- Advanced Materials

- Reverse Osmosis Membrane Market

Reverse Osmosis Membrane Market Size, Share, and Growth Forecast 2026 - 2033

Reverse Osmosis Membrane Market by Membrane Type (Thin Film Composite, Cellulose-based), Configuration (Spiral-wound, Hollow-fiber, Plate and Frame, Tubular), Application (Desalination, Utility Water Treatment, Wastewater Treatment & Reuse, Process Water, Potable Water, Other), End-use Industry, and Regional Analysis for 2026 - 2033

Reverse Osmosis Membrane Market Size and Trend Analysis

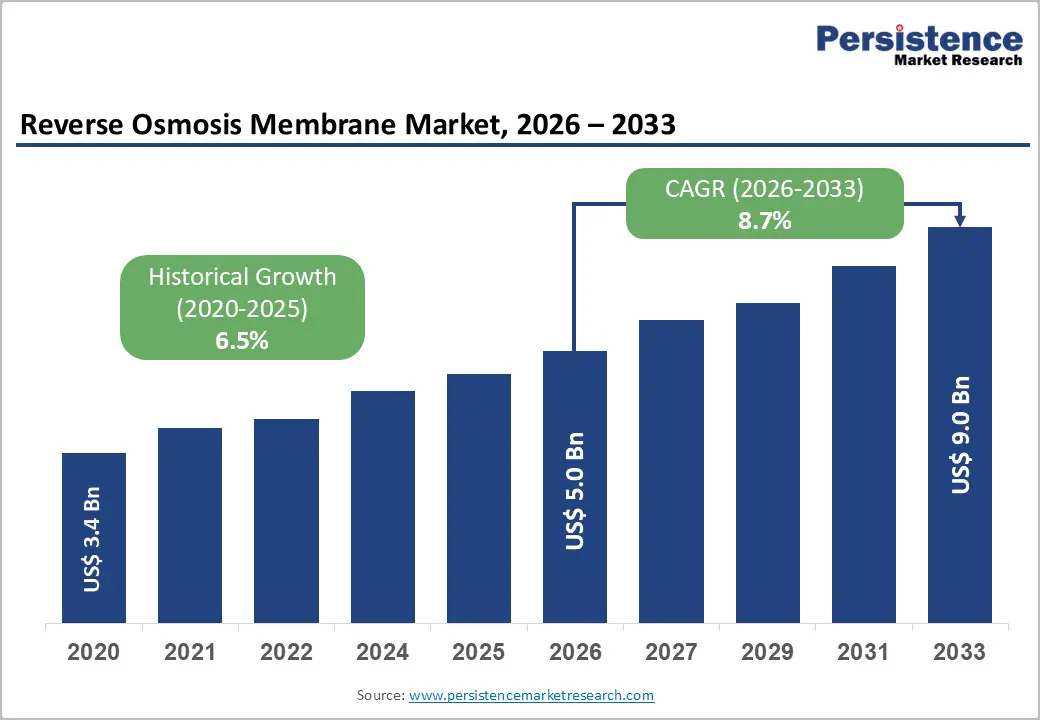

The global reverse osmosis membrane market size is valued at US$ 5.0 billion in 2026 and is projected to reach US$ 9.0 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

Rise in freshwater scarcity is the overriding catalyst, with the World Health Organization (WHO) reporting that approximately 2.2 billion people globally lack access to safely managed drinking water services. Coupled with rapid urbanization, intensifying climate disruption, and tightening environmental discharge regulations across both developed and emerging economies, demand for high-efficiency membrane-based water treatment is accelerating at an unprecedented pace. The market recorded a historical CAGR of 6.5% during 2020 - 2025, reflecting a structurally robust growth trajectory underpinned by enduring water security imperatives.

Key Industry Highlights:

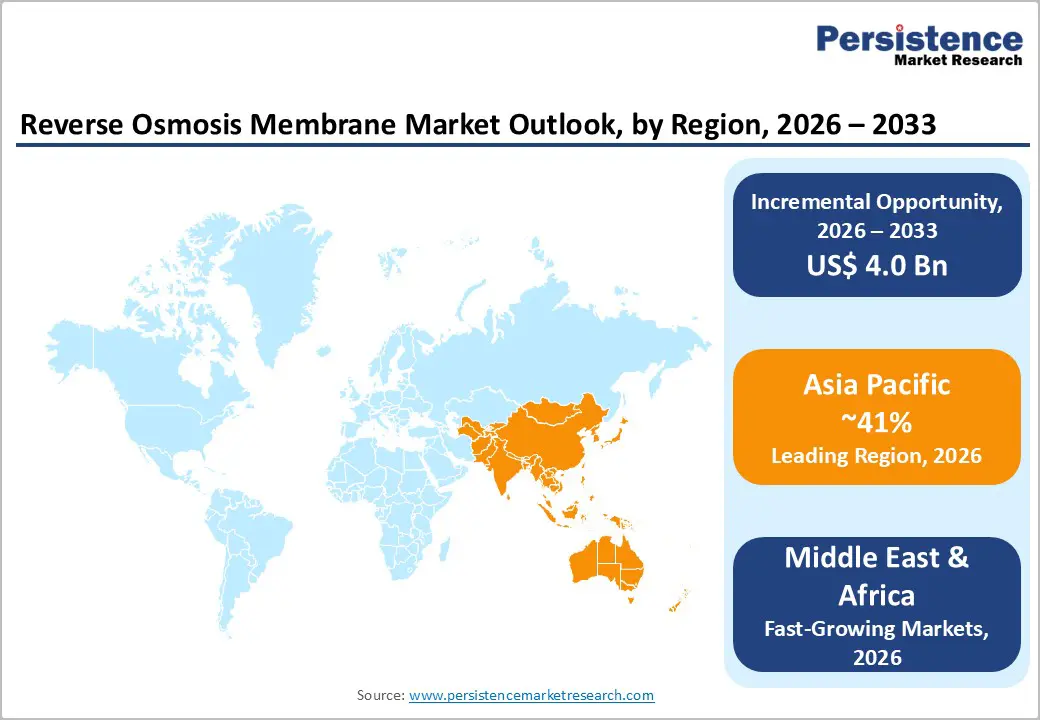

- Regional Leader: Asia Pacific is the leading regional market, accounting for approximately 41% of global Reverse Osmosis Membrane revenue in 2025, driven by severe freshwater scarcity, rapid industrialization, and large-scale government investments in water treatment infrastructure across China, India, and Southeast Asia.

- Fastest Growing Region: The Middle East and Africa region is the fastest-growing market for Reverse Osmosis Membranes, propelled by emergency desalination infrastructure investments following conflict-related damage, Vision 2030-aligned water projects in Saudi Arabia, and expanding municipal water access initiatives across the GCC states.

- Leading Segment: Thin Film Composite (TFC) membranes dominate the global market with approximately 62% share, attributed to superior salt rejection rates exceeding 99.5%, broad chemical resistance, and versatility across seawater desalination, brackish water treatment, and industrial process water applications.

- Fastest Growing Segment: The hollow-fiber membrane module segment is the fastest-growing configuration, gaining traction in compact industrial and semiconductor applications due to superior fouling resistance, high packing density, and growing demand for ultrapure water in advanced manufacturing facilities.

- Key Opportunity: Post-conflict reconstruction of desalination infrastructure across the Gulf Cooperation Council (GCC) region represents a key near-term market opportunity, with over 400 vulnerable desalination plants requiring urgent membrane replacements, upgrades, and resilience enhancements.

| Key Insights | Details |

|---|---|

| Reverse Osmosis Membrane Market Size (2026E) | US$ 5.0 Bn |

| Market Value Forecast (2033F) | US$ 9.0 Bn |

| Projected Growth CAGR (2026 - 2033) | 8.7% |

| Historical Market Growth (2020 - 2025) | 6.5% |

DRO Analysis

Drivers - Rise in Global Water Scarcity and Rising Demand for Desalination

The accelerating global freshwater crisis remains the most significant structural driver of the Reverse Osmosis (RO) Membrane market. Projections from the United Nations Environment Programme indicate that nearly 1.8 billion people will reside in regions experiencing absolute water scarcity by 2025, while the World Economic Forum anticipates that global freshwater demand will surpass supply by 40% by 2030. This widening disparity has prompted governments worldwide to invest in large-scale desalination and wastewater reuse initiatives, thereby strengthening the procurement cycles for RO membranes.

Saudi Arabia’s Saline Water Conversion Corporation operates the world’s largest RO desalination facility at Ras al-Khair, producing over 1.4 million m³ of water per day. In India, the Jal Jeevan Mission continues to expand tap-water connectivity, driving extensive deployment of RO membranes in high-TDS regions.

Stringent Environmental Regulations Driving Wastewater Treatment Investments

Regulatory mandates requiring advanced wastewater treatment and water reuse are steadily strengthening global demand for reverse osmosis (RO) membranes across municipal and industrial applications. In the United States, the Environmental Protection Agency continues to tighten effluent standards under the Clean Water Act, compelling industries such as pharmaceuticals, semiconductors, and power generation to adopt high-rejection RO membrane systems.

Similarly, the European Union’s revised Urban Wastewater Treatment Directive of 2024 has introduced more stringent micropollutant removal requirements, effectively making RO-based tertiary treatment essential for utilities serving populations exceeding 150,000. Furthermore, what are the Zero Liquid Discharge mandates in water-stressed regions, particularly in India and China, that are accelerating the integration of RO membranes within comprehensive water management frameworks, reinforcing long-term, structural market demand?

Restraints - High Capital and Operational Costs Limiting Adoption in Price-Sensitive Markets

The high initial capital expenditure required to install RO membrane systems remains a principal restraint on market penetration in low- and middle-income economies. Industrial-grade reverse osmosis plants require significant investment in pre-treatment infrastructure, high-pressure pumps, and energy recovery devices, which can render the technology cost-prohibitive for smaller municipalities and rural water utilities.

According to the International Desalination Association (IDA), the levelized cost of water from seawater RO systems ranges from USD 0.5 to USD 1.0 per cubic meter, a level that remains financially challenging for governments with constrained public budgets. Operational expenditure, particularly energy consumption, can account for 30-50% of total operating costs, adding substantially to the total cost of ownership and slowing adoption in emerging markets.

Membrane Fouling and Scaling Challenges Elevating Maintenance Costs

Membrane fouling and scaling represent persistent technical barriers that inflate maintenance expenditure and reduce operational efficiency. Biofouling, caused by microbial biofilm formation and inorganic scaling driven by salts such as calcium carbonate and barium sulfate, can reduce water flux by 20-40% if not proactively managed, according to peer-reviewed research published in the Journal of Membrane Science.

Operators are compelled to implement costly chemical-cleaning protocols and replace membranes before their designed service life of 5-7 years, thereby increasing lifecycle costs. These challenges disproportionately affect installations processing highly variable feed water, elevating technical barriers to entry for operators lacking sophisticated monitoring capabilities.

Opportunities - Emerging Demand from Middle East Post-Conflict Reconstruction and Resilience Investment

The ongoing geopolitical disruption in the Middle East, triggered by the U.S.-Israel-Iran conflict that began on February 28, 2026, has underscored the region's critical vulnerability to desalination infrastructure. Reports from the Atlantic Council and the Center for Strategic and International Studies (CSIS) confirm that desalination facilities in Bahrain, Iran, and the UAE have sustained damage, compelling affected nations to fast-track infrastructure modernization and redundancy projects.

With over 400 desalination plants operating along the shores of the Arabian Gulf, supplying approximately 100 million people, post-conflict reconstruction will require substantial procurement of RO membranes across the Gulf Cooperation Council (GCC) states. This creates a near-term surge in demand for manufacturers with localized production and established supply agreements in the region, particularly as Saudi Arabia and the UAE seek to decentralize and harden their desalination capacity against future geopolitical disruptions.

Technological Innovation in Next-Generation Membrane Materials and Smart Water Systems

Advancements in membrane chemistry, nanotechnology, and digital technologies are creating substantial long-term growth prospects for the reverse osmosis membrane industry. Research documented in peer-reviewed studies highlights that graphene oxide and aquaporin-based membranes can deliver water permeability enhancements of three to five times compared with traditional thin-film composite membranes.

Furthermore, integrating Internet of Things (IoT) sensors and AI-enabled predictive maintenance solutions enables real-time fouling detection and autonomous system optimization, helping reduce chemical use and extend membrane service life. DuPont Water Solutions has further advanced digital adoption through its WAVE PRO platform, introduced in March 2025, to streamline the design of ultrafiltration and RO systems. Collectively, these innovations are reducing total ownership costs and broadening market accessibility.

Category-wise Analysis

Membrane Type Insights

The Thin Film Composite (TFC) segment remains the leading membrane type, accounting for approximately 62% of total market share in 2025. TFC membranes feature a layered polyamide barrier supported by a polysulfone base, enabling salt rejection rates exceeding 99.5%, significantly outperforming cellulose-based alternatives. Their strong chemical resistance, broad operational pH range of 2-11, and compatibility with demanding pre-treatment processes make them the preferred option for seawater desalination, brackish water purification, and industrial process water applications.

Major manufacturers such as DuPont Water Solutions, Toray Industries, Inc., and LG Chem Ltd. continue to advance TFC formulations to enhance flux efficiency and reduce energy consumption. While cellulose-based membranes maintain relevance in food and beverage applications, lower rejection capability and narrower pH tolerance limit their scalability.

Configuration Insights

The spiral-wound module configuration holds a dominant position, accounting for approximately 67% of the configuration-based market share in 2025. Its leadership is supported by high packing density, cost-efficient manufacturing, and operational simplicity, making it particularly suitable for large-scale municipal and industrial water treatment systems.

Spiral-wound elements enhance membrane surface area by tightly rolling flat-sheet membranes along with feed and permeate spacers into compact cylindrical modules, allowing scalable deployment from small point-of-use units to mega desalination facilities exceeding 500,000 m³ per day. This configuration is widely adopted in major global installations such as the Sorek B plant in Israel and the Hassyan plant in the UAE. Meanwhile, hollow-fiber modules demonstrate the fastest growth, driven by superior fouling resistance and high surface-area-to-volume efficiency essential in semiconductor and compact industrial applications.

Application Insights

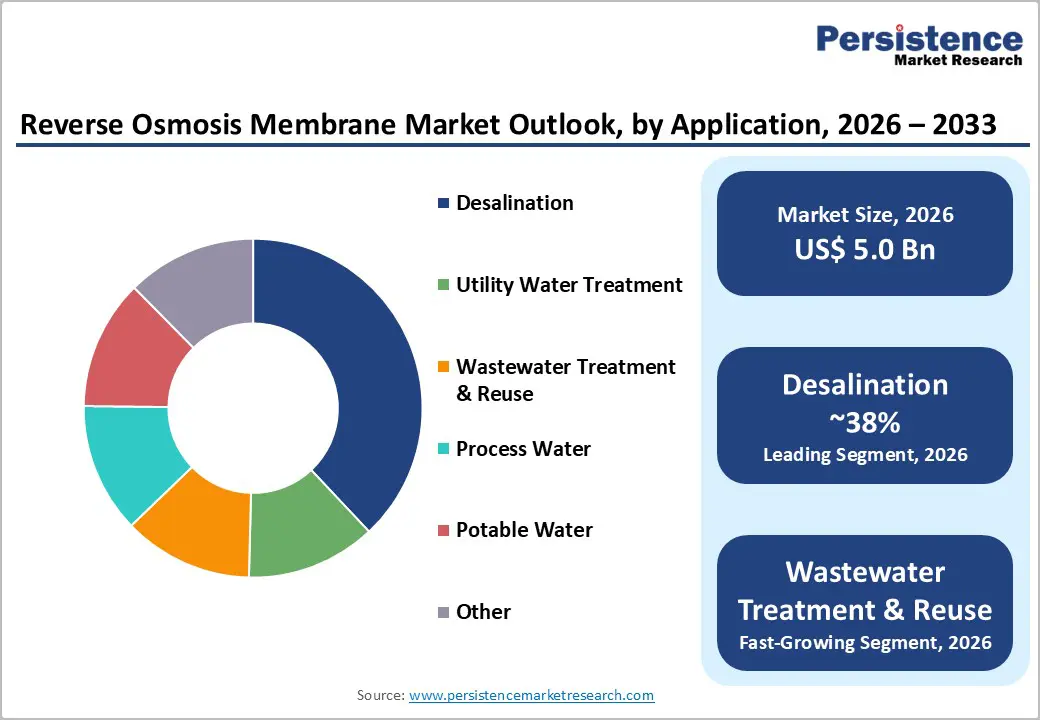

The Desalination segment maintains its position as the leading application, with 38% market share, underpinned by the irreplaceable role of seawater and brackish water desalination in meeting freshwater demands across water-scarce geographies. The GCC countries alone account for approximately 33% of global daily desalinated water production according to data from the International Desalination Association (IDA), reflecting the region's existential dependence on RO-based water infrastructure.

Major projects such as the Taweelah plant in the UAE, processing 909,200 m³/day, and the Shoaiba 5 plant in Saudi Arabia, fully operational as of 2024, collectively deploy hundreds of thousands of high-rejection seawater RO membrane elements. The Wastewater Treatment & Reuse segment is simultaneously the fastest-growing application, accelerated by tightening environmental regulations, urban water recycling mandates, and increasing recognition of treated wastewater as a strategic alternative water source.

Industry Insights

The Municipal and Desalination Utilities segment represents approximately 39%, making it the largest end-use category and underscoring the scale of public investment in water security infrastructure. Utilities operating large-scale desalination and water treatment facilities constitute the highest-volume purchasers of RO membranes, with individual projects often requiring tens of thousands of membrane elements during each commissioning cycle.

The Industrial Process Water segment ranks as the second-largest category, driven by stringent purity requirements across the pharmaceutical, semiconductor, power generation, and food and beverage industries. Meanwhile, the Healthcare sector is experiencing above-average growth as global biopharmaceutical production increases demand for water for injection and sterile-grade process water.

Regional Insights

North America Reverse Osmosis Membrane Market Trends

North America continues to rank among the largest regional markets, supported by the United States’ strong industrial base, advanced water treatment infrastructure, and concentration of technology-intensive sectors such as pharmaceuticals and semiconductor manufacturing. Municipalities are increasingly investing in upgraded purification systems to comply with revised contaminant limits under the Safe Drinking Water Act, particularly for emerging pollutants like PFAS.

The U.S. also remains a leading exporter of desalination technologies to Latin America and the Caribbean, reinforcing the region’s role as a global center for membrane innovation. Furthermore, the evolving geopolitical landscape, including the U.S.-Iran conflict beginning in February 2026, has introduced supply chain pressures, prompting operators to secure inventory buffers. Persistent drought in southwestern states further accelerates the adoption of water reuse and advanced desalination solutions.

Europe Reverse Osmosis Membrane Market Trends

The European market is characterized by its advanced regulatory environment and its growing commitment to water circularity principles. The 2024 revision of the EU Urban Wastewater Treatment Directive establishes a binding pathway for member states to adopt advanced tertiary treatment by 2039, thereby embedding RO membrane technologies within municipal wastewater reuse frameworks. Germany and France continue to lead industrial deployment, while Spain remains one of Europe’s highest per-capita consumers of desalinated water, supported by substantial RO-based capacity along its Mediterranean coast.

Furthermore, indirect disruptions from the U.S.-Iran conflict, such as desalination supply chain volatility and elevated energy prices, have strengthened Europe’s focus on domestic water resilience. Under the EU Water Resilience Strategy, increased emphasis on reducing freshwater extraction and expanding industrial water reuse is expected to drive significant demand for RO membranes through 2033.

Asia Pacific Reverse Osmosis Membrane Market Trends

Asia Pacific remains the dominant regional market, contributing nearly 41% of global market revenue in 2025. The region’s leadership is driven by severe freshwater scarcity and rapid industrial expansion across China, India, and Southeast Asia. China leads the market, supported by the Water Ten Plan and sustained investments in wastewater treatment and advanced purification infrastructure. India’s Jal Jeevan Mission has promoted extensive deployment of RO membranes in high-TDS regions to expand tap-water access for 191 million rural households.

The U.S.-Iran conflict has further underscored the need for water security across hydrocarbon-dependent economies such as South Korea, Japan, and emerging Southeast Asian nations. Japan’s leading manufacturers continue to advance next-generation membrane technologies, while India is projected to record the fastest growth through 2033.

Competitive Landscape

The global Reverse Osmosis Membrane market exhibits a moderately consolidated structure, with a small cohort of multinational corporations, including DuPont, Toray Industries, Inc., LG Chem Ltd., and Veolia Water Technologies & Solutions, commanding a disproportionate share of global capacity and proprietary technology. These incumbents leverage deep R&D capabilities, extensive patent portfolios, and established customer relationships with major desalination and industrial water treatment operators. Market strategies increasingly center on regional manufacturing localization, illustrated by LG Chem's and Veolia's collaborations with Alkhorayef Group to establish RO membrane production in Saudi Arabia, alongside digital service integration, sustainability-aligned product development, and long-term supply agreements with utilities. Emerging competitors from China, including Vontron Membrane Technology, are intensifying competitive pressure in price-sensitive segments.

Key Developments:

- March 2026: DuPont Water Solutions announced the expansion of Water Application Value Engine, its advanced online water treatment modeling tool, with the addition of reverse osmosis and nanofiltration capabilities. The enhanced platform now integrates ultrafiltration (UF), ion exchange (IX), RO, and NF into a single, comprehensive water treatment design solution for applications including drinking water, industrial utility water, wastewater, and seawater desalination.

- April 2024: Toray Industries, Inc., announced the launch of the TLF-400ULD reverse osmosis (RO) membrane. It developed this offering with Toray Membrane (Foshan) Co., Ltd., and Toray Advanced Materials Research Laboratories (China) Co., Ltd., for industrial wastewater reuse and sewage treatment.

- May 2025: Veolia has signed an agreement with CDPQ for the acquisition of its 30% stake in Veolia’s subsidiary Water Technologies and Solutions, allowing Veolia to achieve full ownership of WTS, enabling it to unlock more value potential, simplify further its structure, and extract additional run-rate cost synergies of ~€90m. This acquisition is a logical step in the deployment of Veolia’s GreenUp strategic roadmap, with an efficient capital allocation to strengthen the Group’s anchoring in Water technologies activities and in the United States, both identified as priority growth “boosters”.

Top Companies in the Reverse Osmosis Membrane Market

- DuPont (Wilmington, U.S.) is the global market leader in RO membranes, powered by its patented FilmTec™ technology that delivers industry-leading salt rejection and durability. The company serves over 10,000 desalination and water reuse plants across more than 100 countries, with manufacturing and distribution spanning North America, Europe, and Asia. Its product portfolio covers seawater, brackish water, and nanofiltration membranes, supported by digital tools including the WAVE PRO modeling platform.

- Toray Industries, Inc. (Tokyo, Japan) is a pioneering manufacturer of high-performance RO membranes, combining advanced nanotechnology with precision manufacturing across mega-factories in Japan, South Korea, and China, with annual output exceeding 10 million membrane elements. In 2024, Toray secured a landmark supply contract for a large-scale mining desalination project in Chile and launched next-generation high-durability membranes for semiconductor ultrapure water applications, reflecting the company's broad cross-sector innovation pipeline.

- LG Chem Ltd. (Seoul, South Korea) has established a strong competitive position in the seawater RO segment through its proprietary QUANTUM™ nanocomposite membrane technology, which delivers approximately 20% higher productivity than conventional membranes. The company's 2014 acquisition of NanoH2O provided a foundational technological advantage, and its ongoing collaboration with Alkhorayef Group in Saudi Arabia reflects a strategic commitment to localized production in high-growth Middle Eastern markets.

Companies Covered in Reverse Osmosis Membrane Market

- DuPont

- Toray Industries Inc.

- LG Chem Ltd.

- Hydranautics

- Veolia Water Technologies & Solutions

- Toyobo Co., Ltd.

- Alfa Laval

- MANN+HUMMEL

- Pentair

- Kovalus Separation Solutions

- Pall Corporation

- Koch Membrane Systems, Inc.

- Lenntech B.V.

Frequently Asked Questions

The global Reverse Osmosis Membrane market is valued at US$ 5.0 Bn in 2026 and is projected to reach US$ 9.0 Bn by 2033, expanding at a CAGR of 8.7% during the forecast period of 2026-2033. The market registered a historical CAGR of 6.5% during 2020 - 2025.

Escalating global water scarcity is the primary growth driver. The United Nations estimates approximately 2.2 billion people lack access to safely managed drinking water, compelling governments and industries worldwide to invest in RO-based desalination and wastewater reuse technologies. Stricter environmental discharge regulations across the U.S., EU, India, and China further underpin sustained demand.

Thin Film Composite (TFC) membranes dominate the market with approximately 62% share, attributable to their superior salt rejection rates exceeding 99.5%, high chemical resistance, broad pH tolerance, and versatility across seawater desalination, brackish water treatment, and industrial process water applications compared with cellulose-based alternatives.

Asia Pacific leads the global market with approximately 41% revenue share in 2024, driven by acute freshwater scarcity, rapid urbanization, and large-scale government investments in water infrastructure across China, India, Japan, and Southeast Asia. China holds the largest country-level share within the region, while India is expected to register the fastest national growth rate through 2033.

Key opportunities include post-conflict desalination infrastructure reconstruction across the GCC region, with over 400 plants requiring upgrades, growing demand for next-generation graphene oxide and AI-integrated RO membrane systems, and fast-expanding water reuse markets in India, China, and Southeast Asia under mandatory water recycling regulations.

The major players in the global Reverse Osmosis Membrane market include DuPont, Toray Industries Inc., LG Chem Ltd., Hydranautics, Veolia Water Technologies & Solutions, Toyobo Co., Ltd., Alfa Laval, MANN+HUMMEL, Pentair, Kovalus Separation Solutions, Pall Corporation, Koch Membrane Systems, Inc., and Lenntech B.V.