- Automotive Components & Materials

- Regenerative Braking System Market

Regenerative Braking System Market Size, Share, and Growth Forecast 2026 - 2033

Regenerative Braking System Market by Component (Battery, Motor, ECU, Flywheel), Propulsion (BEV, PHEV, FCEV), Vehicle Type (Passenger Car, Light Commercial Vehicle, Heavy Commercial Vehicle, Electric Vehicles), and Regional Analysis for 2026 - 2033

Regenerative Braking System Market Size and Trend Analysis

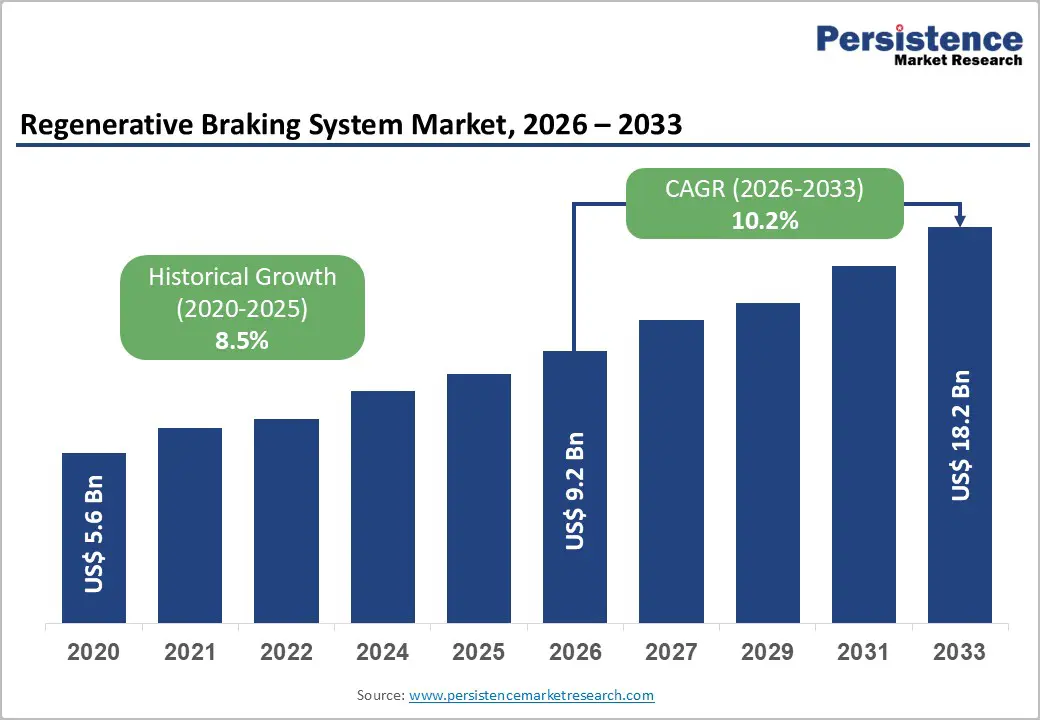

The global regenerative braking system market is valued at approximately US$ 9.2 billion in 2026 and is projected to reach US$ 18.2 billio by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

This robust and sustained growth trajectory is underpinned by the global automotive industry's decisive shift toward electrification, reinforced by stringent government emission mandates and exponentially rising Electric Vehicle (EV) adoption worldwide. According to the International Energy Agency (IEA), nearly 14 million new electric cars were registered globally in 2023, a 35% year-on-year increase, bringing the total global EV stock to 40 million vehicles, each of which relies on regenerative braking as a core energy recovery mechanism.

Key Industry Highlights:

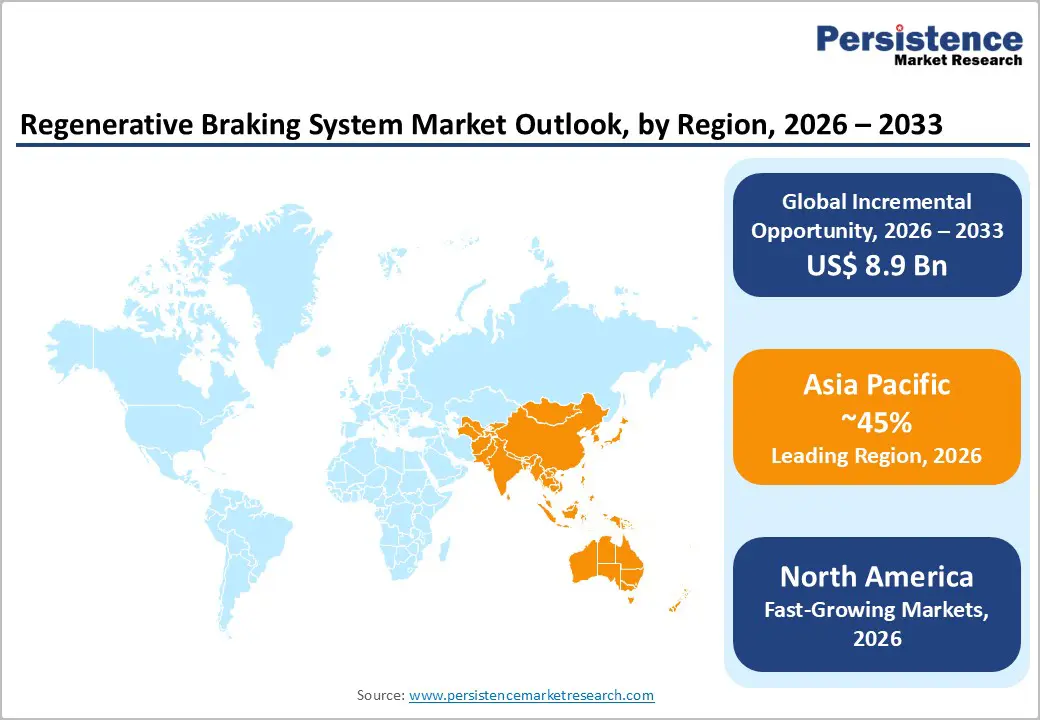

- Leading Region - Asia Pacific leads the global Regenerative Braking System market with approximately 45%revenue share in 2024, anchored by China's massive NEV fleet, Japan's advanced braking component suppliers, and rapidly expanding EV manufacturing across India and ASEAN nations.

- Fastest-Growing Region - North America is one of the leading regions in the global Regenerative Braking System market, with the United States serving as the primary demand driver.

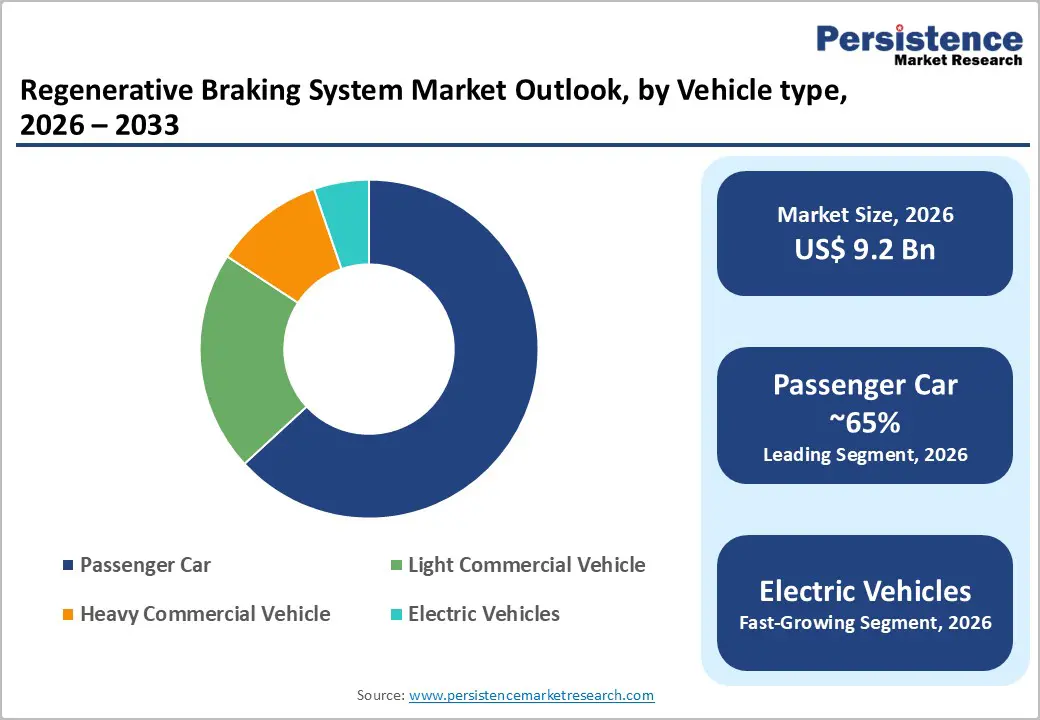

- Dominant Segment - The Battery component segment leads with approximately 41% revenue share, as traction batteries are the primary energy storage destination for regenerated kinetic energy in every BEV and PHEV powertrain, with global EV battery production exceeding 1 TWh in 2024 per the IEA.

- Fastest-Growing Segment - The Heavy Commercial Vehicle segment is the fastest-growing vehicle type, driven by urban zero-emission zone mandates, fleet electrification economics improving, and the superior energy recovery potential of high-mass vehicles in stop-and-go urban delivery and transit bus operations.

- Key Market Opportunity - ZF's July 2024 comprehensive brake-by-wire platform supporting up to Level 4 automation and Brembo's Sensify AI-driven smart braking system represent high-growth opportunities in software-optimized regenerative-friction brake blending for next-generation EVs and autonomous vehicles.

| Key Insights | Details |

|---|---|

| Regenerative Braking System Market Size (2026E) | US$ 9.2 Billion |

| Market Value Forecast (2033F) | US$ 18.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 10.2% |

| Historical Market Growth (2020 - 2025) | 8.5% |

DRO Analysis

Drivers - Exponential Growth in Electric and Hybrid Vehicle Adoption

The most powerful structural driver of the global Regenerative Braking System market is the accelerating worldwide transition to electric and hybrid vehicle powertrains, where regenerative braking is a non-optional core system. The IEA reported that global electric car sales reached approximately 14 million units in 2023, representing a 35% year-on-year increase and bringing the cumulative global EV fleet to 40 million vehicles. EV sales in the United States exceeded one in ten cars sold in 2024 per the IEA.

China the world's largest automobile market produced approximately 35 million vehicles domestically in 2023 per the International Trade Administration (ITA), with a rapidly rising share being New Energy Vehicles (NEVs) equipped with regenerative braking systems. Regenerative braking systems can recover 10-25% of kinetic energy during braking in urban drive cycles, extending EV range and reducing battery degradation making them indispensable to every battery-electric powertrain architecture.

Stringent Emission Regulations and Fuel Economy Standards

Global governments are enforcing increasingly stringent emission and fuel economy regulations that directly compel OEMs to integrate regenerative braking across all vehicle segments. In Europe, the EU's Fit for 55 package mandates a 55% reduction in passenger car CO2 emissions by 2030 and a 100% zero-emission requirement for new passenger cars from 2035 effectively mandating electrified powertrains in which regenerative braking is a core energy efficiency technology.

The Euro 7 regulation applicable to passenger cars from July 2025 additionally regulates non-exhaust brake particle emissions, incentivizing OEMs to maximize regenerative braking to minimize friction brake usage and associated particulate generation. In the United States, NHTSA's updated CAFE standards require significant improvements in fleet average fuel economy, while the EPA's emission rules similarly encourage energy recovery technologies.

Restraints - High System Complexity and Elevated Manufacturing Costs

Regenerative braking systems require integration of multiple advanced components high-voltage battery packs, electric motors/generators, power electronics, sophisticated ECUs, and brake-by-wire control systems resulting in significant cost premiums over conventional friction braking systems. The incremental cost of integrating a full regenerative braking system can add several thousand dollars to vehicle manufacturing cost, a barrier particularly acute for mass-market segments in price-sensitive emerging economies.

System complexity also demands specialized engineering competencies and precision manufacturing tolerances, creating entry barriers for smaller automotive suppliers and slowing adoption in developing markets.

Limited Energy Recovery Efficiency in Certain Driving Conditions

The energy recovery efficiency of regenerative braking systems varies significantly with driving patterns, reducing their value proposition in certain scenarios. On highways or at sustained high speeds, regenerative braking events are infrequent and of lower magnitude, limiting energy recovery below the 10-25% achievable in urban stop-and-go cycles.

In heavy commercial vehicles operating on mountainous routes with extended sustained deceleration, thermal management of recovered energy can also present engineering challenges. These efficiency limitations restrict the commercial payback period for regenerative braking investments in certain fleet and route types, moderating adoption in specific segments.

Opportunities - Brake-by-Wire Technology Integration and Software-Defined Braking

The emergence of brake-by-wire (BBW) technology which eliminates conventional hydraulic braking lines in favour of software-controlled electronic actuators represents a transformative opportunity for the Regenerative Braking System market. Brake-by-wire architectures enable seamless, software-optimized blending of regenerative and friction braking, maximizing energy recovery across diverse driving scenarios while enhancing pedal feel consistency.

In February 2024, Tevva (UK) and ZF Friedrichshafen AG successfully integrated a full Brake-by-Wire regenerative braking system into Tevva's 7.5-ton battery-electric truck designed for last-mile urban delivery demonstrating the technology's commercial readiness for commercial vehicles. In July 2024, ZF announced a comprehensive brake-by-wire platform designed for electric and automated vehicles operating entirely on electronic signals without hydraulic components, supporting up to Level 4 autonomous driving.

Heavy Commercial Vehicle Electrification and High-Capacity Energy Recovery

The accelerating electrification of Heavy Commercial Vehicles (HCVs) encompassing electric buses, electric trucks, and heavy-duty logistics vehicles presents an exceptionally high-value opportunity for regenerative braking system suppliers. Heavy commercial vehicles operate with substantially higher gross vehicle weights (15-40+ tonnes), generating proportionally larger kinetic energy during deceleration events, resulting in much greater absolute energy recovery potential than passenger cars.

SAF-HOLLAND launched its SAF TRAKr regenerative braking axle in September 2022, targeting refrigerated semi-trailers, tank trucks, and silo trailers with a high-voltage generator module delivering a maximum regenerative power of 20 kW. The IEA forecasts commercial vehicle electrification to accelerate significantly through 2030 as Total Cost of Ownership (TCO) economics improve.

Category-wise Analysis

Component Insights

The battery component segment leads the global regenerative braking system market, accounting for approximately 41% of total revenue in 2024. Batteries are the central energy storage medium for regenerated kinetic energy in both BEV and PHEV architectures, with every regenerative braking event directing recovered electrical energy back into the traction battery for subsequent propulsion use.

As EV battery pack capacities increase modern BEVs commonly featuring packs of 60-100+ kWh the absolute energy that can be captured and stored per braking event grows proportionally, reinforcing battery dominance in the component segment. The IEA reports that global EV battery production exceeded 1 TWh in 2024, all which interface with regenerative braking systems.

Propulsion Insights

The battery electric vehicle (BEV) propulsion segment dominates the global regenerative braking system market, holding the largest revenue share in 2024 of approximately 55%. BEVs depend entirely on electric propulsion and possess no internal combustion engine energy source making regenerative braking the only onboard energy recovery mechanism and rendering it critically important for maximizing driving range per charge.

The IEA reported 14 million new electric car registrations globally in 2023, the vast majority being BEVs, directly expanding the installed base for regenerative braking systems. Technological advancements in BEV motor and power electronics design including one-pedal driving modes that enable continuous regeneration during coasting are expanding regenerative braking's operating envelope.

Vehicle Type Insights

Passenger cars dominate the global market by vehicle type, accounting for approximately 60% of total revenue in 2024. This leadership reflects the world's largest vehicle segment in terms of production volume the International Organization of Motor Vehicle Manufacturers (OICA) documents global passenger car production of over 70 million units annually and the rapid penetration of electrified powertrains across mainstream and premium passenger car segments.

Nearly all BEVs and PHEVs in production globally integrate regenerative braking as a standard system. Heavy Commercial Vehicles (HCVs) buses and heavy trucks are the fastest-growing vehicle type segment, projected to expand at the highest CAGR through 2033 as fleet electrification economics improve, urban zero-emission zone mandates proliferate, and the superior energy recovery potential of high-mass commercial vehicles drives compelling total cost of ownership reductions.

Regional Analysis

Asia Pacific Regenerative Braking System Market Insights and Trends

Asia Pacific is the dominant region in the global Regenerative Braking System market, commanding approximately 45% of global revenue in 2024, driven by the world's largest automotive manufacturing base and the most aggressive EV transition programs. China the world's largest automobile market is the single most important country market, with the government's New Energy Vehicle (NEV) policy having catalyzed the world's largest installed base of electrified vehicles, all equipped with regenerative braking systems. China produced approximately 35 million vehicles domestically in 2023 per the International Trade Administration (ITA), with NEVs representing a rapidly expanding share.

Japan is home to global regenerative braking technology pioneers including Denso Corporation, AISIN Corp., and Advics Co., Ltd. all of which supply advanced braking components to Toyota, Honda, and Nissan's electrified platforms. Advics Co., Ltd. supplied its regenerative coordinated braking system for GAC Group's GS8 hybrid vehicle, demonstrating Japan's depth in electrified braking system supply chains. ASEAN nations particularly Thailand, Indonesia, and Vietnam are attracting EV OEM manufacturing investments, creating growing downstream demand for regenerative braking components aligned with their expanding electrified vehicle fleets.

North America Regenerative Braking System Market Insights and Trends

North America is one of the leading regions in the global Regenerative Braking System market, with the United States serving as the primary demand driver. EV sales in the U.S. exceeded one in ten cars sold in 2024, with the IEA confirming a roughly 10% electric vehicle market share for new light-duty vehicles a threshold that expands the installed base of vehicles requiring regenerative braking systems at an accelerating pace. The U.S. Corporate Average Fuel Economy (CAFE) standards and EPA emission regulations continue to mandate fleet-wide energy efficiency improvements, incentivizing OEM integration of regenerative braking across all electrified powertrain configurations.

The North American innovation ecosystem anchored by automotive technology suppliers headquartered in the region and innovation hubs in Michigan, California, and Ontario is driving next-generation brake system development. BorgWarner Inc. headquartered in Auburn Hills, Michigan offers advanced electrified powertrain components including integrated regenerative braking-compatible motor and power electronics systems. Canada contributes through growing EV manufacturing investments and national zero-emission vehicle mandates targeting 100% zero-emission new passenger car sales by 2035.

Europe Regenerative Braking System Market Insights and Trends

Europe is one of the most regulation-driven markets for regenerative braking systems globally, shaped by the European Union's comprehensive suite of automotive emission and energy efficiency legislation. The EU's Fit for 55 package mandates a 100% zero-emission requirement for all new passenger cars from 2035, effectively requiring full electrification and with it, universal regenerative braking integration across the European passenger car fleet within a decade. Germany is the region's dominant market, home to Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, and Brembo's European manufacturing operations.

Brembo partnered with Michelin in 2025 to launch the Sensify smart braking system an AI-driven, wheel-specific braking control platform designed specifically for EVs and autonomous vehicles that optimizes the blend between regenerative and friction braking in real time. Continental AG and Deep Drive (Munich) formed a joint development partnership in September 2024 to develop integrated wheel-unit core technologies for EVs combining braking and drive systems.

Competitive Landscape

The global regenerative braking system market is moderately consolidated, with Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen AG collectively holding a commanding share estimated at over 40% of the global automotive brake system market. These leaders differentiate through deep integration of regenerative systems with ADAS, ECU, and powertrain control, comprehensive OEM qualification portfolios, global manufacturing scale, and substantial R&D investment.

Key Developments:

- In February 2025, ZF Friedrichshafen AG launched an integrated brake-by-wire regenerative system aimed at improving coordination between friction and regenerative braking mechanisms.

- In June 2025, Hitachi Astemo introduced a next-generation inverter platform incorporating advanced thermal management to enhance regenerative braking efficiency and durability in battery electric vehicles.

Companies Covered in Regenerative Braking System Market

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- ZF Friedrichshafen AG

- BorgWarner Inc.

- Hyundai Mobis

- Eaton

- Brembo S.P.A.

- Skeleton Technologies GmbH

- Advics Co. Ltd.

Frequently Asked Questions

The global Regenerative Braking System market is estimated to be valued at US$ 9.2 Billion in 2026 and is projected to reach US$ 18.2 Billion by 2033, registering a CAGR of 10.2% during the forecast period 2026 - 2033.

The primary demand drivers are the global acceleration of EV and hybrid vehicle adoption with the IEA forecasting a global EV sales share of 35% by 2030 and regulatory mandates including the EU's Fit for 55 package (requiring 100% zero-emission new passenger cars by 2035), Euro 7 regulations on brake particle emissions effective from July 2025, and the U.S. CAFE and EPA standards.

The Battery Electric Vehicle (BEV) propulsion segment leads the global Regenerative Braking System market with approximately 55% of revenue share in 2024. BEVs rely entirely on electric propulsion with no combustion engine energy source, making regenerative braking the only onboard energy recovery mechanism and the most critical system for maximizing per-charge driving range.

Asia Pacific leads the global Regenerative Braking System market with approximately 45% of total revenue in 2024, anchored by China's world-leading New Energy Vehicle (NEV) production and deployment scale with the country producing approximately 35 million vehicles domestically in 2023 per the International Trade Administration (ITA).

The leading companies in the global Regenerative Braking System market include Robert Bosch GmbH, ZF Friedrichshafen AG, Continental AG, Hyundai Mobis, Eaton Corporation, AISIN Corp., and Advics Co., Ltd. Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen AG together hold a combined estimated market share of over 40% in the global automotive brake system industry.