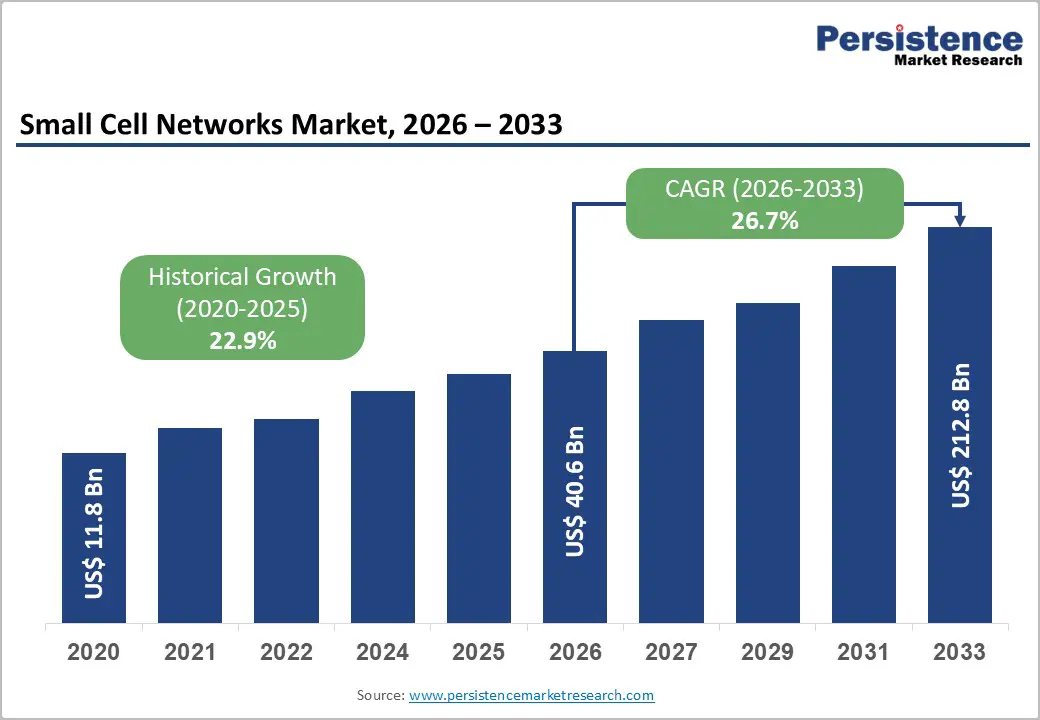

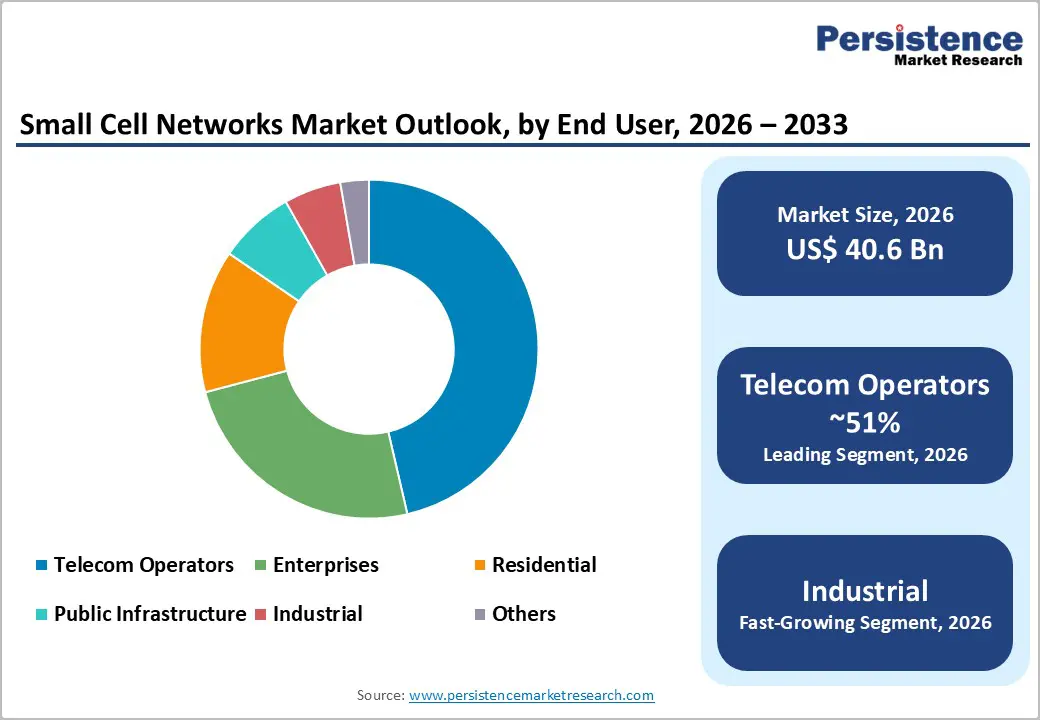

The global small cell networks market size is expected to be valued at US$ 40.6 billion in 2026 and is projected to reach US$ 212.8 billion by 2033, growing at a CAGR of 26.7% between 2026 and 2033, driven by an unprecedented convergence of 5G densification mandates, surging mobile data traffic, and enterprise digitisation at scale. This trajectory reflects the critical role that small cells play in bridging macro-network coverage gaps and enabling ultra-low-latency connectivity in dense urban environments. Accelerating 5G rollout programmes across North America, Europe, and Asia Pacific combined with rising enterprise demand, and for private wireless networks.

Key Industry Highlights:

- Leading Component: Hardware dominates the Small Cell Networks market with over 65% share in 2026, valued at more than US$ 26.4 Bn, driven by the capital-intensive nature of network densification requiring radio units, antennas, and power systems for each deployment.

- Leading Cell Type: Femtocells lead with 46% market share in 2026, valued at over US$ 18.7 Bn, supported by their low cost, plug-and-play deployment, and strong adoption for residential and small office indoor coverage.

- Leading Deployment: Indoor deployment dominates with over 62% share in 2026, valued at more than US$ 25.1 Bn, due to the majority of mobile data consumption occurring indoors and persistent signal attenuation in modern buildings.

- Fastest Growing Deployment: Outdoor deployment is the fastest growing, propelled by urban 5G densification, smart city initiatives, and rising connectivity demand across public venues and transport corridors.

- Leading End-user: Telecom operators account for over 51% market share in 2026, valued at approximately US$ 20.7 Bn, driven by large-scale 5G rollout requirements and exponential mobile data growth.

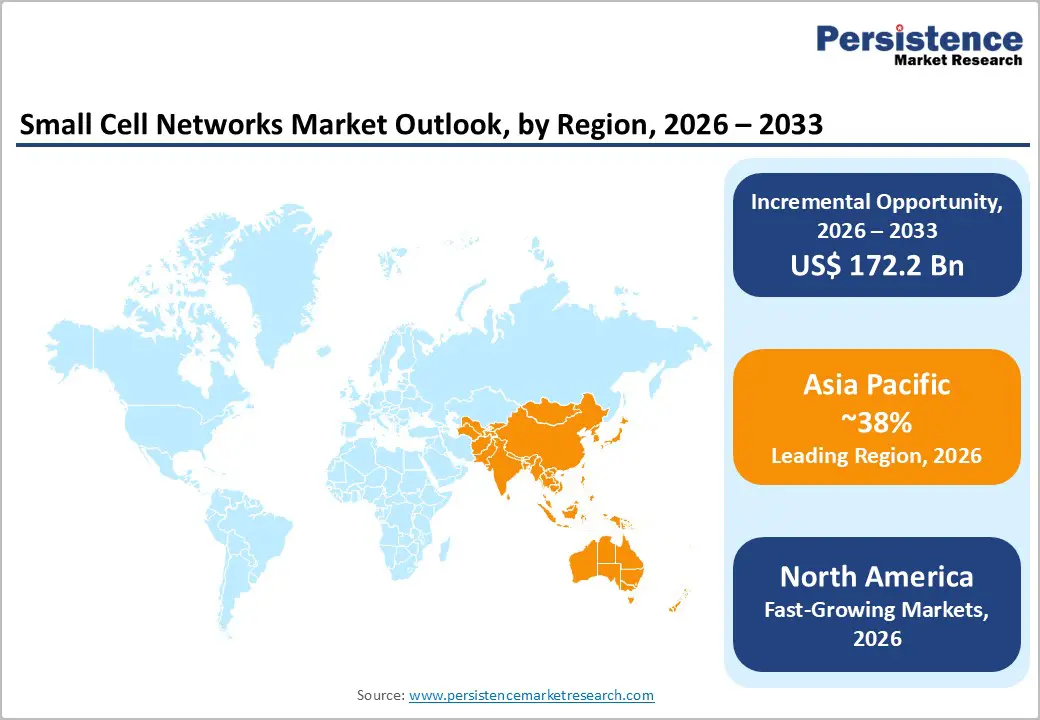

- Leading Region: Asia Pacific leads with 38% market share in 2026, valued at US$ 15.43 Bn, driven by aggressive 5G deployments, government-led smart city initiatives, and industrial digitization across China, Japan, and India. It is also the fastest-growing region, expanding at a CAGR of 33.2%, supported by a large-scale subscriber base and increasing enterprise adoption of private networks.

Market Dynamics

Drivers - Explosive Growth in Mobile Data Traffic and Indoor Connectivity Demand

Mobile data traffic globally is growing at a rate that macro-network infrastructure cannot absorb without significant small cell supplementation, and this imbalance is surging demand. According to a study, over 80% of mobile data traffic originates indoors, inside offices, shopping centres, airports, stadiums, and residential complexes where macro tower signals are weakest.

Enterprises increasingly demand carrier-grade indoor connectivity as a prerequisite for deploying Internet of Things (IoT) devices, augmented reality (AR) tools, and mission-critical communications platforms. This creates a powerful pull-side dynamic where both operators and enterprise end users simultaneously invest in small cell solutions, compressing sales cycles and broadening the total addressable market.

Accelerating Global 5G Network Densification

The global mandate to densify 5G networks to meet the throughput and latency requirements that macro towers alone cannot fulfil is driving demand for small cell networks market. Telecom operators across the United States, South Korea, Japan, and China have committed billions of dollars in capital expenditure specifically to small cell deployments as part of their mid-band and millimetre-wave (mmWave) 5G strategies.

The mmWave 5G signals attenuate significantly over short distances and require small cell nodes every 100-200 metres in dense urban corridors, making small cell infrastructure non-negotiable rather than optional. This structural dependency means that every new 5G spectrum auction and every new operator licence agreement directly translate into incremental small cell network investment.

Restraints - High Upfront Capital Expenditure and Site Acquisition Complexity

The prohibitively high upfront cost associated with deploying dense small cell grids, particularly in urban environments where real estate and permitting costs are elevated, is limiting the growth. Securing rooftop rights, street furniture mounting agreements, and municipal permits for thousands of individual small cell nodes adds substantial time and cost to network rollout timelines, sometimes extending project schedules by 12-24 months in heavily regulated jurisdictions.

Smaller telecom operators and emerging-market carriers frequently lack the capital reserves and regulatory relationships to execute large-scale small cell programmes at the pace that 5G roadmaps demand. This cost barrier concentrates deployment activity among tier-one operators and well-capitalised infrastructure firms, limiting the breadth of market participation.

Spectrum Interference and Backhaul Capacity Constraints

Deploying small cells at high density introduces technical challenges around inter-cell interference management and backhaul capacity, and these challenges erode network performance gains if not carefully engineered. As the density of small cell nodes increases particularly in environments where multiple operators co-exist, managing radio frequency (RF) interference requires sophisticated self-organising network (SON) software and continuous optimisation, adding operational complexity and cost.

Backhaul connectivity, whether via fibre, microwave, or millimetre-wave links, must scale proportionally with small cell density, and in markets where fibre penetration remains below 40%, this creates a genuine bottleneck. Operators that underestimate backhaul planning during the network design phase frequently encounter performance degradation that undermines the business case for their small cell investments.

Opportunities - Open RAN Architecture Adoption Driving Vendor Diversification

Open RAN disaggregates hardware and software components, allowing operators to mix and match best-of-breed small cell solutions from multiple vendors rather than committing to a single proprietary ecosystem. Regulatory momentum behind Open RAN, including government mandates in the United Kingdom, United States, and Japan, is accelerating operator trials and commercial deployments at a pace that creates a significant new pipeline for vendors capable of delivering compliant, interoperable small cell products.

Vendors that invest now in Open RAN-compatible hardware and cloud-native RAN software stand to gain outsized market share when operators are making long-term network architecture commitments.

Private 5G Network Deployments Across Industrial and Enterprise Verticals

Manufacturers, logistics operators, ports, mining companies, and smart factory operators are actively evaluating private wireless networks to support automated guided vehicles (AGVs), real-time video analytics, and machine-to-machine (M2M) communication, all of which demand the low-latency, high-reliability connectivity that small cells enable. Regulatory bodies in the European Union, the United States, and Germany have allocated dedicated spectrum bands for private network use, removing a historical barrier to entry and dramatically accelerating enterprise procurement decisions.

Vendors with proven indoor small cell portfolios and systems integration capabilities are best positioned to capture this opportunity by offering end-to-end private network solutions rather than standalone hardware.

Category-wise Analysis

Component Insights

Hardware segment accounts for 65.0% of the global small cell networks market in 2026, exceeding the value of US$ 26.4 Billion. This leadership is driven by the capital-intensive nature of network densification, where each small cell deployment requires dedicated physical infrastructure, including radio units, antennas, power systems, and enclosures. The integration of advanced technologies such as Massive MIMO radios and the proliferation of indoor enterprise deployments, including private 5G and neutral host networks, are further elevating hardware spending per node.

The Software segment is the fastest-growing component category, driven by the increasing need for network automation, AI-based optimisation, cloud-native RAN architectures, and Open RAN software stacks. As operators deploy dense and highly distributed networks, software becomes essential for real-time control, scalability, and cost efficiency capabilities that hardware alone cannot provide. This reinforces the strategic importance of integrated hardware-software solutions to maintain performance and operational efficiency.

Cell Type Insights

Femtocells hold for 46.0% of the share in 2026, with a value of over US$ 18.7 Billion. Their plug-and-play deployment model, low cost, and ability to improve indoor coverage make them well-suited for coverage-challenged locations such as homes, small offices, and branch sites. Broadband operators have deployed millions of femtocell units to offload macro-network traffic and enhance indoor quality of experience (QoE). Femtocells continue to represent a large installed base; however, their growth is moderating as operators increasingly invest in enterprise small cells, 5G indoor systems, and alternative offloading solutions.

Picocells are the fastest-growing cell type category, due to the increasing need for higher-capacity indoor coverage solutions at enterprise campuses, shopping malls, transportation hubs, and stadiums. Their ability to support higher user densities, deliver consistent throughput, and operate within managed enterprise environments makes them well-suited for 4G and 5G deployments. Growth is further supported by increasing adoption of private networks, neutral host models, and digital transformation initiatives, where enterprises require scalable, low-latency, and high-performance connectivity solutions.

Deployment Insights

Indoor deployment segment accounts for 62.0% of the global Small Cell Networks market in 2026, with a value of over US$ 25.1 Billion, reflecting the fundamental reality that the majority of cellular coverage and capacity challenges originate inside buildings. This leadership is driven by macro network signals that lose 10-30 dB or more when penetrating modern construction materials such as low-emissivity glass and reinforced concrete, resulting in persistent indoor coverage gaps. Indoor small cells provide a cost-effective and scalable solution to address these challenges, particularly in dense urban and enterprise environments.

Outdoor segment is the fastest growing, propelled by smart city initiatives, urban 5G densification programs, and infrastructure upgrades across transportation corridors and public venues. As mobile data traffic surges in dense urban environments, macro networks alone are insufficient to deliver the required capacity and low-latency performance. It plays a critical role in addressing coverage gaps, particularly for high frequency 5G deployments, enabling enhanced connectivity in city centers, stadiums, and transit hubs.

End-user Insights

Telecom Operators account for 51% of the global Small Cell Networks market in 2026, approximately to US$ 20.71 Billion, due to the need to support large-scale 5G deployments, particularly in dense urban environments where network densification is critical to meeting capacity and quality-of-service requirements. While spectrum licences in several markets include coverage and performance obligations that indirectly encourage small cell deployment, the primary driver remains the exponential growth in mobile data traffic and the need to enhance indoor and hotspot coverage. Leading mobile network operators across the United States, China, Germany, and Japan are increasingly allocating a meaningful portion of their radio access network (RAN) capital expenditure toward small cell infrastructure.

The industrial segment is growing at the fastest rate, due to the rapid adoption of private 5G networks across factories, warehouses, ports, and energy facilities. These environments require ultra-reliable, low-latency connectivity to support autonomous operations, predictive maintenance, and real-time process monitoring. Small cells play a critical role by enabling localized, high-capacity network coverage and seamless integration with edge computing infrastructure. As industries accelerate digital transformation and Industry 4.0 initiatives, demand for dedicated and secure wireless networks continues to rise, further driving segment growth.

Regional Insights

North America Small Cell Networks Market Trends and Insights

North America accounts for 30.0% of the global Small Cell Networks market in 2026, representing US$ 12.2 Billion, underpinned by some of the world's advanced 5G spectrum deployment programmes and the highest per-capita mobile data consumption rates. The Federal Communications Commission (FCC) in the United States has actively streamlined small cell permitting through infrastructure rules that cap local authority review timelines, directly accelerating deployment velocity.

The United States Small Cell Networks market represents 78.0% of the North America regional market in 2026, value over US$ 9.5 Billion, driven by the aggressive 5G buildout strategies of AT&T, Verizon, and T-Mobile US. Federal infrastructure funding programmes, including allocations under the Infrastructure Investment and Jobs Act, are supplementing commercial operator investment and accelerating municipal small cell deployment.

Europe Small Cell Networks Market Trends and Insights

Europe accounts for 25.0% of the share in 2026 with growth shaped by the European Union's ambitious 5G Action Plan and member-state commitments to deliver uninterrupted 5G coverage along major transport corridors and urban centres by 2030. The regulatory environment in Europe actively encourages Open RAN adoption, creating fertile conditions for challenger vendors to gain traction alongside incumbent suppliers.

Germany small cell networks market represents 23.0% of the Europe regional market in 2026, approximately to US$ 2.33 Billion, due to its advanced industrial digitisation agenda. The Bundesnetzagentur (Federal Network Agency) has allocated dedicated spectrum for private campus networks, catalysing enterprise-grade small cell deployments outside of traditional telecom operator rollouts.

The United Kingdom small cell networks market is expected to be valued at over US$1.83 billion, supported by its Wireless Infrastructure Strategy targeting nationwide standalone 5G coverage. The Shared Rural Network programme and urban 5G densification initiatives by BT/EE, Vodafone UK, O2, and Three UK are collectively expanding small cell deployment activity across metropolitan and transport corridor environments.

France small cell networks market value is expected to surpass US$ 1.52 billion in 2026, driven by the French government's digital infrastructure investment priorities under its France 2030 plan. Public infrastructure demand, including smart transportation systems and connected public spaces, is emerging as a secondary growth driver that supplements operator-led investment.

Asia Pacific Small Cell Networks Market Trends and Insights

Asia Pacific accounts for 38.0% of the global small cell networks market in 2026, representing US$ 15.43 billion, and it is the fastest-growing market. Government-led smart city programmes and industrial digitisation initiatives across the region are amplifying demand well beyond operator-driven deployments.

The China small cell networks market account over 40% of the Asia Pacific regional market in 2026, surpassing a value of over US$ 6.17 Billion. The Chinese government's strategic priority for 5G leadership, embedded in its 14th Five-Year Plan, directly mandates small cell deployment at a pace and scale that no other national market currently matches.

Japan small cell networks market is expected to surpass the value of US$ 2.31 billion in 2026, underpinned by Japan's advanced 5G ecosystem. Japan's market is structurally differentiated by its high indoor deployment intensity, driven by the country's densely populated urban building stock and its leadership in robotics and smart manufacturing applications that require private wireless networks.

India Small Cell Networks market is expected to exceeding US$ 2.01 Billion value by 2026. India's market is at an earlier stage of small cell densification relative to China and Japan, but the scale of its mobile subscriber base, exceeding 1.2 billion connections, creates enormous long-term demand for capacity enhancement solutions.

Competitive Landscape

The small cell networks market exhibits a moderately concentrated competitive structure at the top tier, where a small number of scale vendors, particularly those with integrated hardware, software, and managed services capabilities, command disproportionate revenue share. Companies are focusing on technology differentiation, particularly in enterprise and industrial segments where reliability, latency performance, and vendor support quality outweigh procurement cost considerations.

Strategic consolidation activity is intensifying, as larger vendors seek to acquire software capabilities and channel access to defend against Open RAN-driven disaggregation. Cloud-native RAN platforms, AI-powered network management, and end-to-end private network offerings are emerging.

Key Developments:

- February 2026, Airspan Networks launched its AirUnity portfolio of software-defined small cells, supporting both LTE and 5G deployments for carriers and enterprises. The solution enables flexible, scalable network densification across indoor and outdoor environments, strengthening next-generation connectivity use cases.

- February 2026, The Small Cell Forum launched an initiative to bridge the gap between local authorities and the telecom industry, aiming to simplify small cell deployment processes. The program provides standardized tools and frameworks to address regulatory and municipal challenges, thereby accelerating small cell network rollouts.

Small Cell Networks Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 11.8 Billion |

| Current Market Value (2026) | US$ 40.6 Billion |

| Projected Market Value (2033) | US$ 212.8 Billion |

| CAGR (2026 - 2033) | 26.7% |

| Leading Region | Asia Pacific, 38.0% Share |

| Dominant Component | Hardware, 65.0% Share |

| Top-ranking Cell Type | Femtocell, 46.0% Share |

| Incremental Opportunity (2026 - 2033) | US$ 172.2 Billion |

Companies Covered in Small Cell Networks Market

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Samsung Electronics Co., Ltd.

- Airspan Networks Inc.

- CommScope Inc.

- Cisco Systems, Inc.

- NEC Corporation

- Mavenir Systems, Inc.

- Parallel Wireless, Inc.

- JMA Wireless

- Casa Systems, Inc.

- Qualcomm Technologies, Inc.

- Others

Frequently Asked Questions

The small cell networks market size is likely to be valued at US$ 40.6 billion in 2026 and is expected to reach US$ 212.8 billion by 2033, growing at a CAGR of 26.7%, driven by rapid 5G densification and rising demand for high-capacity, low-latency networks.

Growth is fueled by 5G network densification, especially for mmWave deployments, and the fact that 80% of data traffic originates indoors. Supportive regulations and enterprise spectrum allocations are accelerating adoption.

The hardware segment dominates with 65% share in 2026 due to essential investments in radios, antennas, and infrastructure.

Asia Pacific leads with 38.0% share in 2026 with a value over US$15.43 billion, driven by strong government support, spectrum availability, and high data consumption, further accelerating small cell adoption.

The opportunity lies in private 5G networks across industries like manufacturing, logistics, and energy. Enterprises are investing in dedicated small cell infrastructure to enable automation and real-time connectivity.

Leading players include Telefonaktiebolaget LM Ericsson, Nokia Corporation, Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., ZTE Corporation, and CommScope Inc.