- Food Ingredients & Additives

- Strawberry Puree Market

Strawberry Puree Market Size, Share, and Growth Forecast, 2026 - 2033

Strawberry Puree Market by Nature (Conventional, Organic), Processing Type (Concentrated, Non-Concentrated/NFC), Application (Beverages, Baby Food, Others), and Regional Analysis 2026 - 2033

Strawberry Puree Market Size and Trends Analysis

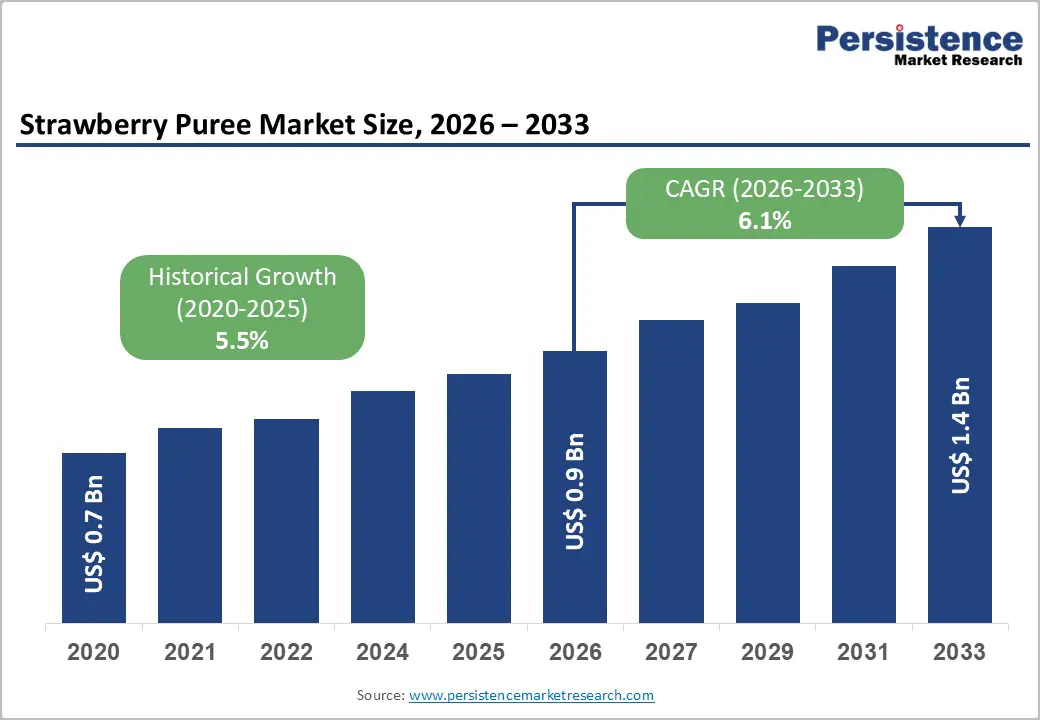

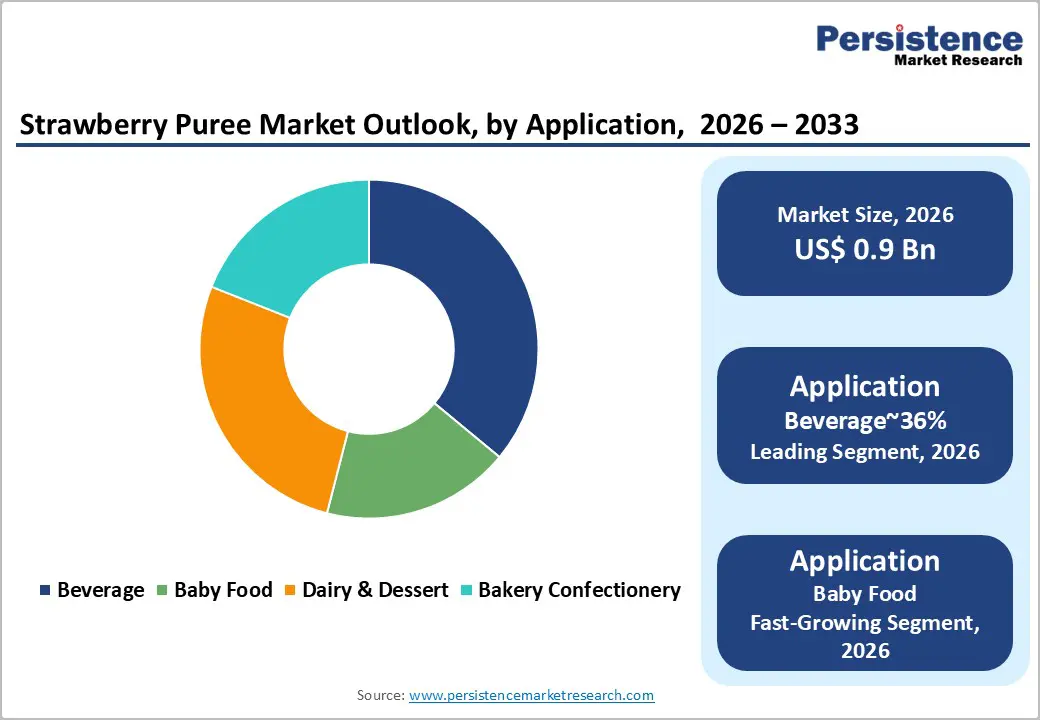

The global strawberry puree market size is likely to be valued at US$0.9 billion in 2026 and is expected to reach US$1.4 billion by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033, driven by the rising demand for natural ingredients in beverages and baby food, with beverages and baby food expanding fastest due to clean-label weaning products.

Macroeconomic indicators reveal a pronounced consumer preference for natural flavoring and coloring agents over synthetic alternatives, directly augmenting industrial consumption. Strategic product formulations in the baby food and premium beverage sectors serve as the foundational pillars sustaining this upward growth trajectory.

Key Industry Highlights:

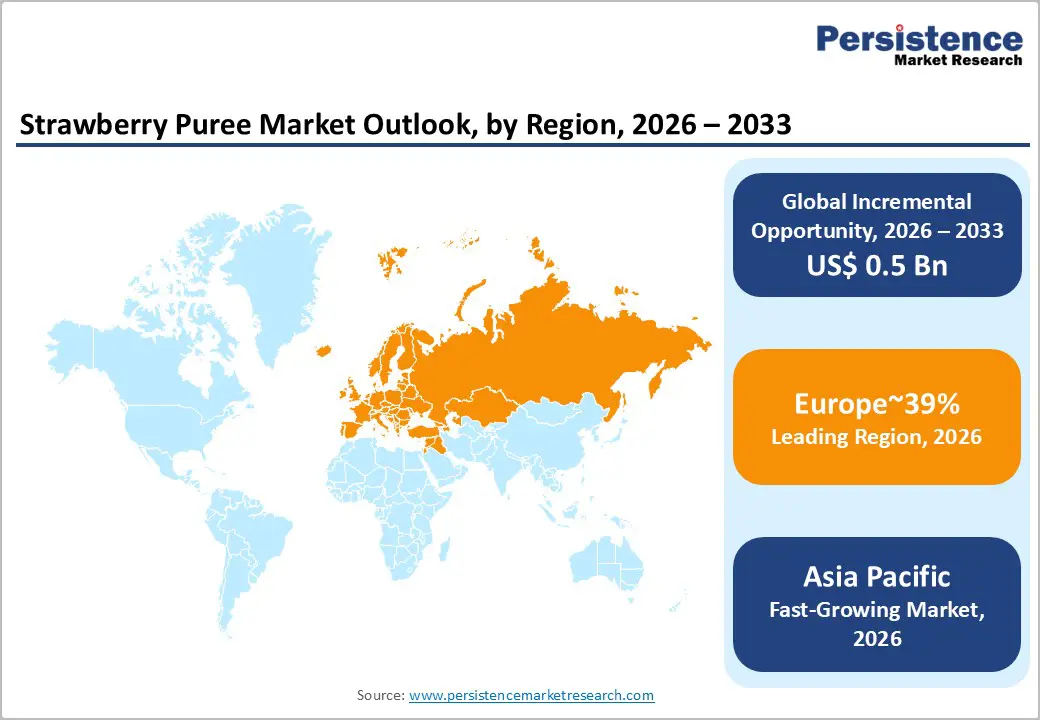

- Leading Region: Europe is projected to lead due to mature bakery, dairy, and confectionery ecosystems accounting for approximately 39% share in 2026, advanced processing technologies, and integrated fruit supply networks. Adoption is reinforced by R&D investments, harmonized regulations, major players such as AGRANA and Andros, and high-value applications in yogurt and desserts, sustaining structural market positioning.

- Fastest-Growing Region: Asia Pacific is anticipated to grow fastest due to rapid industrial growth, policy support for food safety and quality standards, and adoption across dairy, beverage, and bakery sectors. Key countries are expected to drive adoption through manufacturing scale, premium infant nutrition demand, and infrastructure initiatives, particularly in China, India, and ASEAN economies.

- Leading Nature Segment: Conventional strawberry puree is expected to lead, accounting for approximately 78% share in 2026, driven by industrial adoption, throughput efficiency, consistent quality, and high-volume applications across beverages and dairy.

- Leading Application: Beverages are projected to dominate, driven by versatility, cost efficiency, and suitability across RTD, functional drinks, and flavored water portfolios, with approximately 36% share in 2026.

| Key Insights | Details |

|---|---|

|

Strawberry Puree Market Size (2026E) |

US$0.9 Bn |

|

Market Value Forecast (2033F) |

US$1.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Escalating Clean Label Reformulation across Food and Beverage

The global transition toward transparent ingredient declarations is structurally reinforcing demand for strawberry puree across processed food categories. Regulatory scrutiny over synthetic additives and artificial flavor systems is compelling manufacturers to redesign formulations using fruit-derived inputs. Clean-label positioning is increasingly influencing procurement strategies across the beverage, dairy, and confectionery value chains. Strawberry puree functions simultaneously as a natural colorant, flavor enhancer, and intrinsic sweetening agent. Public health advocacy for reduced refined sugar consumption further strengthens reliance on fruit-based carbohydrate profiles. This substitution dynamic reconfigures ingredient hierarchies within industrial recipe development frameworks. As labeling compliance and consumer trust become commercially decisive, puree integration supports the preservation of brand equity. Consequently, natural ingredient sourcing is transitioning from discretionary differentiation to a structural necessity for formulation.

This reformulation shift alters cost structures and sourcing priorities across processing ecosystems. Manufacturers increasingly secure vertically integrated fruit supply contracts to stabilize quality and traceability standards. Processing technologies such as aseptic handling and cold-chain optimization gain strategic relevance under clean-label mandates. Regulatory alignment across international markets reinforces standardized documentation for origin, purity, and additive exclusion. Margin structures are influenced by premium raw material inputs offset by brand positioning advantages. Technology-enabled preservation techniques help maintain sensory integrity without the use of chemical stabilizers. Retailers and private labels embed natural-ingredient benchmarks into supplier qualification criteria. Collectively, these forces embed strawberry puree within long-term reformulation roadmaps across global food systems.

Advancements in Processing Technologies Enhancing Product Integrity

Technological advancements in fruit processing are significantly enhancing the competitive edge of strawberry puree. The adoption of Not From Concentrate (NFC) processing is growing among premium manufacturers aiming for better flavor preservation and greater sensory authenticity. This method minimizes thermal degradation, thereby preserving volatile aroma compounds and natural color stability. Regulatory harmonization across European markets is reinforcing standardized safety and compositional benchmarks for fruit derivatives. Unified compliance frameworks reduce cross-border certification frictions and improve trade predictability within the regional supply chain. Concurrently, cold-chain optimization technologies are mitigating risks of microbial degradation and post-processing spoilage. These infrastructure upgrades enhance shelf stability without reliance on synthetic preservatives.

Advanced processing architectures recalibrate cost structures and inventory management strategies. Improved preservation efficiency reduces waste intensity, strengthening processor margins and throughput predictability. Harmonized regulatory standards lower compliance duplication costs for exporters operating across multiple jurisdictions. Premium positioning enabled by NFC technology supports price realization within artisanal and specialty product segments. Cold-chain investments also stabilize seasonal procurement cycles by extending usable product windows. This reduces exposure to raw material volatility linked to harvest variability. Technology-driven quality assurance enhances retailer confidence and procurement continuity.

Barrier Analysis - Competitive Displacement from Synthetic Flavor and Color Systems

Strawberry puree faces sustained competitive pressure from low-cost synthetic flavoring systems. Artificial alternatives provide chemical uniformity, simplified storage, and extended shelf stability. These attributes materially reduce logistics complexity compared with temperature-sensitive fruit derivatives. Mass market manufacturers prioritize input predictability to protect production continuity and pricing structures. Synthetic esters replicate sensory characteristics without exposure to risks associated with agricultural variability. Natural puree, by contrast, reflects fluctuations in harvest quality and ripeness parameters. This variability introduces formulation-recalibration costs in standardized industrial processing environments. Cost-sensitive segments often default toward synthetics to safeguard margin stability.

The economic divergence between authenticity and affordability reshapes procurement behavior across value chains. Synthetic concentrates eliminate cold-chain dependencies, reducing transportation and inventory-holding costs. Natural puree requires controlled storage, increasing working capital intensity and operational overhead. Uniform sensory output from artificial inputs simplifies quality assurance and batch consistency protocols. Processors thus avoid reformulation cycles triggered by seasonal compositional variation. In response, puree suppliers emphasize clean label positioning and non-synthetic preservation technologies. High-pressure and aseptic systems extend usability while maintaining additive-free claims. These technological adaptations partially mitigate competitive disadvantages against petrochemical-derived substitutes.

Perishability Constraints and Cold Chain Infrastructure Gaps

The inherent fragility of strawberries creates structural vulnerabilities within upstream supply chains. Rapid post-harvest degradation necessitates immediate temperature-controlled handling and transport protocols. Any interruption in cooling continuity accelerates microbial growth and enzymatic deterioration. This sensitivity elevates operational complexity from farm aggregation to processing facilities. Cold chain dependency increases capital intensity across storage, transport, and handling nodes. Inadequate infrastructure amplifies spoilage risk and reduces the yield of usable raw material. Quality variability directly affects puree consistency, safety compliance, and downstream manufacturing performance. Perishability embeds cost volatility and throughput uncertainty across the value chain.

Limited refrigerated logistics restrict scalable procurement networks and export readiness. Small-scale producers often lack access to advanced storage, grading, and rapid pre-cooling systems. Infrastructure gaps undermine adherence to international sanitary and phytosanitary certification frameworks. Export-oriented processors face rejection risks when temperature compliance documentation is insufficient. Elevated spoilage rates compress processor margins and inflate insurance and waste management expenditures. Cold chain investment requirements raise entry barriers for emerging suppliers. Technology adoption remains uneven due to financing constraints and fragmented farm structures. These systemic limitations structurally constrain global supply reliability for strawberry puree markets.

Opportunity Analysis - Organic and NFC Premiumization within Clean Label

Premiumization anchored in organic certification and NFC (Not From Concentrate) processing is expanding structural headroom for strawberry puree differentiation. Consumer preference for minimally processed fruit ingredients reinforces demand for traceable agricultural sourcing models. Organic positioning embeds compliance with pesticide residue standards and sustainability disclosure frameworks. NFC processing preserves volatile compounds, thereby strengthening sensory authenticity and clean-label credibility. Together, these attributes elevate perceived product integrity across dairy, beverage, and infant nutrition segments. Retailers increasingly integrate organic and minimally processed benchmarks into supplier qualification matrices. This shift reallocates demand toward processors capable of maintaining segregation and certification integrity. Consequently, premium subsegments generate higher value realization relative to conventional concentrate categories.

Organic and NFC adoption reconfigures procurement, processing, and margin architectures. Certified cultivation requires controlled input management and audited farm-level documentation systems. Segregated processing lines and traceability software increase operational sophistication and fixed cost intensity. However, premium price realization offsets compliance expenditures and strengthens brand positioning leverage. Regulatory recognition of organic standards enhances acceptance of cross-border trade and harmonization of labeling. NFC technologies reduce thermal exposure, preserving nutritional and organoleptic properties without synthetic stabilizers. These structural advantages support portfolio diversification across high-value applications. Premiumization, therefore, represents a durable pathway for margin expansion within strawberry puree markets.

Aseptic Packaging and Shelf Life Extension Technologies

Advancements in aseptic packaging are structurally reshaping logistics within the strawberry puree ecosystem. Sterile filling and hermetic sealing technologies minimize the risk of microbial contamination during post-processing handling. These systems materially reduce reliance on continuous freezing across storage and transport networks. Lower temperature dependence reduces energy intensity and operating expenses across distribution channels. Extended shelf stability enables a broader geographic reach without the integration of chemical preservatives. Retail and food service operators benefit from improved inventory flexibility and reduced exposure to spoilage. Packaging innovation, therefore, aligns product integrity with evolving clean label compliance expectations. This convergence enhances the viability of trade across infrastructure-constrained and temperature-sensitive markets.

Aseptic adoption reconfigures capital allocation and margin dynamics. Processors invest in sterile environments, automated filling lines, and barrier-optimized materials. Reduced cold-chain burden lowers downstream logistics costs and carbon-exposure liabilities. Longer shelf windows facilitate export expansion into regions with limited refrigeration capacity. Regulatory frameworks governing food safety increasingly recognize validated aseptic protocols as compliance enablers. Improved storage resilience strengthens procurement planning and working capital efficiency. Packaging differentiation also enhances private label participation within organized retail systems. Mutually, shelf life extension technologies unlock scalable growth pathways across fragmented global markets.

Category-wise Analysis

Nature Insights

The conventional segment is projected to dominate the market, by accounting for approximately 78% share in 2026, underpinned by entrenched integration across high-volume beverage and dairy manufacturing ecosystems. Its dominance reflects scale efficiencies, established agricultural supply chains, and cost-optimized pasteurization infrastructure supporting mass-market production. Processors prioritize price stability and consistent input quality to protect margins within competitive retail categories. Döhler GmbH and AGRANA Beteiligungs-AG leverage vertically integrated sourcing and large-scale fruit preparation facilities to secure industrial contracts. SVZ International B.V. expands conventional capacity to maintain throughput leadership across transatlantic markets. SunOpta Inc. deploys aseptic filling platforms that enable bulk storage and simplify logistics. Mature infrastructure, predictable procurement cycles, and embedded enterprise relationships collectively sustain conventional segment leadership.

The organic segment is expected to be the fastest-growing, driven by accelerating clean-label preferences in premium baby food and health-oriented formulations. Rising scrutiny of pesticide residues is driving demand for certified sourcing and traceable farm-to-processing workflows. Processors invest in segregated organic lines to preserve certification integrity and prevent cross-contamination risk. Boiron Frères SAS advances flash-pasteurization techniques that retain sensory authenticity for professional culinary channels. Tree Top Inc. expands organic certifications to meet stringent infant nutrition specifications. Ingredion Incorporated strengthens traceability platforms supporting premium brand positioning. Technology-enabled transparency and certification-backed differentiation accelerate adoption across value-added applications.

Application Insights

Beverages are projected to lead the market in 2026, accounting for approximately 36% share, underpinned by entrenched integration across global smoothie, flavored water, and functional dairy workflows. High-volume beverage manufacturing relies on strawberry puree for natural sweetness, color stability, and texture enhancement in ready-to-drink portfolios. Döhler GmbH supplies multi-sensory concentrates tailored for flavored water and juice platforms seeking to reduce additive use. Monin Inc. expands high-fruit formulations, enabling operational consistency across foodservice chains. The Coca-Cola Company, through its Innocent smoothie lines, scales procurement for functional fruit blends. PepsiCo advances no-sugar-added juice formats, reinforcing demand for high-quality puree inputs. Established RTD infrastructure, aseptic logistics, and predictable consumption cycles collectively sustain beverage segment dominance.

Baby food is anticipated to be the fastest-growing segment, driven by accelerating parental preference for clean-label, minimally processed infant nutrition products. Rising scrutiny of added sugars and artificial preservatives strengthens reliance on fruit-based weaning formulations. Nestlé, through its Gerber portfolio, embeds organic strawberry puree within certified infant feeding lines. Campbell Soup Company via Plum Organics advances fruit-vegetable pouch blends, leveraging strawberry as a natural palatability enhancer. Danone expands regenerative sourcing models within premium infant nutrition platforms. Beech-Nut Nutrition Corporation emphasizes cold-processed formulations supporting nutrient retention claims. Traceability systems, pouch convenience formats, and heightened quality testing collectively accelerate adoption across global pediatric nutrition value chains.

Regional Insights

Europe Strawberry Puree Market Trends

Europe is anticipated to remain the leading regional market, accounting for approximately 39% of global share in 2026, supported by its mature bakery, dairy, and confectionery ecosystems. The region is positioned to maintain structural dominance through integrated fruit-processing networks and sophisticated consumer demand for high-fruit-content formulations. Sustainability alignment and organic portfolio expansion are expected to reinforce procurement of certified strawberry puree across retail and private-label channels. Harmonized quality frameworks under European food safety authorities are likely to standardize residue compliance and traceability benchmarks, strengthening cross-border trade cohesion. A diversified supplier base, including AGRANA Beteiligungs-AG and Andros Group, is expected to anchor industrial-scale fruit preparation for yogurt and dessert brands. Investment in energy-efficient processing and NFC technologies is projected to enhance margin durability and premium product positioning.

Poland is anticipated to function as the regional processing anchor, shaping supply continuity and export competitiveness across continental markets. Its concentrated fruit preparation infrastructure is expected to support large-scale shipments into Germany and France, reinforcing intra-European trade flows. Regulatory harmonization is likely to streamline certification pathways, enabling Polish processors to integrate seamlessly with multinational dairy manufacturers. Vendor strategies are projected to prioritize green processing technologies and sustainability-linked sourcing contracts to align with retailer procurement mandates. Expansion of processing capacity within Poland is expected to strengthen upstream bargaining power and stabilize seasonal supply cycles. This structural centralization positions Poland as the operational fulcrum sustaining Europe’s leadership in the global strawberry puree market.

Asia Pacific Strawberry Puree Market Trends

Asia Pacific is projected to remain the fastest-growing regional market, while structurally expanding its consumption base through accelerating urbanization and rising middle-income households. The region will strengthen its position through rapid modernization of food processing infrastructure, expanding dairy, beverage, and bakery manufacturing capacity, and increasing alignment with premium fruit-based formulations. Demand will intensify as westernized dietary preferences reshape packaged yogurt, functional beverages, and ready-to-drink categories across China, India, Japan, and ASEAN economies. Regulatory tightening will professionalize supply chains and standardize quality benchmarks, encouraging higher adoption of Not From Concentrate processing technologies. The region will increasingly function as both a high-growth consumption center and a scalable manufacturing base for fruit puree applications.

China will anchor regional acceleration by shaping regulatory direction, capital allocation, and technology deployment across the broader Asia Pacific ecosystem. National food safety standards will favor premium-grade and traceable fruit inputs, accelerating the adoption of NFC formats within beverage and dairy categories. Large-scale dairy and beverage manufacturers such as Bright Dairy & Food Co. and Nongfu Spring will expand demand for standardized, high-quality strawberry puree in premium yogurt and fruit tea portfolios. Infrastructure modernization and procurement integration will position China as the operational nucleus influencing vendor strategies, cross-border sourcing flows, and technology adoption trajectories across the Asia Pacific market.

North America Strawberry Puree Market Trends

North America is expected to remain a stable market, supported by deep enterprise penetration and a mature food-processing ecosystem. The region is positioned to maintain structural dominance through a strong alignment among clean-label demand, advanced cold-chain logistics, and vertically integrated fruit-sourcing networks. Innovation intensity across the beverage, dairy, and infant nutrition categories is expected to drive the use of strawberry puree in premium and functional formulations. Regulatory clarity under food safety frameworks is likely to reduce friction in commercialization while enabling rapid product reformulation cycles. A consolidated supplier base, including Tree Top Inc. and Ingredion Incorporated, is expected to provide stability in large-scale procurement.

The U.S. is anticipated to function as the primary anchor shaping regional momentum through scale, production capacity, and innovation-led product development. Its expansive strawberry cultivation base and advanced processing infrastructure are expected to ensure continuity of raw materials for both domestic and export channels. Federal food safety oversight is likely to sustain high compliance thresholds, reinforcing quality differentiation across premium retail segments. Enterprise adoption of functional smoothie and fortified beverage formats is expected to intensify, embedding puree demand within high-value wellness portfolios. Strategic partnerships between processors and agricultural cooperatives are anticipated to enhance supply chain resilience, positioning the U.S. as the structural driver of North American market evolution.

Competitive Landscape

The global strawberry puree market is moderately consolidated, with leadership concentrated among multinational suppliers such as Nestlé, Tree Top, and Agrana, while numerous regional processors sustain a fragmented base. Leading entities exert influence through vertically integrated supply chains, operational scale, and expansive distribution networks, ensuring consistent availability for high-volume industrial applications. The structural market duality reflects top-tier consolidation via strategic acquisitions and alliances, juxtaposed against localized production maintained by cooperatives and smaller processors. Geographic diversification, organic and non-GMO certification capabilities, and technological investments in aseptic and cold-chain processing define the functional prominence of these major players.

Competitive positioning differentiates cost-focused, high-volume producers from premium-segment innovators specializing in organic, clean-label, or specialty fruit purees. Top-tier players leverage economies of scale and global procurement to reinforce market influence, while regional and niche suppliers emphasize traceability, quality, and flavor integrity to capture emerging demand. Industry dynamics are shaped by platform integration, M&A activity, and investment in processing technologies, including NFC extraction and extended shelf-life solutions, creating a forward-looking ecosystem in which consolidation, innovation, and operational resilience guide market evolution.

Key Industry Developments:

- In January 2025, HEYTEA transitioned to an innovation-driven model, focusing on premium ingredients and healthy-lifestyle branding. This shift, highlighted by the "Super Plant" and high-quality fruit series, led to a record 37 million cups sold of new functional beverages.

- In November 2024, AGRANA launched its "AGRANA NEXT LEVEL" strategy to boost efficiency and profitability. The restructuring aimed to minimize exposure to volatile raw material markets and ensure long-term supply chain stability for its fruit and sugar segments across Europe.

Companies Covered in Strawberry Puree Market

- Döhler Group SE

- Tree Top Industries Inc.

- Agrana Beteiligungs-AG

- Nestlé

- SunOpta Inc.

- Boiron Frères SAS

- SVZ International B.V.

- Symrise AG

- Capfruit/Capricorn Food Products India Ltd.

- Grünewald GmbH

- Milne Fruit Products Inc.

- Oregon Fruit Products

- Andros Group

- Kerr/Ingredion

- Jain Irrigation

- Monin Inc.

Frequently Asked Questions

The global strawberry puree market is projected to be valued at US$0.9 billion in 2026 and is expected to reach US$1.4 billion by 2033, driven by rising demand for natural ingredients in beverages, baby food, and premium clean-label applications.

The transition toward transparent ingredient declarations is reinforcing demand for strawberry puree across processed food categories, as manufacturers substitute synthetic flavors and colors with fruit-based ingredients to comply with regulatory standards and meet consumer expectations for natural, minimally processed products.

The strawberry puree market is forecast to grow at a CAGR of 6.1% from 2026 to 2033, reflecting sustained adoption in beverages, baby food, and high-fruit-content dairy and confectionery applications.

Europe is the leading regional market, accounting for approximately 39% share, supported by mature bakery, dairy, and confectionery ecosystems, integrated fruit processing networks, and widespread adoption of certified organic and Not From Concentrate (NFC) products.

The strawberry puree market is moderately consolidated, with key players including Döhler Group SE, Tree Top Industries Inc., Agrana Beteiligungs-AG, Nestlé, SunOpta Inc., Boiron Frères SAS, SVZ International B.V., Symrise AG, Capfruit / Capricorn Food Products India Ltd., Grünewald GmbH, Milne Fruit Products Inc., Oregon Fruit Products, Andros Group, Kerr/Ingredion, Jain Irrigation, and Monin Inc. These players compete through scale, integrated supply chains, and technological capabilities in aseptic and NFC processing.