- Automotive Components & Materials

- Off-road Vehicle Braking System Market

Off-road Vehicle Braking System Market Size, Share, and Growth Forecast, 2026 - 2033

Off-road Vehicle Braking System Market by Vehicle Type (All-Terrain Vehicles (ATVs), Utility Task Vehicles (UTVs), Others), Brake Type (Hydraulic Brakes, Disc Brakes, Others), Application, Sales Channel, and Regional Analysis for 2026 - 2033

Off-road Vehicle Braking System Market Size and Trends Analysis

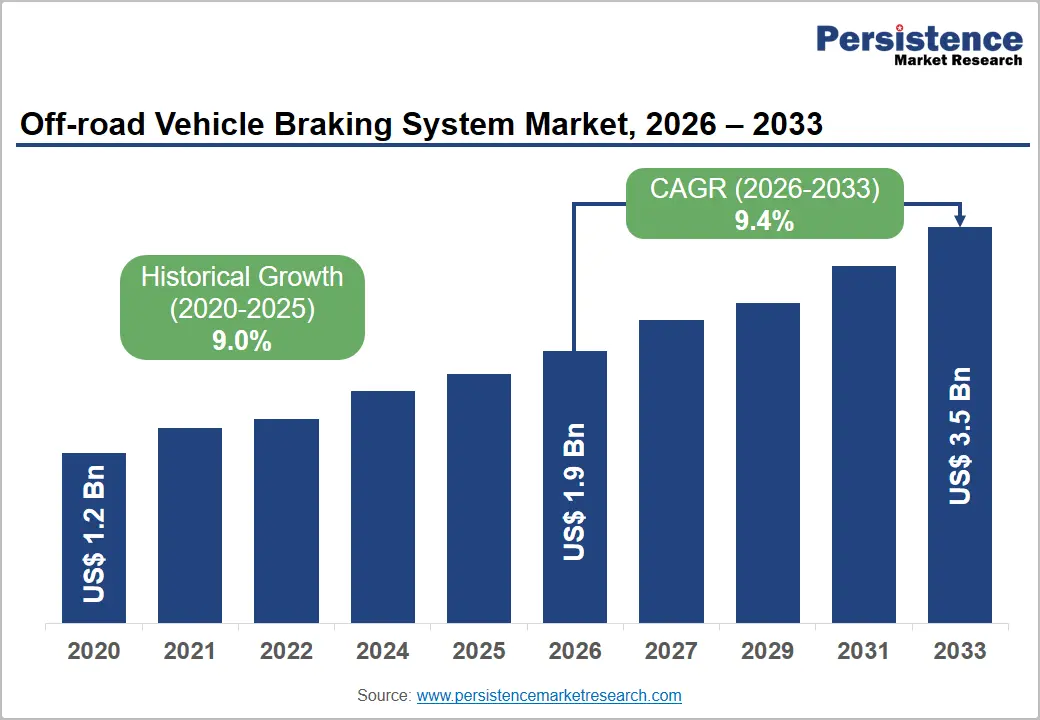

The global off-road vehicle braking system market size is likely to be valued at US$1.9 billion in 2026 and is expected to reach US$3.5 billion by 2033, growing at a CAGR of 9.4% during the forecast period from 2026 to 2033, driven by the increasing demand for off-road vehicles across agriculture, construction, mining, recreational activities, and defense applications.

Growing adoption of advanced safety technologies, including anti-lock braking systems (ABS), electronic stability control (ESC), traction control systems (TCS), and brake-by-wire solutions, is accelerating market expansion. Equipment manufacturers are increasingly integrating electronically controlled braking systems to improve vehicle stability, operational safety, and performance under challenging terrain conditions. The transition toward electrified and autonomous off-road vehicles is further creating opportunities for advanced braking technologies.

Key Industry Highlights:

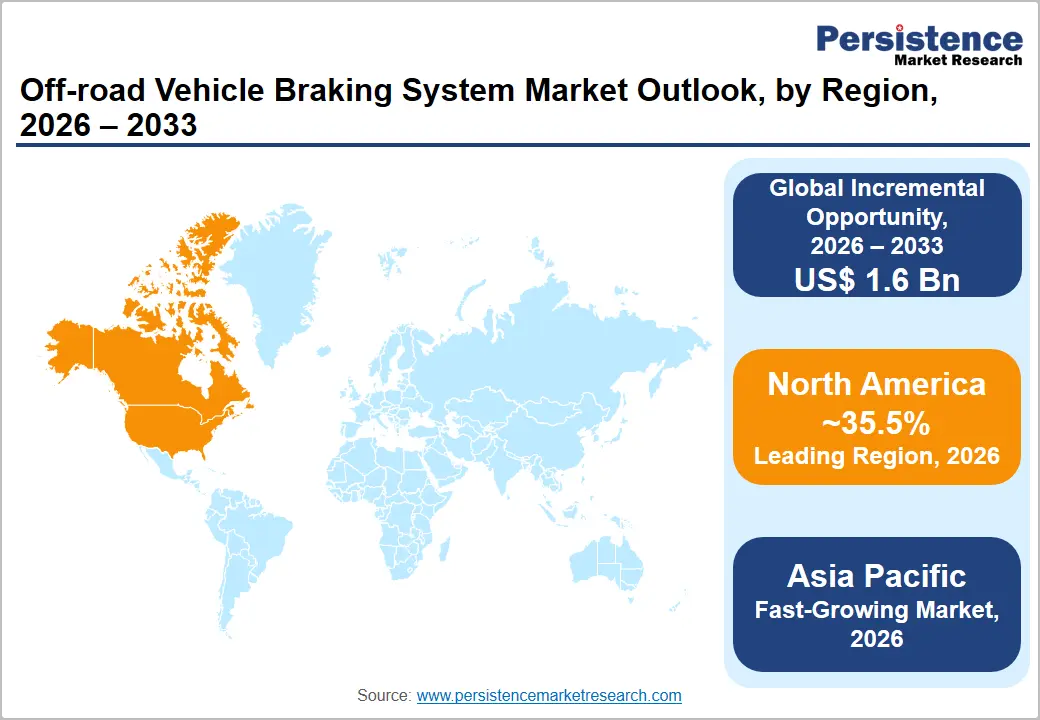

- Leading Region: North America is anticipated to account for approximately 35.5% of the market share, supported by strong demand from agricultural, construction, mining, recreational, and defense vehicle fleets, along with high adoption of advanced braking technologies.

- Fastest-growing Region: Asia Pacific is expected to register the fastest CAGR, driven by infrastructure development, agricultural mechanization, mining investments, and increasing adoption of advanced off-road vehicles across China, India, and Southeast Asia.

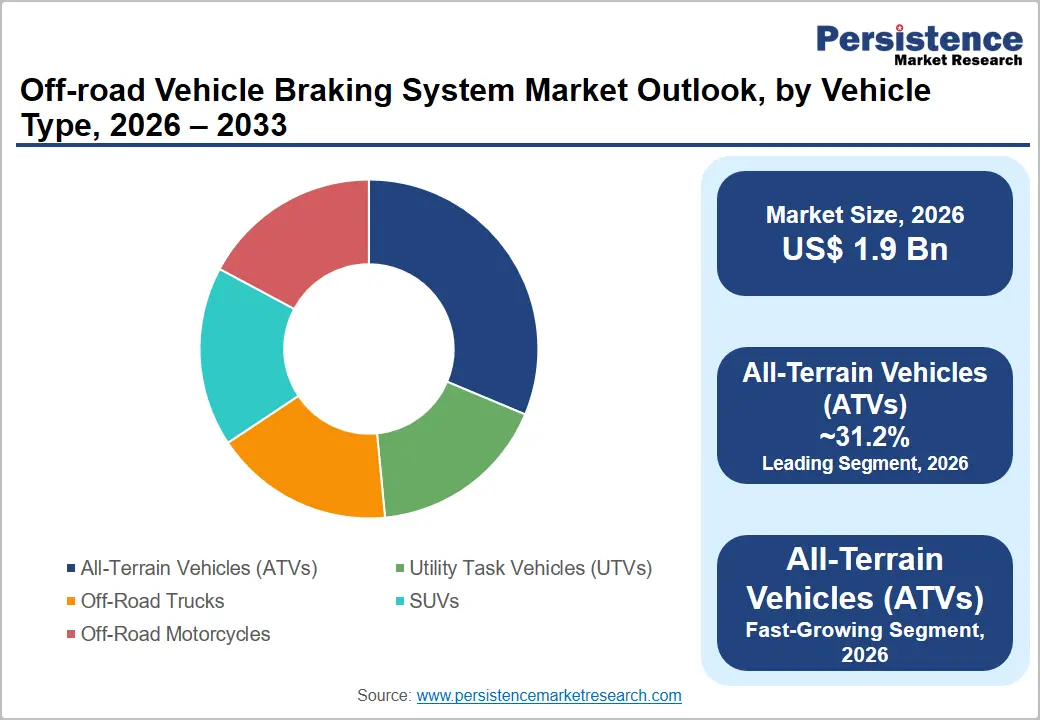

- Dominant Vehicle Type: All-Terrain Vehicles (ATVs) are anticipated to account for approximately 31.2% of the market share, driven by strong demand across recreational, agricultural, forestry, and utility applications, particularly in North America.

- Leading Brake Type: Hydraulic brakes are anticipated to hold approximately 44.9% of the market share, owing to their superior stopping power, durability, reliability, and widespread adoption across ATVs, UTVs, agricultural machinery, construction equipment, and mining vehicles.

DRO Analysis

Driver - Rising Demand for Off-road Equipment across Agriculture, Construction, and Mining

The growing utilization of off-road vehicles in agricultural mechanization, infrastructure development, mining operations, and industrial applications remains one of the primary growth drivers for the market. Governments worldwide continue to increase investments in transportation infrastructure, renewable energy projects, mining activities, and smart agriculture initiatives. These investments directly support demand for tractors, utility task vehicles (UTVs), construction machinery, and specialized off-road trucks, all of which require highly reliable braking systems.

The increasing deployment of heavy-duty machinery in challenging environments creates demand for advanced braking technologies capable of delivering consistent stopping performance under high loads and difficult operating conditions. Modern braking systems improve vehicle control, reduce operational risks, and enhance productivity. As fleet operators focus on reducing downtime and improving safety standards, demand for technologically advanced braking components is expected to increase throughout the forecast period.

Increasing Adoption of Electrification and Advanced Vehicle Safety Technologies

The rapid integration of electronic controls into off-road vehicles is transforming braking system requirements. Vehicle manufacturers are increasingly adopting ABS, ESC, TCS, and brake-by-wire technologies to improve maneuverability and safety on uneven surfaces. These systems provide enhanced traction control, shorter stopping distances, and better vehicle stability in mud, gravel, snow, and steep-gradient environments.

Electrification trends within utility vehicles, agricultural equipment, and construction machinery are further supporting demand for intelligent braking systems. Electric and hybrid off-road vehicles require advanced braking architectures that can seamlessly integrate with regenerative braking systems and electronic vehicle control platforms. The growing emphasis on autonomous and semi-autonomous machinery is also increasing demand for electronically controlled braking solutions capable of supporting advanced driver assistance and machine automation functions.

Restraint - High System Costs and Integration Complexity

Despite strong growth prospects, the adoption of advanced braking technologies faces challenges associated with high implementation costs and system complexity. Electronic braking systems, brake-by-wire architectures, and integrated stability-control technologies require additional sensors, software validation, electronic control units, and redundancy mechanisms. These requirements increase manufacturing costs and development timelines.

Many agricultural operators, mining contractors, and construction fleet owners continue to prioritize durability and affordability when making equipment purchasing decisions. In emerging markets, cost-sensitive buyers often prefer conventional hydraulic braking systems due to lower maintenance requirements and easier servicing. Supply-chain disruptions affecting electronic components and semiconductors may also create temporary challenges for advanced braking system deployment, particularly in developing regions.

Opportunity - Growing Aftermarket Demand and Fleet Modernization Programs

The large installed base of off-road vehicles worldwide presents substantial opportunities for aftermarket suppliers. Off-road vehicles operate in harsh environments characterized by dust, moisture, vibration, and heavy loads, resulting in higher wear rates for braking components. This creates recurring demand for replacement brake pads, discs, calipers, hydraulic assemblies, and electronic braking modules.

Fleet modernization initiatives across agriculture, construction, mining, and utility sectors are creating opportunities for brake-system upgrades. Many operators are investing in advanced braking technologies to improve workplace safety, reduce maintenance costs, and extend vehicle service life. The aftermarket segment is expected to remain a significant revenue contributor as fleet operators prioritize operational efficiency and regulatory compliance.

Rapid Industrialization and Mechanization in Asia Pacific

Asia Pacific represents one of the most attractive growth opportunities for braking system manufacturers. Expanding agricultural mechanization, infrastructure development, mining investments, and industrial automation are driving demand for off-road vehicles throughout China, India, Southeast Asia, and Australia.

The region's strong manufacturing ecosystem enables cost-effective production of braking components while supporting rapid technology adoption. Local vehicle manufacturers are increasingly integrating advanced braking technologies to enhance product competitiveness and meet evolving safety expectations. As governments continue to invest in transportation networks, mining capacity expansion, and agricultural productivity improvements, demand for reliable braking systems is expected to grow significantly across the region.

Category-wise Analysis

Vehicle Type Insights

All-Terrain Vehicles (ATVs) are anticipated to account for approximately 31.2% of the market share in 2026, making them the leading vehicle-type segment. Their dominance is supported by widespread use across recreational activities, agriculture, forestry, and utility operations, particularly in North America. Major manufacturers such as Polaris, Yamaha, and Honda continue to expand ATV portfolios with enhanced safety and braking features. ATVs require reliable braking performance across challenging terrains, including mud, sand, and rocky surfaces. Growing integration of ABS, hydraulic disc brakes, and electronic stability technologies is improving vehicle control and rider safety, supporting continued demand for advanced braking systems.

ATVs are also expected to be the fastest-growing vehicle-type segment during the forecast period. Growth is driven by increasing participation in outdoor recreation, expanding agricultural applications, and rising demand in emerging markets. New premium ATV models from manufacturers such as Can-Am and Polaris increasingly incorporate advanced braking and traction-control systems. The adoption of electronic braking technologies and enhanced vehicle stability systems is expected to further accelerate segment growth as consumers and fleet operators prioritize safety and performance.

Brake Type Insights

Hydraulic brakes are anticipated to account for approximately 44.9% of the market share in 2026, making them the dominant brake-type segment. Their widespread adoption is attributed to strong stopping power, durability, cost efficiency, and ease of maintenance. Hydraulic braking systems remain standard across ATVs, UTVs, tractors, construction equipment, and mining vehicles. Manufacturers continue to improve hydraulic brake performance through corrosion-resistant materials and enhanced fluid-management systems. Equipment from companies such as John Deere, Caterpillar, and Kubota extensively utilizes hydraulic braking solutions due to their reliability in harsh operating environments.

Electromechanical brakes are expected to register the fastest growth throughout the forecast period, driven by increasing electrification and automation in off-road vehicles. These systems provide faster response times, improved diagnostics, and seamless integration with electronic vehicle controls. The growing adoption of electric utility vehicles, autonomous agricultural machinery, and smart construction equipment is accelerating demand for electromechanical braking technologies. Manufacturers are increasingly incorporating brake-by-wire systems to support advanced safety features, autonomous functions, and connected vehicle platforms.

Regional Insights

North America Off-road Vehicle Braking System Market Trends

North America is anticipated to account for approximately 35.5% of the market share in 2026, making it the leading regional market. Growth is supported by a large installed base of agricultural, construction, mining, recreational, and defense vehicles, coupled with high adoption of advanced braking technologies such as ABS, ESC, and brake-by-wire systems.

U.S. Off-road Vehicle Braking System Market Trends

The U.S. represents the largest market within North America due to its extensive off-highway equipment fleet and strong presence of major OEMs, including Caterpillar, Deere & Company, Polaris, and Textron. Ongoing investments in infrastructure development, mining operations, and precision agriculture continue to drive demand for advanced braking systems. Increasing adoption of autonomous construction and agricultural equipment is further supporting demand for electronically controlled braking technologies.

Canada Off-road Vehicle Braking System Market Trends

Canada contributes significantly through its mining, forestry, and agricultural sectors. The country's harsh operating environments require durable and high-performance braking systems capable of functioning under extreme weather and terrain conditions. Growing investments in mining projects and utility vehicle fleets are supporting market growth.

Europe Off-road Vehicle Braking System Market Trends

Europe remains a significant market for off-road vehicle braking systems, supported by advanced manufacturing capabilities, stringent safety regulations, and increasing adoption of electrified off-highway equipment. The region benefits from strong demand across agricultural machinery, construction equipment, and specialty off-road vehicles.

Germany Off-road Vehicle Braking System Market Trends

Germany serves as the largest market and technology hub in Europe. The country is home to several leading braking-system manufacturers and off-highway equipment suppliers. Strong engineering expertise and ongoing investments in automation, electrification, and vehicle safety technologies continue to drive market expansion.

U.K. Off-road Vehicle Braking System Market Trends

The U.K. is witnessing growing demand for braking systems in agricultural machinery, utility vehicles, and defense applications. Increasing investments in rural infrastructure projects and modernization of farming equipment are supporting market growth. Demand for premium off-road recreational vehicles is also contributing to braking system adoption.

France Off-road Vehicle Braking System Market Trends

France maintains a strong agricultural machinery sector, creating sustained demand for reliable braking systems. The country's focus on sustainable farming practices and equipment modernization is encouraging the integration of advanced safety and control technologies in off-road vehicles.

Spain Off-road Vehicle Braking System Market Trends

Spain's market growth is supported by expanding agricultural operations, construction activities, and tourism-related recreational vehicle usage. Increasing mechanization in farming and infrastructure projects is expected to drive steady demand for off-road braking solutions.

Asia Pacific Off-road Vehicle Braking System Market Trends

Asia Pacific is anticipated to register the fastest CAGR during the forecast period, driven by rapid industrialization, infrastructure investments, agricultural mechanization, and expanding mining activities. The region's manufacturing capabilities and growing domestic demand continue to attract significant investment from global vehicle and braking-system manufacturers.

China Off-road Vehicle Braking System Market Trends

China represents the largest market in Asia Pacific due to its dominant construction equipment, mining machinery, and agricultural vehicle industries. Government-led infrastructure initiatives, mining investments, and smart agriculture programs continue to create substantial demand for advanced braking systems. Increasing adoption of electric and autonomous off-road equipment further supports market growth.

India Off-road Vehicle Braking System Market Trends

India is one of the fastest-growing markets in the region, driven by agricultural mechanization, infrastructure development, and expanding construction activities. Government initiatives aimed at improving farm productivity and rural infrastructure are increasing demand for tractors, utility vehicles, and construction equipment equipped with advanced braking systems.

Japan Off-road Vehicle Braking System Market Trends

Japan contributes through its strong automotive technology ecosystem and advanced manufacturing capabilities. The country's focus on vehicle safety, automation, and electrification is encouraging the development of next-generation braking systems for off-road applications. Japanese manufacturers continue to play a critical role in braking-system innovation across the region.

Australia Off-road Vehicle Braking System Market Trends

Australia's mining sector remains a major driver of demand for heavy-duty off-road vehicles and specialized braking systems. Large-scale mining operations require highly durable braking technologies capable of operating under extreme environmental conditions, creating opportunities for premium braking-system suppliers.

Competitive Landscape

The global off-road vehicle braking system market exhibits a moderately consolidated structure, with several multinational manufacturers holding significant market positions while numerous regional suppliers serve niche and aftermarket segments. Competition is based on technological innovation, product reliability, manufacturing scale, aftermarket support, and OEM partnerships.

Market leaders are prioritizing product innovation, electronic braking integration, regional manufacturing expansion, and strategic OEM partnerships. Companies are investing heavily in brake-by-wire technology, advanced safety systems, predictive maintenance capabilities, and software-enabled vehicle control solutions. The growing convergence of hardware, software, and aftermarket services is emerging as a key competitive differentiator.

Key Industry Developments:

- In July 2025, ZF Friedrichshafen AG launched a comprehensive Brake-by-Wire portfolio designed to support software-defined and highly automated vehicles.

- In September 2025, ZF Friedrichshafen AG showcased its latest by-wire steering and braking technologies at IAA Mobility 2025.

Companies Covered in Off-road Vehicle Braking System Market

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Knorr-Bremse AG

- Continental AG

- Brembo S.p.A.

- ADVICS Co., Ltd.

- Hitachi Astemo, Ltd.

- Akebono Brake Industry Co., Ltd.

- Carlisle Brake & Friction

- Brakes India Private Limited

- Eaton Corporation plc

- Haldex AB

- Bendix Commercial Vehicle Systems LLC

- Wabtec Corporation

- Alcon Components Ltd.

- Aisin Corporation

Frequently Asked Questions

The global off-road vehicle braking system market is anticipated to be valued at US$1.9 billion in 2026.

The off-road vehicle braking system market is expected to reach US$3.5 billion by 2033.

Key trends include the growing adoption of ABS, electronic stability control (ESC), brake-by-wire technologies, electromechanical braking systems, vehicle electrification, and autonomous off-road equipment, alongside increasing demand for advanced safety and control solutions.

All-Terrain Vehicles (ATVs) are anticipated to be the leading vehicle type segment, accounting for approximately 31.2% of the market share, driven by strong demand across recreational, agricultural, and utility applications.

The off-road vehicle braking system market is projected to expand at a CAGR of 9.4% between 2026 and 2033.

Major players include ZF Friedrichshafen AG, Robert Bosch GmbH, Knorr-Bremse AG, and Continental AG.