- Biotechnology

- GMP Biologics Market

GMP Biologics Market Size, Share, and Growth Forecast 2026 - 2033

GMP Biologics Market by Product Type (Monoclonal Antibodies, Vaccines, Recombinant Proteins, Cell & Gene Therapies), Application (Cancer, Infectious Diseases, Autoimmune Diseases, Rare Diseases), End User (Pharmaceutical Companies, Biotechnology Companies, Research Institutes), by Regional Analysis, 2026 - 2033

GMP Biologics Market Share and Trends Analysis

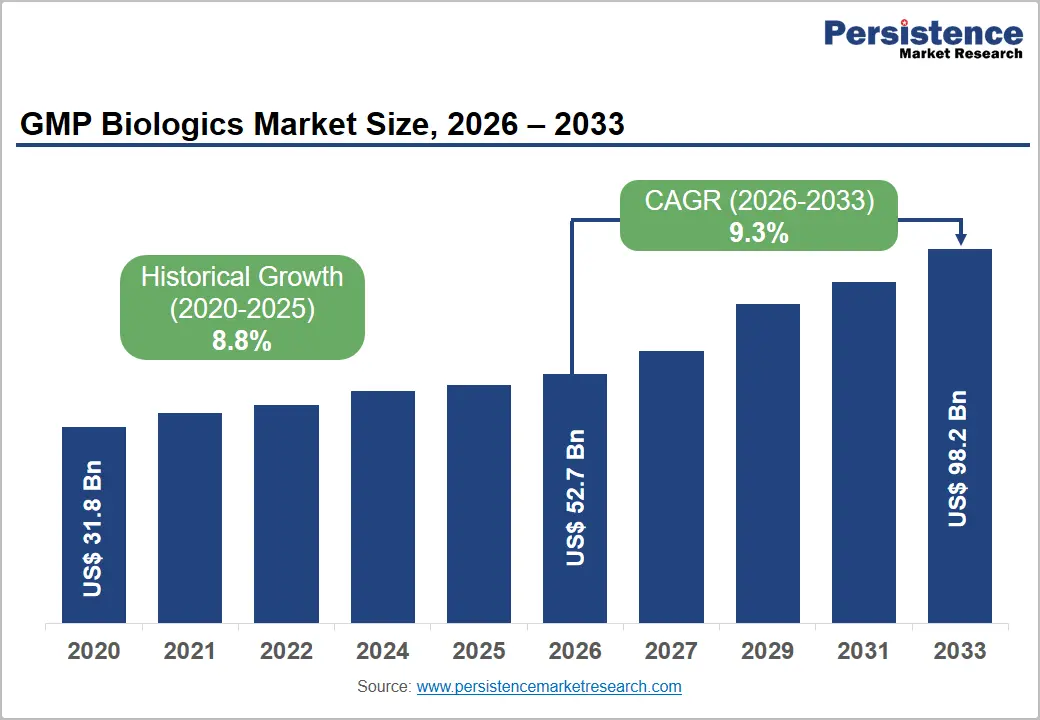

The global GMP biologics market size is expected to be valued at US$ 52.7 billion in 2026 and projected to reach US$ 98.2 billion by 2033, growing at a CAGR of 9.3% between 2026 and 2033.

The rising demand for monoclonal antibodies, cell and gene therapies, and recombinant proteins has fueled the need for GMP biologics. Increasing outsourcing of biologics manufacturing to contract development and manufacturing organizations (CDMOs) has strengthened global capacity and accelerated clinical-to-commercial transitions. Strict regulatory requirements from agencies such as the FDA and EMA have further reinforced the need for compliant GMP infrastructure. Advances in single-use technologies, continuous bioprocessing, and automated manufacturing systems are improving efficiency and scalability.

Key Industry Highlights:

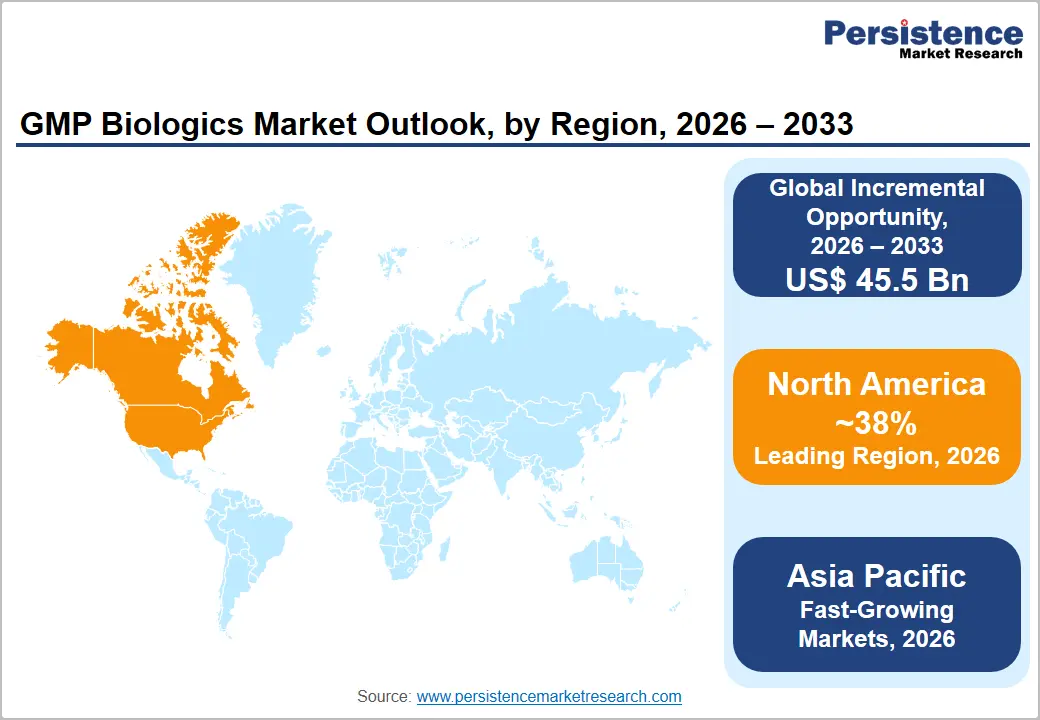

- Leading Region - North America commands approximately 38% of the global GMP biologics market in 2026, driven by US$ 102 billion in annual PhRMA R&D investment, the world's most active biologics IND/BLA pipeline, and CDMO leaders Catalent, Thermo Fisher Scientific, and KBI Biopharma.

- Fastest Growing Region - Asia Pacific is the fast-growing GMP biologics market, anchored by Samsung Biologics' 604,000-liter Songdo campus, WuXi Biologics' multi-country CDMO network, India's biosimilar manufacturing leaders, and Singapore's FDA/EMA-accepted GMP biologics manufacturing infrastructure.

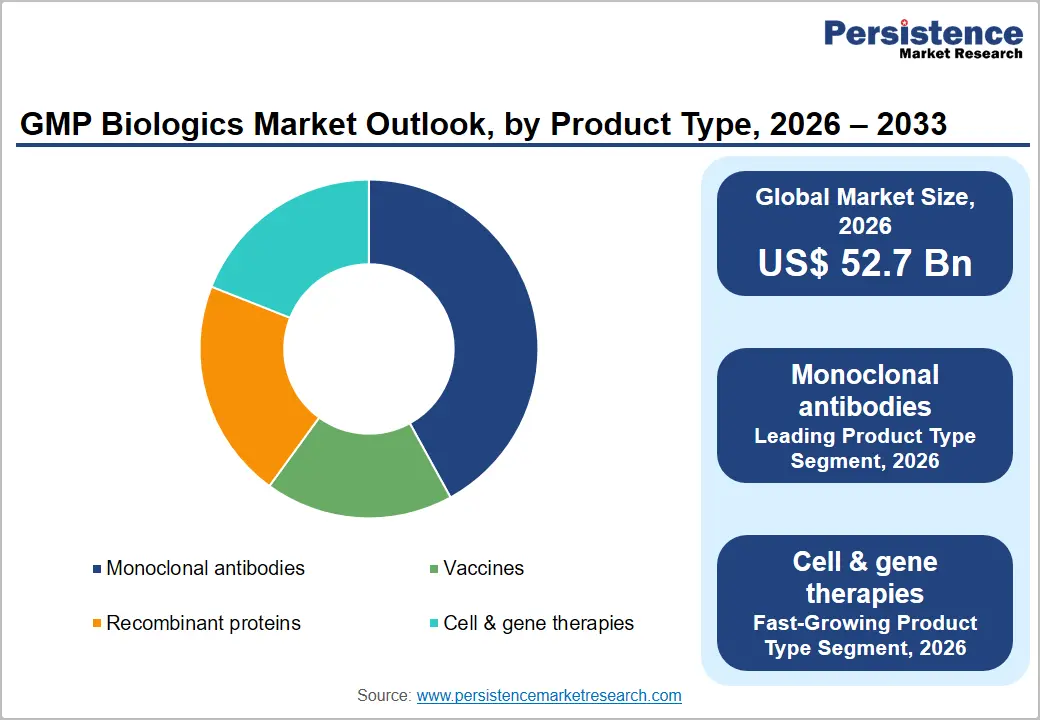

- Dominant Segment - Monoclonal antibodies hold approximately 42% of GMP biologics product type revenues in 2026, driven by blockbuster mAb franchises exceeding US$ 10B annually (Keytruda, Dupixent) and the proliferation of bispecific antibodies and ADCs expanding mAb GMP manufacturing demand.

- Fast-Growing Product Segment - Cell and gene therapies are the fastest-growing GMP biologics product type, driven by over 1,000 active clinical trials (ARM), FDA CBER projecting 10-20 annual approvals by late 2020s, and CDMOs investing billions in viral vector and cell therapy GMP manufacturing capacity.

- Key Market Opportunity - Cell & Gene Therapy GMP Manufacturing Capacity: With ARM reporting a 6-18 month capacity wait time at leading CDMOs for cell and gene therapy programs, Lonza, FUJIFILM Diosynth, and Thermo Fisher are investing billions, representing the highest-margin growth opportunity in GMP biologics manufacturing through 2033.

Market Dynamics

Drivers - Accelerating Biologics Pipeline and FDA/EMA Approval Wave Sustaining GMP Manufacturing Demand

The global biopharmaceutical pipeline has reached unprecedented scale, creating sustained and compounding demand for GMP biologics manufacturing capacity. According to IQVIA, over 3,000 biologic drug candidates are in active clinical development globally as of 2024, including monoclonal antibodies, bispecific antibodies, fusion proteins, cell therapies, and gene therapies. The FDA's Center for Biologics Evaluation and Research (CBER) has projected that 10-20 gene therapy products could be approved annually by the late 2020s, each requiring specialized GMP vector manufacturing.

The EMA has similarly established accelerated pathways, including PRIME designation, that are compressing development timelines for advanced biologics. Each new IND filing, Phase advancement, and commercial approval directly generates new GMP manufacturing contracts, creating a structural, compounding demand foundation for the GMP biologics market.

Rising Biopharmaceutical Outsourcing Trend Expanding CDMO Revenue Base

The structural shift of biopharmaceutical companies toward outsourced GMP manufacturing is a powerful secular growth driver for the GMP biologics market. PhRMA data indicate that biopharmaceutical R&D investment exceeded US$ 102 billion in 2022, with an increasing proportion of companies, particularly emerging biotech firms without owned manufacturing infrastructure, directing production to CDMOs.

The Pharmaceutical Research and Manufacturers of America (PhRMA) reports that over 5,000 medicines are in development across the U.S. biopharmaceutical pipeline. Small and mid-size biotechs, which constitute the majority of biologics pipeline sponsors, lack the capital and expertise to build GMP bioreactor suites, viral vector facilities, or sterile fill-finish capacity, making outsourcing to GMP CDMOs the operational default and sustaining long-term CDMO revenue growth.

Restraints - Severe Shortage of GMP-Qualified Cell and Gene Therapy Manufacturing Capacity

Despite rapid pipeline growth, the global supply of GMP-qualified cell and gene therapy manufacturing capacity remains critically constrained. Viral vector production required for AAV and lentiviral gene therapies demands specialized containment suites, validated upstream bioreactor processes, and analytical infrastructure that takes 3-5 years to build and validate. The Alliance for Regenerative Medicine (ARM) has identified manufacturing capacity as the leading operational bottleneck for the cell and gene therapy sector, with clinical stage programs experiencing 6-18 month manufacturing slot wait times at leading CDMOs directly constraining clinical timelines and delaying market expansion.

Opportunities - Cell and Gene Therapy GMP Manufacturing: The Fastest-Growing and Highest-Margin Segment

Cell and gene therapy GMP manufacturing represents the most commercially transformative opportunity in the GMP biologics market, offering the highest per-batch revenue and margin of any biologic modality. The Alliance for Regenerative Medicine (ARM) reported over 1,000 active cell and gene therapy clinical trials globally as of 2023, with commercial approvals accelerating. FDA CBER has projected up to 20 annual gene therapy approvals by 2025 based on pipeline maturity.

Each commercial gene therapy requires dedicated GMP viral vector manufacturing suites, creating a structural, per-approval capacity demand that far exceeds current global supply. CDMOs, including Lonza (Cocoon platform), FUJIFILM Diosynth Biotechnologies, and Thermo Fisher Scientific, are investing billions in cell and gene therapy GMP infrastructure to capture this premium manufacturing segment.

Asia Pacific GMP Biologics Manufacturing: Cost-Competitive Capacity Expansion Opportunity

Asia Pacific is emerging as a critical growth frontier for GMP biologics manufacturing, offering substantially lower facility construction and labor costs relative to North America and Europe. Samsung Biologics (South Korea) has become the world's largest single-site biopharmaceutical CDMO by capacity, with over 604,000 liters of bioreactor capacity at its Songdo campus. WuXi Biologics has built the largest global CDMO network spanning China, Ireland, and Singapore. For pharmaceutical companies seeking supply chain diversification post-COVID-19 and cost optimization for commercial-stage biologics, Asia Pacific GMP CDMOs offer an increasingly compelling value proposition with regulatory pathway acceptance from the FDA and EMA.

Category-wise Insights

Product Type Insights

Monoclonal antibodies (mAbs) represent the dominant product type in the GMP biologics market, commanding approximately 42% of global revenues in 2026. mAbs are the most commercially successful class of biologics, occupying multiple positions in the world's top-selling drug lists. Humira (AbbVie), Keytruda (Merck), and Dupixent (Sanofi/Regeneron) represent blockbuster mAb franchises generating peak revenues exceeding US$ 10 billion annually each. The manufacturing scale of mAb production requiring large-scale mammalian cell bioreactors of 10,000-25,000 liters makes mAb GMP manufacturing the highest-volume biologic production category. The rapid proliferation of bispecific antibodies, antibody-drug conjugates (ADCs), and antibody fragments is expanding the technical breadth of mAb GMP manufacturing demand beyond conventional IgG production.

Application Insights

Oncology (cancer) is the leading application segment in the GMP biologics market, accounting for approximately 44% of revenues in 2026. The dominance of oncology reflects the concentration of high-value biologic drug approvals in cancer indications, including checkpoint inhibitors, ADCs, bispecific T-cell engagers (BiTEs), and CAR-T cell therapies. The International Agency for Research on Cancer (IARC) projects global cancer incidence to reach 35 million cases by 2050, creating an expanding patient population requiring biologic treatments.

The FDA consistently approves more oncology biologics annually than in any other therapeutic area, and oncology programs command the highest development-stage manufacturing volumes, sustaining this application segment's revenue leadership in GMP biologics manufacturing.

End-user Insights

Pharmaceutical companies represent the leading end-user segment in the GMP biologics market, accounting for approximately 52% share in 2026. Large pharmaceutical companies, including Roche, Johnson & Johnson, AbbVie, Pfizer, and Merck & Co. are the primary sponsors of commercial-stage biologic drug manufacturing contracts, which represent the highest value GMP manufacturing engagements by batch size and annual contract value. Commercial supply agreements often spanning 5-10 years provide CDMOs with the most predictable and high-margin revenue streams in the GMP biologics market. Pharmaceutical companies' growing preference for outsourcing legacy biologic products to CDMOs while focusing internal manufacturing on next-generation pipeline assets is expanding their role as CDMO revenue contributors.

Regional Insights

North America GMP Biologics Market Trends and Insights

North America leads the global GMP biologics market with approximately 38% revenue share in 2025, anchored by the world's largest biopharmaceutical R&D ecosystem, the highest concentration of FDA-regulated GMP biologics manufacturing sites, and the most active commercial biologics pipeline globally. The region benefits from FDA CBER accelerated approval pathways and Breakthrough Therapy designations that compress development-to-commercialization timelines for advanced biologics, sustaining high CDMO manufacturing volumes.

U.S. GMP Biologics Market Size

The United States accounts for approximately 87% of North American GMP biologics revenues in 2026. The U.S. is the global headquarters of the majority of the world's largest biologics developers and CDMOs, including Catalent, KBI Biopharma, and Thermo Fisher Scientific (Patheon) and processes the highest number of biologic IND filings, BLA submissions, and commercial approvals annually. PhRMA reports US$ 102 billion in annual biopharmaceutical R&D investment, fueling sustained GMP manufacturing demand.

Europe GMP Biologics Market Trends and Insights

Europe is the second-largest GMP biologics market, characterized by a strong regulatory framework under EMA and nationally harmonized GMP standards, leading CDMO infrastructure, and policy support for biopharmaceutical manufacturing under the European Commission's Pharmaceutical Strategy. Switzerland (Lonza), Germany, and the U.K. are the primary GMP biologics hubs. EU GMP Annex 1 compliance upgrades are driving facility modernization investments across European CDMOs.

Germany GMP Biologics Market Size

Germany is the largest European GMP biologics market, contributing approximately 22% of regional revenues in 2026. Home to Boehringer Ingelheim BioXcellence, Rentschler Biopharma SE, and Siegfried Holding AG German operations, Germany has a dense CDMO manufacturing ecosystem. Germany's BioNTech mRNA manufacturing success and government investment in biomanufacturing capacity reinforce the country's GMP biologics leadership in Europe.

U.K. GMP Biologics Market Size

The U.K. accounts for approximately 14% of European GMP biologics revenues in 2026. Post-Brexit, the MHRA has implemented an independent regulatory framework enabling faster biologics approvals. The UK BioIndustry Association (BIA) supports a large biotech cluster in the Cambridge-London Golden Triangle, generating substantial CDMO outsourcing demand. Government investment in the Cell and Gene Therapy Catapult is building national advanced therapy manufacturing capacity.

France GMP Biologics Market Size

France represents approximately 12% of European GMP biologics revenues in 2026. Recipharm AB and 3P Biopharmaceuticals maintain significant French GMP biologics operations. France's national biopharmaceutical strategy backed by Bpifrance investment, supports domestic biologics manufacturing capacity building. Sanofi's extensive biologics manufacturing network in France further anchors the country's GMP biologics market scale.

Asia Pacific GMP Biologics Market Trends and Insights

Asia Pacific is the fastest-growing GMP biologics market, driven by Samsung Biologics' world-leading 604,000-liter Songdo bioreactor campus, WuXi Biologics' multi-country CDMO network, and rapidly expanding biosimilar and innovator biologics manufacturing in India, China, and Japan. China's NMPA harmonization with ICH guidelines has improved GMP compliance standards, enabling Chinese CDMO facilities to seek FDA and EMA regulatory acceptance for global supply.

India GMP Biologics Market Size

India's GMP biologics market is valued at approximately US$ 2.1 billion in 2026, growing rapidly, driven by its world-leading biosimilar manufacturing industry with companies such as Biocon Biologics, Dr. Reddy's Laboratories, and Serum Institute operating large GMP biologic facilities. India's PLI scheme for pharmaceuticals is incentivizing domestic GMP biologics capacity expansion, positioning India as a key global biologics CDMO destination.

Competitive Landscape

The GMP Biologics market is highly competitive and moderately consolidated, dominated by global CDMOs and large biopharma companies such as Lonza, Samsung Biologics, WuXi Biologics, Catalent, and Thermo Fisher Scientific. These players compete through capacity expansion, advanced GMP-compliant manufacturing facilities, and strategic partnerships with biotech firms. Pharmaceutical giants such as Pfizer, Roche, and Amgen strengthen competition via strong biologics pipelines and in-house production capabilities. Rising demand for biosimilars, monoclonal antibodies, and gene therapies has intensified outsourcing to CDMOs.

Key Developments

- In March 2024, AGC Biologics expanded its collaboration with Novelty Nobility to advance a bispecific antibody drug candidate through GMP manufacturing. Under the expanded agreement, AGC Biologics supported cell line development and master cell bank generation using its CHEF1 expression platform, followed by process development and preparation for GMP-scale production.

- In April 2026, WuXi Biologics secured Good Manufacturing Practice (GMP) certification from South Korea’s Ministry of Food and Drug Safety (MFDS) for three of its key manufacturing facilities following a five-day on-site inspection.

- In February 2026, NorthX Biologics entered into a strategic collaboration with Demeetra to deliver an integrated, end-to-end pathway from cell line development to GMP manufacturing for biologics candidates. The partnership combined Demeetra’s CleanCut™ CHO cell line development platform with NorthX Biologics’ GMP manufacturing, process scale-up, and fill-finish capabilities.

Companies Covered in GMP Biologics Market

- Lonza Group

- Samsung Biologics

- WuXi Biologics

- Catalent Inc.

- FUJIFILM Diosynth Biotechnologies

- Boehringer Ingelheim BioXcellence

- Thermo Fisher Scientific (Patheon)

- AGC Biologics

- Rentschler Biopharma SE

- Recipharm AB

- KBI Biopharma

- Siegfried Holding AG

- 3P Biopharmaceuticals

Frequently Asked Questions

The global GMP biologics market is projected to be valued at US$ 52.7 billion in 2026.

Strong expansion in monoclonal antibodies, recombinant proteins, vaccines, and advanced therapies (cell & gene therapy) is increasing GMP manufacturing demand.

North America leads with approximately 38% market share in 2025, driven by the United States' US$ 102 billion biopharmaceutical R&D base (PhRMA), the world's highest concentration of biologics IND/BLA filings, FDA CBER accelerated approval pathways, and commercial CDMO leaders Catalent, KBI Biopharma, and Thermo Fisher Scientific (Patheon) operating FDA-inspected GMP biologics facilities.

Expanding use of monoclonal antibodies, vaccines, recombinant proteins, and biosimilars is creating strong GMP manufacturing demand, especially as more products gain regulatory approvals.

The leading companies include Lonza Group, Samsung Biologics, WuXi Biologics, and Catalent Inc.