- Communication Infrastructure & Services

- Router and Switch Infrastructure Market

Router and Switch Infrastructure Market Size, Share, and Growth Forecast, 2026 - 2033

Router and Switch Infrastructure Market by Router Type (Core Routers, Edge Routers, Others), Switch Type (Managed Switches, Unmanaged Switches, Others), Infrastructure (Network Infrastructure, Others), and Regional Analysis for 2026 - 2033

Router and Switch Infrastructure Market Size and Trends Analysis

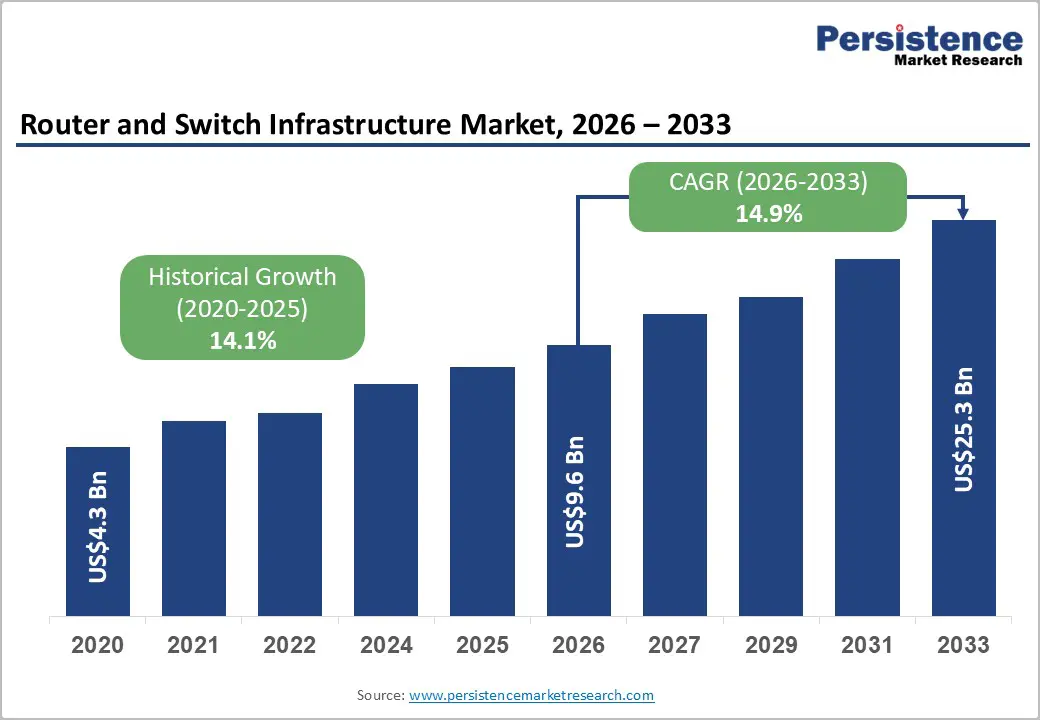

The global router and switch infrastructure market size is likely to be valued at US$9.6 billion in 2026, and is expected to reach US$25.3 billion by 2033, growing at a CAGR of 14.9% during the forecast period from 2026 to 2033, driven by rising global data traffic and the increasing need for advanced networking solutions across enterprises, cloud data centers, telecom networks, and edge computing environments, prompting continuous investment in capacity expansion and technology upgrades.

Key Industry Highlights:

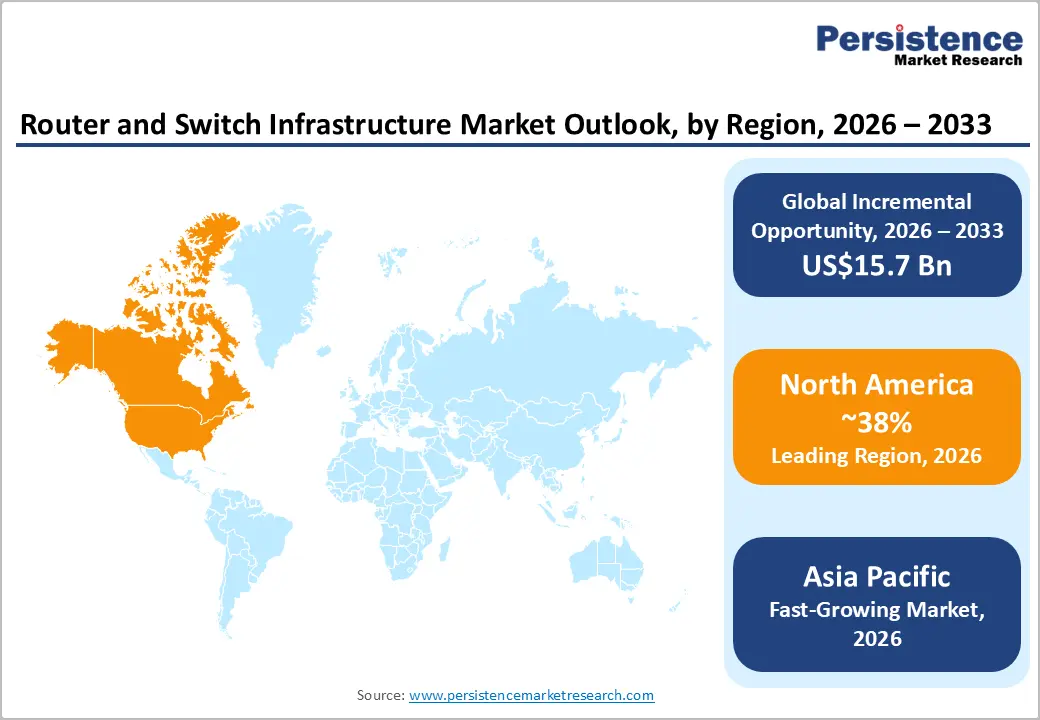

- Dominant Region: North America is projected to dominate with ~38% revenue share in 2026, driven by U.S. hyperscale data center investments, enterprise network modernization, and the presence of key vendors such as Cisco Systems, Juniper Networks, and Arista Networks.

- Fastest-growing Region: Asia-Pacific is the fastest-growing region, driven by 5G expansion in China, digital infrastructure growth in India, rising hyperscale data center investments in Southeast Asia, and rapid enterprise network modernization.

- Dominant Infrastructure: Data center infrastructure is expected to dominate the market with ~35% share in 2026, driven by surging investments in hyperscale, colocation, and enterprise data centers requiring high-performance switching and routing to support AI workloads, cloud delivery, and large-scale application hosting.

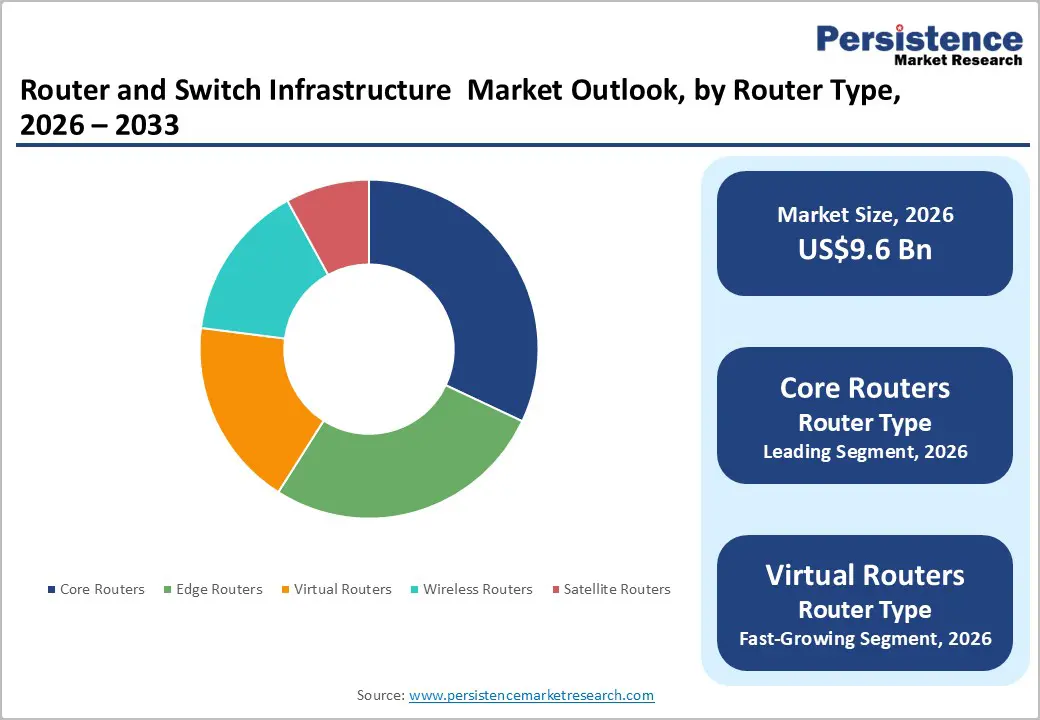

- Leading Router Type: Core routers are expected to dominate with ~32% share in 2026, driven by their role in high-capacity traffic aggregation for carrier and cloud networks, delivering terabit-scale performance and commanding the highest per-unit value in the routing market.

DRO Analysis

Driver - 5G Rollout & Telecom Modernization Drive Router and Switch Demand

The global 5G network rollout represents the major growth driver, with telecommunications operators worldwide investing hundreds of billions of dollars in 5G radio access network (RAN) deployment, core network transformation, and transport network modernization that requires extensive new router and switch infrastructure at every tier of the network architecture, from metro edge aggregation through regional routing to national backbone.

The Global System for Mobile Communications Association (GSMA) projects that 5G connections will grow to 5.5 billion globally by 2030, with network operators investing an estimated US$900 billion cumulatively in 5G infrastructure over the 2020–2030 decade. Each new 5G base station requires packet-based fronthaul and backhaul transport connectivity provided by edge routers and managed switches, while 5G core network functions require new IP routing infrastructure supporting the multi-Gbps throughput and microsecond latency requirements of 5G network slicing. ZTE Corporation and Huawei Technologies are significant beneficiaries of the 5G network equipment procurement wave in Asian markets, while Juniper Networks and Cisco serve telecom operator routing needs in Western markets with their high-performance service provider edge and core routing platforms.

Restraint - Shift to SDN Disrupts Hardware Revenue Models

The accelerating transition to software-defined networking (SDN), network functions virtualization (NFV), and cloud-managed network architectures is creating structural revenue pressure on traditional hardware-centric router and switch business models as virtualization progressively reduces the proportion of network functionality requiring dedicated hardware appliances versus software running on commodity servers or delivered as cloud-managed subscription services.

Cisco, Juniper, and HPE have all invested substantially in transitioning toward higher-software and subscription revenue business models, with Cisco's ARR (Annual Recurring Revenue) exceeding US$27 billion in fiscal 2024, representing the majority of total company revenue, but the transition creates near-term hardware revenue pressure as customers defer physical equipment purchases in favor of subscription or virtual alternatives.

Opportunity - AI-Driven Networking Unlocks Premium Software Value

The integration of artificial intelligence and machine learning into network management and orchestration, enabling intent-based networking, predictive fault management, automated capacity optimization, and AI-driven security threat detection and response, represents a high-value commercial opportunity for router and switch infrastructure vendors to expand per-network revenue by layering AI-powered management software on top of hardware infrastructure.

Cisco's AI-driven network assurance platform (Cisco ThousandEyes, Catalyst Center), Juniper Networks' Mist AI, which delivers AI-driven wireless and wired networking operations with consistently high customer satisfaction metrics, and Arista's CloudVision network management platform collectively demonstrate that AI-augmented network management delivers measurable operational efficiency improvements that justify premium subscription pricing above hardware-only purchase models.

Juniper Networks' Mist AI platform has achieved notable commercial traction, with the company reporting that Mist-managed networks experience significantly lower mean time to resolution for network issues compared to traditionally managed networks, creating quantifiable IT operations cost savings that enterprise network buyers can present as ROI justifications for premium network infrastructure investment.

Category-wise Analysis

Router Type Insights

Core routers are expected to dominate with ~32% share in 2026, fueled by their role in high-capacity traffic aggregation for carrier and cloud networks, delivering terabit-scale performance and commanding the highest per-unit value in the routing market. The Cisco ASR 9000 Series from Cisco Systems delivers multi-terabit capacity (~48 Tbps+) and high-density 100G/400G interfaces, enabling large-scale traffic aggregation for carrier and cloud networks.

Virtual routers are the fastest-growing segment, driven by the shift to software-defined, cloud-native architectures and NFV, replacing dedicated hardware with software-based routing on x86 servers and containerized platforms. Juniper Networks deployed its vMX Virtual Router with South Korean telecom operator LG U+ as part of an NFV-based architecture to support 5G services.

Switch Type Insights

Managed switches are anticipated to dominate with ~40% share in 2026, supported by strong demand for advanced Layer 2/3 features, network control, security, and visibility across enterprise and data center environments. The Cisco 350 Series Managed Switches from Cisco Systems deliver advanced VLAN, QoS, and security features, enabling strong network control, visibility, and performance across enterprise and SMB environments.

PoE switches represent the fastest-growing segment, powered by rising adoption of IP cameras, wireless access points, VoIP devices, and smart building systems requiring power and connectivity over a single Ethernet cable. The TP-Link Omada PoE managed switches (e.g., SG3218XP-M2) are widely used in enterprise and SMB networks to power Wi-Fi access points, IP cameras, and VoIP devices, delivering up to 30W per port and centralized cloud-based management.

Infrastructure Insights

Data center infrastructure is expected to dominate with ~35% share in 2026, fueled by hyperscale cloud expansion, AI-driven high-bandwidth network demand, and ongoing colocation and enterprise data center modernization. Cisco Nexus 9000 Series from Cisco Systems delivers 100G–800G high-bandwidth connectivity and is deployed by enterprises like Workday to build scalable, high-performance cloud data center networks, exemplifying the critical role of data center infrastructure.

Cloud infrastructure is likely to be the fastest-growing segment, propelled by enterprise migration to public cloud and rising demand for high-performance connectivity via SD-WAN, cloud-managed switching, and virtual routing. Cisco Systems’ Cisco SD-WAN (Viptela) enables enterprises to connect branch networks to AWS using virtual routers and automated provisioning, supporting high-performance multi-cloud connectivity and accelerating enterprise cloud migration.

Regional Insights

North America Router and Switch Infrastructure Market Trends

North America market growth is projected to dominate, capturing the 38% of share in 2026, driven by digital-transformation projects, 5G deployment, cloud and hybrid-work adoption, and rising IoT and AI-driven data traffic. The region holds roughly one-third of global router and switch spend, with demand concentrated in high-speed data-center switches, secure enterprise-core gear, and 5G-backhaul and campus-edge platforms.

U.S Router and Switch Infrastructure Market Insights

The U.S. is anticipated to lead by aggressive 5G infrastructure investment, hyperscale-oriented data centers, and strong enterprise-network modernization budgets. Adoption of SDN, NFV, Wi-Fi 6/6E, and AI-ready Ethernet fabrics is pushing upgrades across telecom, cloud, and campus networks, making the U.S. the primary technology-adoption and volume engine.

Canada Router and Switch Infrastructure Market Trends

Canada’s market is growing steadily, supported by 5G and rural-broadband initiatives and rising demand for secure, high-speed enterprise connectivity. Public-sector spectrum releases and smart-city programs are driving campus and carrier-class deployments, positioning Canada as a smaller but structurally expanding node within North American infrastructure investment.

Europe Router and Switch Infrastructure Market Trends

Europe’s market is driven by 5G rollout, hyperscale-data-center growth, and EU-backed digital-infrastructure initiatives such as the Digital Decade and Horizon Europe programs. Demand is concentrated in high-speed Ethernet switches, 5G-backhaul routers, and cloud-managed campus networks, with cybersecurity, energy-efficient gear, and AI-enabled network automation reshaping procurement preferences across public and private sectors.

Germany Router and Switch Infrastructure Market Trends

Germany is expected to dominate Europe’s market by value, powered by Industry 4.0, industrial IoT, and smart-city investments. Enterprises and critical-infrastructure operators are upgrading to high-performance, secure networking gear to support real-time automation, edge computing, and 5G-enabled factories, making Germany the core technology-adoption and scale node in the region.

U.K. Router and Switch Infrastructure Market Trends

The U.K. is one of Europe’s largest, with strong mid-single digit growth underpinned by 5G deployment, financial services, and media sector upgrades, and rising demand for secure, cloud-connected enterprise networks. Fintech, co-working hubs, and media production facilities are driving adoption of certified, high-assurance switches and dual router architectures, while energy efficiency and cyber compliance requirements are pushing buyers toward modern, low-power platforms.

Asia Pacific Router and Switch Infrastructure Market Trends

Asia Pacific is likely to be the fastest-growing region, driven by 5G deployment, hyperscale and edge-data-center builds, and national digital-infrastructure programs across China, India, Japan, and Southeast Asia. Rising data traffic from cloud, video, and IoT, together with shorter hardware refresh cycles, is pushing enterprises and service providers to invest in higher-bandwidth, low-latency routers and Ethernet switches.

China Router and Switch Infrastructure Market Trends

China is expected to dominate in Asia Pacific, powered by its “New Infrastructure” plan, nationwide 5G rollout, and dense network of data centers and telecom backbones. Massive government-led investments in information technology and smart-city infrastructure, plus rapidly expanding cloud and enterprise-network demand, make China the core volume and technology-adoption engine for the regional market.

India Router and Switch Infrastructure Market Trends

India is one of the fastest growing router and switch nodes, with mid to high single digit CAGR as 4G/5G, “Digital India,” and smart city programs drive broadband and enterprise network expansion. Service providers and enterprises are upgrading to 100G–400 G-ready routers and PoE-enabled switches for campuses, ISPs, and edge sites, turning India into a key growth frontier for Asia Pacific routing and switching infrastructure.

Competitive Landscape

The global router and switch infrastructure market is dominated by Cisco Systems, supported by its vast installed base, end-to-end portfolio across enterprise, data center, and service provider networks, and a strong transition toward high-margin software and subscription platforms such as IOS XE, NX-OS, Meraki, and ThousandEyes.

Juniper Networks maintains a solid position in carrier-grade routing and data center networking, differentiated by its Junos OS and AI-driven Mist platform that enhances automation and operational efficiency. Arista Networks continues to gain significant traction in hyperscale data center and AI networking, leveraging its EOS platform’s programmability, stability, and cloud-native design to attract large cloud and enterprise customers.

Key Industry Developments:

- In March 2026, Juniper Networks introduced the PTX12000 series modular routers, delivering 800GE throughput and ultra-high density in 1.6T-ready platforms to support AI data center scale, with a power- and space-efficient design for next-generation interconnect demands.

- In February 2026, Cisco Systems launched a new chip and router to accelerate data flow in AI data centers, targeting the rapidly expanding AI infrastructure market and competing with Broadcom and NVIDIA. Its Silicon One G300 chip, built on TSMC’s 3nm process, is set for release in the second half of the year and improves AI workload performance by up to 28% through microsecond-level data rerouting.

Companies Covered in Router and Switch Infrastructure Market

- Cisco Systems

- Juniper Networks

- Arista Networks

- Hewlett-Packard Enterprise

- Huawei Technologies

- Dell Technologies

- Extreme Networks

- NETGEAR

- TP-Link

- Mikrotik

- ZTE Corporation

Frequently Asked Questions

The global router and switch infrastructure market is projected to reach US$9.6 billion in 2026.

The router and switch infrastructure market is driven by surging AI workloads requiring high-bandwidth, ultra-low-latency data center networks, alongside global 5G rollout fueling large-scale telecom routing and switching investments across core, transport, and edge networks.

The router and switch infrastructure market is poised to witness a CAGR of 14.9% from 2026 to 2033.

Key opportunities include AI-driven automation and intent-based networking driving premium software value, edge computing and industrial IoT expanding demand in new environments, and private 5G enabling convergence between enterprise and telecom networks across industrial and campus deployments.

Key players include Cisco Systems, Juniper Networks, Arista Networks, Hewlett Packard Enterprise, Huawei Technologies, Dell Technologies, Extreme Networks, NETGEAR, TP-Link, Mikrotik, and ZTE Corporation.