- Metalworking & Fabrication

- Precision Turned Product Manufacturing Market

Precision Turned Product Manufacturing Market Size, Share, and Growth Forecast, 2026 - 2033

Precision Turned Product Manufacturing Market by Operation (CNC Operation, Swiss-Type Turning, Others), Machine Type (Computer Numerically Controlled (CNC) machines, Automatic Screw Machines, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Precision Turned Product Manufacturing Market Size and Trends Analysis

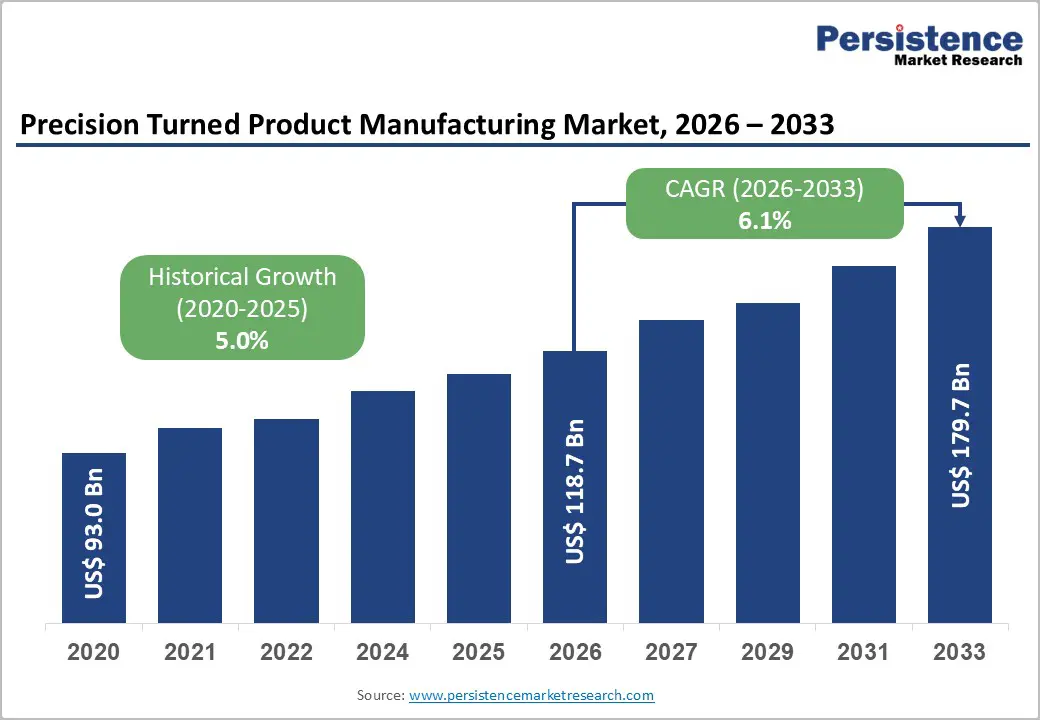

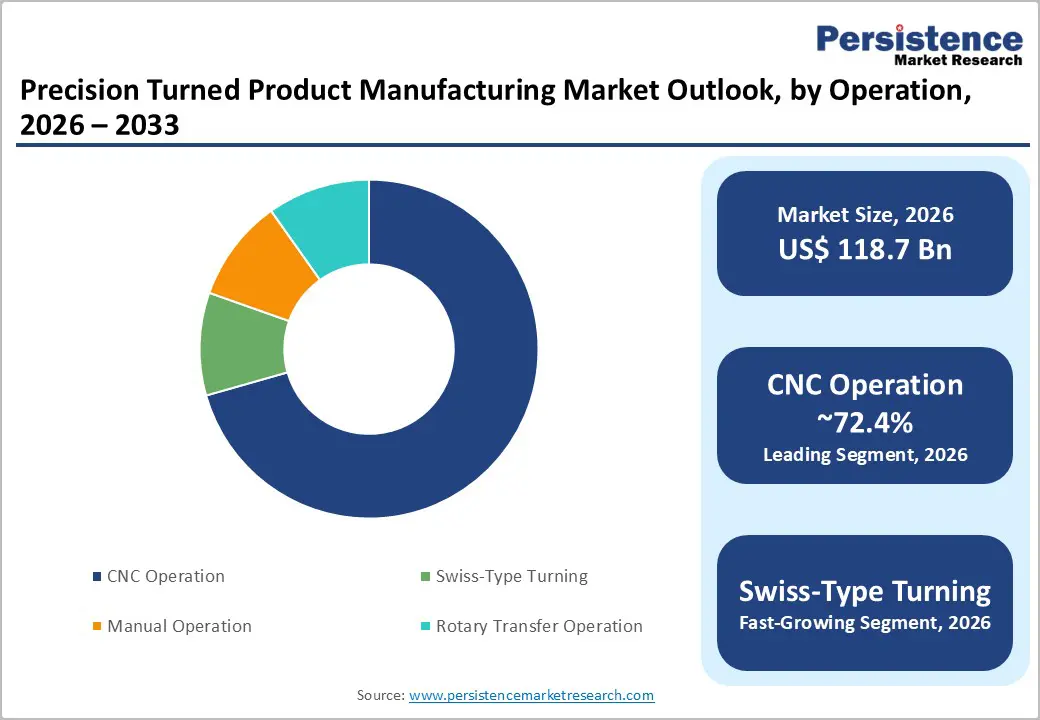

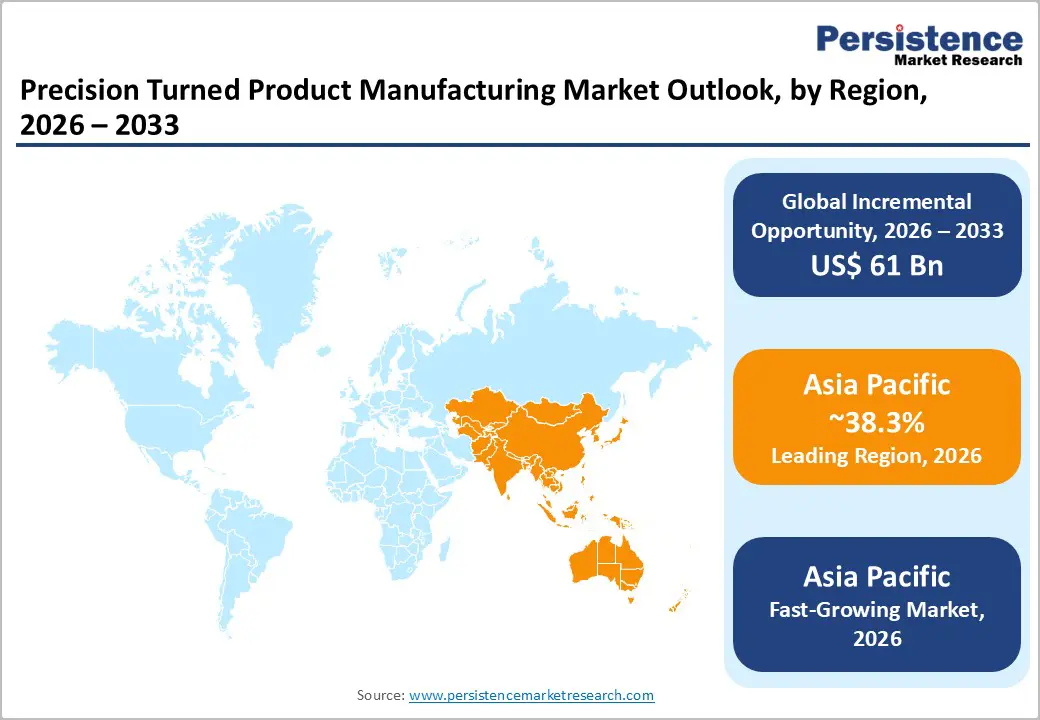

The global precision turned product manufacturing market size is likely to be valued at US$118.7 billion in 2026 and is expected to reach US$179.7 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by increasing demand for high-precision components across the automotive, aerospace, medical, defense, and electronics industries.

The widespread adoption of CNC-based manufacturing technologies continues to improve production efficiency, repeatability, and quality assurance. At the same time, growing requirements for miniaturized and complex components are accelerating the adoption of Swiss-type turning technologies. The market outlook remains supported by ongoing industrial automation, electric vehicle production growth, and rising regulatory requirements for precision-engineered products.

Key Industry Developments:

- Leading Region: Asia Pacific is anticipated to account for approximately 38.3% of market share in 2026, supported by China's manufacturing leadership, strong automotive production, electronics manufacturing, and expanding industrial automation investments.

- Fastest-growing Region: Asia Pacific is projected to register the highest growth rate through 2033, driven by rising manufacturing localization, electric vehicle production, aerospace expansion, and increasing adoption of advanced CNC and automation technologies across China, India, and Southeast Asia.

- Dominant Operation: CNC Operation is anticipated to hold approximately 72.4% market share in 2026, driven by superior precision, repeatability, automation capabilities, and widespread adoption across automotive, aerospace, medical, and electronics manufacturing.

- Leading End-use Industry: Automobile is anticipated to account for approximately 34.2% of market share in 2026, driven by rising vehicle production, electric vehicle adoption, and growing demand for precision-engineered automotive components.

DRO Analysis

Driver - Rising Electric Vehicle Production Driving Demand for Precision Components

The rapid expansion of the electric vehicle (EV) industry is creating significant demand for precision turned components such as shafts, connectors, housings, fasteners, bushings, and motor assemblies. Modern EV platforms require highly engineered components capable of maintaining strict dimensional tolerances while supporting lightweight vehicle architectures and advanced powertrain systems. The increasing adoption of electric mobility across major markets, including China, the U.S., and Europe, has expanded the demand for high-volume precision machining operations.

Precision turned products play a critical role in battery systems, electric motors, charging infrastructure, and thermal management systems. Manufacturers capable of delivering consistent quality, tighter tolerances, and scalable production volumes are benefiting from long-term supply agreements with automotive OEMs and Tier-1 suppliers. As vehicle electrification continues to reshape global transportation markets, demand for precision manufacturing capabilities is expected to remain a major growth catalyst throughout the forecast period.

Increasing Regulatory Requirements in Medical and Aerospace Manufacturing

Medical device and aerospace manufacturers operate under some of the world's most stringent quality and traceability requirements. Regulatory frameworks emphasizing process validation, material traceability, product consistency, and documentation have increased reliance on specialized precision machining suppliers capable of meeting these standards.

In the medical sector, demand for surgical instruments, orthopedic implants, dental components, diagnostic equipment, and minimally invasive devices continues to increase. Similarly, aerospace manufacturers require highly reliable precision parts for engines, landing gear systems, hydraulic assemblies, and structural components. These industries increasingly favor automated CNC and Swiss-type manufacturing operations due to their ability to deliver repeatable quality and comprehensive process documentation. The trend is expanding outsourcing opportunities for precision turned product manufacturers that maintain advanced quality systems and certified production environments.

Restraint - Raw Material Price Volatility and Margin Pressure

Fluctuations in the prices of stainless steel, titanium, aluminum, brass, copper, and specialty alloys represent a significant challenge for precision turned product manufacturers. Since raw materials account for a substantial portion of production costs, sudden price increases can negatively impact profitability, particularly for suppliers operating under fixed-price contracts.

Smaller manufacturers are especially vulnerable because they often possess limited purchasing power and reduced ability to negotiate long-term material agreements. In addition, rising labor costs, energy expenses, and compliance-related investments further pressure operating margins. The uncertainty associated with material procurement may delay capital investments in automation and advanced machining technologies. As a result, manufacturers must continuously optimize supply chain management and production efficiency to maintain competitiveness in a cost-sensitive environment.

Opportunity - Growing Outsourcing Trends in Medical Device Manufacturing

The medical device industry presents a significant growth opportunity for precision turned product manufacturers. Device manufacturers are increasingly outsourcing the production of complex and micro-scale components to specialized suppliers possessing advanced machining expertise and validated manufacturing processes.

Miniaturized surgical devices, dental implants, orthopedic components, catheter systems, and diagnostic instruments require exceptional dimensional accuracy and surface finish quality. Swiss-type turning technology is particularly well-suited for producing these highly specialized parts. As healthcare expenditures increase globally and aging populations drive greater demand for medical treatments, outsourcing partnerships are expected to expand, creating attractive long-term growth opportunities for precision component manufacturers.

Expansion of Manufacturing Capacity across Asia Pacific

Asia Pacific continues to emerge as the most attractive region for precision manufacturing investments. Strong industrial growth, expanding automotive production, rising electronics manufacturing, and government initiatives supporting advanced manufacturing have accelerated demand for precision turned products.

Countries such as China, India, Vietnam, Thailand, and Indonesia are strengthening their positions within global manufacturing supply chains. The region benefits from extensive supplier ecosystems, competitive production costs, growing domestic consumption, and increasing investments in automation technologies. Manufacturers establishing localized production facilities and distribution networks across Asia Pacific are well-positioned to capture rising demand from both domestic and export-oriented industries.

Category-wise Analysis

Operation Insights

CNC operation is anticipated to account for approximately 72.4% of the market share in 2026, maintaining its position as the dominant operational segment. Its leadership is driven by superior precision, repeatability, automation, and production efficiency compared with conventional machining methods. CNC systems are extensively used to manufacture critical components such as automotive transmission shafts, aerospace fasteners, medical implants, and electronic connectors. Their ability to support tight tolerances, reduce scrap rates, and ensure consistent quality across high-volume production runs continues to strengthen their market dominance.

Swiss-type turning is anticipated to be the fastest-growing operational segment through 2033, supported by increasing demand for miniature and highly complex precision components. The technology is widely used for manufacturing orthopedic screws, catheter components, surgical instruments, aerospace pins, and telecommunications connectors. Its ability to machine long, slender parts with exceptional accuracy and surface finish makes it particularly valuable in medical, aerospace, and electronics applications. Growing product miniaturization trends are expected to accelerate adoption throughout the forecast period.

End-use Industry Insights

The automobile industry is anticipated to account for approximately 34.2% of the market share in 2026, remaining the largest end-use segment. Automotive manufacturers rely heavily on precision turned products for engine components, transmission systems, fuel injectors, steering assemblies, brake systems, and electric vehicle motor parts. The continued expansion of electric vehicle production is further increasing demand for precision-engineered battery housings, charging connectors, and thermal management components, supporting the segment's long-term market leadership.

Medical devices and equipment are anticipated to be among the fastest-growing end-use segments through 2033, driven by rising healthcare investments and increasing demand for advanced medical technologies. Precision turned components are widely used in orthopedic implants, dental implants, surgical instruments, endoscopic devices, and diagnostic equipment. Stringent quality and traceability requirements encourage healthcare manufacturers to partner with specialized precision machining suppliers, creating significant growth opportunities for the segment over the forecast period.

Regional Insights

North America Precision Turned Product Manufacturing Market Trends

North America is supported by its advanced manufacturing ecosystem, strong regulatory framework, and high demand for precision-engineered components. The region benefits from significant investments in automation, digital manufacturing technologies, robotics, and quality-control systems. Aerospace, defense, medical devices, automotive, and industrial equipment remain the primary end-use sectors driving market demand.

U.S. Precision Turned Product Manufacturing Market Trends

The U.S. dominates the North American market, accounting for the majority of regional revenue. The country benefits from a large aerospace and defense industry, extensive medical device manufacturing capabilities, and a growing electric vehicle sector. Precision turned products are widely used in aircraft engines, landing gear systems, surgical instruments, orthopedic implants, fuel systems, and EV powertrain components. Increasing reshoring initiatives and investments in smart manufacturing facilities continue to strengthen domestic production capacity.

Canada Precision Turned Product Manufacturing Market Trends

Canada contributes through its aerospace, industrial machinery, and energy equipment sectors. The country's advanced manufacturing base and growing focus on automation technologies are supporting demand for precision machined components. Canadian suppliers increasingly participate in North American aerospace and defense supply chains, creating opportunities for precision turning manufacturers.

The region is expected to maintain steady growth through continued investment in robotics, automated inspection systems, advanced CNC technologies, and workforce development programs.

Europe Precision Turned Product Manufacturing Market Trends

Europe remains a strategically important market for precision turned product manufacturing. The region is characterized by strong engineering expertise, advanced industrial infrastructure, and stringent quality standards. Demand is primarily supported by automotive, aerospace, medical technology, industrial machinery, and defense applications.

Germany Precision Turned Product Manufacturing Market Trends

Germany represents the largest market in Europe due to its globally competitive automotive sector and advanced industrial machinery industry. Precision turned components are extensively utilized in automotive powertrains, industrial automation equipment, aerospace systems, and renewable energy technologies. The country's continued investment in Industry 4.0 initiatives is accelerating demand for high-precision machining capabilities.

U.K. Precision Turned Product Manufacturing Market Trends

The U.K. maintains a strong position in aerospace and medical device manufacturing. Demand for precision turned products is supported by aircraft production programs, defense modernization projects, and growing healthcare technology investments. The country's focus on advanced engineering and high-value manufacturing continues to support market growth.

France Precision Turned Product Manufacturing Market Trends

France benefits from a well-established aerospace industry and growing investments in industrial automation. Precision machined components are widely used in aircraft structures, engine systems, medical devices, and industrial equipment manufacturing.

Spain Precision Turned Product Manufacturing Market Trends

Spain contributes significantly through its automotive production sector and expanding aerospace industry. The country's manufacturing modernization efforts and increasing adoption of automation technologies are creating new opportunities for precision turning suppliers.

European manufacturers continue to invest in digital production systems, energy-efficient equipment, and smart factory technologies. These initiatives are expected to enhance productivity and support long-term market expansion.

Asia Pacific Precision Turned Product Manufacturing Market Trends

Asia Pacific is anticipated to account for approximately 38.3% of the market share in 2026, making it both the largest and fastest-growing regional market. The region benefits from extensive manufacturing infrastructure, competitive production costs, strong export capabilities, and growing domestic demand across multiple industries. Automotive, electronics, aerospace, medical devices, and industrial machinery remain the primary growth drivers.

China Precision Turned Product Manufacturing Market Trends

China dominates the Asia Pacific market and is estimated to account for approximately 57% of the market. The country benefits from a highly developed manufacturing ecosystem, extensive supplier networks, and large-scale automotive and electronics production. Continued investments in advanced machine tools, electric vehicle manufacturing, and industrial automation are strengthening China's leadership position.

Japan Precision Turned Product Manufacturing Market Trends

Japan remains a global leader in precision engineering and advanced machining technologies. The country's expertise in CNC equipment, robotics, aerospace systems, and electronics manufacturing supports strong demand for high-precision turned components. Japanese manufacturers continue to focus on automation, productivity improvements, and next-generation manufacturing technologies.

India Precision Turned Product Manufacturing Market Trends

India is emerging as one of the fastest-growing markets in the region, supported by government initiatives promoting domestic manufacturing, infrastructure development, and industrial modernization. Growth in automotive production, aerospace manufacturing, medical devices, and industrial equipment sectors is driving demand for precision machined components. Increasing foreign direct investment and expansion of industrial corridors are further strengthening market opportunities.

Competitive Landscape

The global precision turned product manufacturing market is highly fragmented, with numerous regional and global participants competing across various end-use industries. No single company commands a dominant market share, as customer requirements often vary based on application, material expertise, certification requirements, and production capabilities. Companies that invest in automation, advanced machining technologies, and specialized production capabilities are generally better positioned to secure long-term contracts from aerospace, automotive, medical, and electronics customers.

Leading companies focus on automation, process innovation, precision engineering, and geographic expansion to strengthen market positions. Investments in digital manufacturing technologies, advanced metrology systems, smart factory solutions, and customer-specific engineering services are becoming increasingly important competitive differentiators. Strategic partnerships, regional expansion initiatives, and technology-driven productivity improvements remain key priorities across the industry.

Key Industry Developments:

- In April 2025, Citizen Machinery Co., Ltd. launched the third-generation Cincom L20-LFV series of sliding-head CNC lathes, featuring enhanced productivity, improved energy efficiency, and advanced machining capabilities for high-precision turned components.

- In December 2025, Tornos SA expanded its strategic partnership with Ellison Technologies to strengthen distribution and customer support for Swiss-type CNC lathes across multiple U.S. manufacturing regions.

Companies Covered in Precision Turned Product Manufacturing Market

- Citizen Machinery Co., Ltd.

- Tornos SA

- Star Micronics Co., Ltd.

- TSUGAMI Corporation

- INDEX-Werke GmbH & Co. KG Hahn & Tessky

- Yamazaki Mazak Corporation

- Okuma Corporation

- DMG MORI Co., Ltd.

- Haas Automation, Inc.

- Makino Milling Machine Co., Ltd.

- Nakamura-Tome Precision Industry Co., Ltd.

- Hardinge Inc.

- Schütte Group GmbH

- Marubeni Citizen-Cincom Inc.

- Precision Swiss Products, Inc.

- Cox Manufacturing Company, Inc.

Frequently Asked Questions

The global precision turned product manufacturing market is estimated to be valued at US$118.7 billion in 2026.

The market is expected to reach US$179.7 billion by 2033.

Key trends include rising adoption of CNC machining and Swiss-type turning technologies, increasing electric vehicle production, growing medical device outsourcing, expansion of smart manufacturing facilities, and higher investments in automation and Industry 4.0 technologies.

CNC operation is the leading segment, anticipated to account for approximately 72.4% of the market in 2026, owing to its superior precision, automation capabilities, and production efficiency.

The precision turned product manufacturing market is projected to grow at a CAGR of 6.1% between 2026 and 2033.

Some of the major players include Citizen Machinery Co., Ltd., Tornos SA, Star Micronics Co., Ltd., TSUGAMI Corporation, and INDEX-Werke GmbH & Co. KG Hahn & Tessky.