- Industrial Machinery

- Spinning Machine Market

Spinning Machine Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Spinning Machine Market by Machine Type (Ring Spinning, Rotor Spinning, Others), Fiber Type (Natural Fiber, Synthetic Fiber, Blended Fiber), Industry (Apparel & Fashion Industry, Home Textiles, Industrial Textiles, Miscellaneous), and Region Analysis for 2026 to 2033

Spinning Machine Market Trends & Analysis

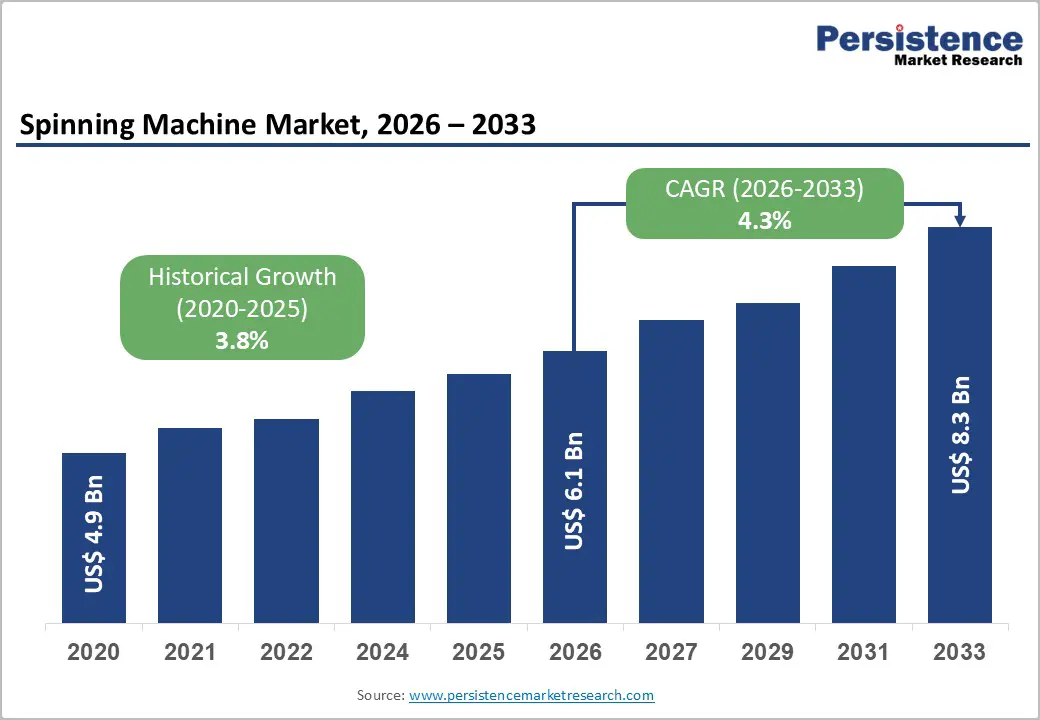

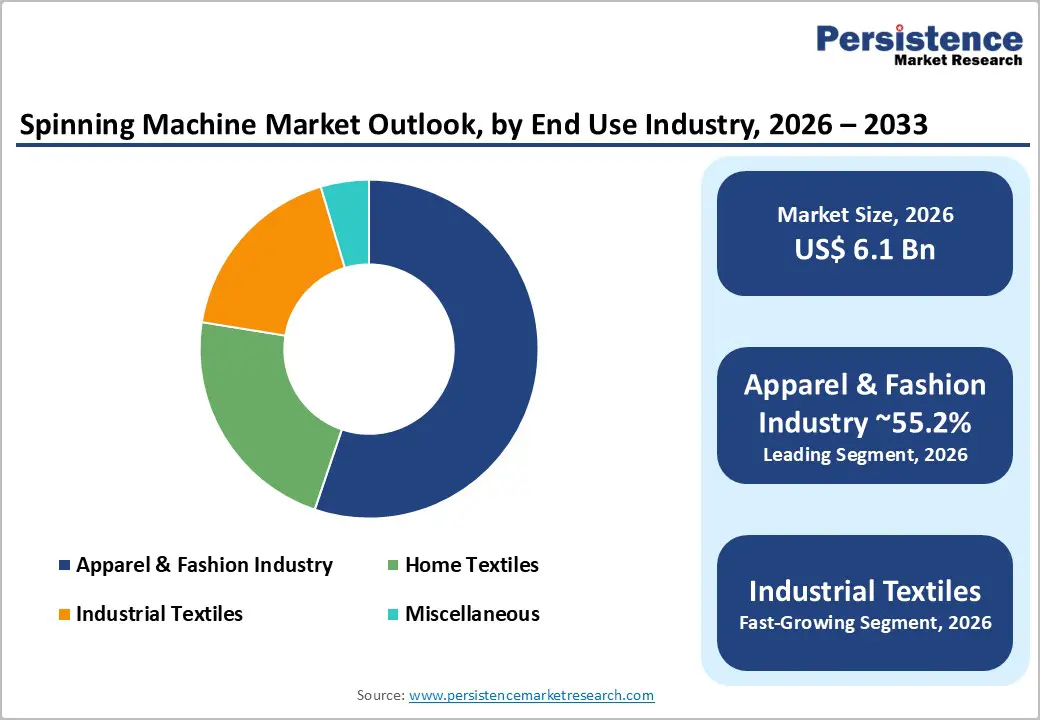

The global spinning machine market size is likely at US$ 6.1 Bn in 2026 and is projected to reach US$ 8.3 Bn by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

Global textile exports exceeded US$ 800 Bn annually by 2024; Asia Pacific textile output expanded 6.2% YoY; industrial textile demand for geotextiles, filtration, and medical fabrics grew 9.1%, while India's PLI-linked textile production investments reached US$ 1.97 Bn in 2023-24, accelerating spinning machine procurement regionally.

Rising demand for technical and industrial textiles, smart automation integration in ring and rotor spinning platforms, and expanding apparel manufacturing capacity across Asia Pacific are primary structural growth drivers.

Key Industry Highlights:

- Leading Machine Type: Ring Spinning leads at 46.9% share; Others (Air-jet, Vortex, Hybrid) grow fastest at 5.7% CAGR, driven by 3-8x higher production speed advantage at MMF and technical textile yarn mills globally.

- Leading Fiber Type: Natural Fiber leads at 42.6% share; Blended Fiber grows fastest at 5.6% CAGR, driven by cotton-polyester and cotton-Tencel performance blend adoption at activewear and sustainable fashion supply chains.

- Leading End Use: Apparel & Fashion leads at 55.2% share; Industrial Textiles grows fastest at 5.2% CAGR, driven by geotextile, medical textile, and automotive composite yarn demand expansion.

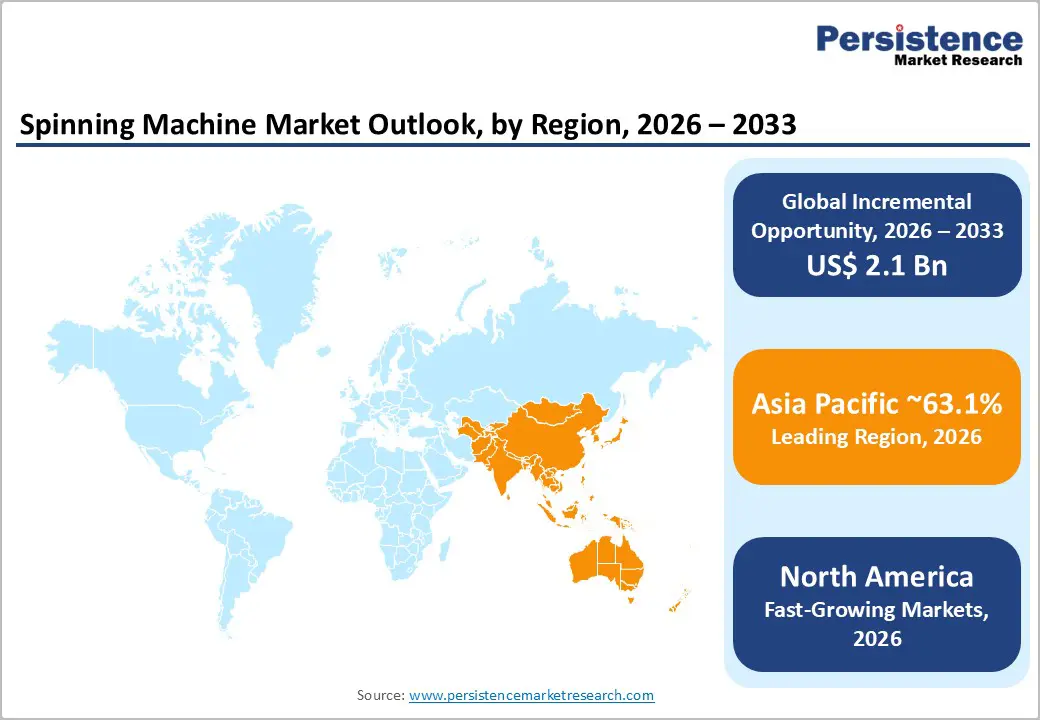

- Regional Leader: Asia Pacific leads at 48.5% share (China US$ 2.4 Bn, India US$ 872.9 Mn); grows fastest at 8.5% CAGR; North America grows at 3.3% CAGR (U.S. US$ 560 Mn) anchored by technical textile modernization.

- Strategic Milestone: Rieter's AI spindle fault detection ESSENTIAL package (January 2025) and LMW's US$ 85 Mn Coimbatore facility expansion (November 2023) signal smart automation and South Asian capacity investment as defining spinning machine market themes.

Market Dynamics Analysis

Drivers - Textile Industry Automation, IoT Integration, and Industry 4.0 Adoption Driving Spinning Machine Technology Upgrades

Global textile machinery capital expenditure exceeded US$ 25 Bn in 2024 (International Textile Manufacturers Federation, ITMF Annual Survey), with Industry 4.0 IoT-enabled spinning machine platforms, integrating real-time yarn quality monitoring sensors, AI-powered spindle fault detection, and automated doffing systems, reducing per-unit production labor requirements by 25-35% and yarn defect rates by 15-20% versus conventional ring spinning configurations at equivalent production throughput.

Rieter's SPIDERweb digital mill monitoring platform and Saurer's Spinner Vision AI quality monitoring system, both commercially deployed across 200+ mills in Asia Pacific and Europe by 2024, exemplify the IoT automation technology investment trend driving spinning machine replacement and upgrade procurement globally.

The ITMF confirmed that 47% of surveyed textile mills globally planned spinning machine automation upgrades between 2024 and 2026, prioritizing compact spinning conversion, automatic piecing, and real-time energy monitoring integration to achieve 12-18% energy cost reduction per kg of yarn produced. China's "Made in China 2025" textile equipment modernization program allocated CNY 8.6 Bn in direct machinery subsidies through 2025, generating structured spinning machine procurement demand at China's ring and rotor spinning mills across Xinjiang, Jiangsu, Zhejiang, and Shandong textile manufacturing provinces.

Growing Technical and Industrial Textile Demand Expanding Spinning Machine Application Scope Beyond Apparel

Global technical textile market output reached US$ 220 Bn in 2024 at 4.8% CAGR (Textile Exchange, Technical Textiles Global Benchmark Report), with geotextiles, medical textiles, protective workwear, automotive nonwovens, and filtration textiles each requiring high-tenacity specialty yarn types produced on modern ring and air-jet spinning platforms capable of processing high-tenacity polyester, aramid, and glass fiber roving at 25,000+ rpm spindle speeds. The European Union's Single-Use Plastics Directive (EU 2019/904) and Extended Producer Responsibility frameworks accelerating bio-based technical textile development are driving demand for spinning machines capable of processing novel fiber types including PLA, Tencel, and recycled polyester blends at commercial production volumes.

India's National Technical Textiles Mission (NTTM), allocating US$ 200 Mn between 2020 and 2026 for technical textile manufacturing capacity expansion, is generating structured spinning machine procurement at Indian mills investing in agro-textiles, medical textiles, and protective textile production lines requiring new ring and air-jet spinning platform installations. Technical textile yarn production's premium average selling price, 40-65% higher per kg versus commodity apparel yarn, provides textile mill operators with strong return-on-investment justification for higher-specification spinning machine capital expenditure across technical textile yarn production programs globally.

Restraints - Skilled Operator Shortage and Machine Technician Availability Constraining Spinning Mill Automation Deployment

The global textile machinery technician workforce faces skills gap estimated at 120,000-150,000 qualified spinning machine maintenance technicians by 2025 (ITMF Workforce Skills Report), with digital automation platforms, IoT spindle monitoring, AI quality control, and automated piecing systems, requiring multi-disciplinary mechatronics expertise unavailable at legacy mill operator skill levels in South Asia and ASEAN manufacturing regions. Machine downtime from inadequate preventive maintenance in mills deploying new automated spinning platforms averages 18-24% of scheduled production hours in emerging market installations, reducing operational ROI for new spinning machine capital investments below anticipated break-even thresholds.

Fiber Supply Chain Volatility and Raw Material Quality Inconsistency Disrupting Spinning Production Planning

Global cotton supply volatility, driven by La Niña weather pattern-induced yield fluctuations affecting US, India, Pakistan, and Uzbekistan production collectively representing 72% of global cotton exports, creates raw material quality inconsistencies that force spinning mill operators to adjust machine settings, spindle speed, and tension parameters 3-8 times per production shift during volatile supply periods. Polyester staple fiber feedstock supply disruptions, linked to PTA/MEG petrochemical feedstock price volatility, created 30-45-day supply delays at synthetic fiber spinning mills in China and India during 2023-2024, constraining spinning machine utilization rates below 78% capacity at affected facilities.

Opportunities - Recycled and Sustainable Fiber Spinning Machine Platform Development for Circular Economy Textile Programs

The global recycled textile fiber market, valued at US$ 5.8 Bn in 2024 at 9.2% CAGR (Textile Exchange, Preferred Fiber & Materials Report), is generating demand for spinning machine platforms capable of processing mechanically recycled cotton, rPET staple fiber, and blended post-consumer waste fibers, where conventional ring spinning configurations require specialized rotor diameter, opening roller, and fiber guide modifications to handle the shorter staple length and higher trash content of recycled fiber inputs. EU Ecodesign Regulation for Textiles (2024), mandating minimum 20% recycled content in textile products by 2030, is creating a regulatory procurement driver for recycled-fiber-capable spinning machine upgrades at European and export-oriented Asian apparel yarn spinning mills servicing EU brand supply chains.

The circular textile spinning machine upgrade opportunity is estimated at US$ 420-580 Mn in addressable retrofit and new equipment investment by 2030, concentrated at Italian, German, Spanish, and South Asian spinning mills supplying EU sustainable fashion brand value chains where Rieter, Saurer, and Trützschler recycled-fiber-optimized spinning platforms command 18-25% premium pricing versus standard spinning machine configurations for equivalent spindle count capacity.

South and Southeast Asian Spinning Capacity Expansion Funded by Government Manufacturing Incentive Programs

India's Production Linked Incentive (PLI) Scheme for Textiles, allocating US$ 1.97 Bn in incentives through 2027, is generating structured spinning machine procurement at new greenfield textile manufacturing facilities targeting man-made fiber (MMF) apparel production, where government incentives require minimum capital investment thresholds that include spinning machine procurement as qualifying capital expenditure. Bangladesh's US$ 4.5 Bn in annual textile FDI and Vietnam's US$ 7.8 Bn in textile export capacity expansion investments between 2022 and 2026, attracting EU and U.S. apparel brand supply chain diversification away from China, are generating both greenfield and capacity-expansion spinning machine procurement demand across South and Southeast Asian textile manufacturing corridors.

Combined, India, Bangladesh, Vietnam, Indonesia, and Pakistan represent an estimated US$ 1.2-1.6 Bn in incremental annual spinning machine procurement through 2030, concentrated in ring spinning, compact spinning, and rotor spinning platforms for cotton, MMF, and blended yarn production targeting global fast fashion, premium apparel, and home textile export supply chains requiring OEKO-TEX and GOTS-certified yarn manufacturing capability.

Category-wise Analysis

Machine Type Insights

Ring Spinning leads the machine type segment with a 46.9% market share in 2026, estimated at approximately US$ 2.88 Bn, driven by its unmatched versatility across cotton, MMF, and blended fiber processing, high-tenacity yarn production capability, and established global installed base exceeding 200 million operational ring spindles concentrated in China, India, and Bangladesh apparel yarn mills. Ring spinning's production of high-quality fine count yarn (Ne 40-120) for premium apparel fabrics, unachievable through rotor or air-jet platforms at equivalent quality grades, sustains its machine type leadership.

While Others (Air-jet, Vortex, Hybrid) grow faster, ring spinning's fine-count yarn quality advantage for premium apparel and technical textile applications and its embedded installed base at global apparel yarn mills sustains machine type segment leadership through 2033 without structural displacement risk.

Others (Air-jet, Vortex, Hybrid) are the fastest-growing machine type at 5.7% CAGR through 2033. Air-jet and vortex spinning platforms, delivering 3-8x higher production speeds than ring spinning at coarse-to-medium yarn counts, are gaining adoption at MMF spinning mills and technical textile yarn producers, with Murata Vortex and Toyota RX300 air-jet platforms capturing greenfield investment share at South Asian and ASEAN expansion sites through 2033.

Fiber Type Insights

Natural Fiber leads the fiber type segment with a 42.6% market share in 2026, estimated at approximately US$ 2.62 Bn, anchored by cotton's dominant position as the world's most widely processed staple fiber with global consumption of 26.4 million metric tons in 2024 (ICAC, Cotton This Month Report), requiring the largest installed base of ring and rotor spinning platforms globally concentrated at India, China, Bangladesh, and Pakistan cotton yarn mills.

Natural fiber's consumer preference for comfort and breathability, sustaining cotton's 27% global textile fiber market share (Textile Exchange, 2024), maintains spinning machine procurement volumes at established natural fiber mills despite synthetic fiber growth. Blended fiber is growing faster due to MMF-cotton blend adoption, but natural fiber's commodity volume scale at apparel and home textile mills globally sustains its fiber type segment leadership through 2033.

Blended Fiber is the fast-growing fiber type at 5.6% CAGR by 2033. Rising apparel brand demand for cotton-polyester, cotton-modal, and cotton-Tencel performance blend fabrics combining natural fiber comfort with MMF durability, requiring spinning machines configured for mixed fiber processing, is driving blended fiber spinning machine adoption at mills servicing athleisure, activewear, and sustainable fashion supply chains globally.

Industry Analysis

Apparel & Fashion Industry leads the end use segment with a 55.2% market share in 2026, estimated at approximately US$ 3.39 Bn, reflecting the global apparel market's structural scale as the world's largest textile end-use segment, with global clothing and footwear market revenue exceeding US$ 1.7 Tn in 2024 (Euromonitor International Global Apparel Overview) creating sustained demand for ring and compact spinning platforms producing Ne 20-80 count cotton and blended yarns across Asian apparel yarn spinning mill procurement programs.

Apparel's dominance reflects both the sheer spinning machine volume consumed by fast fashion and premium apparel yarn supply chains and the segment's consistent annual capital investment cycle at India, Bangladesh, Vietnam, and China apparel yarn mills. Industrial textiles is growing faster, but apparel's installed base scale and recurring capacity expansion investment sustains end-use segment leadership through 2033.

Industrial Textiles is the fastest-growing end-use segment at 5.2% CAGR in the forecast period. Expanding geotextile infrastructure projects, EU-mandated technical protective workwear standards, medical textile fiber demand growth at 8.4% CAGR (Textile Exchange Technical Benchmark, 2024), and automotive composite fiber yarn adoption are collectively driving industrial textile spinning machine procurement acceleration globally through 2033.

Regional Insights

North America Spinning Machine Market Insights

North America is growing at a consistent 3.3% CAGR by 2033, holding approximately 10.4% of global Spinning Machine Market share in 2026, estimated at approximately US$ 639 Mn, anchored by U.S. technical textile spinning investment, reshoring-driven apparel yarn production programs, and Canadian and Mexican textile manufacturer spinning machine procurement under USMCA preferential sourcing requirements for U.S. apparel brand near-shoring supply chains.

U.S. Spinning Machine Market: Technical Textile Innovation, USMCA Reshoring, and Smart Spinning Investment

The United States holds approximately US$ 560 Mn in 2026, with the National Council of Textile Organizations (NCTO) confirming US$ 19 Bn in U.S. textile and apparel capital investments between 2014 and 2024, including ring and rotor spinning capacity at North Carolina, Georgia, and South Carolina technical textile mills. Parkdale Mills, operating 6.5 Bn yards of annual yarn production capacity, represents North America's largest ring spinning operator. Canada and Mexico contribute through USMCA-compliant yarn manufacturing investments by apparel brands reshoring production from Asian supply chains.

North America's growth is reinforced by USMCA near-shoring apparel yarn capacity investment, U.S. technical textile spinning machine modernization at defense and protective textile mills, and AI-integrated smart spinning platform adoption at North American premium yarn producers by 2033.

Europe Spinning Machine Market Insights

Europe holds a 17.9% share of the global Spinning Machine Market in 2026, estimated at approximately US$ 1.10 Bn, driven by Germany's precision textile machinery manufacturing leadership, Italian premium yarn spinning technology investment, and EU Ecodesign and circular economy policy frameworks accelerating recycled-fiber-capable spinning machine procurement at European sustainable textile mills.

Germany Spinning Machine Market: Precision Machinery, Sustainable Yarn, and Circular Textile Policy

Germany accounts for approximately US$ 421.1 Mn in 2026, anchored by Rieter and Saurer German-language R&D innovation, Oerlikon Schlafhorst rotor spinning platform manufacturing, and BMW, Audi, and automotive composite technical yarn spinning investment. The U.K. sustains British Wool premium spinning operations and Courtaulds successor specialty technical yarn mills. France contributes through Chanel, Hermès, and LVMH premium yarn supply chain sustainable spinning investments. Spain expands through Inditex supply chain-linked cotton and blended yarn spinning capacity upgrades at domestic mills.

Europe's EU Ecodesign Regulation-driven recycled fiber spinning upgrade cycle, German precision spinning technology OEM leadership, and premium sustainable yarn brand supply chain investments sustain structured mid-to-high specification spinning machine procurement volumes across European textile manufacturing corridors through 2033.

Asia Pacific Spinning Machine Market Trends

Asia Pacific is the leading and fastest-growing region at 8.5% CAGR through 2033, commanding approximately 48.5% of global spinning machine market share in 2025, driven by China's ring and rotor spinning installed base modernization under "Made in China 2025," India's PLI-funded MMF textile capacity expansion, and Bangladesh and Vietnam's export-oriented apparel yarn manufacturing investment attracting global spinning machine OEM procurement.

China Spinning Machine Market: Ring Spinning Dominance, PLI Investment, and MMF Capacity Expansion

China is likely to account for US$ 2.4 Bn in 2026, the world's largest spinning machine installed base with over 140 million operational ring spindles, driven by CATD and CNTAC textile industry digitalization programs, Jingwei Textile Machinery domestic spinning machine supply, and synthetic fiber rotor spinning expansion at Jiangsu and Zhejiang mills.

Indian market is expanding through the PLI scheme, LMW and Rieter co-investment at Tamil Nadu and Gujarat spinning corridors. Japan sustains Toyota Industries and TMT Machinery's precision air-jet and vortex platform leadership. Bangladesh and Vietnam absorb Chinese spinning machine OEM exports.

Asia Pacific's China ring spinning installed base modernization, India PLI MMF textile spinning expansion, and ASEAN export-oriented apparel yarn mill greenfield investment collectively sustain the region's combined market leadership and fastest-growth regional trajectory.

Competitive Landscape

The global spinning machine market is moderately consolidated, with Rieter, Saurer, Toyota Industries, Lakshmi Machine Works (LMW), and Trützschler collectively holding approximately 52-58% of global spinning machine revenue share, while mid-tier and regional players including Jingwei, Savio, and Marzoli compete on price and regional service networks. Proprietary spindle technology IP, digital mill monitoring software ecosystem, and energy-efficient compact spinning platform differentiation are the primary competitive moats.

AI-integrated quality monitoring platform development, recycled fiber spinning machine certification, Asia Pacific OEM distribution network expansion, and energy-efficient compact spinning platform cost leadership define the dominant competitive strategic investment themes across all major Spinning Machine market participants through 2033.

Strategic Developments

- In January 2025, Rieter Holding AG launched its ESSENTIAL package for ring spinning machines, integrating AI-based spindle fault detection, automated ring traveler wear monitoring, and remote diagnostic access, targeting 15% productivity uplift per shift at Asian and European apparel yarn mills upgrading legacy ring spinning installations with smart automation retrofits.

- In March 2024, Saurer Intelligent Technology AG signed a €153 million (≈1.2 billion yuan) strategic collaboration with DIW in China to supply and integrate advanced spinning systems-including blow room, carding, roving, and ring spinning equipment-for large-scale, digitally enabled textile industrial parks focused on intelligent yarn production.

- In November 2023, Lakshmi Machine Works (LMW) announced a US$ 85 Mn greenfield spinning machinery manufacturing facility expansion in Coimbatore, Tamil Nadu, adding ring spinning frame, compacting unit, and draw frame production lines to serve growing domestic and export demand for LMW spinning machines across South Asian textile manufacturing markets.

Companies Covered in Spinning Machine Market

- Rieter Holding AG

- Saurer Intelligent Technology AG

- Toyota Industries Corporation

- Lakshmi Machine Works Ltd. (LMW)

- Trützschler Group SE

- Jingwei Textile Machinery Co., Ltd.

- Murata Machinery Ltd. (Muratec)

- Oerlikon Schlafhorst

- Savio Macchine Tessili S.p.A.

- Marzoli Machines Textile S.r.l.

- TMT Machinery Inc.

- Zinser Textilmaschinen GmbH

- Shima Seiki Mfg. Ltd.

- Juki Corporation

- Picanol Group

Frequently Asked Questions

The spinning machine market is valued at US$ 6.1 Bn in 2026, projected to reach US$ 8.3 Bn by 2033, generating an incremental opportunity of US$ 2.10 Bn by 2033.

Industry 4.0 IoT automation reducing spinning mill labor costs 25-35%, India PLI and China "Made in China 2025" machinery subsidies, and expanding industrial and technical textile yarn demand growing at 8.4% CAGR are the primary growth drivers.

The spinning machine market grows at a CAGR of 4.3% from 2026 to 2033, building on a historical CAGR of 3.8% from 2020 to 2026.

EU Ecodesign Regulation-driven recycled fiber spinning machine upgrade opportunity (US$ 420-580 Mn by 2030) and South and Southeast Asian PLI and FDI-funded greenfield spinning capacity expansion (US$ 1.2-1.6 Bn annually through 2030) represent the highest-value market opportunities.

Rieter, Saurer, Toyota Industries, LMW, Trützschler, Jingwei, Muratec, Oerlikon Schlafhorst, Savio, Marzoli, TMT Machinery, Zinser, Shima Seiki, Juki, and Picanol are the leading global Spinning Machine market participants.