- Medical Devices

- Portable Oxygen Concentrators Market

Portable Oxygen Concentrators Market Size, Share, and Growth Forecast, 2025 - 2032

Portable Oxygen Concentrators Market by Technology Type (Continuous Flow, Pulse Flow, Others), Application (Chronic Obstructive Pulmonary Disease (COPD), Asthma, Respiratory Distress Syndrome, Others), End-use (Hospitals, Home-care Settings, Ambulatory Surgical Centers, Long-term Care Facilities, Emergency Medical Services), and Regional Analysis for 2025 - 2032

Portable Oxygen Concentrators Market Size and Trend Analysis

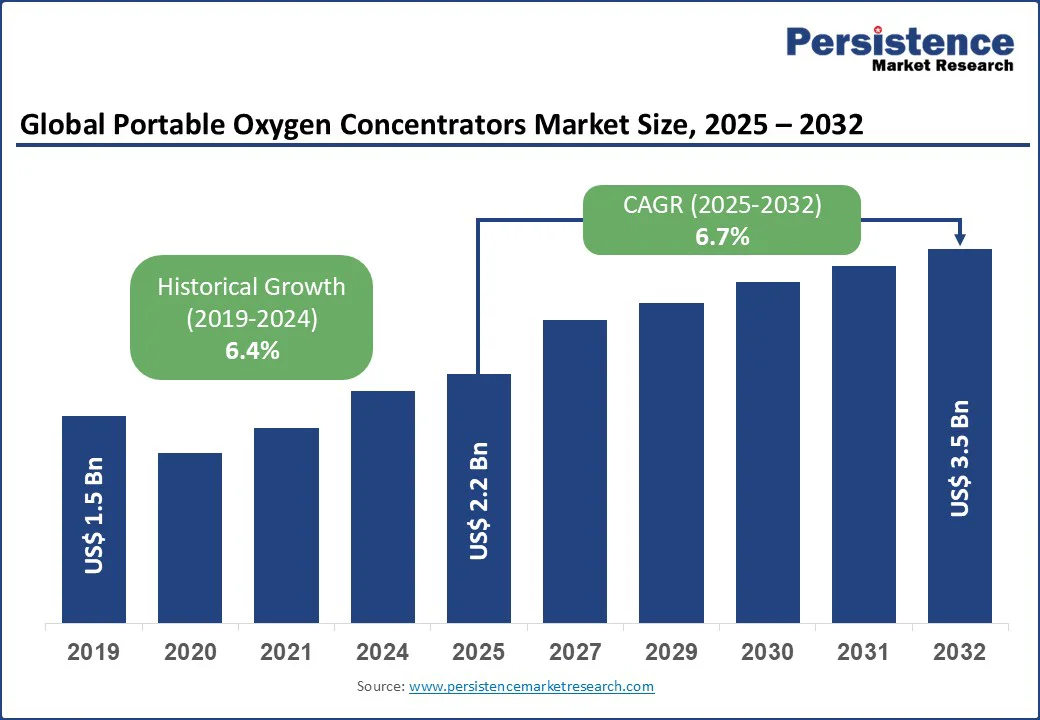

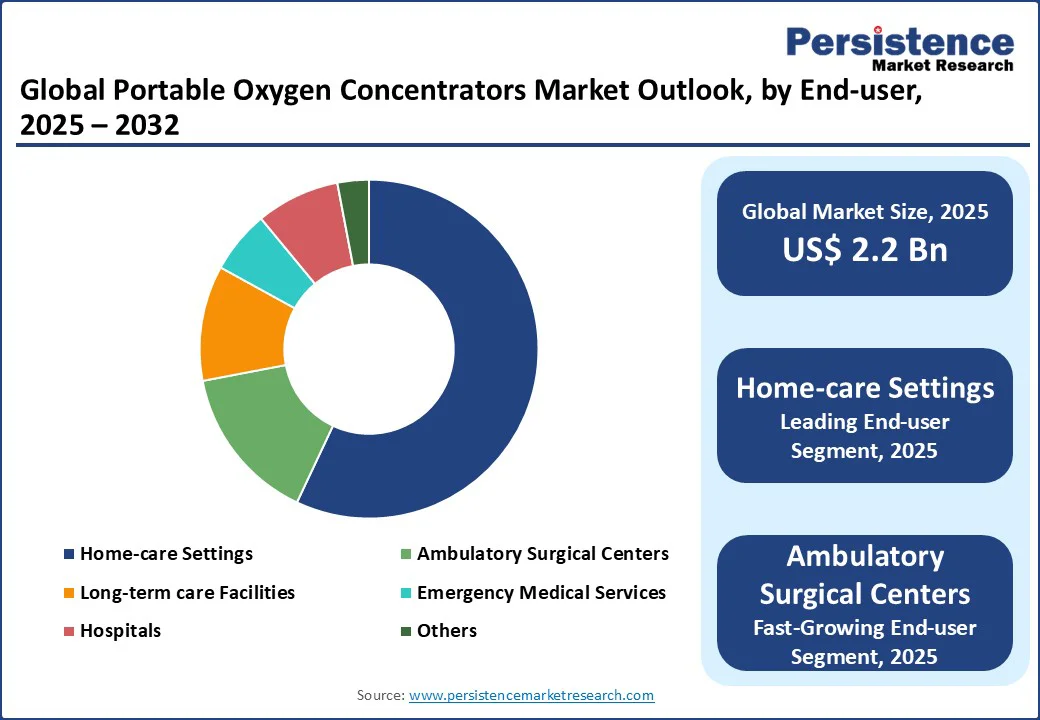

The global portable oxygen concentrators market size is likely to be valued at US$2.2 Bn in 2025 and is expected to reach US$3.5 Bn by 2032, growing at a CAGR of 6.7% from 2025 to 2032.

Rising incidence of chronic respiratory conditions such as COPD and asthma, the increasing geriatric population requiring continuous oxygen support, and the growing shift toward home healthcare solutions drives demand for portable oxygen concentrators.

Advancements in portable oxygen concentrator technology, such as lightweight design, longer battery life, and enhanced efficiency, further support adoption. Additionally, supportive reimbursement frameworks, higher patient awareness, and demand for mobility-oriented medical devices are propelling market expansion, making portable oxygen concentrators a preferred choice in respiratory care management.

Key Industry Highlights:

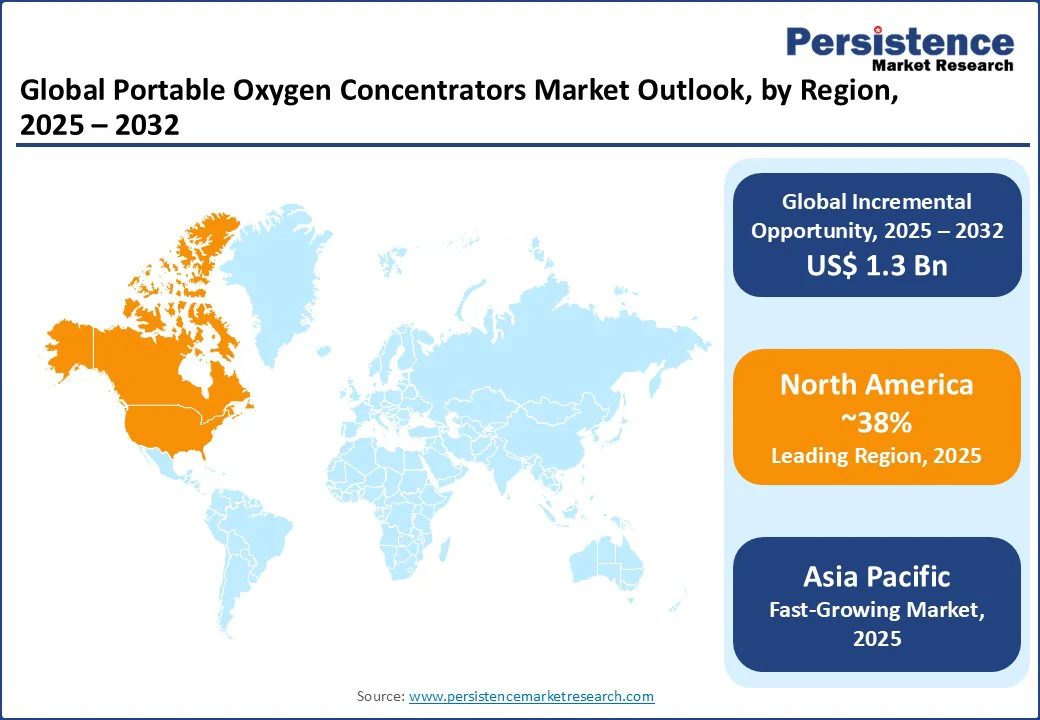

- Leading Region: North America holds a 38% global portable oxygen concentrators market share in 2025, driven by well-established healthcare infrastructure, high COPD prevalence, and supportive reimbursement policies that encourage adoption of portable oxygen concentrators.

- Fastest-growing Region: Asia Pacific is the fastest-growing market, driven by rising healthcare expenditure, increasing respiratory disease cases in China and India, and expanding awareness of home-based and portable oxygen therapy solutions.

- Dominant Technology Type: Continuous flow devices lead with a 54% market share in 2025, favored for managing severe respiratory conditions, delivering steady oxygen flow, and supporting long-term clinical and home-based therapy.

- Leading Application: COPD remains the largest application, capturing 60% market share, driven by its high global prevalence and the growing need for long-term oxygen therapy to improve patient quality of life.

- Leading End-use: Home-care settings dominate with 57% of market revenue, reflecting a global shift toward home-based care, patient convenience, and mobility-focused oxygen therapy solutions.

- Key Developments: In 2024, Inogen launched a lightweight pulse flow concentrator enhancing mobility, while Philips introduced an energy-efficient model in India to strengthen adoption in home-care settings.

|

Global Market Attribute |

Key Insights |

|

Portable Oxygen Concentrators Market Size (2025E) |

US$2.2 Bn |

|

Market Value Forecast (2032F) |

US$3.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.4% |

Market Dynamics

Driver: Rising Prevalence of Respiratory Diseases and Aging Population

The growing prevalence of chronic respiratory diseases, particularly COPD, along with the expanding elderly population, is a major factor boosting demand for portable oxygen concentrators. For instance, according to the U.S. Centers for Disease Control and Prevention (CDC), in 2023, the age-adjusted prevalence of COPD among adults was 3.8%, but it rose sharply to 10.5% among those aged 75 and older.

This reflects how aging directly correlates with increased respiratory disease incidence, driving higher reliance on oxygen therapy. Portable concentrators address this need by offering mobility, independence, and continuous respiratory support outside clinical settings.

As global life expectancy continues to grow, the elderly population represents a rapidly growing consumer base for portable oxygen concentrators. With COPD already affecting more than 213 million people worldwide and remaining the fourth-leading cause of death, demand for efficient, lightweight, and home-friendly oxygen therapy devices is set to accelerate significantly over the forecast period.

Restraint: High Costs and Limited Battery Life

One of the key restraints impacting the portable oxygen concentrator market is the high cost of these devices. Prices generally range from US$1,500 to over US$4,000 in developed countries, while in emerging markets such as India, units are typically priced between INR 1,00,000 and INR 3,50,000 (USD 1,200-4,200).

Advanced concentrators offering continuous flow technology or extended battery options fall at the upper end, making them less affordable for a large patient base. This limits widespread adoption of oxygen therapy devices in low- and middle-income economies where healthcare budgets and reimbursement frameworks are still developing.

In addition to cost, limited battery life reduces the usability of portable systems designed for patient mobility. Most devices provide 3-5 hours of runtime, restricting independence during travel or outdoor activities. Premium models such as the Inogen One G5 extend up to 13 hours, but come with higher costs. This trade-off between affordability and performance remains a major challenge for the growth of respiratory care equipment and home healthcare solutions.

Opportunity: Technological Advancements and Expansion in Emerging Markets

Rapid technological advancements are creating strong growth opportunities in the portable oxygen concentrator market. Manufacturers are increasingly focused on developing lightweight, compact, and energy-efficient devices that enhance patient mobility and convenience.

Innovations such as longer-lasting lithium-ion batteries, smart connectivity for real-time oxygen monitoring, and noise-reduction technology are improving the overall user experience. Integration of AI and IoT-enabled features is also enabling remote patient monitoring, aligning with the rising demand for home healthcare solutions. These advancements are not only improving treatment outcomes but also expanding the potential customer base for oxygen therapy devices.

At the same time, the expansion of emerging markets presents a significant growth avenue. Countries in Asia-Pacific, Latin America, and the Middle East are witnessing a surge in chronic respiratory diseases, coupled with a rapidly aging population. Rising healthcare investments, government support for affordable care, and growing awareness of respiratory care equipment are driving adoption. As affordability improves and infrastructure strengthens, demand for advanced portable oxygen concentrators in these regions is expected to accelerate.

Category-wise Insights

Technology Type Insights

The continuous flow portable oxygen concentrators (POCs) segment continues to lead the portable oxygen concentrators market, accounting for nearly 54% share in 2025. These devices deliver a constant oxygen supply, making them indispensable for patients with severe respiratory illnesses such as chronic obstructive pulmonary disease (COPD) and respiratory distress syndrome.

Their reliability in providing uninterrupted therapy has also driven their dominance in clinical settings, with approximately 60% of hospital-based oxygen therapy in 2024 relying on continuous flow systems to support critical care and long-term treatment needs.

In contrast, the pulse flow POCs segment is witnessing the fastest growth, propelled by rising demand for lightweight, portable, and energy-efficient solutions. Growing adoption among active patients, particularly those managing asthma and mild COPD, is expected to rise by nearly 20%, as pulse flow devices enhance mobility while optimizing battery performance

Application Insights

Chronic Obstructive Pulmonary Disease (COPD) remains the leading application area for portable oxygen concentrators, capturing nearly 60% of the portable oxygen concentrators market in 2025 and generating revenues of around US$0.95 Bn. This dominance is attributed to the high global burden of COPD and the critical need for continuous oxygen therapy among patients.

In fact, an estimated 70% of POC users worldwide in 2024 were individuals diagnosed with COPD, relying on these devices to improve mobility, support daily activities, and enhance overall quality of life. The growing elderly population and increasing hospital discharges with home-based oxygen care are further strengthening COPD’s role in driving demand.

Meanwhile, asthma applications represent the fastest-growing segment in the portable oxygen concentrators market. This segment is growing rapidly, supported by a 15% rise in POC prescriptions for asthma patients in 2024. The surge is particularly noticeable in urban regions with deteriorating air quality, where portable oxygen therapy offers both flexibility and effective disease management.

End-use Insights

Home-care settings dominate the portable oxygen concentrators market, accounting for nearly 57% share in 2025. This leadership reflects the growing global preference for home-based healthcare solutions, particularly among elderly patients and those with chronic respiratory conditions requiring long-term oxygen therapy.

In 2024, approximately 65% of oxygen therapy users opted for home-care POCs, highlighting their convenience, cost-effectiveness, and ability to support independent living. The increasing emphasis on reducing hospital stays and improving quality of life is further accelerating adoption in this segment.

On the other hand, ambulatory surgical centers (ASCs) represent the fastest-growing end-use segment. This segment is projected to double by 2032. Growth is being driven by the rising trend of outpatient respiratory procedures and the need for cost-effective treatment options. In 2024 alone, POC installations in outpatient facilities rose by 12%, underscoring their role in providing convenient, efficient, and patient-centered respiratory care.

Regional Insights

North America Portable Oxygen Concentrators Market Trends

North America dominates the portable oxygen concentrators market with a 38% share in 2025, supported by advanced healthcare infrastructure and a high prevalence of respiratory diseases. The United States leads, generating around US$0.84 Bn, driven by over 16 million COPD cases and favorable Medicare coverage, which reimburses up to 80% of POC costs in 2024.

In Canada, market growth is fueled by rising demand in home-care settings, where nearly 15% of elderly patients use POCs. Government-backed respiratory health programs and strong emphasis on patient-centered care continue to strengthen adoption across the region.

Europe Portable Oxygen Concentrators Market Trends

Europe holds a significant share of the portable oxygen concentrators market in 2025, supported by a growing elderly population and rising prevalence of chronic respiratory disorders such as COPD and asthma. Countries such as Germany, the UK, and France are major contributors, driven by strong healthcare infrastructure and increasing adoption of home-based oxygen therapy.

Favorable reimbursement policies across the European Union further encourage patient access to advanced respiratory care devices. With the region’s aging population projected to exceed 20% by 2030, demand for efficient and portable oxygen therapy solutions is expected to expand steadily throughout the forecast period.

Asia Pacific Portable Oxygen Concentrators Market Trends

Asia-Pacific is the fastest-growing region in the portable oxygen concentrators market, driven by a rising burden of respiratory diseases, rapid urbanization, and increasing healthcare spending. Countries such as China, India, and Japan are witnessing higher adoption due to worsening air quality, large patient pools, and growing awareness of home healthcare solutions.

Supportive government initiatives to improve access to respiratory care devices are further fueling growth. With the region’s elderly population expanding rapidly and healthcare infrastructure improving, the Asia Pacific is projected to record the highest CAGR through 2032, making it a key growth engine for the global market.

Competitive Landscape

The global portable oxygen concentrators market is moderately consolidated, with a few global manufacturers holding nearly 70% of the total share in 2025. Competition is driven by continuous innovation in lightweight designs, extended battery performance, and smart connectivity features to meet rising patient demand.

Many companies are expanding their presence in emerging markets through partnerships and distribution networks, while also investing in sustainable production practices. Intense R&D focus on enhancing efficiency and affordability continues to shape the industry’s competitive dynamics.

Key Developments

- September 2024: Oxymed introduced the P2 Portable Oxygen Concentrator in India. The device weighs 1.98 kg and offers up to 10 hours of battery life with a double battery option, making it highly suitable for mobile and home-care use.

- April 2024: Philips launched the EverFlo Oxygen Concentrator in India, featuring ≥93% oxygen purity and an energy-efficient design. Its compact build and reduced power consumption have strengthened adoption in home-care respiratory therapy.

Companies Covered in Portable Oxygen Concentrators Market

- Koninklijke Philips N.V.

- CAIRE Inc. (Chart Industries)

- Inogen Inc.

- Invacare Corporation

- Drive DeVilbiss Healthcare

- ResMed Inc.

- O2 Concepts LLC

- Precision Medical Inc.

- Nidek Medical Products Inc.

- GCE Group

- Besco Medical

- Yuwell Jiangsu Medical

- OxyGo LLC

- Foshan Keyhub Electronic Industries

- Beijing North Star Sci-Tech

- Longfian Scitech

- Others

Frequently Asked Questions

The portable oxygen concentrators market is projected to reach US$2.2 Bn in 2025, driven by rising respiratory disease prevalence and home-care demand.

Key drivers include increasing COPD and asthma cases, aging populations, and advancements in lightweight, portable devices.

The portable oxygen concentrators market will grow from US$2.2 Bn in 2025 to US$3.5 Bn by 2032, with a CAGR of 6.7%.

Opportunities include technological advancements in pulse flow devices and expansion into emerging markets such as India and China.

Leading players include Koninklijke Philips N.V., CAIRE Inc., Inogen Inc., Invacare Corporation, Drive DeVilbiss Healthcare, and ResMed Inc.