- Communication Infrastructure & Services

- Maritime Digitization Market

Maritime Digitization Market Size, Share, and Growth Forecast, 2026 - 2033

Maritime Digitization Market by Component (Hardware, Software, Services), Deployment (On-Premises, Cloud / SaaS), End User (Shipping Companies, Ports & Terminal Operators, Freight Forwarders & Logistics Providers, Defense, Offshore & Energy Operators, Others), and Regional Analysis for 2026 - 2033

Maritime Digitization Market Size and Trends

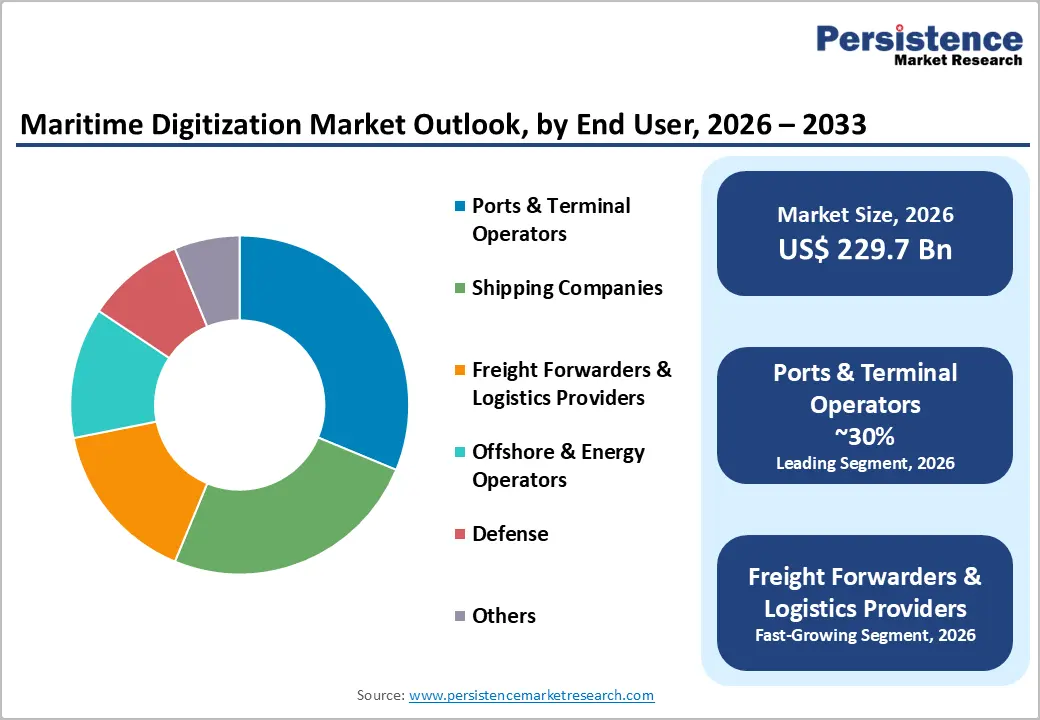

The global maritime digitization market size is projected to rise from US$229.7 Bn in 2026 to US$453.1 Bn by 2033. It is anticipated that the market will grow at a CAGR of 10.2% from 2026 to 2033, driven by the imperative to enhance operational efficiency across global shipping networks.

Escalating regulatory mandates from the International Maritime Organization (IMO), including Resolution MSC.428(98) on cyber risk management and the IACS Unified Requirements E26 and E27, are compelling fleet operators, port authorities, and offshore energy companies to invest heavily in compliant digital infrastructure. The industry's decarbonization agenda, driven by the IMO's greenhouse gas strategy, is catalyzing the adoption of AI-powered fuel-optimization and emissions-monitoring solutions.

Key Industry Highlights:

- Leading Component: Hardware dominates with over 40% market share in 2026, valued at more than US$ 92 Bn, driven by the adoption of IoT-enabled sensors, smart navigation systems, and automation equipment across shipping fleets and ports. Software is the fastest-growing, fueled by integrated fleet management platforms, AI-driven analytics, and predictive maintenance solutions.

- Leading Deployment: On-Premises holds over 47% market share in 2026, valued at more than US$ 108.0 Bn, due to their secure, reliable infrastructure and full control over critical operational data. Cloud/SaaS is the fastest-growing deployment model, providing flexibility, scalability, and cost-effective access for smaller ports and logistics operators.

- Leading End-user: Ports & terminal operators command the largest market share at over 30% in 2026, valued at more than US$ 68.9 Bn, driven by automation, AI-driven scheduling, and IoT-enabled container tracking. Freight forwarders & logistics providers are expanding at a 14.7% CAGR, adopting digital platforms for real-time cargo visibility, route optimization, and supply chain integration.

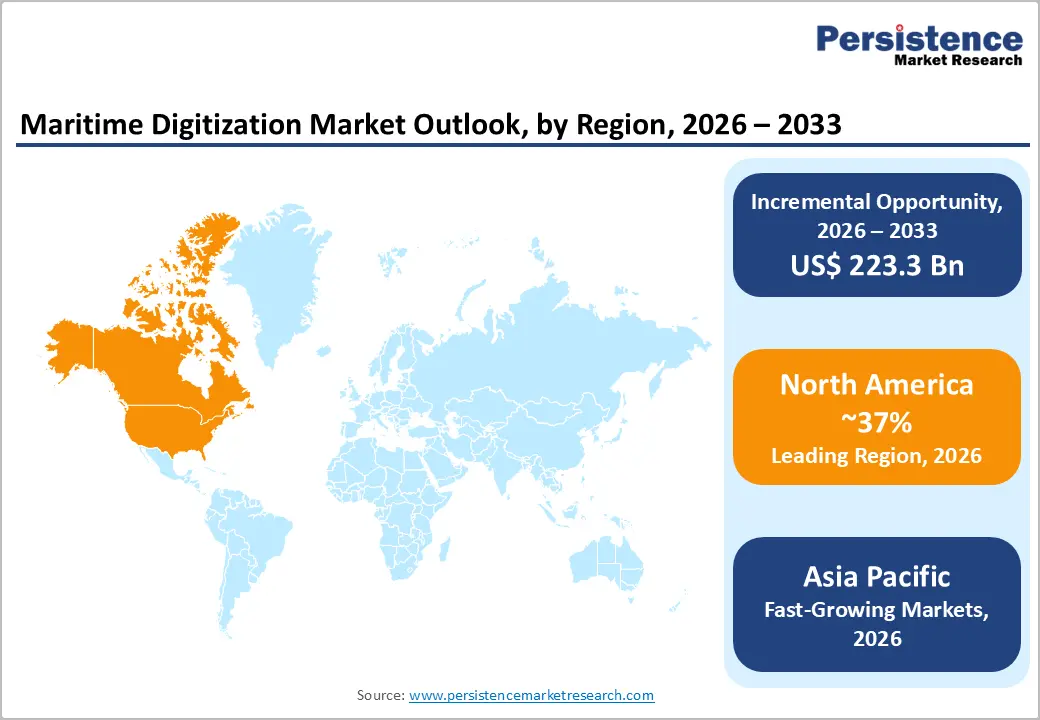

- Leading Region: North America leads with over 37% market share in 2026, valued at US$ 85 Bn, supported by advanced regulatory frameworks, smart port initiatives, and investments in autonomous and AI-powered maritime technologies. Asia Pacific is the fastest-growing region, expected to expand at a CAGR of 15.3%, driven by port modernization, government investments, and adoption of AI, 5G, and predictive analytics.

Market Dynamics

Driver - Regulatory Mandates and IMO Compliance Requirements Driving Digital Adoption

The International Maritime Organization (IMO) mandated integration of cyber risk management into safety management systems under Resolution MSC.428(98), effective January 1, 2021, compelling shipowners worldwide to upgrade legacy IT and OT infrastructure. The European Union's NIS2 Directive, transposed into national law by October 2024, obligates major ports and shipping companies to establish robust cybersecurity governance structures and report critical cyber incidents. These regulations are triggering multi-billion-dollar investments in digital solutions, spanning onboard software systems, fleet monitoring platforms, and secure communication infrastructure.

Rising Seaborne Trade and Demand for Operational Efficiency and Decarbonization

According to the Review of Maritime Transport 2025 report, maritime trade volumes reached 12,720 million tons in 2024, up 2.2%, with ton-miles increasing due to longer shipping routes triggered by disruptions at the Suez and Panama Canals. This surge in trade volumes is driving demand for real-time fleet tracking, predictive maintenance, and voyage-optimization tools.

Shipping accounts for approximately 3% of global greenhouse gas emissions, according to UNCTAD, and the IMO's net-zero strategy is pushing operators to adopt digital fuel management and carbon-intensity monitoring platforms. Technology providers are enabling real-time AI-powered engine performance monitoring and fleet optimization to help shipping companies meet CII compliance targets, EU ETS obligations, and FuelEU Maritime regulations, making digitization inseparable from commercial viability.

Restraint - Rise in Cybersecurity Vulnerabilities Threatening Operational Technology Systems

As maritime assets become progressively interconnected, their vulnerability to cyberattacks has increased substantially. The International Chamber of Shipping (ICS) Maritime Barometer Report flagged technologically driven attacks against shipping, ports, and navigation systems as a distinct possibility, citing a state-sponsored attack on Viasat in February 2022 that disrupted satellite communications across maritime networks.

Many vessels still rely on legacy Operational Technology (OT) systems originally designed without internet connectivity, creating critical security gaps as digitization expands. These cybersecurity risks are complicating the adoption of digitization, particularly among smaller shipping companies and regional port authorities with limited IT security budgets and expertise.

High Capital Investment Requirements and Fragmented Interoperability Standards

The upfront capital expenditure required for maritime digitization remains prohibitively high for a significant segment of the industry, especially aging fleets operating on thin margins. According to a study, around 20% of new tonnage ordered in 2025 was alternative fuel-ready, highlighting the industry's broader challenge of fleet renewal amid financial constraints. Layered on this is a lack of universal interoperability standards across ship management software, port operating systems, and logistics platforms, which creates complex integration and additional cost. Competing proprietary ecosystems from leading vendors fragment the technology landscape, discouraging smaller operators from committing to comprehensive digital programs and slowing market penetration beyond Tier-1 shipping companies.

Opportunity - Expansion of Smart Ports and Digital Terminals

Ports worldwide are investing in automation technologies that integrate AI-driven logistics, blockchain-based documentation, and robotics for container handling. Smart port initiatives enhance throughput, reduce vessel turnaround time, and optimize supply chain coordination. With global trade volumes expected to rise, ports in the Asia Pacific and the Middle East are deploying advanced terminal operating systems and predictive analytics to manage congestion. The move toward digital twins of port infrastructure provides predictive insights into infrastructure stress and logistics bottlenecks, promising future growth for providers of advanced digital solutions.

Predictive Maintenance and AI-Driven Analytics

Predictive maintenance, driven by AI and machine learning, offers substantial value to shipowners and operators by minimizing unplanned downtime and optimizing maintenance schedules. Digital platforms that analyze sensor data can forecast equipment failures weeks in advance, enabling proactive servicing and reducing life-cycle costs. As data from fleets proliferates, analytics platforms become more accurate and valuable. The application of AI in maritime digitization not only enhances reliability but also supports energy-saving strategies and route optimization, positioning AI-driven analytics as a growth frontier for solution providers.

Category-wise Analysis

Component Insights

Hardware dominates the market, capturing more than 40% market share in 2026 with a value exceeding US$ 92 Bn, due to increasing adoption of IoT-enabled sensors, smart navigation systems, and automation equipment across shipping fleets and ports. Ships and terminals are modernizing infrastructure to improve operational efficiency, safety, and compliance with international maritime regulations. The growing need for real-time monitoring, predictive maintenance, and digital twin solutions further fuels hardware investments. As vessels integrate more advanced tracking and communication devices, hardware continues to play a critical role in maritime digitization.

Software is expected to grow rapidly as demand for integrated fleet management platforms, cargo tracking solutions, and analytics tools surges. Shipping operators are increasingly relying on software for predictive analytics, route optimization, and compliance management. Cloud-based analytics, AI-driven decision support systems, and automated reporting software are enabling faster, data-driven operations. The need to enhance operational efficiency, reduce fuel consumption, and ensure regulatory compliance is pushing software adoption at an accelerated pace.

Deployment Insights

On-Premises holds over 47% market share in 2026, with a value exceeding US$ 108.0 Bn, driven by companies' need for secure, reliable systems with full control over critical operational data. It ensures high data privacy, minimal dependency on internet connectivity, and seamless integration with existing IT infrastructure. Companies with long-term digital investment strategies often prefer on-premises systems to customize workflows and maintain operational continuity. The need for stringent cybersecurity and low-latency processing continues to drive demand for on-premises deployment.

Cloud / SaaS is expected to grow rapidly due to its flexibility, scalability, and cost-effectiveness. Smaller ports and logistics companies are adopting cloud platforms to reduce upfront infrastructure costs and accelerate digital transformation. SaaS solutions enable remote access to fleet and terminal data, real-time collaboration, and integration with external supply chain partners. The need for operational agility, quick deployment, and continuous software updates is encouraging businesses to migrate to cloud-based maritime digitization platforms.

End-user Insights

Ports & terminal operators command the largest market share at over 30% in 2026, with a value exceeding US$ 68.9 Bn. Their need for automation, efficient cargo handling, and enhanced terminal throughput is driving the adoption of digitization solutions. Advanced terminal operating systems, AI-driven scheduling, and IoT-enabled container tracking help minimize delays and reduce operational costs. The emphasis on safety, environmental compliance, and predictive maintenance further fuels investment. Digitization allows operators to streamline port processes while offering transparency to shipping lines and stakeholders.

Freight Forwarders & Logistics Providers are expected to grow at a CAGR of 14.7%, driven by the increasing need for real-time cargo visibility, route optimization, and supply chain integration. As global trade volumes expand, these users rely on digital platforms to monitor shipments, manage documentation, and ensure timely deliveries. Cloud-based solutions and mobile applications allow smaller operators to access advanced tools without heavy infrastructure investment. The push for customer satisfaction, compliance, and cost efficiency makes maritime digitization increasingly critical for logistics providers.

Regional Insights

North America Maritime Digitization Market Trends

North America holds over 37% share in 2026, reaching US$ 85 Bn value, led by the United States, driven by advanced regulatory frameworks, defense investment, and technology innovation. The USCG maritime cybersecurity rule, effective July 16, 2025, mandates phased compliance for vessels and ports, boosting demand for digital compliance and cybersecurity solutions. Major technology companies support AI, IoT, and the development of autonomous vessels. Growing investments in autonomous defense vessels and advanced naval surveillance, combined with smart port initiatives at the Port of Los Angeles and Port of Long Beach, reinforce the region’s leadership in integrated maritime digital solutions.

Asia Pacific Maritime Digitization Market Trends

Asia Pacific is expected to grow at a significant rate, with a CAGR of 15.3%, driven by expanding trade volumes, rapid port modernization, and strong government investment. China’s coastal ports are deploying AI-driven logistics platforms, integrated terminal operating systems, and 5G connectivity to handle massive cargo throughput.

Japan’s maritime industry focuses on autonomous navigation technologies and smart vessel systems to improve safety and efficiency in busy sea lanes. India’s major ports are adopting digital customs processing, electronic documentation, and predictive analytics to facilitate trade and integrate supply chains. Singapore and Malaysia are developing smart port frameworks and digital logistics corridors, supported by public-private partnerships and technology investments.

Europe Maritime Digitization Market Trends

Europe is expected to hold more than 25% share by 2026, supported by strong regulatory harmonization and concentrated maritime activity across Norway, Germany, the UK, Finland, and Greece. The EU NIS2 Directive, the FuelEU Maritime Regulation, and the EU Emissions Trading System require shipping companies and ports to invest in compliance reporting, emissions monitoring, and cybersecurity infrastructure.

The United Kingdom and France are investing in AI-powered analytics for predictive maintenance and operational risk management, while Spain focuses on smart port initiatives to manage Mediterranean trade flows. Innovation hubs in Norway and Finland supply navigation, automation, and sustainability solutions, while the Port of Rotterdam develops digital infrastructure for carbon capture and sustainable bunkering, linking digitization with decarbonization goals.

Competitive Landscape

The global maritime digitization market exhibits a moderately consolidated structure at the top tier, with established leaders commanding significant revenue shares through deeply integrated product ecosystems. These incumbents are increasingly pursuing vertical integration and strategic acquisitions to build end-to-end digital maritime platforms.

Key competitive differentiators include real-time AI analytics capabilities, regulatory compliance coverage, global service network reach, and interoperability with third-party systems. Emerging business models include outcome-based SaaS contracts, digital twin subscriptions, and performance-based lifecycle agreements that align vendor revenues with operator efficiency gains.

Key Developments:

- In December 2025, BIMCO launched the Maritime Digitalization Network, a collaborative platform to accelerate digital transformation in the shipping industry. The network enables stakeholders to share experiences, adopt digital solutions, and improve efficiency through technologies like electronic documentation, voyage optimization, and data-driven operations.

- In January 2025, Kongsberg Digital will be integrated into Kongsberg Maritime to consolidate its digital solutions within the broader maritime operations portfolio. This move aims to strengthen digital offerings for fleet optimization, data analytics, and operational intelligence, reflecting the industry’s growing focus on maritime digitization and decarbonization.

Companies Covered in Maritime Digitization Market

- ABB

- Kongsberg Gruppen

- Wärtsilä

- Siemens

- Emerson Electric

- Thales Group

- Lockheed Martin

- ORBCOMM

- DNV

- NAPA

- MariApps Marine Solutions

- Navis

- IBM

- Cisco Systems

- ABS Group

- Bureau Veritas

- Others

Frequently Asked Questions

The global maritime digitization market is projected to be valued at US$229.7 Bn in 2026.

The need for enhanced operational efficiency, regulatory compliance, and cybersecurity, as shipping companies and ports adopt digital solutions to optimize fleet management, navigation, and safety are key driver of the market.

The market is expected to witness a CAGR of 10.2% from 2026 to 2033.

Expanding smart shipping solutions, predictive maintenance, and integrated port management systems are creating strong growth opportunities.

ABB, Kongsberg Gruppen, Wärtsilä, Siemens, Emerson Electric, Thales Group, Lockheed Martin, ORBCOMM, DNV are among the leading key players.