- Hardware & Software IT Services

- ODM and EMS Wi-Fi Devices Market

ODM and EMS Wi-Fi Devices Market Size, Share, and Growth Forecast, 2026 - 2033

ODM and EMS Wi-Fi Devices market by Manufacturing Model (Original Design Manufacturing (ODM), Electronics Manufacturing Services (EMS)), Device Type (Wi-Fi Gateways, Wi-Fi Routers, Wi-Fi Access Points, Wi-Fi Mesh Nodes, and Miscellaneous.), Industry (IT & Telecom, Banking, Financial Services & Insurance (BFSI), Healthcare & Life Sciences, Manufacturing & Industrial, and Miscellaneous.), and Regional Analysis for 2026 - 2033

ODM and EMS Wi-Fi Devices Market Size and Trends Analysis

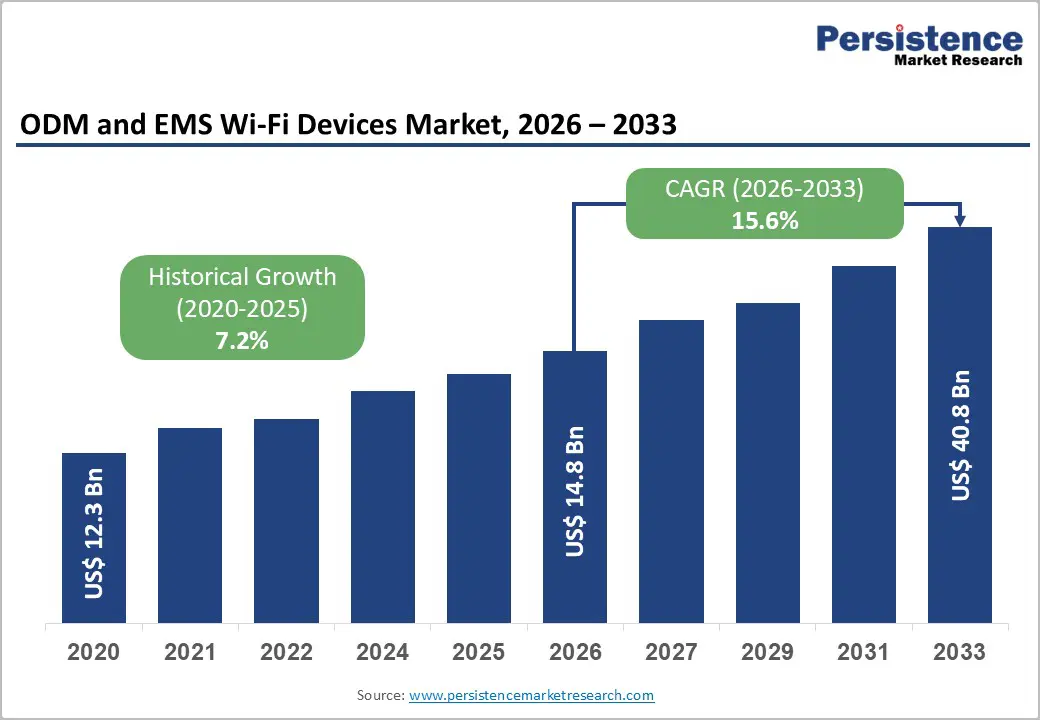

The global ODM and EMS Wi-Fi devices market size is likely to be valued at US$ 14.8 billion in 2026 and is projected to reach US$ 40.8 billion by 2033, growing at a CAGR of 15.6% between 2026 and 2033. This substantial expansion reflects the accelerating demand for advanced wireless connectivity solutions driven by 5G network proliferation, enterprise digital transformation, and the widespread adoption of Internet of Things (IoT) applications across residential, commercial, and industrial sectors.

The market's trajectory is underpinned by India's telecommunications sector gross revenue growth from US$ 39.22 billion in FY24 to US$ 43.42 billion in FY25, with internet penetration reaching 979 million subscribers by June 2025, and global internet users reaching 6 billion people, representing 74% of the world population in 2025.

Concurrent with Wi-Fi 6E and emerging Wi-Fi 7 technology adoption, delivering unprecedented bandwidth through the 6 GHz band with seven additional 160 MHz channels, organizations are requiring sophisticated ODM and EMS Wi-Fi device solutions addressing healthcare, enterprise, manufacturing, and telecommunications applications with enhanced performance, security, and management capabilities.

Key Industry Highlights:

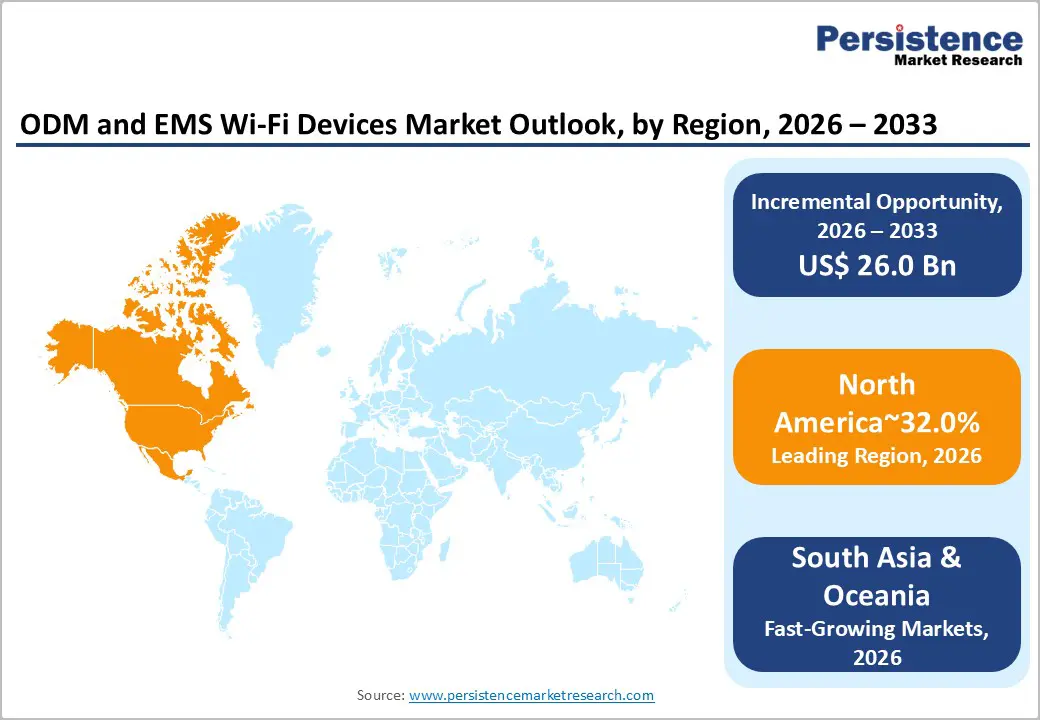

- Regional Leadership: North America dominates the global ODM and EMS Wi-Fi Devices Market with ~32% share in 2026, supported by rapid enterprise AI adoption, advanced healthcare connectivity, and accelerated 5G deployment.

- Fastest-Growing Region: India emerges as the fastest-growing region, driven by rural broadband expansion, 5G subscriber surge, indigenous electronics manufacturing initiatives, and government-backed infrastructure investments.

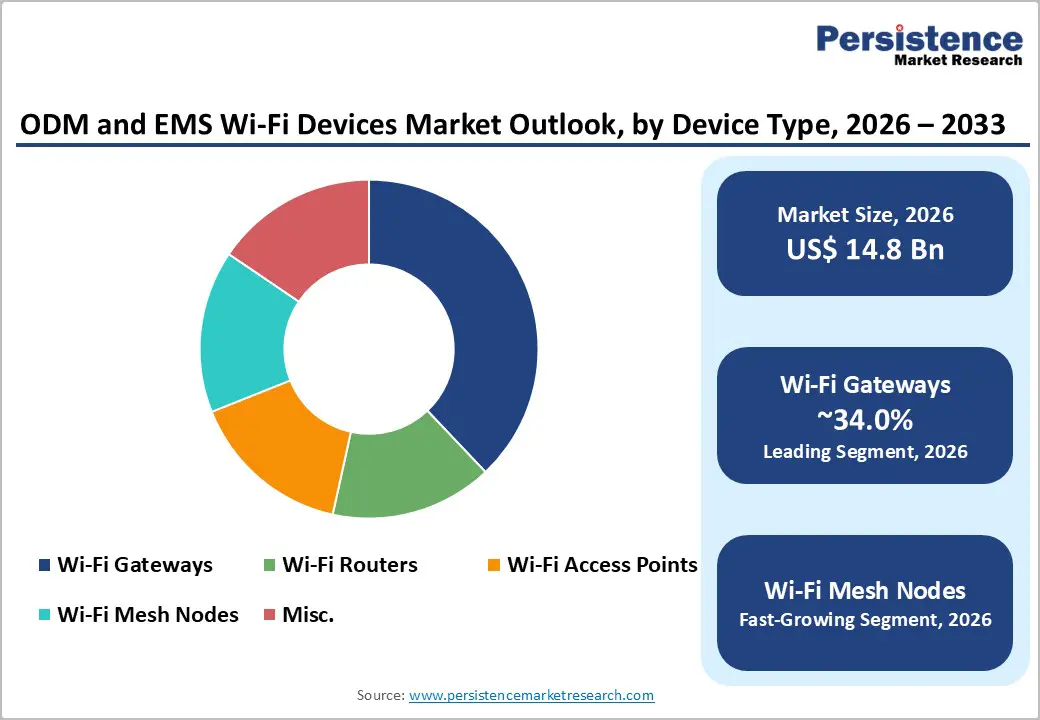

- Leading Device Segment: Wi-Fi gateways lead with ~34% market share in 2026, serving as primary network access points across residential, commercial, and small enterprise installations.

- Fastest-Growing Device Segment: Wi-Fi mesh nodes exhibit the fastest growth, fueled by demand for seamless coverage, IoT integration, automatic failover, and multi-location enterprise connectivity.

- Leading Industry: IT & Telecommunications remains the largest end-use segment with ~28% share in 2026, anchored by last-mile connectivity requirements, enterprise digital transformation, and broadband infrastructure expansion.

- Growing Industry: Healthcare & Life Sciences is the fastest-growing segment, driven by clinical AI adoption, connected medical devices, telemedicine, and mission-critical ultra-low latency Wi-Fi requirements.

- Technology & Growth Opportunity: Wi-Fi 6E and Wi-Fi 7 adoption, combined with enterprise AI and edge computing deployment, presents a substantial opportunity for ODM and EMS providers to deliver advanced, cloud-managed, and high-performance Wi-Fi solutions.

- Competitive Leadership: Foxconn, Pegatron, Askey, Arcadyan, and Sercomm lead the market through scale, vertical integration, strong ODM capabilities, and global manufacturing footprints supporting premium and carrier-grade Wi-Fi devices.

| Key Insights | Details |

|---|---|

|

ODM and EMS Wi-Fi Devices Market Size (2026E) |

US$ 14.8 Bn |

|

Market Value Forecast (2033F) |

US$ 40.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

15.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

12.3% |

Market Dynamics

Drivers - 5G Network Infrastructure Expansion and Wireless Technology Evolution

The global deployment of 5G networks represents a transformative driver fundamentally reshaping the ODM and EMS Wi-Fi devices market through complementary wireless connectivity requirements and infrastructure densification. The 5G infrastructure market is projected to surge from INR 1,19,966 crore (US$ 14 billion) in 2025 to INR 49,18,606 crore (US$ 574.4 billion) by 2035, growing at a 45% CAGR, directly corresponding to demand for Wi-Fi gateway, router, and access point solutions supporting 5G infrastructure integration and small cell deployment. India added a record 6,450 new 5G base stations in July 2025, its strongest monthly rollout in 2025, bringing the nationwide total to 4,92,520 base stations, requiring sophisticated backhaul and mesh networking solutions that ODM and EMS manufacturers provide.

The emergence of Wi-Fi 6E technology utilizing the 6 GHz spectrum band and early Wi-Fi 7 product announcements promise substantial performance improvements, with seven additional 160 MHz channels dramatically increasing available bandwidth and reducing interference in high-density environments. The ODM and EMS Wi-Fi devices market directly benefits from 5G deployment acceleration, as network operators, telecommunications providers, and infrastructure companies require advanced Wi-Fi gateway solutions, multi-band routers with superior interference management, and enterprise access points delivering reliable backhaul connectivity.

Askey Computer's debut of the RT5031W Tri-band Wi-Fi 6E MDU at Mobile World Congress 2025, featuring up to 1148 Mbps on 2.4 GHz, 4804 Mbps on 5 GHz, and 4804 Mbps on 6 GHz, exemplifies ODM innovation addressing 5G infrastructure requirements and smart building deployment.

Rise in Healthcare and Enterprise Adoption of Advanced Connectivity Solutions

Healthcare and enterprise sectors are driving unprecedented demand for sophisticated ODM and EMS Wi-Fi devices capable of supporting mission-critical applications, high device density, and strict security compliance requirements. Healthcare organizations are scaling AI adoption at 2.2x the rate of the broader economy, with AI applications including diagnostics, patient monitoring, and operational optimization requiring ultra-reliable, low-latency wireless connectivity.

Wi-Fi 7 deployment in healthcare enables remote surgery, real-time patient monitoring, electronic health record system integration, and telemedicine applications through multi-link operation, delivering ultra-low latency and 320 MHz channels supporting massive throughput. The ODM and EMS Wi-Fi Devices Market is experiencing corresponding demand for healthcare-grade access points, secure mesh networks, and gateway solutions ensuring HIPAA compliance, encryption of sensitive patient data, and seamless integration with medical IoT devices and imaging equipment.

Enterprise organizations deploying AI-driven analytics, cloud collaboration platforms, and advanced automation systems require enterprise-grade Wi-Fi infrastructure supporting thousands of simultaneous device connections without performance degradation. Large enterprises generating 61,519 TB of aggregated data consumption in India alone during FY25, with global wireless data usage reaching 2,28,779 PB in FY25, reflecting 17.46% growth from FY24, directly necessitate advanced router, gateway, and access point solutions managing network traffic, ensuring security, and optimizing bandwidth allocation. The ODM and EMS Wi-Fi Devices Market expands substantially as healthcare providers and enterprise organizations prioritize network infrastructure modernization, with 4G data representing 74.57% of total wireless data usage and emerging 5G data reaching 24.93% in FY25, reflecting the critical role of complementary Wi-Fi infrastructure in hybrid connectivity environments.

Internet of Things Proliferation and Smart Infrastructure Deployment

Internet of Things applications spanning smart homes, smart cities, industrial IoT, and connected healthcare are driving exponential demand for Wi-Fi mesh nodes, specialized gateways, and secure connectivity solutions.

The adoption of IoT standards, including oneM2M, promoted by India's Department of Telecommunications in August 2025, emphasizes secure, interoperable, and scalable IoT ecosystems requiring specialized ODM and EMS devices addressing IoT-specific connectivity, security, and management requirements. BharatNet initiative deployment of 13,01,193 fibre-to-the-home connections, creating rural connectivity infrastructure directly necessitates last-mile Wi-Fi mesh networks, outdoor access points, and residential gateways connecting villages to broadband infrastructure. Smart living experiences utilizing AWS IoT integration, home automation, intelligent lighting systems, and connected appliances require mesh node solutions providing seamless coverage, automatic failover capabilities, and cloud-connectivity management.

The market is experiencing accelerating demand for mesh nodes, specialized outdoor access points for IoT sensor networks, and integrated gateway solutions embedding security, device management, and analytics capabilities. Global IoT module outsourced manufacturing demonstrates the market's scale, with cellular IoT module ODM/EMS growth reaching 45% year-over-year in H1 2022, establishing foundation for complementary Wi-Fi device outsourcing expansion. Askey's RT5031W integration with AWS IoT Device Management, enabling seamless connectivity and control of thermostats, window sensors, and motion sensors exemplifies ODM innovation addressing smart living requirements and the broader ODM and EMS Wi-Fi Devices Market expansion trajectory.

Restraint - Supply Chain Complexities and Semiconductor Component Scarcity

The ODM and EMS Wi-Fi Devices Market faces substantial constraints from semiconductor supply chain disruptions, component scarcity, and manufacturing capacity limitations impacting device production and delivery timelines. Wi-Fi device manufacturing requires specialized semiconductor components including Wi-Fi System-on-Chips, memory modules, power management circuits, and RF components subject to global supply chain volatility.

Geopolitical tensions and trade restrictions affecting semiconductor supply from advanced manufacturing regions create procurement challenges and cost pressures on ODM and EMS manufacturers dependent on component sourcing from concentrated suppliers. Manufacturing capacity utilization challenges in established production regions necessitate geographic diversification, with companies expanding production facilities in India, Southeast Asia, and Latin America to mitigate supply chain concentration risks, requiring substantial capital investment and operational complexity.

Quality assurance and regulatory compliance requirements across multiple international markets including FCC regulations, RoHS directives, and cybersecurity protocols increase manufacturing costs and complexity. Foxconn's $1.5 billion investment in Tamil Nadu component production facility announced in May 2025 and Vietnam facility capacity expansion exemplify the substantial capital requirements for manufacturing diversification, constraining smaller ODM and EMS providers' ability to scale production.

Opportunity - Enterprise AI and Edge Computing Infrastructure Modernization

Enterprise digital transformation, artificial intelligence deployment, and edge computing architecture adoption represent substantial ODM and EMS Wi-Fi Devices Market opportunities, as organizations require advanced wireless infrastructure supporting AI workloads, real-time analytics, and autonomous systems. Enterprises deploying AI-driven analytics, machine learning pipelines, and autonomous automation systems require network infrastructure supporting massive data throughput, ultra-low latency, and consistent performance in high-density device environments spanning headquarters, branch offices, manufacturing facilities, and distribution centers.

The International Data Corporation projection that enterprise spending on AI services will surpass $200 billion by 2026, combined with edge AI infrastructure deployment reducing latency-sensitive AI processing to network edges, directly necessitates advanced ODM and EMS Wi-Fi solutions managing network complexity and ensuring reliable AI system operation.

The ODM and EMS Wi-Fi devices market is benefiting from enterprise organizations prioritizing network infrastructure modernization to support AI adoption, cloud computing integration, and autonomous systems deployment. Organizations require gateway solutions managing 5G backhaul and fiber connectivity, enterprise access points delivering unified management across distributed locations, and mesh networks addressing coverage requirements in facilities with challenging propagation characteristics.

Cloud-managed Wi-Fi platforms integrating AI-driven network optimization, predictive maintenance capabilities, and security threat detection represent premium ODM and EMS solutions commanding pricing premiums over baseline connectivity products. Enterprise customers are investing substantially in wireless infrastructure upgrades supporting Wi-Fi 6E and Wi-Fi 7 adoption, creating substantial ODM and EMS opportunities addressing technology transition requirements, backward compatibility management, and enterprise-scale deployment complexity requiring specialized consulting, integration, and managed services capabilities.

India's Telecommunications Expansion and Rural Connectivity Infrastructure

India's telecommunications sector positioned as the world's second-largest market with 1.21 billion total telephone subscribers and 86.09% tele-density by June 2025, combined with government initiatives emphasizing rural broadband deployment and digital infrastructure, represents substantial ODM and EMS Wi-Fi Devices Market opportunities for geographic expansion and manufacturing capability development. The BharatNet initiative deploying 13,01,193 fibre-to-the-home connections across rural villages requires last-mile Wi-Fi mesh networks, outdoor access points, and residential gateway solutions enabling consumers including farmers to access e-education, e-health, e-governance, and e-commerce services.

India's draft National Telecom Policy 2025 targeting doubling annual investment to Rs. 1,00,000 crore (US$ 11.67 billion) by 2030 directly corresponds to ODM and EMS manufacturing opportunity expansion, with state-backed initiatives emphasizing domestic semiconductor and electronics manufacturing development creating favorable policy environments for manufacturing facility establishment. India's projected 5G subscriber base surge to 980 million by 2030 from 290 million in 2024 necessitates complementary Wi-Fi infrastructure at industrial facilities, commercial establishments, and residential locations, creating sustained demand for advanced connectivity devices.

Indian companies including CG-Semi and Vervesemi Microelectronics are advancing domestic semiconductor innovation through SEMICON India 2025 initiatives and the Semiconductor Product Design Leadership Forum, signaling increasing capacity for specialized device design and manufacturing. The ODM and EMS Wi-Fi Devices Market benefits from India's investment climate, talent availability, manufacturing cost advantages, and growing domestic demand, with companies like Foxconn, Pegatron, and Askey expanding manufacturing capacity in India, Southeast Asia, and supporting geographic diversification strategies.

India's strategic emphasis on indigenous manufacturing, regulatory frameworks supporting electronics manufacturing development, and substantial infrastructure investment create distinctive opportunities for ODM and EMS providers establishing Indian operations, developing local supply chains, and capturing emerging market opportunities preceding broader global geographic expansion.

Category-wise Analysis

Device Type Insights

Wi-Fi gateways represent the largest device category, capturing approximately 34% of market share in 2026. Wi-Fi gateways function as integrated network access devices combining Wi-Fi router capabilities with broadband connectivity interfaces, serving as primary network entry points for residential and small commercial installations. Gateway devices integrate multiple connectivity technologies including Ethernet, coaxial cable connectivity for cable operators, and fiber interfaces, enabling seamless integration with diverse broadband delivery architectures.

Advanced gateway solutions embed quality-of-service management, parental controls, guest network functionality, and integration with smart home platforms, creating comprehensive connectivity and management solutions. The dominance of gateway devices reflects widespread residential deployment patterns where unified gateway solutions combine broadband interface termination, Wi-Fi radio transmission, and residential network management into single integrated devices. ODM and EMS manufacturers specialize in gateway design optimization addressing specific operator requirements, cost points, and feature differentiation.

Wi-Fi mesh nodes represent the fastest-advancing device segment within the ODM and EMS Wi-Fi Devices Market, reflecting expanding adoption of mesh network architectures enabling seamless coverage expansion, automatic failover, and simplified deployment across residential, commercial, and industrial environment

Industry Insights

The IT and Telecommunications industry represents the largest end-use segment within the ODM and EMS Wi-Fi Devices Market, commanding approximately 28% of market share in 2026. Telecommunications operators require gateway and router solutions addressing last-mile connectivity requirements, integrating with fiber, cable, and fixed wireless access infrastructure. IT service providers and systems integrators demand comprehensive ODM and EMS solutions addressing enterprise customer requirements for network modernization, remote work infrastructure, and digital transformation initiatives.

Healthcare and Life Sciences represent the fastest-advancing end-use industry segment within the ODM and EMS Wi-Fi Devices Market, driven by clinical AI adoption, connected medical device proliferation, and operational digitalization initiatives. Healthcare organizations require specialized Wi-Fi infrastructure supporting HIPAA compliance, medical device integration, ultra-low latency connectivity for time-sensitive applications, and seamless roaming across clinical environments.

The deployment of Wi-Fi 6E and Wi-Fi 7 technology in healthcare settings enables multi-link operation reducing latency to milliseconds, 320 MHz channels supporting massive medical imaging data throughput, and encryption meeting healthcare security and privacy requirement.

Regional Insights and Trends

North America ODM and EMS Wi-Fi Devices Market Trends

North America commands approximately 32% of the global ODM and EMS Wi-Fi Devices Market and represents a mature, technology-forward region driving innovation and premium product adoption. The United States telecommunications infrastructure investment emphasizing 5G deployment acceleration, fiber-to-the-home network expansion, and rural broadband initiatives drives substantial demand for gateway and router solutions. North American enterprises demonstrate the highest global AI adoption rates, requiring enterprise-grade Wi-Fi infrastructure supporting AI-driven analytics, cloud computing, and autonomous systems deployment.

Healthcare organizations across North America are prioritizing network modernization supporting telemedicine, real-time patient monitoring, and medical device integration, with Wi-Fi 6E and Wi-Fi 7 adoption supporting mission-critical application requirements.

East Asia ODM and EMS Wi-Fi Devices Market Trends

East Asia commands approximately 22% of the global ODM and EMS Wi-Fi Devices Market and represents the predominant manufacturing hub for ODM and EMS Wi-Fi device production. China's telecommunications sector revenues totaled 1.17 trillion yuan (approximately 167.6 billion U.S. dollars) in January-August 2024, with emerging sectors including big data, cloud computing, and Internet of Things posting strong performance.

Chinese telecom companies' emerging business revenue jumped 10.5 percent year-on-year to 289.7 billion yuan, demonstrating accelerating demand for advanced connectivity solutions. Taiwan-based manufacturers including Foxconn, Pegatron, Askey, and Gemtek maintain global manufacturing leadership, with facilities across China, Taiwan, Vietnam, and India supporting 5G infrastructure deployment and IoT device proliferation. Askey's March 2025 unveiling of the RT5031W Tri-band Wi-Fi 6E MDU demonstrates East Asian ODM innovation addressing multi-dwelling unit connectivity and IoT integration requirements.

East Asian government initiatives emphasizing domestic semiconductor and electronics manufacturing development create favorable policy environments accelerating regional manufacturing capacity and supply chain development.

Europe ODM and EMS Wi-Fi Devices Market Trends

Europe commands approximately 25% of the global ODM and EMS Wi-Fi Devices Market, representing a mature, regulation-focused region emphasizing data protection, security, and digital sovereignty. Europe's information and communication services sector numbered approximately 1.4 million enterprises in 2022, employing almost 7.2 million persons and generating €667 billion of value added, underscoring the region's substantial digital economy and corresponding connectivity infrastructure requirements.

European regulatory frameworks including GDPR, cybersecurity directives, and digital sovereignty requirements create distinctive compliance needs driving demand for specialized ODM and EMS Wi-Fi solutions embedding European-specific privacy, security, and data residency capabilities. Healthcare organizations across Europe are prioritizing network modernization supporting telemedicine, electronic health records integration, and medical device connectivity, with Wi-Fi 6E and Wi-Fi 7 adoption supporting clinical AI deployment.

Competitive Landscape

The global ODM and EMS Wi-Fi devices market exhibits a moderately consolidated structure, dominated by a limited number of large-scale ODM players with deep engineering capabilities, global manufacturing footprints, and long-standing relationships with tier-1 OEMs and telecom operators. Foxconn Technology Group and Pegatron Corporation anchor the market through high-volume EMS production, vertical integration, and strong supply-chain control across routers, gateways, and access points.

Alongside them, Taiwan-based Wi-Fi specialists such as Arcadyan Technology, Sercomm Corporation, and Askey Corporation play a critical role, leveraging in-house RF design, firmware development, and rapid product customization for broadband service providers. Gemtek Technology and Alpha Networks further strengthen the competitive core by focusing on carrier-grade and enterprise Wi-Fi platforms, particularly for Wi-Fi 6 and Wi-Fi 6E deployments.

While several mid-sized and regional players operate in niche or cost-driven segments, pricing power, scale advantages, and design ownership remain concentrated among these leading firms. As a result, the market is not fully fragmented, yet it stops short of a strict oligopoly due to ongoing entry by regional ODMs targeting specific geographies and customer requirements.

Key Industry Developments:

- October 1, 2024, Gemtek Technology Co., Ltd. – Gemtek, in collaboration with Adant Technologies Inc., announced the development of a compact tri-band 2×2 Wi-Fi 7 mesh extender (TB-372s), strengthening its ODM portfolio in next-generation Wi-Fi mesh devices. The solution integrates smart antenna optimization technology to deliver improved throughput, coverage, and reliability, targeting advanced home networking and mesh Wi-Fi deployments

- October 23, 2023, Gemtek Technology Co., Ltd. – Gemtek, in collaboration with MaxLinear, launched two Wi-Fi 6 AX3000 PON Home Gateway Units (TB-362 and TB-380), reinforcing its ODM capabilities in carrier-grade Wi-Fi gateway manufacturing. The solutions integrate 10G G-PON/XGS-PON and Wi-Fi 6 SoCs to support scalable FTTH deployments while enabling service providers to accelerate time-to-market and optimize operational efficiency.

Companies Covered in ODM and EMS Wi-Fi Devices Market

- Foxconn Technology Group

- Pegatron Corporation

- Arcadyan Technology Corporation

- Sercomm Corporation

- Askey Corporation

- Gemtek Technology Co., Ltd.

- Alpha Networks Inc.

- Delta Networks, Inc.

- Kinpo Electronics, Inc.

- Accton Technology

- Actiontec Electronics, Inc.

- VVDN Technologies

Frequently Asked Questions

The global ODM and EMS Wi-Fi Devices market is projected to be valued at US$ 14.8 Bn in 2026.

The Wi-Fi Gateways segment is expected to account for approximately 34.0% of the global ODM and EMS Wi-Fi Devices market by Device Type in 2026.

The market is expected to witness a CAGR of 15.6% from 2026 to 2033.

The ODM and EMS Wi-Fi Devices market is driven by rapid 5G network expansion, evolution toward Wi-Fi 6E and Wi-Fi 7 technologies, rising healthcare and enterprise demand for high-performance connectivity, and the large-scale proliferation of IoT and smart infrastructure deployments.

Key market opportunities in the ODM and EMS Wi-Fi Devices market include enterprise AI- and edge-driven network infrastructure modernization and large-scale telecommunications expansion particularly India’s 5G, rural broadband, and indigenous manufacturing push driving sustained demand for advanced, cloud-managed, high-performance Wi-Fi solutions.