- Automotive Components & Materials

- Automotive Metal Market

Automotive Metal Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Metal Market by Metal Type (Steel, Aluminum, Magnesium, Copper, Titanium, Nickel, Zinc, Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, Hybrid Vehicles), Product Form (Flat Products, Long Products, Castings, Forgings, Extrusions, Tubes & Pipes), Application (Body Structure, Chassis & Suspension, Powertrain, Wheels & Tires, Battery Components, Others), End-user (OEMs, Aftermarket), and Regional Analysis for 2026 - 2033

Automotive Metal Market Size and Trend Analysis

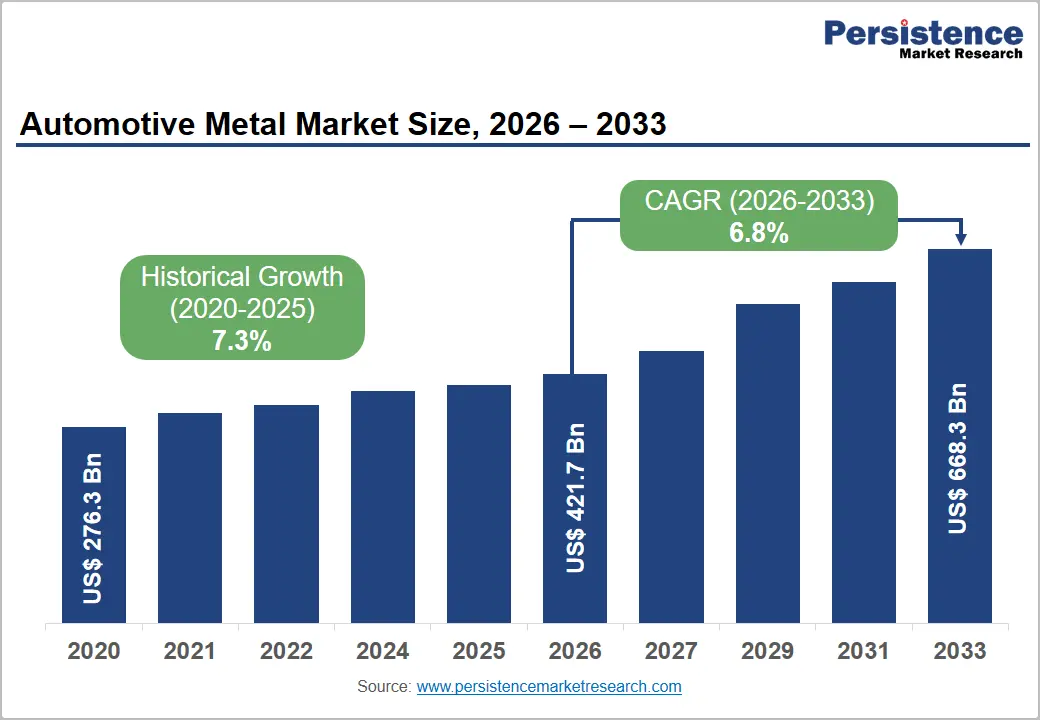

The global automotive metal market is expected to be valued at US$ 421.7 billion in 2026 and is projected to reach US$ 668.3 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033. Sustained growth in global vehicle production, the accelerating electrification of vehicle fleets, and rising demand for lightweight, high-strength metals, particularly advanced high-strength steel (AHSS) and aluminum alloys, are the primary structural forces driving this market forward.

The global automotive industry's simultaneous pursuit of fuel efficiency, safety compliance, and EV range optimization is systematically elevating per-vehicle metal content and diversifying the metal type mix. Government-mandated emission reduction targets across the European Union, United States, China, and India are accelerating OEM investment in lightweight material substitution, supporting above-GDP growth in premium-grade automotive metal consumption through 2033.

Key Industry Highlights

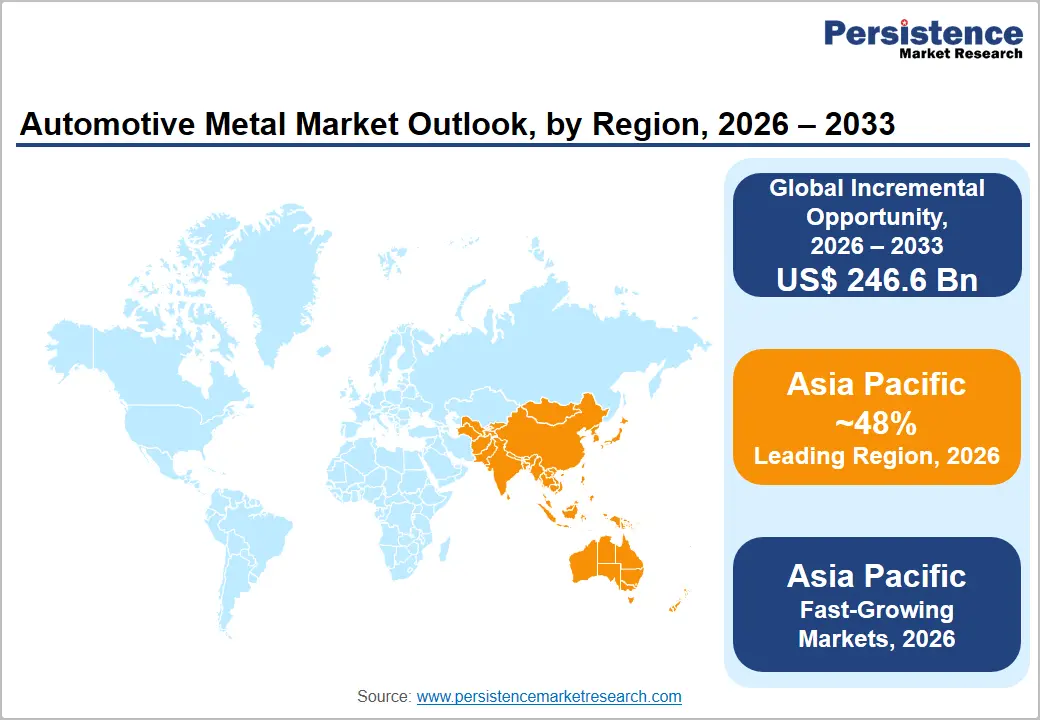

- Leading Region: Asia Pacific commands 48% of global Automotive Metal market revenue in 2025, driven by China's dominance as the world's largest vehicle production and EV market, supported by integrated steel and aluminum supply chains serving over 30 million vehicles annually.

- Fast-Growing Market: Asia Pacific is one of the fast-growing market at 8.1% CAGR in the forecast period with India's PLI-driven automotive production expansion and South Korea's EV platform investments emerging as the highest-growth national markets within the region.

- Dominant Segment: Steel leads the Metal Type category with ~55% market share in 2025, sustained by AHSS and UHSS adoption in body structure and chassis applications, a position reinforced by OEMs' cost-disciplined vehicle programs where steel's strength-to-cost ratio remains unmatched.

- Fastest Growing Segment: Battery Components is the fastest growing application at ~18.2% CAGR through 2033, driven by global EV production scale-up, generating surging demand for aluminum enclosures, copper busbars, and high-strength steel battery protection structures.

- Key Opportunity: Scrap-based low-carbon metal production aligned with CSRD and IRA domestic content requirements offers a commercially actionable premium opportunity. Producers such as Novelis and Steel Dynamics, Inc. are already capturing supply agreement premiums that will become industry-standard OEM procurement criteria by 2027 - 2028.

Market Dynamics

Drivers - Accelerating Electric Vehicle Production Reshaping Metal Demand Composition

The shift toward electric vehicle (EV) manufacturing represents the most structurally transformative demand signal for automotive metal producers, and market participants that align their product portfolios with EV-specific material requirements are best positioned to capture the incremental revenue opportunity. EVs require approximately 25-30% more aluminum than comparable internal combustion engine (ICE) vehicles, driven by battery enclosure structures, thermal management components, and lightweight body architecture requirements, a shift that directly benefits aluminum producers and processors.

According to the International Energy Agency (IEA), global EV sales exceeded 14 million units in 2023, with EVs representing approximately 18% of all new car sales globally, up from under 5% in 2020. The IEA's Net Zero by 2050 scenario projects over 60% of new car sales to be electric by 2030, implying a secular, decade-long structural demand shift that rewards aluminum, magnesium, and copper producers while pressuring traditional steel suppliers to develop ultra-high-strength grades that remain competitive on a weight-adjusted basis.

Stringent Global Emission Regulations Driving Lightweight Metal Substitution

Regulatory pressure on automakers to reduce fleet-average CO2 emissions is directly translating into materials substitution decisions at the OEM level, giving lightweight metal suppliers a powerful and policy-backed demand catalyst. The European Union's revised CO2 emission standards mandate a 55% reduction in passenger car emissions by 2030 relative to 2021 levels, compelling European OEMs to aggressively pursue mass reduction strategies.

The U.S. Environmental Protection Agency (EPA) finalized new tailpipe emission standards in 2024, targeting a fleet average of approximately 85 g CO2/mile by 2032, which auto industry analysts at the Center for Automotive Research (CAR) estimate will require average vehicle weight reductions of 100-150 kg per vehicle across major model lines. Each kilogram of structural steel replaced by aluminum in a vehicle body-in-white reduces vehicle mass by approximately 0.5 kg on a secondary-effect basis, making aluminum sheet and extrusions one of the highest-leverage materials in compliance-driven lightweighting strategies, a dynamic that is rapidly reshaping procurement priorities across General Motors, Ford, BMW, and Volkswagen Group supply chains.

Restraints - Volatile Raw Material and Energy Costs Compressing Manufacturer Margins

Raw material and energy cost volatility constitutes a structural profitability risk for automotive metal producers, constraining their ability to invest in value-added processing capabilities and pass-through pricing to cost-disciplined OEM customers. Steel production is among the most energy-intensive industrial processes globally, consuming approximately 18-20 GJ per tonne of crude steel, while primary aluminum smelting requires roughly 14-15 MWh of electricity per tonne, making both sectors acutely exposed to natural gas and electricity price shocks.

The World Steel Association reported that energy costs accounted for 20-35% of total crude steel production costs in 2022-2023, a period marked by severe European energy price volatility following geopolitical disruptions. These dynamics compress EBITDA margins, particularly at mid-tier integrated producers who lack the hedging infrastructure of global majors such as ArcelorMittal or Novelis, and disproportionately impact new entrants seeking to scale value-added automotive-grade production without the benefit of captive energy or vertically integrated ore supply.

Supply Chain Fragility and Critical Metal Import Concentration Risks

The automotive metal supply chain's structural dependence on a narrow set of geographies for critical inputs, including manganese, nickel, and rare earth-alloying elements, exposes OEMs and tier-1 metal processors to substantial supply concentration risk that becomes commercially material during periods of geopolitical stress. According to the U.S. Geological Survey (USGS), the Democratic Republic of Congo accounts for over 70% of global cobalt mining output, while China dominates processing of multiple battery-relevant metals, including nickel sulfate and lithium, creating single-point-of-failure dynamics in EV-related metal supply chains.

The European Commission's Critical Raw Materials Act (2024) explicitly identifies this concentration risk, mandating that no more than 65% of any critical raw material consumed in the EU may originate from a single third country, a policy constraint that will require substantial upstream supply chain reconfiguration at cost and timeline implications that directly affect automotive metal procurement planning. For market participants, this structural fragility signals the need for supply chain diversification investments, long-term offtake agreements with diversified mine operators, and accelerated scrap-based secondary metal production as a supply security hedge.

Opportunities - High-Growth EV Battery Component Metals Creating a Premium Demand Segment

The commercial-scale build-out of EV battery gigafactories across North America, Europe, and Asia is generating a structurally new, high-value demand segment for specialty automotive metals, particularly copper, nickel, aluminum, and advanced steel grades, that rewards producers capable of meeting exacting metallurgical specifications. Copper content per EV averages approximately 83 kg versus 23 kg in a conventional ICE vehicle, per Copper Development Association data, representing a near-four-fold per-unit content increase that translates directly into volume uplift for copper processors supplying the EV powertrain and battery wiring harness segments.

The U.S. Inflation Reduction Act (IRA) has catalyzed over US$ 130 billion in new EV and battery manufacturing announcements in the United States alone through 2024, according to the U.S. Department of Energy (DOE), creating a multi-year, policy-backstopped demand surge for domestically sourced battery component metals. Companies including Novelis, Constellium NV, and AMG Advanced Metallurgical Group, that proactively develop battery enclosure aluminum alloys and high-purity specialty metal grades are positioned to capture the premium pricing and long-term OEM supply agreements that will define competitive advantage in this sub-segment through 2033.

Scrap-Based Secondary Metal Production Aligning with OEM Sustainability Mandates

The automotive industry's accelerating adoption of Scope 3 emissions reduction commitments is creating a commercially actionable opportunity for secondary metal producers who can demonstrate verified, low-carbon metal supply chains at automotive quality levels. Novelis, the world's largest recycler of aluminum, reported that its recycled content accounted for approximately 63% of total input materials in fiscal 2024, enabling it to offer OEM customers aluminum with a carbon footprint approximately 75% lower than primary smelted aluminum, a differentiation that is increasingly commanding supply agreement premiums as BMW, Ford, and Volkswagen publish supplier sustainability requirements.

The European Commission's Corporate Sustainability Reporting Directive (CSRD), effective from 2024, mandates disclosure of Scope 3 supply chain emissions for large automotive OEMs, a regulatory development that is directly elevating the commercial value of certified low-carbon metal supply relative to conventionally produced primary metal. For producers investing in electric arc furnace (EAF) steel production or high-scrap-rate aluminum rolling, including Steel Dynamics, Inc. and Constellium NV, this policy-driven premium represents a meaningful and growing revenue differential that justifies capacity investment today ahead of what is projected to become a mainstream OEM procurement requirement by 2027-2028.

Category-wise Analysis

Metal Type Insights

Steel remains the dominant metal type in the global automotive metal market, accounting for approximately 55% of total revenue in 2026 due to its strong balance of strength, safety performance, and cost efficiency. Automotive manufacturers extensively use advanced high-strength steel and ultra-high-strength steel in vehicle body structures, chassis systems, suspension components, and powertrain applications.

These materials help automakers reduce vehicle weight while maintaining the crash resistance and structural integrity required under stringent safety regulations. The widespread global presence of steel processing infrastructure and established automotive supply chains further strengthens steel’s market position. Automakers also continue investing in next-generation steel grades to improve fuel efficiency and support electric vehicle development. The material’s recyclability, durability, and compatibility with existing manufacturing systems continue to make steel the preferred choice across mass-market and commercial vehicle production worldwide.

Vehicle Type Insights

Passenger cars are expected to lead the vehicle type segment with approximately 45% share in 2026, supported by their dominant contribution to global automobile production volumes. Rising consumer demand for personal mobility, urban transportation, and technologically advanced vehicles continues to drive passenger car manufacturing across Asia Pacific, Europe, and North America. Automakers are increasingly incorporating lightweight metals such as advanced steel, aluminum, and specialty alloys into passenger car designs to improve fuel efficiency, enhance safety, and support electric vehicle performance targets.

The segment also benefits from continuous innovation in vehicle body engineering, emission reduction technologies, and battery integration systems. Long-term supply agreements between vehicle manufacturers and metal producers create stable procurement demand for automotive-grade materials. Growth in electric passenger vehicle production is further accelerating the use of lightweight and high-performance metals across modern passenger car platforms globally.

Product Form Insights

Flat products are likely to dominate the product form segment with approximately 42% share in 2026 due to their extensive use in automotive body manufacturing and structural vehicle components. Products such as hot-rolled steel sheets, cold-rolled coils, and coated steel panels are widely utilized in body-in-white structures, doors, roofs, hoods, and floor assemblies. Automotive manufacturers prefer flat products because they support efficient stamping, forming, and welding processes required for high-volume vehicle production.

The increasing use of advanced high-strength steel grades within flat product applications is also supporting lightweight vehicle development without compromising structural safety. Established flat-rolling infrastructure and long-term OEM procurement contracts continue to strengthen market demand. As automakers focus on fuel efficiency, crash performance, and electric vehicle integration, flat products remain critical to modern automotive manufacturing and large-scale production operations worldwide.

Application Insights

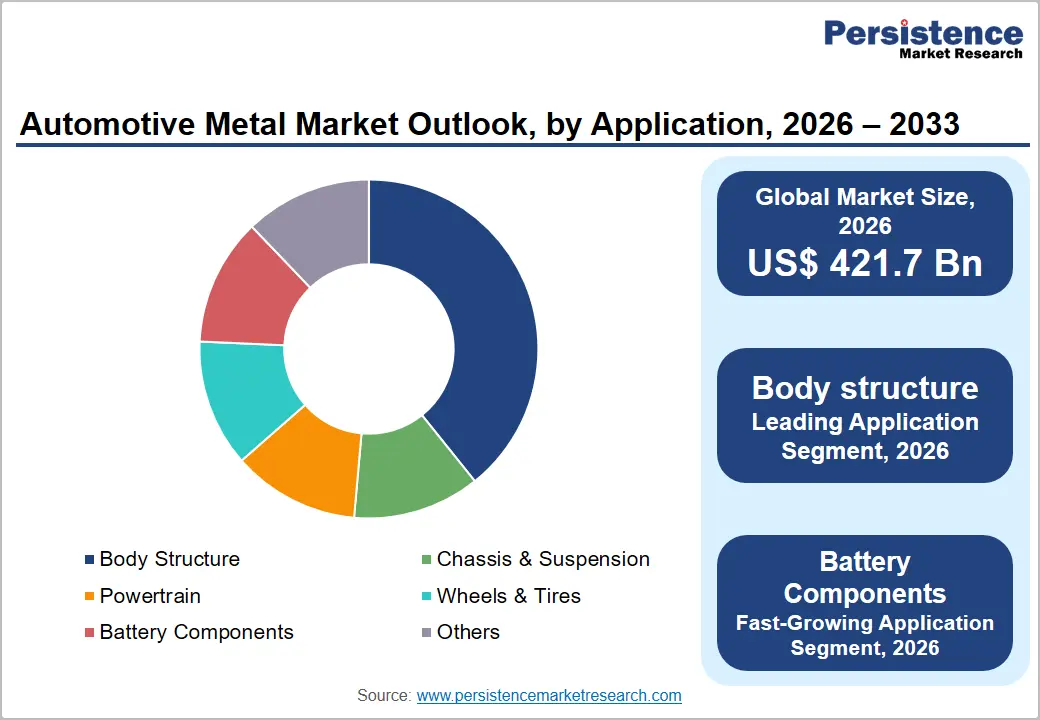

Body structure represents the leading application segment in the automotive metal market with approximately 35% share in 2026 due to its position as the largest metal-consuming component within vehicle manufacturing. Automakers increasingly utilize advanced high-strength steel, aluminum, and multi-material structures to improve crash performance, reduce vehicle weight, and enhance fuel efficiency. The body-in-white assembly requires significant volumes of automotive-grade metals for structural integrity, passenger safety, and durability under varying operating conditions.s

Advancements in joining technologies such as laser welding, structural adhesives, and friction stir welding are enabling the production of lighter and stronger vehicle body structures. The rapid expansion of electric vehicle production is also increasing demand for lightweight body engineering solutions to maximize driving range and battery efficiency. Continuous innovation in vehicle platform design further supports long-term demand for automotive metals within body structure applications.

End-user Insights

OEMs dominate the end-user segment with approximately 78% market share in 2025 due to the automotive industry’s highly integrated manufacturing and procurement structure. Vehicle manufacturers source large volumes of automotive-grade steel, aluminum, copper, and specialty alloys directly from global metal producers through long-term supply agreements and technical qualification programs. OEM procurement prioritizes consistent material quality, supply reliability, cost efficiency, and compliance with strict automotive engineering standards.s

Major automotive metal suppliers collaborate closely with OEMs during vehicle design and development processes to optimize lightweighting performance, crash safety, and manufacturing efficiency. The growing production of electric vehicles is further strengthening OEM demand for advanced lightweight materials and battery-compatible metal solutions. High-volume vehicle manufacturing operations across Asia Pacific, Europe, and North America continue to support stable and large-scale procurement demand from automotive OEMs globally.

Regional Insights

North America Automotive Metal Market Trends and Insights

North America represents approximately 20% of global automotive metal market revenue in 2026, with the region's competitive dynamics shaped by a combination of established domestic steel and aluminum production capacity, progressive electrification mandates from the U.S. EPA and Canada's emission reduction framework, and the transformative investment effects of the U.S. Inflation Reduction Act (IRA). The IRA's domestic content requirements for EV battery and vehicle components have catalyzed a reshoring of automotive metal processing capacity, particularly aluminum rolling and specialty steel production, that is structurally realigning supply chains toward North American producers.

Looking forward, the combination of IRA-driven EV investment momentum, U.S. Steel's capacity modernization programs, and Novelis' expanded recycled aluminum rolling capacity positions North America as a high-growth destination for EV-specific metal supply investment through 2033.

U.S. Automotive Metal Market Size

The United States accounts for approximately 85% of North American automotive metal demand, driven by the world's largest concentration of light vehicle assembly capacity outside China and the accelerating EV manufacturing build-out catalyzed by IRA tax credits. The U.S. automotive metal market is benefiting from nearshoring of EV battery and component manufacturing by General Motors, Ford, Tesla, and international OEMs, which is directly increasing domestic demand for aluminum sheet, copper, and AHSS grades.

The country's trajectory is firmly toward higher-value, EV-aligned metal grades as domestic EV penetration, projected to reach 50% of new car sales by 2030 under EPA targets, drives a structural shift in the metal type and product form mix consumed by U.S. automotive manufacturers.

Europe Automotive Metal Market Trends and Insights

Europe accounts for approximately 22% of global automotive metal market revenue in 2026, with market dynamics driven by the EU's stringent CO2 emission standards, the European Green Deal's industrial decarbonization agenda, and the regional automotive industry's deep commitment to electrification. The European Commission's mandate for 100% zero-emission new car sales by 2035 is accelerating OEM procurement transitions toward low-carbon, lightweight automotive metals, particularly recycled aluminum, advanced steel grades, and copper, while the EU Critical Raw Materials Act is reshaping upstream metal supply chain strategies. Europe's trajectory is toward a high-quality, sustainability-certified metal supply ecosystem in which EAF-based steel producers and high-recycled-content aluminum processors command pricing premiums over conventional primary metal suppliers.

Germany Automotive Metal Market Size

Germany accounts for approximately 28% of European automotive metal demand, reflecting its position as Europe's largest automotive production hub and home to premium OEMs including BMW, Mercedes-Benz, and Volkswagen Group. German OEMs' aggressive electrification roadmaps, with Volkswagen targeting 70% EV share of European sales by 2030, are driving significant structural shifts in aluminum and AHSS procurement. Germany's trajectory points toward increasing domestic demand for high-specification, low-carbon automotive metals as OEM Scope 3 emission commitments translate into binding supplier qualification requirements.

U.K. Automotive Metal Market Size

The United Kingdom represents approximately 12% of European Automotive Metal demand, anchored by vehicle manufacturing operations at Jaguar Land Rover, Stellantis' Ellesmere Port EV facility, and BMW's Mini plant in Oxford. The UK Automotive Council's Automotive Transformation Fund has committed £1 billion toward EV supply chain development, including battery and lightweight material processing investments that support domestic automotive metal demand. The UK's forward trajectory is high-end use of aluminum and specialty metal consumption as its automotive industry's EV transition reshapes the metal type mix procured by domestic manufacturers.

France Automotive Metal Market Size

France accounts for approximately 11% of European Automotive Metal demand, underpinned by Stellantis' and Renault Group's vehicle manufacturing operations and the French government's €26 billion electromobility investment plan announced through 2030. France's automotive metal demand is progressively shifting toward recycled aluminum and low-carbon steel grades as Renault's transition to electric Megane E-Tech and upcoming platforms increases per-vehicle aluminum content. France's trajectory is toward domestic low-carbon metal processing investment as OEMs seek to satisfy CSRD Scope 3 disclosure requirements with verified, France-sourced material.

Asia Pacific Automotive Metal Market Trends and Insights

Asia Pacific is the dominant regional market for automotive metal, commanding approximately 48% of global revenue in 2026, driven by China's position as both the world's largest automotive production market and the most advanced large-scale EV ecosystem. China's domestic automotive output, exceeding 30 million vehicles annually per OICA data, creates an unparalleled consumption base for flat steel, aluminum, and copper, while the country's EV penetration rate, which surpassed 35% of new car sales in 2023, is systematically increasing per-vehicle aluminum and copper content within the regional metal demand mix.

Looking forward, Asia Pacific is projected to grow at approximately 8.1% CAGR, sustained by India's vehicle production expansion, South Korea's EV platform investments, and Japan's hybrid-to-BEV transition, dynamics that collectively ensure the region's continued dominance and increasing strategic importance for global automotive metal suppliers.

India Automotive Metal Market Size

India accounts for approximately 8% of the Asia Pacific's automotive metal market and is among the region's fastest-growing national markets, driven by a domestic vehicle production base that surpassed 5.8 million units in 2023 per Society of Indian Automobile Manufacturers (SIAM) data and ongoing government support under the Production Linked Incentive (PLI) Scheme for automotive and advanced chemistry cell battery manufacturing.

The rapid expansion of domestic steel capacity, anchored by Tata Steel and JSW Steel, combined with increasing OEM demand for AHSS grades, positions India as a structurally important growth market for automotive-grade flat steel through 2033. India's trajectory points toward accelerating aluminum demand growth as its EV transition gains pace under the FAME III program and domestic EV production scales toward multi-million unit volumes.

Japan Automotive Metal Market Size

Japan represents approximately 15% of Asia Pacific's Automotive Metal demand, anchored by the global production platforms of Toyota, Honda, Nissan, and Mazda, manufacturers whose combined export-oriented output sustains Japan's position as a world-leading automotive metal consumption center. Nippon Steel & Sumitomo Metal Corporation, JFE Steel Corporation, and Kobe Steel collectively supply the majority of domestic automotive-grade steel and aluminum, maintaining tight OEM supply chain integration. Japan's forward trajectory is shaped by Toyota's large-scale BEV platform investments from 2026, which will structurally increase domestic aluminum and copper demand while sustaining premium AHSS demand for BEV structural components.

South Korea Automotive Metal Market Size

South Korea accounts for approximately 12% of Asia Pacific's Automotive Metal market, driven by Hyundai Motor Group's global vehicle production footprint and the country's world-class steel industry anchored by POSCO and Hyundai Steel. POSCO's investment in hydrogen-based steel production (HyREX technology) and Hyundai Steel's EV-specific AHSS grade development signal South Korea's intent to maintain technological leadership in premium automotive metal supply. South Korea's trajectory points toward deepening EV-aligned metal product innovation as Hyundai and Kia accelerate their global EV model rollouts across North America, Europe, and Asia Pacific.

Competitive Landscape

The global automotive metal market is moderately consolidated at the high-performance materials level, where large-scale production capacity, advanced metallurgical capabilities, and long-term OEM relationships create strong barriers to entry. Competition is increasingly defined by technological differentiation rather than price alone, with suppliers focusing on advanced high-strength steel, aluminum alloys, and specialty materials designed for lightweighting and safety compliance in modern vehicles. Market leaders strengthen their positions through deep integration with automotive manufacturers, offering co-engineering support during vehicle platform development and ensuring early-stage material specification wins.

Strategic priorities across the industry include investment in electric arc furnace-based production, expansion of recycling and scrap integration networks, and development of low-carbon and certified sustainable metal products. Companies are also aligning portfolios with electric vehicle requirements, particularly battery enclosures, structural components, and thermal management systems. Increasingly, producers are shifting toward solution-oriented business models that combine material supply with engineering services, digital simulation tools, and lifecycle carbon reporting. These strategies are helping firms secure long-term contracts while meeting tightening regulatory and sustainability expectations from global automotive OEMs.

Key Developments:

- April 2026: ArcelorMittal Nippon Steel India inaugurated a state-of-the-art automotive steel production line at its Hazira plant in Gujarat, strengthening domestic production of advanced high-strength steel for lightweight and safety-focused automotive applications.

- May 2025: Tata Steel Nederland launched HyperFlange®, a new hot-rolled steel product for automotive chassis and suspension parts that improves edge ductility, reduces material wastage, and supports lightweight vehicle manufacturing.

- March 2025: Handtmann announced new lightweight aluminum megacasting components for electric vehicles, including tailgates and front and rear structural sections, expanding its advanced die-casting production capabilities for next-generation automotive manufacturing.

Companies Covered in Automotive Metal Market

- ArcelorMittal

- Essar Steel

- Hyundai Steel

- Nippon Steel & Sumitomo Metal Corporation

- Novelis

- POSCO

- Tata Steel

- Thyssenkrupp AG

- United States Steel Corporation

- Voestalpine Group

- JFE Steel Corporation

- Steel Dynamics, Inc.

- Kobe Steel

- AMG Advanced Metallurgical Group

- Constellium NV

- Nucor Corporation

- Baowu Steel Group

- Outokumpu Oyj

- Salzgitter AG

- Aleris International

Frequently Asked Questions

The global Automotive Metal market is valued at US$ 421.7 billion in 2026 and is projected to reach US$ 668.3 billion by 2033, growing at a CAGR of 6.8%.

Growth is driven by rising electric vehicle production and increasing adoption of lightweight metals to meet emission regulations.

Asia Pacific leads the market with around 48% share due to strong vehicle manufacturing and rapid EV expansion.

Low-carbon and recycled metal production represents a major opportunity as automakers prioritize sustainable supply chains.

Key players include ArcelorMittal, Nippon Steel Corporation, POSCO, Novelis, Tata Steel, and thyssenkrupp AG.