- Industrial Machinery

- Sludge Dewatering Equipment Market

Sludge Dewatering Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Sludge Dewatering Equipment Market by Technology (Centrifuges, Screw Press, Others), Application (Municipal Wastewater, Food & Beverage, Others), Sludge Source, and Regional Analysis for 2026 - 2033

Sludge Dewatering Equipment Market Size and Trends Analysis

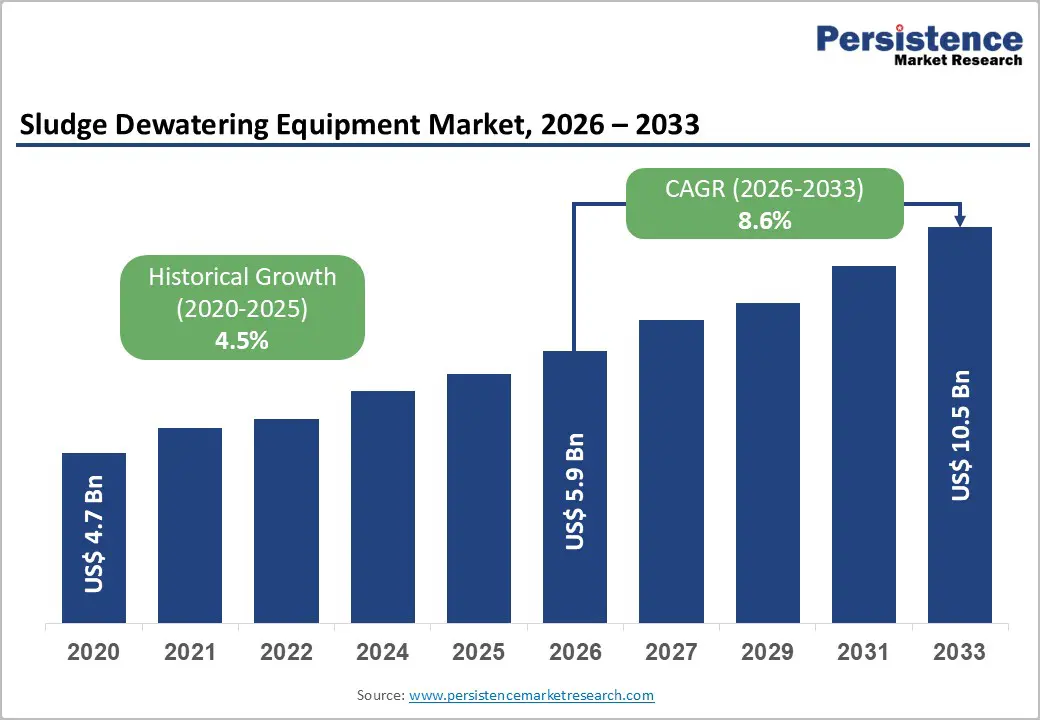

The global sludge dewatering equipment market size is likely to be valued at US$5.9 billion in 2026 and is expected to reach US$10.5 billion by 2033, growing at a CAGR of 8.6% between 2026 and 2033, driven by tightening environmental regulations, increasing wastewater generation from urban and industrial sources, and the transition toward resource recovery-oriented treatment systems.

Regulatory frameworks in developed regions and infrastructure expansion in emerging economies are accelerating equipment adoption. Technological advancements in automation and energy efficiency are improving operational economics, strengthening long-term demand for advanced dewatering solutions.

Key Industry Highlights:

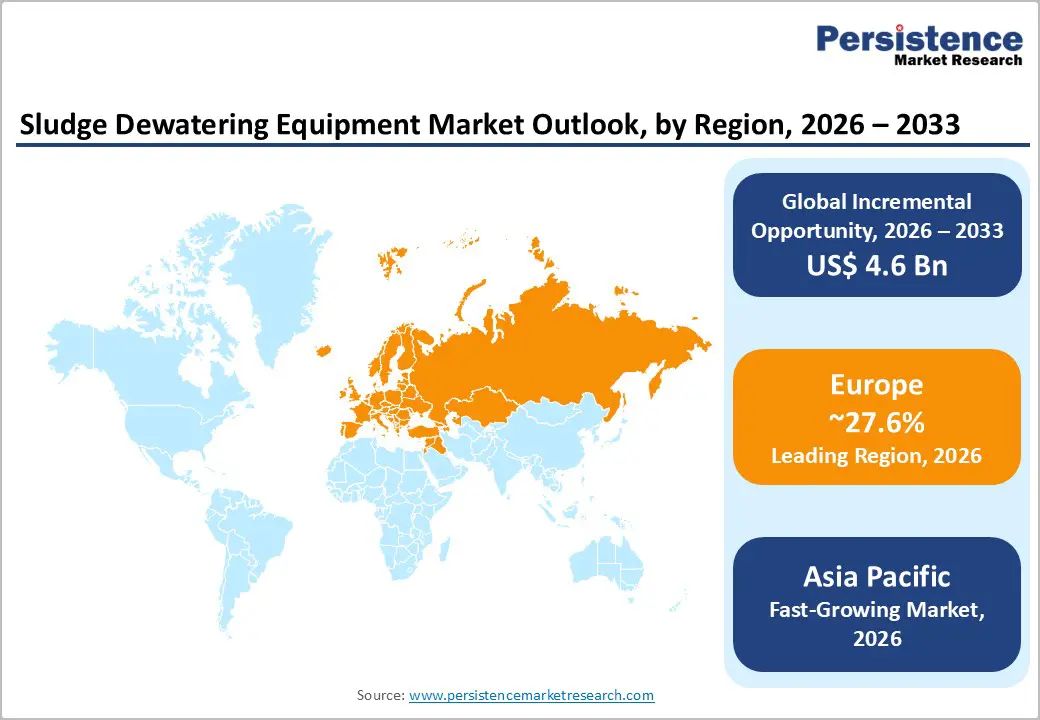

- Leading Region: Europe is projected to account for 27.6% of the market share, supported by stringent environmental regulations and strong investment in advanced wastewater treatment infrastructure.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization and industrial expansion, and is projected to grow at a high CAGR during the forecast period.

- Investment Plans: Global investments are increasingly directed toward wastewater infrastructure modernization and digital upgrades, with a strong focus on automation, energy efficiency, and resource recovery, contributing to steady capital inflow across municipal and industrial sectors.

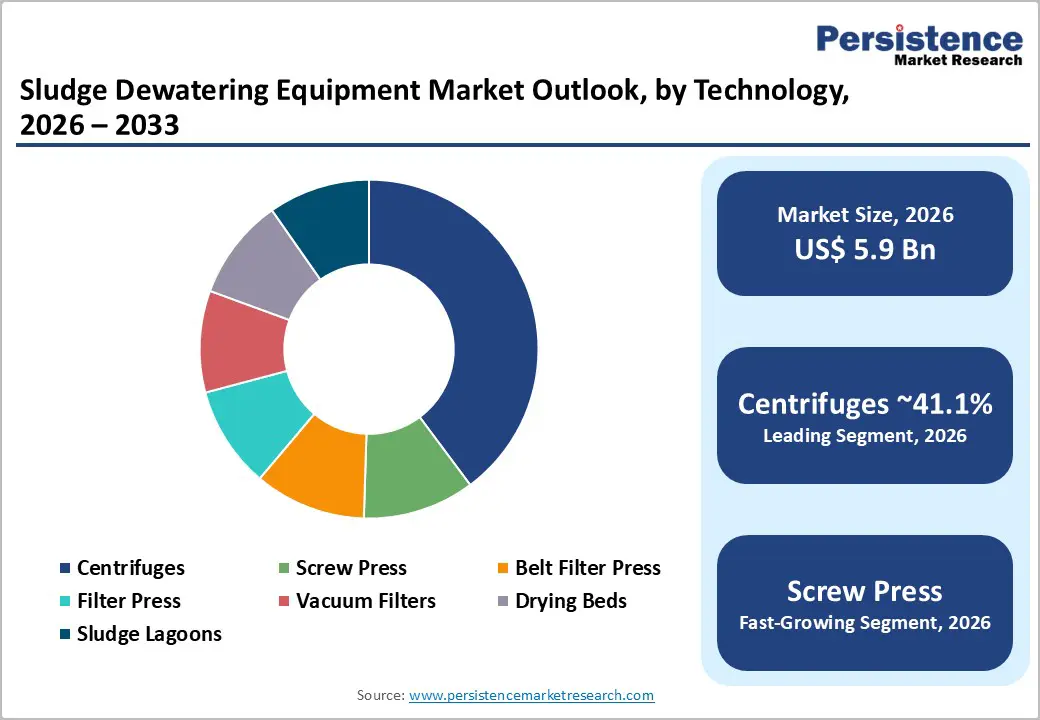

- Dominant Technology: Centrifuges dominate the market with an anticipated 41.1% share, owing to their high efficiency, continuous operation, and suitability for large-scale wastewater treatment applications.

- Leading Application: Municipal wastewater treatment holds the leading position with an anticipated 55.2% market share, driven by consistent sludge generation, regulatory compliance requirements, and ongoing infrastructure upgrades.

| Key Insights | Details |

|---|---|

| Sludge Dewatering Equipment Market Size (2026E) | US$5.9 Bn |

| Market Value Forecast (2033F) | US$10.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

DRO Analysis

Driver Analysis - Stringent Environmental Regulations Driving Equipment Adoption

Regulatory enforcement related to sludge treatment and disposal remains a critical demand driver. In the U.S., biosolids management regulations mandate strict compliance for land application, incineration, and landfill disposal. In Europe, updated wastewater treatment regulations require enhanced nutrient removal and improved treatment performance standards over the coming decades. These regulatory frameworks compel utilities and industrial operators to invest in efficient sludge dewatering technologies to reduce sludge volume, minimize transportation costs, and meet environmental discharge standards. The direct market impact includes increased demand for high-performance equipment, particularly in retrofit projects where existing systems require upgrades to comply with evolving regulations.

Rising Wastewater Volumes and Urban Infrastructure Expansion

Rapid urbanization, industrialization, and population growth are significantly increasing wastewater generation globally. Emerging economies in the Asia Pacific and Latin America are investing heavily in wastewater treatment infrastructure to address sanitation challenges and environmental concerns. Urban population growth is placing additional pressure on existing treatment facilities, necessitating capacity expansion and modernization. This trend directly increases demand for sludge-handling and dewatering systems. The need for compact, scalable, and energy-efficient equipment is particularly strong in densely populated urban areas where space constraints and operational efficiency are critical considerations.

Shift toward Resource Recovery and Process Optimization

The wastewater treatment industry is evolving toward a circular economy model, where sludge is increasingly viewed as a resource rather than waste. Dewatering plays a critical role in enabling downstream processes such as energy recovery, nutrient extraction, and reuse applications. Technological advancements, including automation, real-time monitoring, and process optimization tools, are improving system efficiency and reducing operating costs. Equipment manufacturers are integrating smart control systems to enhance performance consistency and reduce manual intervention. This shift is influencing purchasing decisions, with end users prioritizing lifecycle costs, energy consumption, and operational reliability over initial capital expenditure.

Restraint Analysis - High Capital Investment and Operational Cost Challenges

Sludge dewatering equipment requires substantial upfront investment, particularly for advanced technologies such as centrifuges and thermal drying systems. Operating costs, including energy consumption, polymer usage, maintenance, and skilled labor, further add to the financial burden. The economic viability of these systems often depends on achieving optimal dryness levels to reduce disposal costs. For small municipalities and mid-sized industrial facilities, these cost factors can delay or limit adoption. Budget constraints and limited access to financing remain key barriers, particularly in developing regions.

Regulatory and Operational Complexity across Regions

Variations in regulatory frameworks across regions create challenges for standardization and equipment deployment. Differences in sludge classification, disposal methods, and environmental compliance requirements necessitate customized solutions for each market. This increases engineering complexity, project timelines, and overall costs for equipment suppliers. Industrial wastewater treatment adds another layer of complexity due to diverse sludge characteristics and sector-specific regulations. These factors can slow down decision-making processes and hinder the scalability of standardized dewatering solutions.

Opportunity Analysis - Growth in Digital and Retrofit Solutions

A significant opportunity lies in upgrading existing wastewater treatment facilities with digital monitoring and optimization technologies. Many installed dewatering systems can achieve improved performance through retrofits rather than full replacement, making this a cost-effective pathway for operators facing budget constraints. The integration of sensors, automation platforms, and advanced data analytics enables real-time process control, improving cake dryness consistency and reducing operational variability. These enhancements directly contribute to lower energy consumption, optimized polymer dosing, and reduced sludge disposal costs. For equipment manufacturers, this shift supports a transition toward recurring revenue models, including long-term service agreements, predictive maintenance, and performance-based contracts, strengthening customer retention and lifecycle value.

Expansion in High-Value Industrial Applications

Industries such as food and beverage, pharmaceuticals, and specialty chemicals are increasingly investing in advanced wastewater treatment solutions to meet stringent hygiene and environmental standards. These sectors generate complex wastewater streams with high organic loads, requiring precise and reliable dewatering processes. As a result, sludge dewatering systems tailored for these industries often command premium pricing due to specialized design requirements, such as corrosion resistance, hygienic construction, and closed-loop operation. The rising emphasis on water reuse, zero-liquid discharge (ZLD) systems, and sustainability targets is further accelerating adoption. This creates opportunities for vendors to offer customized, high-margin solutions that integrate seamlessly with broader industrial water management systems.

Emerging Market Infrastructure Development

Developing regions, particularly in the Asia Pacific, present substantial growth opportunities due to ongoing investments in wastewater infrastructure and sanitation programs. Rapid urbanization and industrial expansion are driving the need for new treatment facilities and upgrades to existing systems. Governments and private stakeholders are prioritizing environmental protection and public health, leading to increased funding and policy support for wastewater management projects. In these markets, modular, scalable, and cost-efficient dewatering solutions are gaining traction due to their ease of installation and lower upfront investment requirements. Companies that establish localized manufacturing, supply chains, and after-sales service networks can significantly improve competitiveness, enabling faster project execution and better alignment with region-specific regulatory and operational needs.

Category-wise Analysis

Technology Insights

Centrifuges are expected to dominate the market, with an anticipated 41.1% share in 2026, due to their ability to handle large volumes of sludge, operate continuously and achieve high efficiency. These systems are widely deployed in municipal wastewater treatment plants and heavy industrial facilities where process reliability, automation, and high throughput are critical. Their compact footprint and capability to achieve higher cake solids (typically 18-25% depending on sludge type) make them ideal for large-scale operations aiming to reduce sludge transportation and disposal costs.

For example, large metropolitan treatment plants in North America and Europe widely use decanter centrifuges to efficiently manage daily sludge loads, while industries such as pulp & paper and oil refining rely on centrifuges for consistent separation performance. Their integration with SCADA systems and real-time monitoring tools further enhances process optimization. As utilities continue to modernize infrastructure, centrifuges are expected to retain dominance due to their scalability and compatibility with advanced automation systems.

Screw press emerges as the fastest-growing segment, driven by its low energy consumption, reduced polymer requirements, and simplified mechanical design. These systems are particularly well-suited for small to medium-sized treatment plants, decentralized wastewater facilities, and industrial units with moderate sludge volumes. Their enclosed structure minimizes odor emissions and noise levels, making them highly suitable for installations in urban or space-constrained environments.

For instance, municipal plants in Japan and Southeast Asia increasingly deploy screw presses for decentralized sewage treatment, while food processing units use them to handle organic sludge at lower operating costs. Additionally, their ability to operate with minimal supervision makes them attractive in regions facing skilled labor shortages. As end-users increasingly prioritize total cost of ownership and operational simplicity, screw presses are expected to see accelerated adoption across both municipal and industrial sectors.

Application Insights

Municipal wastewater is expected to lead with an anticipated 55.2% market share in 2026, driven by the ongoing, large-scale generation of sludge and stringent environmental regulations. Urban treatment facilities require efficient dewatering systems to reduce sludge volume, lower transportation costs, and ensure compliance with disposal standards. The scale of operations in major cities demands high-capacity and reliable equipment, making centrifuges and belt filter presses commonly deployed solutions.

For example, large wastewater treatment plants in cities such as New York, London, and Tokyo rely on advanced dewatering systems to manage millions of gallons of wastewater daily. Ongoing investments in upgrading aging infrastructure in developed regions, along with new plant construction in developing economies, are sustaining strong demand. The increasing focus on biosolids reuse and energy recovery is further strengthening the role of dewatering systems in municipal operations.

The food and beverage industry is emerging as the fastest-growing application segment, driven by increasing emphasis on water reuse, waste minimization, and sustainability compliance. Wastewater generated from dairy processing, breweries, sugar refining, and beverage production contains high organic loads, requiring efficient sludge separation and handling. For instance, breweries and dairy plants are adopting advanced centrifuge and screw press systems to reduce waste disposal costs and recover usable water for secondary processes.

Many facilities are also integrating dewatering systems with anaerobic digestion units to generate biogas, enhancing overall resource efficiency. The demand for hygienic, corrosion-resistant, and closed-loop systems is particularly strong in this sector. As sustainability regulations tighten and corporate ESG goals gain importance, the adoption of advanced dewatering technologies in food and beverage applications is expected to accelerate significantly.

Regional Insights

North America Sludge Dewatering Equipment Market Trends - Infrastructure Upgrades Driving High-Efficiency and Service-Based Dewatering Solutions

North America remains a mature and technologically advanced market for sludge dewatering equipment. The region benefits from well-established wastewater treatment infrastructure and stringent environmental regulations governing sludge disposal. The U.S. leads the market, driven by continuous upgrades to aging infrastructure and the need to comply with biosolids management standards. High sludge transportation and landfill costs are encouraging utilities to adopt higher-efficiency dewatering systems such as centrifuges and advanced belt filter presses. For example, companies such as Xylem Inc. and Centrisys Corporation have been actively supporting municipal upgrades through high-performance decanter centrifuge installations and service-based offerings, helping utilities improve cake dryness and reduce lifecycle costs.

The region also demonstrates strong innovation capabilities, with manufacturers focusing on automation, digital monitoring, and energy-efficient solutions. GEA Group has introduced advanced process optimization technologies, including real-time monitoring systems that enhance operational efficiency and reduce energy consumption.

Similarly, Komline-Sanderson continues to expand its screw press and drying solutions portfolio tailored for both municipal and industrial clients. Service-based business models, including leasing, retrofits, and long-term maintenance contracts, are gaining traction. These developments are shifting the competitive landscape toward performance-based solutions and lifecycle service models, supporting long-term market stability.

Europe Sludge Dewatering Equipment Market Trends - Circular Economy Policies Advancing Sludge-to-Energy and Resource Recovery Systems

Europe is expected to lead with a 27.6% market share in 2026, supported by strict environmental policies and a strong emphasis on sustainability and circular economy principles. Countries such as Germany, the U.K., France, and Spain play a central role in driving market demand. The region’s regulatory frameworks prioritize nutrient removal, sludge minimization, and safe disposal, thereby increasing the need for efficient dewatering technologies.

Recent developments highlight this trend. ANDRITZ AG secured projects related to sludge treatment and incineration systems in Germany, reflecting growing investment in sludge-to-energy infrastructure. Similarly, Veolia Water Technologies and SUEZ are actively deploying integrated wastewater treatment and resource recovery solutions across France and other European markets. These projects often combine dewatering with energy recovery and phosphorus recycling, aligning with EU sustainability goals.

The region’s mature market structure encourages continuous innovation, with companies such as HUBER SE and Flottweg SE focusing on energy-efficient and automated systems. As a result, Europe is not only the largest market but also a technology leader, where compliance requirements and sustainability targets are shaping next-generation dewatering solutions.

Asia Pacific Sludge Dewatering Equipment Market Trends - Rapid Wastewater Expansion Fueling Demand for Scalable and Cost-Effective Systems

Asia Pacific is the fastest-growing regional market, driven by rapid urbanization, industrial expansion, and increasing environmental awareness. Countries such as China, India, and Japan are investing heavily in wastewater infrastructure to address rising sanitation challenges and industrial pollution. Government initiatives to improve water quality and expand sewage treatment capacity are significantly boosting demand for sludge dewatering equipment.

For example, China’s large-scale wastewater treatment expansion projects have created strong demand for high-capacity centrifuges and filter presses, with global players such as Alfa Laval and ANDRITZ AG actively supplying equipment for municipal and industrial facilities. In Japan, AMCON Inc. has seen increased adoption of its screw press systems, particularly in decentralized and compact treatment plants. Meanwhile, in India, infrastructure programs such as urban sanitation and river-cleaning initiatives are driving installations of modular and cost-effective dewatering systems across municipal treatment plants.

The region presents strong opportunities for both new installations and retrofitting projects. Cost-effective, modular, and easy-to-operate systems are particularly in demand due to budget constraints and varying infrastructure maturity levels. Companies that invest in localized manufacturing, distribution, and service networks are better positioned to capture growth. As a result, Asia Pacific is evolving into a high-volume, high-growth market where affordability, scalability, and operational efficiency are key competitive factors.

Competitive Landscape

The global sludge dewatering equipment market is moderately fragmented, with a mix of global engineering companies and regional specialists. Large players dominate high-value municipal and industrial projects, while smaller companies focus on niche applications and localized markets. Competition is driven by technological innovation, product reliability, and service capabilities. Centrifuge-based solutions show relatively higher consolidation compared to other technologies.

Key strategies include technology innovation, energy efficiency improvements, service expansion, and geographic diversification. Companies are focusing on digital solutions, lifecycle services, and modular system designs to enhance customer value and differentiate their offerings in a competitive market.

Key Industry Developments

- In December 2025, ANDRITZ AG commissioned a sludge drying plant for an industrial customer, designed to process up to 22 tons of dry solids per day. The facility converts dried sludge into fuel for power generation, demonstrating the growing adoption of resource recovery and energy reuse solutions in industrial wastewater treatment.

Companies Covered in Sludge Dewatering Equipment Market

- Alfa Laval

- ANDRITZ AG

- Veolia Water Technologies

- SUEZ

- HUBER SE

- GEA Group

- Flottweg SE

- Evoqua Water Technologies

- Komline-Sanderson

- Xylem Inc.

- AMCON Inc.

- Pieralisi Group

- Hitachi Zosen Corporation

- Kurita Water Industries Ltd.

- Centrisys Corporation

- Aqseptence Group

Frequently Asked Questions

The global sludge dewatering equipment market is estimated to be valued at US$5.9 billion in 2026.

The sludge dewatering equipment market is projected to reach US$10.5 billion by 2033.

Key trends include increasing adoption of automation and digital monitoring, growing focus on energy-efficient and low-cost operations, and a shift toward resource recovery and circular economy practices in wastewater treatment.

The centrifuges technology segment leads the market with an anticipated 41.1% share, driven by high efficiency and suitability for large-scale operations.

The sludge dewatering equipment market is expected to grow at a CAGR of 8.6% from 2026 to 2033.

Major players include Alfa Laval, ANDRITZ AG, GEA Group, Veolia Water Technologies, and Xylem Inc.