- Biotechnology

- Particle Therapy Market

Particle Therapy Market Size, Share, and Growth Forecast 2026 - 2033

Particle Therapy Market by Particle Type (Proton Therapy, Heavy Ion Therapy, Others), System Type (Cyclotron-based Systems, Synchrotron-based Systems, Synchrocyclotron Systems), Application (Prostate Cancer, Pediatric Cancers, Brain Tumors, Lung Cancer, Others), End-User (Hospitals, Specialized Cancer Centers, Academic & Research Institutes, Others), and Regional Analysis, 2026 - 2033

Particle Therapy Market Size and Trend Analysis

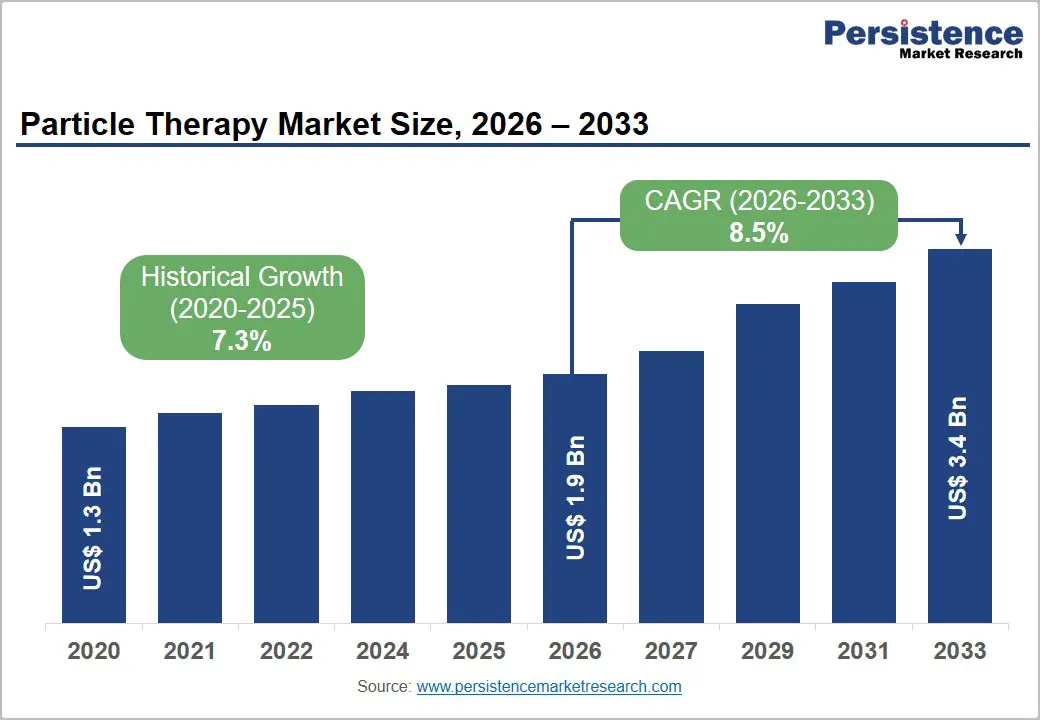

The global particle therapy market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 8.5% between 2026 and 2033. This growth is propelled by the rise in global cancer burden, compelling clinical evidence supporting the dosimetric superiority of particle therapy over conventional photon radiotherapy, and an expanding pipeline of new proton therapy center installations across North America, Europe, and the Asia Pacific.

According to the World Health Organization (WHO), cancer is projected to become the leading cause of death globally in the 21st century, with approximately 20 million new cancer cases recorded in 2022. The established clinical advantages of proton and heavy ion therapy in reducing radiation dose to healthy tissue, particularly in pediatric cancers and tumors adjacent to critical structures, combined with technological advancements enabling more compact and cost-efficient system designs, are driving accelerated facility investment and patient volume growth.

Key Industry Highlights:

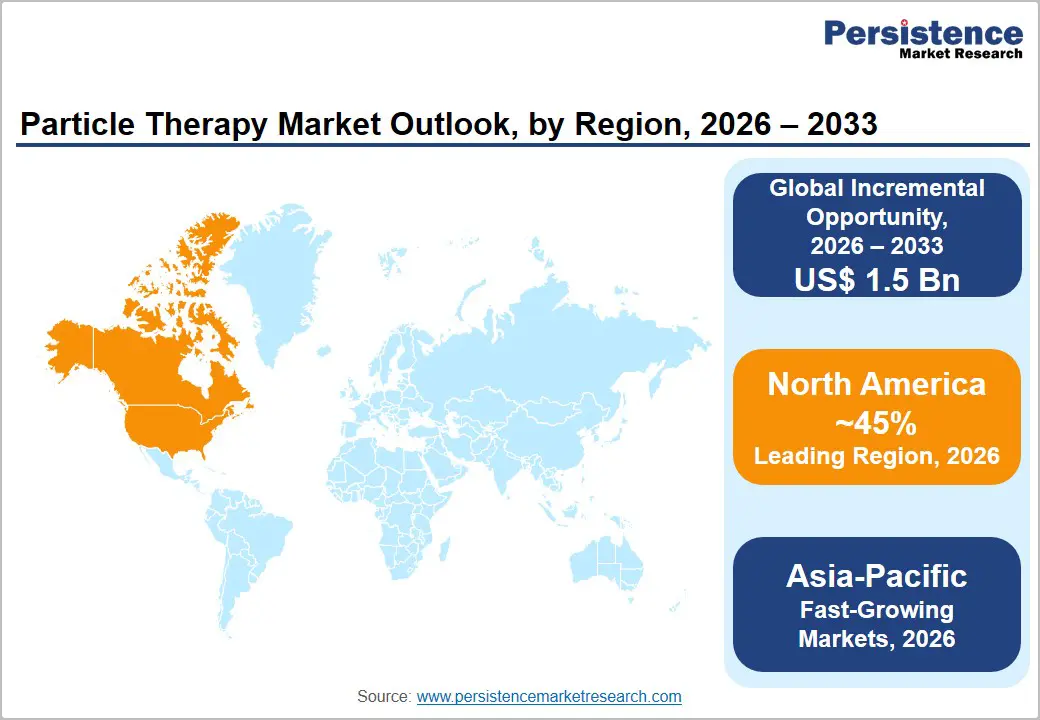

- Leading Region: North America is likely to lead the global particle therapy market with 45% share in 2026, anchored by over 40 operational proton therapy centers in the U.S., strong Medicare reimbursement coverage, and the global R&D presence of IBA Worldwide, Varian (Siemens Healthineers), and Mevion Medical Systems.

- Fastest Growing Region: Asia Pacific is projected to register the highest CAGR during 2026 - 2033, driven by China’s Healthy China 2030 proton center construction program, Japan’s carbon ion therapy leadership, India’s private oncology investment, and rapidly growing medical tourism demand across South Korea and ASEAN.

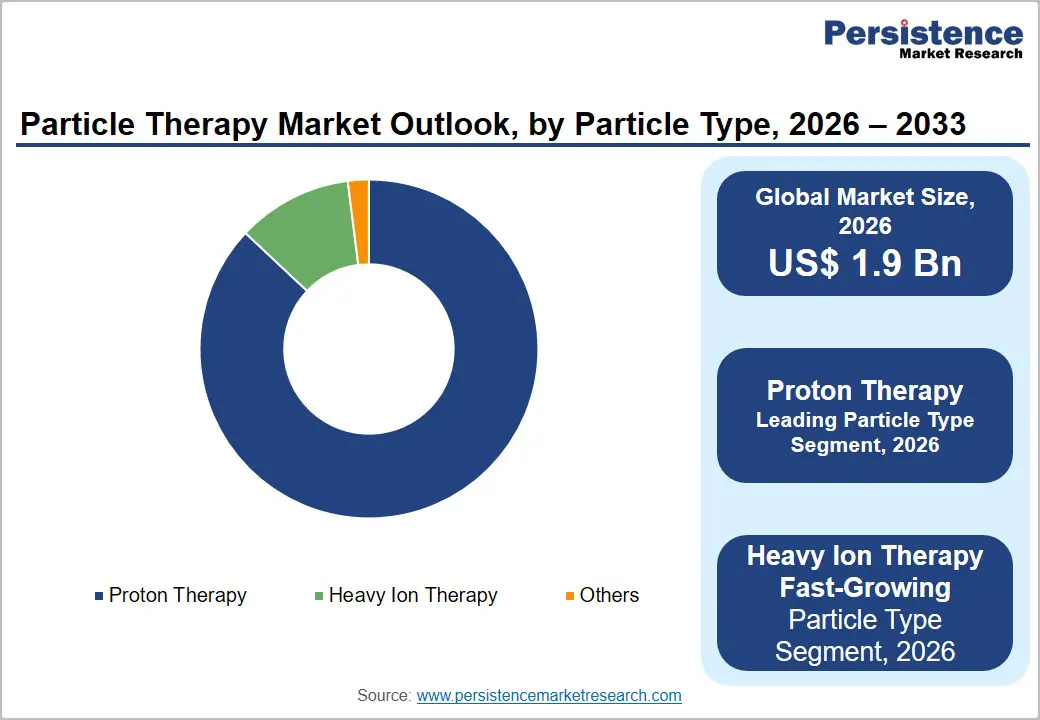

- Dominant Particle Segment: Proton Therapy commands approximately 87% market share in 2026, driven by its extensive clinical evidence base covering over 200,000 treated patients globally, broad FDA/EMA/PMDA regulatory approvals, and the availability of compact single-room systems from multiple commercial vendors enabling wider facility access.

- Fast-Growing Particle Segment: Heavy ion therapy is the fast-growing particle type segment, driven by expanding carbon ion center networks in Europe and China, growing randomized clinical evidence from NIRS-QST programs, and increasing payer recognition of its superior efficacy in radioresistant tumor indications.

- Key Opportunity: The rapid expansion of proton therapy center construction in the Asia Pacific, particularly China’s 20+ facility pipeline under Healthy China 2030, combined with compact single-room system adoption in emerging markets, represents the primary incremental revenue opportunity driving the market toward US$ 3.4 billion by 2033.

Market Dynamics

Drivers - Rise in Global Cancer Incidence and Clinical Evidence Supporting Particle Therapy Superiority

The accelerating global cancer burden is the foundational demand driver for particle therapy adoption. The International Agency for Research on Cancer (IARC) projects global cancer incidence will rise to approximately 35 million new cases annually by 2050, representing a 77% increase from 2022 levels. Particle therapy’s clinical advantages over conventional photon radiotherapy are well-documented: the Bragg peak effect enables precise energy deposition at the tumor site while sparing surrounding healthy tissue, reducing acute and late radiation toxicities.

Multiple studies published in The International Journal of Radiation Oncology, Biology, Physics confirm superior outcomes in pediatric brain tumors, base-of-skull tumors, and prostate cancer when treated with proton therapy compared to photon-based alternatives. These clinical evidence advantages are compelling oncology centers and national health systems to invest in particle therapy infrastructure as the standard of care for specific cancer indications.

Restraints - Extremely High Capital and Operational Costs Limiting Facility Deployment

The prohibitive capital cost of particle therapy systems-ranging from approximately US$ 30-50 million for single-room proton systems to over US$ 200 million for multi-room heavy ion facilities-remains the primary barrier to broader global adoption. Operational costs, including maintenance contracts, specialized physics and engineering staffing, and shielding infrastructure further elevate the total cost of ownership. In low- and middle-income countries (LMICs), where 70% of global cancer burden is concentrated per WHO data, these cost barriers effectively preclude particle therapy deployment without substantial international funding support, creating a persistent access equity gap.

Opportunities - Rapid Expansion of Proton Therapy Centers in Asia Pacific and Emerging Markets

The Asia Pacific region represents the highest-growth commercial opportunity for particle therapy system manufacturers over the forecast period. China has emerged as the most active new facility construction market globally, with government health plans under Healthy China 2030 prioritizing advanced cancer treatment infrastructure investment.

The PTCOG reports that China had over 20 proton therapy facilities in operation or advanced construction phases by 2024, with Hitachi Ltd., Sumitomo Heavy Industries Ltd., and Siemens Healthineers (Varian Medical Systems) competing aggressively for system supply contracts. India’s growing private hospital oncology investment and South Korea’s National Cancer Center expansion are additional high-growth demand centers. The ASEAN region’s increasing medical tourism for advanced oncology therapies further amplifies regional demand for new particle therapy installations through 2033.

Category-wise Analysis

Particle Type Insights

Proton therapy dominates the global market, likely to command approximately 87% share in 2026. This overwhelming leadership reflects proton therapy’s decades-long clinical development head start, extensive regulatory approvals across FDA, EMA, and PMDA jurisdictions, and the existence of over 120 operational treatment centers globally per PTCOG data. The established clinical evidence base spanning more than 200,000 patients treated with proton therapy worldwide has enabled broad payer reimbursement in the U.S., Japan, and across Europe for specific indications.

The availability of both large multi-room and compact single-room system configurations across multiple commercial vendors provides treatment centers with capital investment flexibility that the carbon ion segment currently cannot match, further entrenching proton therapy’s dominant commercial position.

System Type Insights

Cyclotron-based systems are likely to represent the leading system type segment in the particle therapy market in 2026, supported by their well-established clinical track record, broad commercial vendor ecosystem, and the dominance of Ion Beam Applications (IBA Worldwide), which markets the Proteus® series of isochronous cyclotron-based proton therapy systems globally. IBA systems are installed in a significant proportion of the world’s operational proton therapy centers, providing the company with an installed base advantage and a recurring service and upgrade revenue stream.

Cyclotron-based systems deliver continuous beam extraction with high duty cycles suited to pencil beam scanning (PBS) delivery-the current clinical standard for precision proton dose painting. However, the growing adoption of compact synchrocyclotron systems from Mevion Medical Systems is creating competitive pressure in the single-room hospital segment.

Regional Insights

North America Particle Therapy Market Trends and Insights

North America leads the particle therapy market due to high cancer burden, strong reimbursement systems, and rapid adoption of advanced proton therapy infrastructure. The region benefits from extensive clinical research networks and FDA-supported device approvals. The total market is expected to reach ~US$ 1.9 Bn by 2026, supported by increasing oncology capital investment and hospital expansion programs across the U.S. and Canada.

U.S. Particle Therapy Market Trends and Insights

The U.S. dominates due to its high number of proton therapy centers and strong insurance coverage expansion. According to the National Cancer Institute (NCI), over 2 million new cancer cases annually drive demand for precision radiotherapy. Large hospital systems like Mayo Clinic and MD Anderson have expanded particle therapy adoption. Continuous investment in oncology infrastructure and Medicare reimbursement support sustains leadership in advanced radiation technologies.

Canada Particle Therapy Market Trends and Insights

Canada is emerging due to increasing public healthcare investment and expansion of cancer treatment facilities. The Canadian Partnership Against Cancer reports rising incidence rates exceeding 230,000 new cancer cases annually, accelerating demand for precision radiation. New proton therapy planning initiatives and cross-border clinical collaborations with U.S. institutions are improving accessibility, making Canada one of the fastest-growing adopters of particle therapy technologies in North America.

Europe Particle Therapy Market Trends and Insights

Europe is a key region due to strong government-funded healthcare systems, early adoption of carbon ion therapy, and leadership in clinical research. The region’s particle therapy market is supported by national oncology programs and cross-border treatment access policies. Europe continues to expand proton and heavy ion facilities, particularly in Germany, Italy, and France, contributing significantly to global treatment capacity and technological innovation.

Germany Particle Therapy Market Trends and Insights

Germany leads Europe due to advanced heavy ion therapy infrastructure, including Heidelberg Ion Beam Therapy Center (HIT). According to German Cancer Research Center (DKFZ), cancer incidence exceeds 500,000 new cases annually, driving demand for precision radiotherapy. Germany is also a global pioneer in carbon ion therapy research, with strong public funding and integration of particle therapy into university hospital systems.

UK Particle Therapy Market Trends and Insights

The UK is rapidly expanding due to NHS-backed investments in proton therapy centers in London and Manchester. Cancer Research UK reports over 385,000 new cancer cases annually, increasing pressure on advanced radiotherapy solutions. Government-funded programs supporting international patient access and clinical trials are accelerating adoption, making the UK one of the fastest-growing particle therapy markets in Europe.

Asia Pacific Particle Therapy Market Trends and Insights

Asia Pacific is the fast-growing market due to rising cancer prevalence, rapid healthcare infrastructure expansion, and strong government investment in advanced oncology technologies. Countries like Japan, China, and South Korea are aggressively deploying proton and carbon ion therapy systems. The region is also benefiting from increasing medical tourism and domestic manufacturing of particle therapy equipment, significantly reducing treatment costs and improving accessibility.

China Particle Therapy Market Trends and Insights

China is the largest and fastest-expanding market due to large-scale cancer burden and government-backed oncology modernization programs. According to China National Cancer Center, there are over 4.8 million new cancer cases annually, one of the highest globally. Rapid installation of carbon ion and proton therapy centers in major hospitals is accelerating adoption, supported by domestic manufacturers and public-private healthcare investments.

India Particle Therapy Market Trends and Insights

India is emerging as the fastest-growing market due to rising cancer incidence and increasing demand for advanced treatment access. The Indian Council of Medical Research (ICMR) reports over 1.4 million new cancer cases annually, with growing unmet need for precision radiotherapy. Expansion of private oncology chains, medical tourism, and collaborations with global proton therapy providers are driving rapid adoption, despite high capital cost barriers.

Competitive Landscape

The global particle therapy market is highly consolidated, with a small number of specialized medical technology companies commanding the majority of system installation contracts. Ion Beam Applications (IBA Worldwide), Siemens Healthineers (Varian Medical Systems), Hitachi Ltd., and Sumitomo Heavy Industries Ltd. collectively account for the dominant share of global proton therapy system installations.

Key competitive differentiators include system reliability records, pencil beam scanning performance, compact system offerings, service network depth, and clinical outcome publications. Emerging trends include artificial intelligence-driven treatment planning integration, FLASH therapy research partnerships, and turnkey facility development financing models enabling access in capital-constrained healthcare systems.

Key Developments:

- May 2026: Ion Beam Applications (IBA) launched the Rhodotron® LITE, a new low-power X-ray accelerator designed to expand access to sustainable irradiation solutions. The company stated that the new system was developed to provide a more compact and energy-efficient alternative to traditional high-power accelerators, enabling broader adoption of irradiation technologies in medical, industrial, and research applications.

- November 2025: Fosun MedTech and Leo Cancer Care collaborated to promote a new paradigm in upright particle therapy, focusing on advancing patient positioning innovation in radiation oncology. The two companies worked together to explore and promote upright treatment systems, which allow patients to receive particle therapy in a seated or standing position rather than the traditional supine (lying down) position.

Companies Covered in Particle Therapy Market

- Ion Beam Applications (IBA Worldwide)

- Siemens Healthineers (Varian Medical Systems)

- Hitachi Ltd.

- Mevion Medical Systems

- Sumitomo Heavy Industries Ltd.

- ProTom International

- Provision Healthcare

- Advanced Oncotherapy Plc

- Mitsubishi Electric Corporation

- Toshiba Energy Systems & Solutions Corporation

- Danfysik A/S

- Shinva Medical Instrument Co., Ltd.

- China General Nuclear Power Corporation (CGN)

- Others

Frequently Asked Questions

The global particle therapy market is projected to be valued at US$ 1.9 billion in 2026.

Rising cancer prevalence, precision radiation demand, pediatric cancer cases, technology advances, reimbursement growth, and hospital investments.

North America leads with approximately 45% market share in 2026.

Expansion in emerging Asia-Pacific markets, compact systems adoption, and increasing hospital-based proton therapy centers.

Ion Beam Applications (IBA Worldwide), Siemens Healthineers (Varian Medical Systems), Hitachi Ltd., Mevion Medical Systems, Sumitomo Heavy Industries Ltd.