- Medical Devices

- Hernia Repair Devices Market

Hernia Repair Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Hernia Repair Devices Market by Product (Hernia Mesh, Hernia Fixation Devices, and Others), Surgery Type (Open Surgery, Laparoscopic Surgery, and Robotic-Assisted Surgery), Hernia Type (Inguinal Hernia, Incisional Hernia, Umbilical Hernia, Femoral Hernia, Hiatal Hernia, and Others) End-user (Hospitals, Clinics, Ambulatory Surgical Centers (ASCs), and Specialty Surgical Centers), and Regional Analysis from 2026 to 2033

Hernia Repair Devices Market Share and Trend Analysis

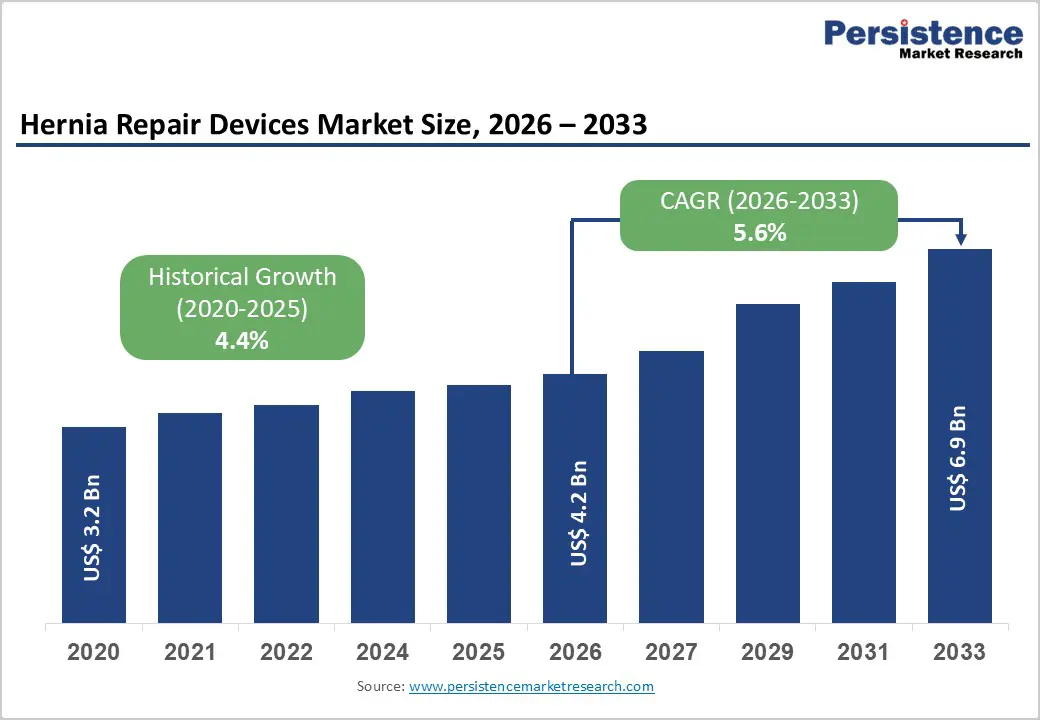

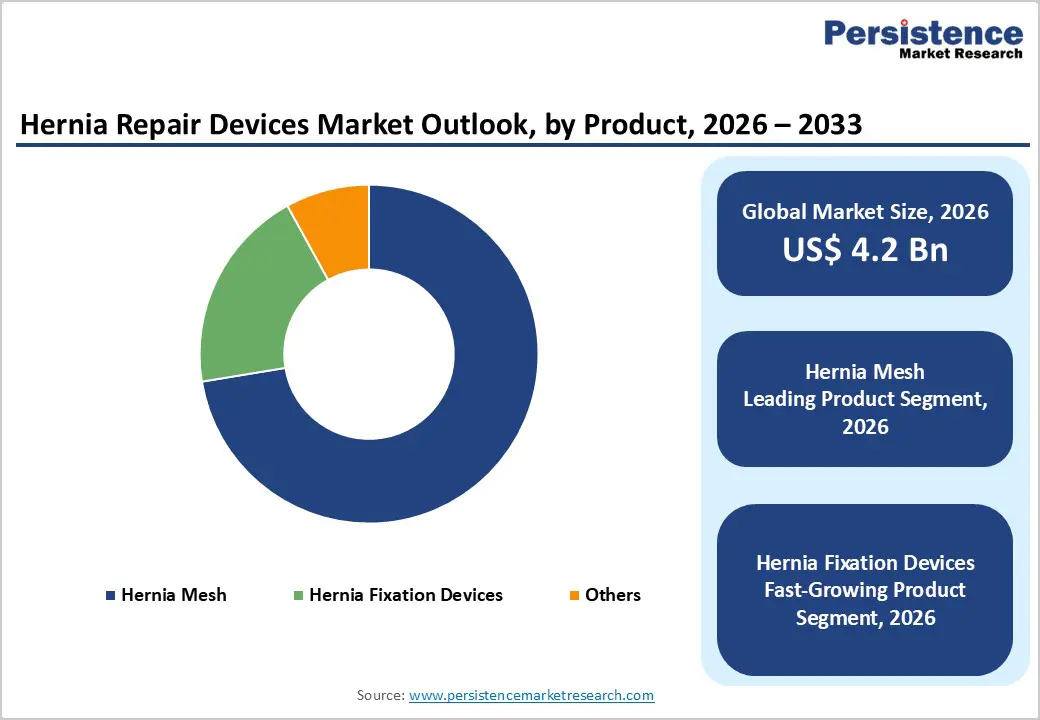

The global hernia repair devices market size is estimated to grow from US$ 4.2 billion in 2026 to US$ 6.9 billion by 2033. The market is projected to record a CAGR of 5.6% during the forecast period from 2026 to 2033.

The growing global incidence of hernia conditions, particularly inguinal and incisional types, is significantly accelerating demand for advanced repair devices. Surgical intervention remains the only definitive treatment, making device utilization directly proportional to procedure volumes.

Increasing preference for tension-free repair techniques has positioned mesh-based solutions as the clinical standard due to their ability to reduce recurrence and improve patient outcomes. In addition, the rising adoption of minimally invasive approaches, including laparoscopic and robotic-assisted surgeries, is driving demand for specialized meshes and fixation devices.

Key Industry Highlights:

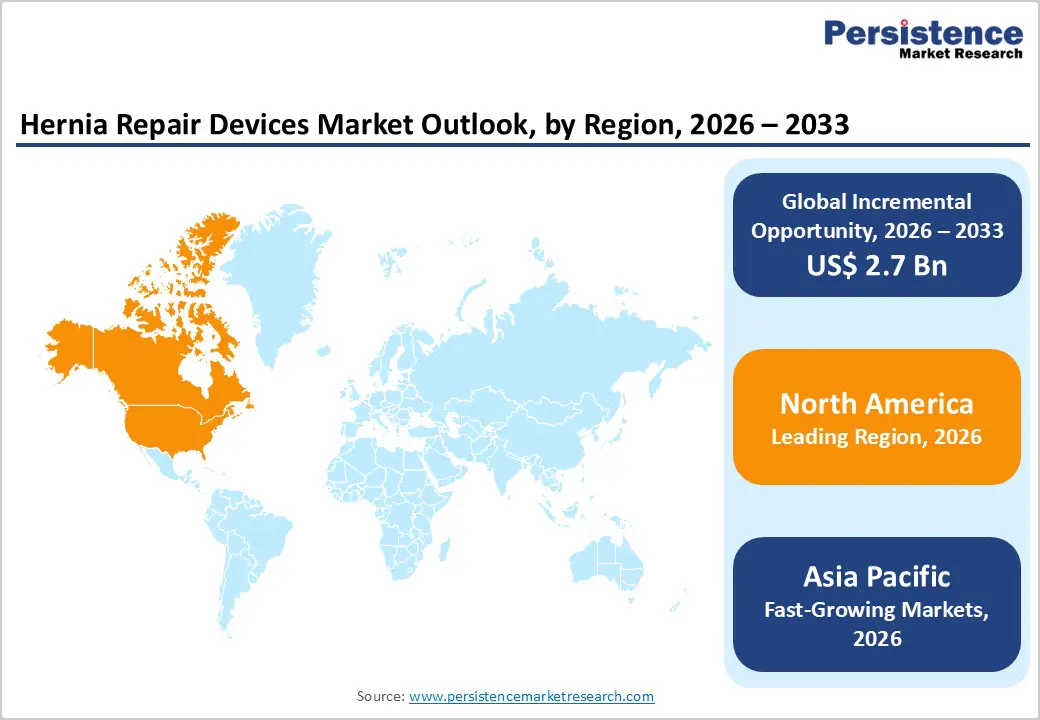

- Leading Region: North America holds 48.5% share, supported by high surgical volumes, advanced healthcare infrastructure, favorable reimbursement systems, and early adoption of minimally invasive and robotic-assisted hernia repair techniques.

- Fastest-Growing Market: Asia Pacific is the most rapidly expanding market, driven by a rising patient pool, increasing healthcare investments, expanding private hospital networks, and growing adoption of laparoscopic procedures across emerging economies.

- Leading Product Segment: Hernia mesh dominates with 72.4% due to its established role in tension-free repair, reduced recurrence rates, and strong clinical preference across both open and minimally invasive procedures.

- Leading Surgery Type Segment: Open surgery accounts for 68.7%, supported by its procedural simplicity, cost-effectiveness, widespread availability, and continued reliance in high-volume and resource-constrained healthcare settings.

Market Dynamics Analysis

Driver - Increasing Surgical Volume and Preference for Tension-Free Repair Driving Adoption

A steady rise in hernia incidence, particularly inguinal and incisional types, is significantly increasing the global volume of repair procedures. Contributing factors such as aging populations, obesity, and post-operative complications from prior abdominal surgeries are expanding the patient pool requiring intervention. Modern clinical practice strongly favors tension-free repair techniques, where mesh implantation has become the gold standard due to its ability to reduce recurrence rates and improve long-term outcomes. Surgeons increasingly rely on advanced mesh materials, including lightweight, composite, and partially absorbable variants, which enhance biocompatibility and minimize complications such as chronic pain and infection.

The growing penetration of minimally invasive procedures, including laparoscopic and robotic-assisted surgeries, is further accelerating device utilization, particularly fixation systems and specialized meshes. Improvements in surgical training, better reimbursement frameworks in developed regions, and expanding healthcare access in emerging markets are also contributing to higher procedural uptake.

Continuous product innovation, combined with strong clinical evidence supporting mesh-based repair, is reinforcing adoption across diverse healthcare settings, ensuring sustained growth momentum for device manufacturers.

Restraint - Post-Surgical Complications and Cost Constraints Limiting Wider Adoption

Despite significant advancements, several challenges continue to hinder broader adoption of hernia repair devices. One of the primary concerns is the risk of post-operative complications associated with mesh implants, including infection, adhesion formation, chronic pain, and, in some cases, mesh migration or rejection. These complications not only impact patient outcomes but also lead to increased medico-legal scrutiny and product recalls, affecting physician confidence and adoption rates.s

The cost burden associated with advanced mesh products, biologic materials, and robotic-assisted procedures remains high, particularly in price-sensitive markets. Limited reimbursement coverage in certain regions further restricts access to premium devices, pushing healthcare providers toward conventional and lower-cost alternatives.

Variability in surgical expertise, especially in minimally invasive techniques, can also influence procedural success and device utilization. Furthermore, stringent regulatory approval processes for new materials and designs increase time-to-market and development costs for manufacturers. These combined factors create operational and financial barriers, slowing the pace of adoption despite clear clinical benefits.

Opportunities - Technological Advancements and Expansion in Emerging Economies Creating Growth Pathways

Rapid innovation in biomaterials and surgical technologies is opening new avenues for growth across the hernia repair landscape. Development of next-generation meshes, including bioresorbable, antimicrobial-coated, and patient-specific designs, is addressing longstanding concerns related to infection, foreign body response, and long-term complications. At the same time, increasing adoption of robotic-assisted and laparoscopic techniques is creating demand for advanced fixation devices and precision-engineered implants.

Emerging economies across Asia-Pacific, Latin America, and parts of the Middle East present significant untapped potential due to rising healthcare expenditure, improving surgical infrastructure, and growing awareness of early hernia treatment. Expansion of private healthcare providers and ambulatory surgical centers is also improving accessibility and procedural volumes in these regions.

Strategic collaborations between device manufacturers and healthcare institutions are accelerating product penetration and training initiatives. Digital integration, including preoperative planning tools and simulation-based training, is further enhancing surgical outcomes. Collectively, these factors are positioning the market for long-term, innovation-driven expansion.

Category-wise Analysis

By Product Insights

Hernia mesh is projected to dominate the global hernia repair devices market in 2026, accounting for 72.4% of total revenue, primarily due to its established role as the standard-of-care in hernia repair procedures. Its widespread adoption is driven by the ability to reinforce weakened tissue, reduce recurrence rates, and improve long-term surgical outcomes compared to suture-only techniques.

Synthetic and biologic meshes are increasingly used depending on patient condition and infection risk, enabling broader clinical applicability. Advancements in lightweight, composite, and absorbable mesh designs are further enhancing patient comfort and reducing post-operative complications such as chronic pain and adhesion formation.

The growing volume of hernia procedures globally, particularly in aging population, continues to drive demand. Strong surgeon preference, extensive clinical validation, and continuous product innovation collectively reinforce mesh as the cornerstone of modern hernia repair.

By Surgery Type Insights

Open surgery is expected to lead the global hernia repair devices market with a 68.7% revenue share in 2026, supported by its widespread use across both developed and emerging healthcare systems. The approach remains highly preferred for its procedural simplicity, lower equipment requirements, and cost-effectiveness, particularly in regions with limited access to advanced surgical infrastructure.

Open repair is commonly performed for inguinal and incisional hernias and is often favored in complex or recurrent cases where direct visualization is critical. Despite the increasing adoption of laparoscopic and robotic-assisted techniques, open surgery continues to account for the majority of procedures due to its shorter learning curve and broad surgeon familiarity.

In addition, high patient volumes in public healthcare systems and outpatient settings further sustain its dominance. Ongoing improvements in surgical techniques and mesh placement strategies continue to enhance outcomes, ensuring its continued relevance in the global market.

By End User, Hospitals Dominate Supported by High Surgical Throughput and Advanced Surgical Infrastructure

Hospitals are projected to account for 61.8% of the global hernia repair devices market in 2026, driven by their role as primary centers for surgical interventions and access to comprehensive healthcare infrastructure. These facilities handle a large share of both elective and emergency hernia procedures, supported by the availability of skilled surgeons, advanced operating rooms, and post-operative care capabilities.

Hospitals are also more likely to adopt advanced technologies such as laparoscopic and robotic-assisted systems, increasing the utilization of premium meshes and fixation devices. Furthermore, favorable reimbursement frameworks in developed markets and higher patient inflow contribute to sustained demand. Complex cases, including recurrent and large incisional hernias, are predominantly treated in hospital settings, further reinforcing their dominance. Continuous investments in surgical capacity expansion and technology upgrades ensure that hospitals remain the central hub for hernia repair procedures globally.

Region-wise Insights

North America Hernia Repair Devices Market Trends

North America accounts for 47.8% of the global hernia repair devices market in 2026, driven by high surgical volumes, strong reimbursement frameworks, and early adoption of advanced mesh and minimally invasive techniques. The region benefits from a high prevalence of inguinal and incisional hernias and robust hospital infrastructure. Increasing preference for laparoscopic and robotic-assisted procedures, along with continuous product innovation, supports growth. The U.S. dominates with 78.6%, while Canada contributes 13.2%, reflecting stable but slower expansion compared to outpatient-focused markets.

U.S. Hernia Repair Devices Market Trends

The U.S. leads North America with approximately 78.6% share, driven by high procedure volumes and rapid adoption of laparoscopic and robotic-assisted hernia repair. Growth is supported by strong reimbursement systems, widespread use of synthetic and biologic mesh, and the presence of leading manufacturers. The increasing shift toward outpatient surgeries and ambulatory surgical centers is improving procedural efficiency and cost outcomes, further strengthening market expansion.

Canada Hernia Repair Devices Market Trends

Canada accounts for around 13.2% of the regional market, supported by a well-established public healthcare system and growing adoption of minimally invasive surgeries. Demand is driven by a rising aging population and an increasing incidence of abdominal hernias. Expansion of surgical capabilities and gradual uptake of advanced mesh technologies are supporting steady growth, although budget constraints and longer procedural wait times moderately limit faster adoption.

Europe Hernia Repair Devices Market Trends

Europe holds approximately 27.8% of the global market, characterized by strong regulatory frameworks and high adoption of tension-free mesh repair techniques. Growth is driven by an increasing geriatric population, rising awareness of early surgical intervention, and the expansion of minimally invasive procedures. Countries such as Germany (25.1%) and the UK (16.4%) lead regional demand. However, pricing pressures and stringent MDR regulations slightly impact product approvals and commercialization timelines across the region.

Germany Hernia Repair Devices Market Trends

Germany dominates Europe with about 25.1% share, supported by an advanced healthcare infrastructure and high surgical volumes. The country shows strong adoption of laparoscopic hernia repair and premium mesh products. Growth is further driven by increasing focus on reducing recurrence rates and post-operative complications. Presence of leading medical device manufacturers and strong reimbursement policies continue to support sustained market expansion.

United Kingdom Hernia Repair Devices Market Trends

The UK accounts for nearly 16.4% of the European market, driven by a well-established public healthcare system and increasing adoption of minimally invasive techniques. Growth is supported by rising demand for cost-effective surgical solutions and the expansion of day-care surgeries. Government initiatives to reduce surgical backlogs and improve access to elective procedures are further contributing to steady demand for hernia repair devices.

Asia Pacific Hernia Repair Devices Market Trends

Asia Pacific is the fastest-growing region, accounting for 15.3% of the global market in 2026. Growth is driven by a large patient pool, increasing healthcare expenditure, and rising adoption of mesh-based repair techniques. Expanding private healthcare infrastructure and medical tourism further accelerate demand. China leads with 39.4%, followed by India at 13.7%, reflecting strong procedural growth and improving access to advanced surgical technologies across emerging economies.

China Hernia Repair Devices Market Trends

China holds approximately 39.4% share in the Asia Pacific, driven by a large patient population and rapid expansion of hospital infrastructure. Growth is supported by increasing adoption of synthetic mesh and minimally invasive procedures. Government healthcare reforms and rising investments in surgical capabilities are improving access to hernia repair procedures, positioning China as a key growth engine in the region.

India Hernia Repair Devices Market Trends

India accounts for around 13.7% of the regional market, driven by rising awareness, increasing surgical volumes, and the expanding private healthcare sector. Growth is supported by cost-effective treatment options and growing adoption of laparoscopic repair techniques. Increasing penetration of ambulatory surgical centers and improving insurance coverage are further enhancing access to hernia repair procedures across urban and semi-urban areas.

Competitive Landscape

The global hernia repair devices market is highly competitive, with strong participation from AbbVie Inc., B. Braun SE, Baxter, BD, and Cook Medical. These companies leverage advanced mesh technologies, fixation innovations, and minimally invasive surgical solutions to improve patient outcomes and procedural efficiency.

Rising demand for tension-free repair techniques and laparoscopic procedures is driving innovation in biologic meshes and absorbable fixation devices. Market players are expanding strategic collaborations, global distribution networks, and R&D investments to deliver cost-effective, durable, and clinically effective hernia repair solutions across diverse healthcare settings.

Key Industry Developments:

- In October 2025, TI Medical introduced its next-generation hernia repair mesh, HIPO, reinforcing its position in advanced surgical innovation. The launch saw participation from leading laparoscopic and gastrointestinal surgeons across India, highlighting the product’s clinical relevance. This development reflects the company’s focus on delivering precision-engineered solutions aimed at enhancing surgical performance, improving patient outcomes, and optimizing procedural efficiency.

- In June 2025, TELA Bio, Inc. announced the European launch of its OviTex Inguinal Reinforced Tissue Matrix, a product specifically designed for laparoscopic and robotic-assisted inguinal hernia repair. The solution is positioned as a reinforced tissue matrix tailored to enhance performance in minimally invasive surgical procedures.

- In April 2025, BD announced that it received 510(k) clearance from the U.S. Food and Drug Administration for its Phasix™ ST Umbilical Hernia Patch and subsequently initiated its commercial launch. The product is recognized as the first fully absorbable hernia patch specifically developed for the treatment of umbilical hernias.

Hernia Repair Devices Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.2 Mn |

| Current Market Value (2026) | US$ 4.2 Mn |

| Projected Market Value (2033) | US$ 6.9 Mn |

| CAGR (2026 - 2033) | 5.6% |

| Leading Region | North America, 47.8% share |

| Dominant Hernia Type | Inguinal Hernia 64.3% share |

| Top-ranking Product | Hernia Mesh, 72.4% |

| Incremental Opportunity | US$ 2.7 Mn |

Companies Covered in Hernia Repair Devices Market

- AbbVie Inc.

- B. Braun SE

- Baxter

- BD

- Cook Medical

- Johnson & Johnson Services, Inc.

- FEG Textiltechnik mbH

- Integra LifeSciences Corporation

- Medtronic

- Meril Life Sciences Pvt. Ltd.

- W. L. Gore & Associates, Inc.

- Getinge AB

- TELA Bio, Inc.

- Herniamesh S.r.l.

- LifeNet Health

- Others

Frequently Asked Questions

The global hernia repair devices market is projected to be valued at US$ 4.2 Bn in 2026.

Rising prevalence of hernia cases, increasing adoption of mesh-based and minimally invasive surgeries, and a growing aging population drive market growth.

The global hernia repair devices market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Expansion of robotic-assisted procedures, innovation in biologic and absorbable meshes, and an increasing shift toward ambulatory surgical centers create growth opportunities.

AbbVie Inc., B. Braun SE, Baxter, BD, and Cook Medical are some of the key players in the hernia repair devices market.