- Industrial Machinery

- Motor Bearings Market

Motor Bearings Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Motor Bearings Market by Bearing Type (Ball Bearings, Roller Bearings, Plain / Sliding Bearings, Specialty / Coated Bearings), Bearing Size (Small, Medium, Large), Material Type (Steel Bearings, Hybrid Bearings, Full Ceramic Bearings), Industry (Automotive, Manufacturing & General Industry, HVAC & Building Systems, Power Generation & Renewable Energy, Oil & Gas, Mining & Heavy Equipment, Aerospace & Marine, Food & Pharmaceuticals), and Region Analysis for 2026 to 2033

Motor Bearings Market Trends & Analysis

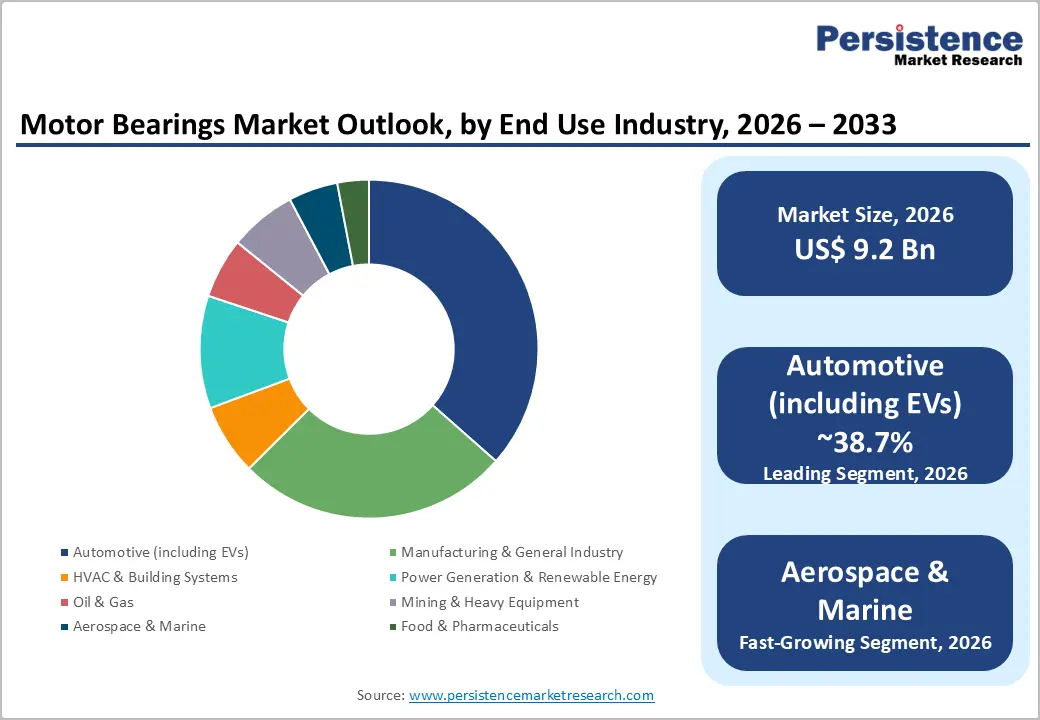

The global motor bearings market size is projected at US$ 9.2 Bn in 2026 and is projected to reach US$ 15.4 Bn by 2033, growing at a CAGR of 7.5% between 2026 and 2033.

Accelerating electric vehicle powertrain adoption demanding low-friction, electrically insulated bearing solutions, expanding renewable energy infrastructure installation generating high-load roller bearing procurement at scale, and progressive industrial automation deployment driving precision miniature bearing demand are the primary growth drivers.

Key Industry Highlights:

- Leading Bearing Type: Roller bearings lead with a 45.3% share; specialty/coated bearings grow fastest at a 9.7% CAGR, driven by EV electrical insulation and food & pharmaceutical corrosion-resistance mandates.

- Leading Material Type: Steel bearings lead at 72.4% share; full ceramic bearings grow fastest at 10.3% CAGR, driven by EV inverter-induced current damage elimination and cleanroom non-contamination requirements.

- Leading End-Use Industry: Automotive leads at 38.7% share; aerospace & marine grows fastest at 9.1% CAGR, driven by Boeing-Airbus delivery backlogs and NADCAP-certified specialty bearing procurement expansion.

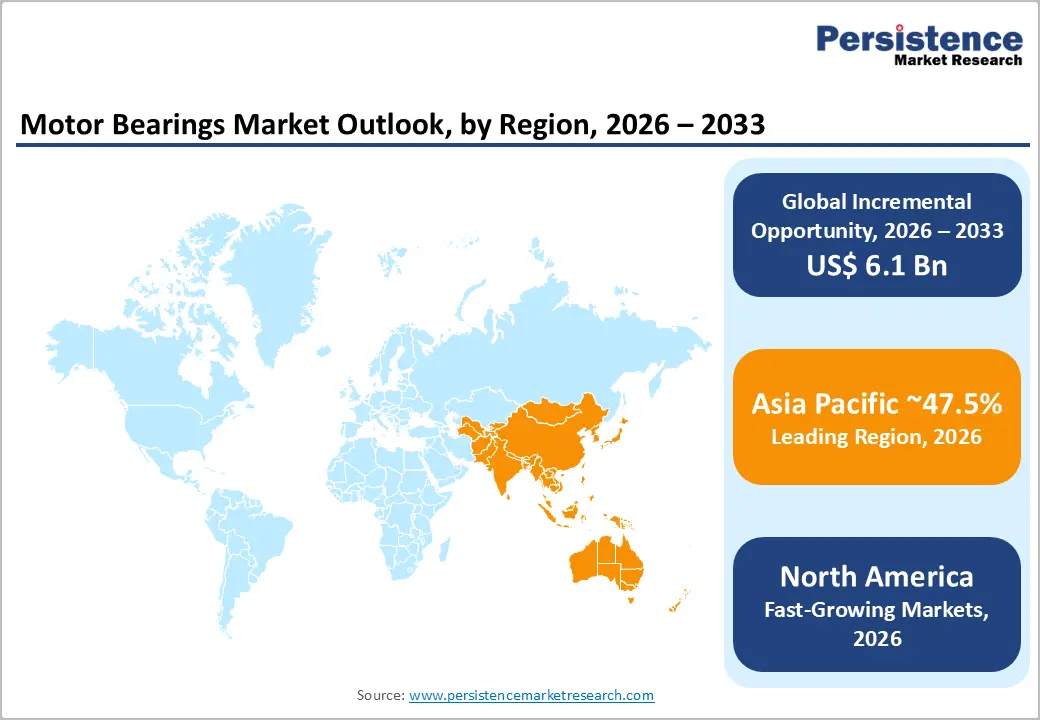

- Regional Leadership: Asia Pacific dominates and grows fastest at 8.3% CAGR with China at US$ 1.8 Bn and India at US$ 483.7 Mn; North America grows at 7.1% CAGR with the U.S. at US$ 1.5 Bn.

- Strategic Developments: SKF's next-generation INSOCOAT EV bearing launch (January 2025) and Schaeffler's €50 Mn India manufacturing expansion (March 2025) are institutionalizing EV-era motor bearing technology and Asia Pacific production capacity leadership.

Market Dynamics Analysis

Drivers - Electric Vehicle Powertrain Proliferation Generating Specialized Motor Bearing Demand

Global EV sales reached 17 million units in 2023 (IEA Global EV Outlook 2024), with projections exceeding 40 million annual units by 2030, each EV incorporating 5-12 precision motor bearings across traction motor, transmission, and auxiliary system applications requiring electrical insulation, low friction coefficient, and extended lubrication interval specifications that conventional steel bearings cannot deliver. EV drive motor bearings must withstand high-frequency shaft currents, generated by inverter switching frequencies of 8-20 kHz, that cause conventional bearing raceway pitting through electrical discharge machining (EDM) damage within 3,000-8,000 operating hours.

The EV drive motor bearings market alone is projected to reach US$ 277 Mn by 2032 at 8.9% CAGR, representing a rapidly expanding high-value bearing sub-segment where SKF's current-insulated INSOCOAT bearings, Schaeffler's electrically insulated FAG bearings, and NSK's hybrid ceramic ball bearing solutions command significant OEM specification premiums. The transition from ICE to EV powertrains is also eliminating conventional crankshaft and camshaft bearing procurement while simultaneously creating substantially higher per-vehicle bearing value content in traction motor applications, structurally increasing average motor bearing revenue per vehicle produced across premium EV platform programs through 2033.

Renewable Energy Infrastructure Expansion Driving Large Roller Bearing Procurement

The International Energy Agency's Renewables 2024 Report projects 7,300 GW of new renewable energy capacity additions through 2030, with wind turbine installations representing the single largest driver of global procurement of large-diameter, high-load motor bearings. Each 5-15 MW offshore wind turbine incorporates 8-12 large spherical roller bearings and cylindrical roller bearings in main shaft, gearbox, and generator applications, with individual turbine bearing sets valued at US$ 50,000-150,000 per installation at premium specifications. The Global Wind Energy Council (GWEC) documented 117 GW of new wind capacity installed in 2023 alone, generating a proportionally large bearing procurement volume.

Solar tracker drive motor bearings, installed across utility-scale photovoltaic plants now exceeding 1,000 GW of global installed capacity (IEA), represent a further rapidly growing precision motor bearing application category. The U.S. Inflation Reduction Act's US$ 369 Bn clean energy investment program and EU REPowerEU's €300 Bn renewable energy deployment commitment are collectively sustaining structurally elevated renewable energy installation rates that generate multi-year forward visibility for large and medium roller bearing procurement programs at wind turbine, hydroelectric generator, and utility-scale solar drive motor component manufacturing facilities globally.

Restraints - Counterfeit Bearing Supply Chain Infiltration Undermining Market Integrity and Safety

The global counterfeit bearing market is estimated to represent 15-25% of total bearing trade volume in emerging market distribution channels (European Association of Bearings Manufacturers), with non-genuine bearings, lacking the material quality, dimensional precision, and heat treatment specifications of OEM-certified products, causing premature motor failures across industrial, automotive, and renewable energy applications.

Counterfeit bearing infiltration is particularly acute in Asian distribution markets, where price-sensitive aftermarket procurement creates channels for the entry of sub-specification products. SKF estimates that counterfeit bearings cost the legitimate bearing industry approximately US$ 1.5 Bn in annual revenue loss, directly suppressing addressable market growth for certified motor bearing suppliers across price-sensitive procurement segments globally.

Extended Motor Bearing Service Life Reducing Replacement Frequency in Established Industrial Markets

Advanced lubrication technologies, surface coating innovations, and improved raceway geometry engineering in next-generation motor bearings are progressively extending the mean time between bearing replacements, from conventional 20,000-30,000 operating-hour service intervals toward 50,000-80,000-hour extended-life specifications in premium industrial motor applications. SKF's EXPLORER performance class bearings and Schaeffler's X-life bearing range document 70-100% service-life extensions over standard specification equivalents, reducing the frequency of aftermarket replacement bearing procurement at established industrial facilities. The IFR projects that the adoption of extended-life bearings will reduce replacement-cycle-driven aftermarket revenue growth rates by an estimated 1.5-2.5 percentage points annually across mature North American and European industrial motor markets.

Opportunities - Condition Monitoring and Smart Bearing Integration for Predictive Maintenance Platforms

Industrial IoT adoption across manufacturing, power generation, and transportation sectors is creating structural demand for smart motor bearings that integrate embedded vibration, temperature, speed, and load sensors directly into bearing assemblies to enable real-time condition monitoring and AI-driven predictive maintenance without external sensor retrofitting. SKF's Insight sensor-integrated bearings, Schaeffler's OPTIME wireless bearing condition monitoring system, and NSK's Condition Monitoring Service platforms are commercially available solutions generating recurring software and service revenue beyond one-time hardware procurement, representing a fundamental business model transformation from product to platform.

The global predictive maintenance market is projected to exceed US$ 28 Bn by 2033 (IFR Industry 4.0 Analytics), with smart bearing condition monitoring representing a US$ 1.5-2.5 Bn addressable sub-segment at full deployment scale.

For motor bearing manufacturers investing in sensor integration and cloud analytics platform development, smart bearing configurations command 30-50% price premiums over standard equivalents while generating annual subscription service revenue per installed unit, creating compound lifetime value per bearing that structurally expands total addressable market beyond hardware replacement cycles, particularly across critical motor applications in power generation, oil & gas, and aerospace end-use sectors through 2033.

Full Ceramic and Hybrid Bearing Adoption in High-Temperature and Corrosive Application Environments

Full ceramic and hybrid (steel + ceramic) motor bearings, utilizing silicon nitride (Si3N4) rolling elements, deliver measurable performance advantages over steel equivalents in high-temperature, corrosive, and electrically active operating environments: 50-70% lighter rolling elements, 58% lower thermal expansion coefficient, 30% higher hardness versus bearing steel, and inherent electrical non-conductivity eliminating EV inverter-induced bearing current damage. Food & pharmaceutical processing, semiconductor cleanroom, chemical processing, and EV traction motor applications represent the highest-growth deployment environments for ceramic bearing adoption.

Full Ceramic Bearings are the fastest-growing material type, with a 10.3% CAGR through 2033, and the addressable market opportunity in EV motor, aerospace, and food processing applications is estimated at US$ 0.8-1.2 Bn by 2030. SKF's full ceramic deep groove ball bearings for food processing, Schaeffler's ceramic hybrid angular contact bearings for machine tool spindles, and NTN's silicon nitride ceramic bearings for EV drive motors are commercially establishing ceramic bearing specification precedents across application categories that collectively represent the highest-value bearing replacement opportunity in the global motor bearings market through 2033.

Category-wise Analysis

Bearing Type Insights

Roller Bearings (Cylindrical, Spherical, Tapered, and Needle sub-types) lead the bearing type segment with a 45.3% market share in 2026. Roller bearings command segment leadership through their superior radial and axial load capacity relative to ball bearings, making them the mandatory specification for high-torque motor applications in wind turbine generators, mining equipment, rolling mill drives, railway traction motors, and heavy industrial motor platforms where ball bearings cannot sustain the required dynamic load ratings at commercially viable service life intervals.

The four roller bearing sub-types serve distinct application niches: cylindrical roller bearings for pure radial loads, spherical for misalignment tolerance, tapered for combined loading, and needle for compact space-constrained motor assemblies. Ball bearings' higher-speed efficiency sustains their position in EV and HVAC motors, but Roller Bearings' industrial volume base sustains segment leadership.

Specialty / Coated Bearings are the fastest-growing bearing type at 9.7% CAGR through 2033. EV motor electrical insulation requirements, food-grade and pharmaceutical cleanroom corrosion-resistance mandates, and aerospace high-temperature performance specifications are collectively driving the adoption of INSOCOAT, DLC (diamond-like carbon), and ceramic-coated specialty motor bearing configurations across premium industrial and transportation applications globally.

Bearing Size Analysis

Medium (30-100 mm) bearings lead the size segment with a 47.8% market share in 2026. Medium-bore bearings occupy the broadest motor application range in the global installed base, serving automotive traction and auxiliary motors, industrial three-phase induction motors (0.75-110 kW range), HVAC fan and compressor drives, pump and conveyor motors, and wind turbine generator accessory drives that collectively represent the largest volume procurement categories across all motor bearing end-use industries.

Their standardized dimensional interchangeability across ISO 15 series specifications enables direct cross-brand replacement procurement, supporting the highest aftermarket replacement volume of any bearing size category. Large bearings serve capital-intensive wind and mining applications, while small bearings address precision miniature motor niches. Medium bearings' volume dominance is structurally sustained through 2033.

Small (≤ 30 mm) bearings are the fastest-growing segment, with a 8.2% CAGR through 2033. Miniaturization of EV auxiliary motor systems, precision robotics joint actuators, medical device drive motors, and semiconductor handling equipment drives demand for ultra-precision miniature deep groove ball bearings with sub-30 mm bores, with tolerances tighter than the ABEC 7 and ISO P4 standards across semiconductor and medical end-use applications globally.

Material Type Insights

Steel Bearings lead the material type segment with a 72.4% market share in 2026. Through-hardened and case-carburized bearing steel, manufactured to ISO 683-17 and ASTM A295 standards, delivers the established cost-performance balance across the broadest range of motor bearing operating conditions, with proven raceway fatigue life, standardized heat treatment specifications, and global raw material supply chain depth that ceramic alternatives cannot currently match at volume scale.

Steel bearings' dimensional standardization, widespread manufacturing capability, and established OEM qualification database across automotive, industrial, and power generation motor applications sustain their material segment dominance. Hybrid bearings are gaining traction in EV applications, while Full Ceramic remains a premium niche. Steel's dominance is expected to persist through 2033, though its share will modestly decline as hybrid adoption grows.

Full ceramic bearings are the fastest-growing material type, with a 10.3% CAGR through 2033. EV drive motor electrical insulation requirements, food processing corrosion elimination mandates, aerospace high-temperature accessory drive applications, and semiconductor cleanroom non-magnetic and non-outgassing specifications are collectively driving full ceramic bearing adoption at a premium but rapidly expanding volume pace across high-specification motor applications.

Industry Insights

Automotive (including EVs) leads the end-use industry segment with a 38.7% share in 2026. Automotive's leadership reflects the industry's unmatched motor bearing consumption volume, with 93 million vehicles produced annually (OICA) each incorporating multiple wheel hub, transmission, engine auxiliary, and increasingly EV traction motor bearings, generating the world's highest sustained motor bearing procurement volume across OEM and aftermarket channels.

The EV transition is structurally increasing per-vehicle bearing content, as traction motors require higher-specification electrically insulated bearings compared to conventional drivetrain bearings. Manufacturing & General Industry, Power Generation, and HVAC sectors serve complementary volume-proportional roles but cannot match automotive's procurement scale. No dominance shift is expected through 2033.

Aerospace & Marine is the fastest-growing industry at 9.1% CAGR through 2033. Boeing and Airbus multi-decade delivery backlogs, expanding naval fleet modernization programs, and NADCAP-certified motor bearing specification requirements for turbine accessory drives and marine propulsion systems are driving global acceleration in aerospace and marine motor bearing procurement across premium full ceramic and specialty-coated bearing configurations.

Regional Market Insights

North America Motor Bearings Market Share

North America is growing at a prominent 7.1% CAGR through 2033, anchored by the U.S. Inflation Reduction Act's US$ 369 Bn clean energy investment driving wind turbine and EV motor bearing procurement, DoD aerospace bearing program investment sustaining NADCAP-certified specialty bearing demand, and advanced manufacturing reshoring initiatives generating new industrial motor bearing facility procurement across automotive EV production corridors in Michigan, Tennessee, Georgia, and Texas.

U.S. Market: EV Manufacturing and Renewable Energy Bearing Investment Leadership

The U.S. market is estimated at US$ 1.5 Bn in 2026, driven by Tesla, GM Ultium, and Ford EV platform traction motor bearing procurement; GE Vernova and Vestas wind turbine generator bearing programs; and Timken and Rexnord domestic bearing manufacturing investments serving IRA-incentivized clean energy projects. Canada contributes to Magna International EV drivetrain bearing manufacturing and Ontario-based wind energy facility bearing procurement programs through 2033.

Europe Motor Bearings Market Share

Europe holds a 21.6% share of the global Motor Bearings Market in 2025, driven by the EU Green Deal's renewable energy deployment, generating large roller bearing procurement, German automotive OEM EV platform transition driving electrically insulated bearing specification adoption, and SKF, Schaeffler, and RKB Bearing's European manufacturing investment, sustaining regional competitive leadership in premium motor bearing technology.

Germany, U.K., France & Spain: Premium Engineering Standards and EV Transition Bearing Demand

Germany's market is estimated at US$ 728.9 Mn in 2026, anchored by BMW, Volkswagen, and Mercedes-Benz EV traction motor bearing programs, Schaeffler's Herzogenaurach headquarters bearing R&D investment, and Siemens and Bosch industrial motor bearing procurement across automation and energy transition applications. The U.K. contributes Rolls-Royce aerospace motor bearing programs and offshore wind bearing procurement. France supports Safran Aerospace and Alstom rail traction motor bearing demand, while Spain supports Siemens Gamesa wind turbine bearing procurement through 2033.

Asia Pacific Motor Bearings Market Share

Asia Pacific is a dominant market poised to reach 8.3% CAGR by 2033, driven by China's world-leading EV production scale, India's rapidly expanding automotive and industrial motor manufacturing base, and Japan's precision bearing manufacturing heritage sustaining NSK, NTN, JTEKT, and Nachi-Fujikoshi global technology leadership across automotive, industrial, and semiconductor motor bearing applications.

China, India & Japan: EV Production Scale and Precision Manufacturing Ecosystem China's market is estimated at US$ 1.8 Bn in 2026, driven by BYD, CATL's ecosystem, and NIO's EV traction motor bearing procurement, alongside Wafangdian Bearing and Luoyang Bearing's domestic production serving industrial and wind energy applications. India's market, at US$ 483.7 Mn, is growing through Tata Motors' and Mahindra EV programs, and SKF India and Schaeffler India's manufacturing investments. Japan sustains global leadership in precision bearing technology through NSK's Fujisawa and NTN's Iwata advanced motor bearing manufacturing facilities.

Competitive Landscape

The global motor bearings market is moderately consolidated, with the top five players, SKF, Schaeffler, NSK, NTN, and JTEKT, collectively controlling approximately 55-60% of global motor bearing revenue in 2025. Key differentiators include proprietary bearing steel alloy formulations, IoT-integrated condition monitoring platforms, and EV-specific electrical insulation bearing technology portfolios. Bearing-as-a-Service predictive maintenance subscription contracts are emerging as strategic revenue model differentiators.

Smart bearing IoT platform investment, full ceramic and hybrid bearing technology commercialization for EV and aerospace applications, geographic manufacturing capacity expansion in India and Southeast Asia, and strategic acquisition of specialty bearing manufacturers targeting renewable energy and medical device motor bearing segments define the dominant competitive strategic themes through 2033.

Strategic Developments:

- In January 2025, SKF AB launched its next-generation INSOCOAT electrically insulated bearing range for EV traction motors, featuring a 20% thicker alumina coating achieving >100 MΩ insulation resistance, targeting EV drive motor bearing current damage elimination across Tier 1 automotive powertrain supplier specifications globally.

- In September 2023, The Timken Company acquired Des-Case Corporation, integrating fluid management and contamination control technology with Timken's motor bearing portfolio to deliver integrated bearing lifecycle management solutions for industrial motor applications in oil & gas and mining sectors across North America.

- In November 2024, NTN Corporation launched its silicon nitride full ceramic deep groove ball bearing series for EV auxiliary motor and fuel cell air compressor applications, demonstrating 40% lower torque loss and complete elimination of bearing current damage in inverter-driven 800V EV architecture applications at Toyota and Honda technology partnership facilities.

Companies Covered in Motor Bearings Market

- SKF AB

- Schaeffler AG

- NSK Ltd.

- NTN Corporation

- JTEKT Corporation

- The Timken Company

- Nachi-Fujikoshi Corporation

- RKB Bearing Industries

- THK Co., Ltd.

- Wafangdian Bearing Co., Ltd.

- ILJIN Bearing

- NRB Bearings Ltd.

- Fersa Group

- Luoyang Bearing Science & Technology

- GRW Bearings GmbH

Frequently Asked Questions

The motor bearing market is valued at US$ 9.2 Bn in 2026, projected to reach US$ 15.4 Bn by 2033.

Electric vehicle powertrain proliferation, demanding electrically insulated precision bearings and renewable energy infrastructure expansion, generating large-diameter roller bearing procurement at scale, are the primary growth drivers.

The motor bearings market is projected to grow at a CAGR of 7.54% from 2026 to 2033, building on a historical 6.7% CAGR from 2020 to 2026.

Smart IoT-integrated bearing condition monitoring platform development and full ceramic and hybrid bearing commercialization for EV, aerospace, and food-grade motor applications represent the highest-value strategic growth opportunities.

SKF, Schaeffler, NSK, NTN, JTEKT, Timken, Nachi-Fujikoshi, RKB Bearing, THK, Wafangdian Bearing, NRB Bearings, Fersa Group, Luoyang Bearing, and GRW Bearings are the leading global market participants.