- Construction & Engineering

- North America Roofing Market

North America Roofing Market Size, Share, and Growth Forecast, 2026 - 2033

North America Roofing Market by Material Type (Asphalt Shingles, Metal Roofing (Steel, Aluminum, Copper), Concrete & Clay Tiles, Polymer & Synthetic Roofing (TPO, PVC, EPDM), Wood Shingles & Shakes), End User (Residential, Commercial, Industrial), Application (New Construction, Renovation / Replacement), and, and Country Analysis for 2026 - 2033

North America Roofing Market Size and Trends Analysis

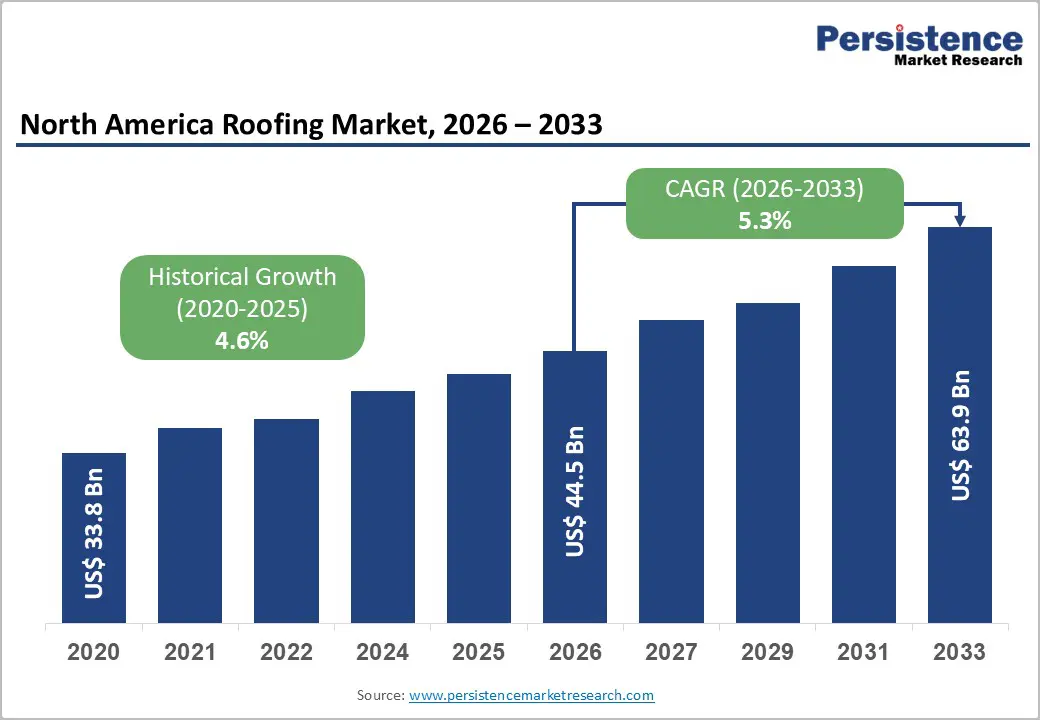

The North America roofing materials market size is likely to be valued at US$ 44.5 billion in 2026 and is projected to reach US$ 63.9 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. The market established a strong historical foundation at US$ 33.0 Bn in 2020, reflecting a historical CAGR of 4.6% through 2026, anchored by the structural resilience of the North American construction ecosystem and consistent investment in both residential and commercial building activity.

Total U.S. construction spending reached US$ 2.16 trillion in January 2024, nearly tripling from US$ 822.1 billion in January 2010, with private construction alone advancing to US$ 1.68 trillion by January 2024, each milestone translating directly into roofing material procurement demand. Rise in post-disaster re-roofing activity, federal infrastructure spending commitments, the sustained commercial real estate build-out cycle, and a decisive industry pivot toward energy-efficient and climate-resilient roofing systems collectively sustain the North America Roofing Materials Market's multi-year growth trajectory through the 2033 forecast horizon.

Key Industry Highlights:

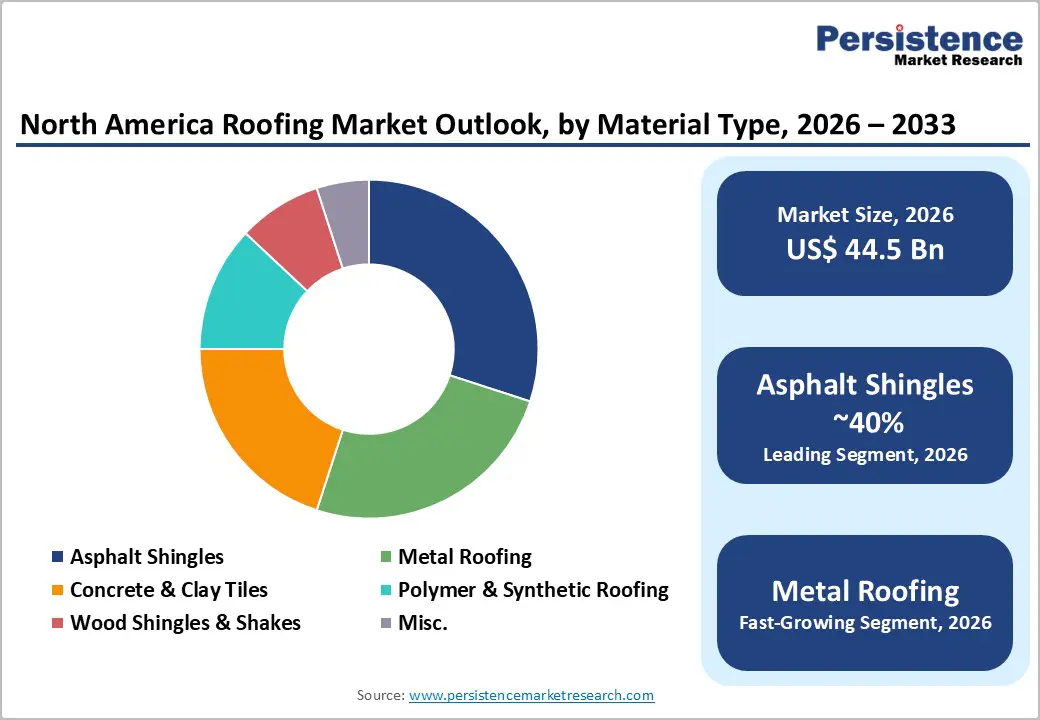

- Asphalt Shingles Lead the Market: Asphalt shingles account for 45% of market revenue in 2026, with strong adoption in U.S. residential construction due to cost-effectiveness, fire resistance, and widespread contractor familiarity.

- Metal Roofing Fastest-Growing Segment: Driven by industrial facilities, commercial buildings, and storm-hardened residential projects, metal roofing, including steel, aluminium, and copper, is expanding rapidly due to durability, recyclability, and solar integration potential.

- Residential Sector Dominates End-Use: Residential construction represents 55% of market revenue, fueled by strong single- and multi-family housing activity in the U.S. and Canada and post-storm replacement demand.

- Commercial and Non-Residential Segment Grows Rapidly: Grade A office parks, data centres, logistics warehouses, and institutional projects are driving fast-paced growth in commercial roofing demand across major North American urban centres.

- Government Programs Driving Market Demand: Federal initiatives, including the Infrastructure Investment and Jobs Act, FEMA resilience programs, and clean energy incentives under the Inflation Reduction Act, are acting as strong demand catalysts for high-performance and solar-ready roofing systems.

| Key Insights | Details |

|---|---|

| North America Roofing Market Size (2026E) | US$ 44.5 Bn |

| Market Value Forecast (2033F) | US$ 63.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Drivers - Structural Surge in U.S. and Canadian Construction Expenditure Driving Sustained Roofing Procurement

The North America Roofing Materials Market is directly and proportionally linked to the trajectory of total construction spending across the United States and Canada, as every newly permitted residential, commercial, or industrial structure represents a primary procurement event for roofing materials. This relationship ensures that the breadth of construction investment activity directly determines the volume and value of roofing product demand across all material categories.

Total U.S. construction spending reached US$ 2.16 trillion in January 2024, up from US$ 1.49 trillion in January 2020 and US$ 822.1 billion in January 2010, reflecting an extraordinary multi-decade trajectory of sector expansion. U.S. residential construction spending reached US$ 912.8 billion in 2024, recovering from the US$ 606.9 billion level recorded in 2022. Concurrently, nonresidential construction in the U.S. surged to a projected US$ 1.25 trillion in 2024 from US$ 558.4 billion in 2010.

In Canada, total building permits reached CAD 138.4 billion in October 2025, with commercial permits alone surging to CAD 27.99 billion, 25.8% above December 2024 commercial levels, signalling continued non-residential pipeline depth. This broad-based construction investment momentum on both sides of the border creates a structurally resilient and expanding demand base for the North America Roofing Materials Market.

Federal Infrastructure Investment and Climate-Resilient Construction Standards Reshaping Roofing Specifications

Federal legislative action and tightening building code requirements for climate resilience are reconfiguring roofing material specifications across both the re-roofing and new construction segments of the North American Roofing Materials Market. Policy-driven construction activity translates directly into incremental demand for higher-performance roofing systems across public facilities, transportation infrastructure, and federally assisted housing programs.

U.S. public construction spending advanced to US$ 484.3 billion in January 2024, the highest level on record and a significant acceleration from US$ 299.0 billion in January 2010, driven by construction commitments under the Infrastructure Investment and Jobs Act and the Inflation Reduction Act. The U.S. Federal Emergency Management Agency (FEMA) Building Resilience Initiative has progressively tightened wind resistance, hail impact, and fire rating requirements for roofing products used on federally funded structures, compelling specification upgrades toward Class 4 impact-resistant shingles and metal systems.

According to a September 2024 survey by Leaf Home, 51% of U.S. homeowners expressed active interest in weather-related home improvements, underscoring the consumer-level demand signal reinforcing re-roofing demand across climate-vulnerable geographies in the South, Midwest, and coastal Northeast.

Commercial Real Estate Development Cycle and Industrial Facility Construction: Elevating Membrane and Metal Demand

The sustained commercial real estate development cycle across major U.S. metropolitan areas and Canada's urban centers is driving structurally elevated demand for commercial-grade roofing membranes, standing-seam metal systems, and thermoplastic single-ply products in the North American Roofing Materials Market. Commercial buildings with large low-slope roof areas consume materially more roofing product per square foot of floor area than residential structures, making this end-use category a high-value revenue driver per project.

U.S. commercial construction spending reached US$ 143.0 billion in 2024, up from US$ 43.4 billion in 2010 and US$ 91.6 billion in 2020, with the sector maintaining its highest spending level across the entire 14-year data series In 2024, over 75% of new industrial facilities in North America specified metal roofing systems, reflecting sector-wide confidence in metal's performance characteristics for large-span industrial structures. Canada's institutional and governmental construction permits surged to CAD 16.37 billion in October 2025, 31.5% above November 2025 levels, adding public facility roofing demand to the commercial procurement pipeline.

Restraint - Material Cost Volatility and Supply Chain Disruptions Constraining Contractor Margins

The North America Roofing Materials Market faces material pressure from input cost volatility, particularly for petroleum-derived asphalt, steel coil, and polymer membranes. Crude oil price fluctuations directly pass through to asphalt shingle pricing, while steel tariff actions under U.S. Section 232 duties have elevated coated steel roofing costs for both domestic manufacturers and importers. U.S. residential construction spending declined to US$ 606.9 billion in 2022 from a peak partially driven by material cost escalation and supply chain friction, a dynamic that compressed both roofing project volumes and contractor profitability, illustrating the direct market impact of input cost instability.

Key Market Opportunities

Solar-Integrated Roofing Systems and Energy Code Mandates Creating High-Value Product Demand

The convergence of state-level renewable energy mandates, federal clean energy tax incentives under the Inflation Reduction Act, and consumer demand for energy cost reduction is creating a high-value, structurally additive opportunity for solar-integrated and energy-reflective roofing solutions within the North America Roofing Materials Market. Building-integrated photovoltaic roofing removes the traditional separation between roof system and energy generation, enabling installers and product manufacturers to command significant price premiums over conventional roofing.

In March 2024, GAF launched its Solar Integrated Roofs system, combining solar panels and asphalt roofing shingles into a single product to streamline installation and enhance energy performance for homeowners, directly targeting the large-scale residential re-roofing market.

The U.S. Department of Energy (DOE) Solar Energy Technologies Office has committed funding to building-integrated PV research, and states including California, New York, and Massachusetts have enacted solar-ready building code requirements that effectively mandate solar-compatible roof system specifications on new construction. Metal roofing's demonstrated energy savings of up to 30% versus traditional materials according to published energy performance data, further positions it as a primary specification beneficiary of energy efficiency mandates across the North America Roofing Materials Market.

Post-Storm Re-Roofing Demand and Climate Adaptation Infrastructure Creating Durable Replacement Cycles

The escalating frequency and severity of severe weather events across North America including hurricanes, hailstorms, wildfires, and freeze-thaw cycles is structurally elevating the addressable re-roofing market, as damaged and aged roof systems require replacement with higher-performance, impact-rated materials. This demand vector is policy-reinforced, repeating, and non-discretionary in nature, creating a reliable revenue base for contractors and product manufacturers participating in the North America Roofing Materials Market.

FEMA's Hazard Mitigation Grant Program and HUD's Community Development Block Grant Disaster Recovery programs collectively direct billions of dollars annually into storm-damaged residential and commercial roof replacement activity across the Gulf Coast, Midwest tornado corridor, and Western wildfire regions.

The National Oceanic and Atmospheric Administration (NOAA) reported that the U.S. experienced 28 weather and climate disaster events exceeding US$ 1 billion in losses in 2023, each generating subsequent roofing replacement demand. As insurance carriers and state building codes progressively mandate Class 4 impact-rated shingles and fire-resistant roofing in high-risk zones, the North America Roofing Materials Market benefits from both volume replacement demand and per-unit value uplift from specification upgrades to premium-grade materials.

Category-wise Analysis

Material Type Insights

Asphalt Shingles command the dominant position within the North America Roofing Materials Market's Material Type segmentation, holding approximately 45% of total material type revenue in 2026. This leadership reflects more than a century of residential installation heritage, broad contractor familiarity, and an unmatched cost-performance proposition for residential pitched-roof applications across the U.S. and Canada.

Asphalt shingles offer fire resistance ratings up to Class A, a wide range of aesthetic profiles, and, according to CertainTeed Corporation, high-quality roofing slats and shingles can last more than 50 years when properly installed. The IKO Industries introduction of computer-controlled manufacturing systems in 2024 has significantly advanced product uniformity in raw material use, shingle weight, and dimensional control, reinforcing quality consistency advantages. Demand from the US$ 912.8 billion residential construction spending pipeline in 2024 ensures that asphalt shingles retain their majority position across the forecast horizon.

Metal Roofing is the fastest-growing material segment within the North America Roofing Materials Market, propelled by demand from commercial facilities, industrial buildings, storm-hardened residential re-roofing, and sustainability-mandated specifications across the region.

In 2024, over 75% of new industrial facilities in North America specified metal roofing systems, reflecting contractors' and facility managers' alignment with metal's superior wind uplift resistance, 50-year lifespan credentials, and 100% recyclability at end of service life. Galvanised steel variants remain the top-volume specification due to cost-effectiveness, while aluminium and copper systems command premium pricing in coastal and luxury residential applications.

Application Insights

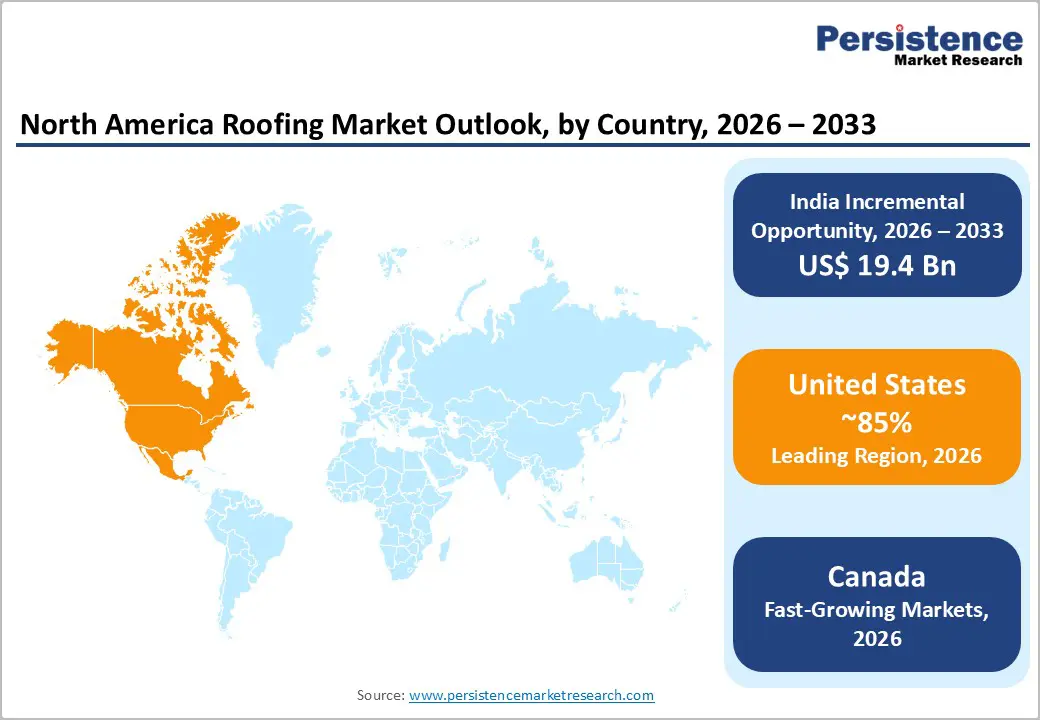

The Residential segment is the dominant end-use category of the North America Roofing Materials Market, holding approximately 55% of total market revenue in 2026. U.S. residential construction spending reached US$ 912.8 billion in 2024, recovering strongly from US$ 606.9 billion in 2022, with single-family and multi-family housing activity generating proportional demand for roofing materials across new construction and re-roofing applications.

In Canada, residential building permits reached CAD 85.2 billion in October 2025, with multi-dwelling permits alone surging to CAD 58.9 billion in that single month, driven by urban population density requirements and rental market investment. Post-storm re-roofing demand in suburban residential markets across the South and Midwest further reinforces the segment's aggregate consumption volumes. The September 2024 Leaf Home survey finding that 51% of U.S. homeowners expressed active interest in weather-related improvements underscores the structural depth of residential replacement demand.

The Commercial and Non-Residential segment is the fastest-growing end-use category within the North America Roofing Materials Market, underpinned by an accelerating U.S. commercial construction spending cycle and expanding Canadian institutional development programs. U.S. commercial construction spending reached US$ 143.0 billion in 2024, its highest level since 2010, with office parks, data centres, logistics warehouses, and retail centres each requiring large-area, long-durability roofing systems.

Competitive Landscape

The North American roofing market is moderately consolidated, with a few large manufacturers and contractors dominating both residential and commercial segments. Leading players such as GAF, TAMKO®, CertainTeed, Holcim, Tecta America, and Austin Roofing & Waterproofing hold significant market influence through product innovation, extensive distribution networks, and large-scale project execution. While the residential market remains competitive with regional and local contractors offering niche solutions, commercial and industrial roofing is dominated by major players capable of delivering complex projects.

Recent trends, including metal roofing adoption, roof restoration, sustainability, and climate-resilient systems, have intensified competition, prompting top companies to invest in new technologies, contractor programs, and acquisitions. Smaller and regional contractors continue to thrive in speciality segments, creating a fragmented mid- and lower-tier market alongside the consolidated leadership.

Key Industry Developments:

- In March 2026, Austin Roofing & Waterproofing Incorporated, Canada’s leading commercial and industrial roofing contractor, expanded its expertise in metal roof coatings and steel roof restoration across Ontario. The company promotes fluid-applied coatings as cost-effective, sustainable alternatives to full roof replacements, reflecting a trend toward roof restoration and lifecycle cost management in North America.

- In March 2026, Tecta America, the largest commercial roofing contractor in the U.S., acquired Roofing Standards in Placentia, California. The acquisition strengthens Tecta America’s presence in California, allowing Roofing Standards to operate under its brand while benefiting from Tecta’s support. This move highlights market consolidation and regional expansion trends among leading North American commercial roofing contractors.

- In January, 2026, GAF, North America’s largest roofing and waterproofing manufacturer, showcased innovative residential and commercial roofing solutions at the 2026 International Roofing Expo in Las Vegas. Highlighted products included Timberline HDZ® shingles and TimberSteel™ metal roofing systems, as well as maintenance solutions like UltraClear Roof Sealant, reinforcing a focus on resilience, sustainability, and installation efficiency.

- In February, 2026, CertainTeed showcased its latest resilient residential and roofing solutions at the International Builders’ Show in Orlando, Florida. The company introduced new colorways across products like RISE®, STONEfaçade, and Landmark® Solaris®, emphasizing durability, wind resistance, and design-driven performance, reflecting a focus on high-performance and climate-resilient roofing systems.

Companies Covered in North America Roofing Market

- CertainTeed Corporation

- TAMKO Building Products

- Atlas Roofing Corporation

- GAF

- Owens Corning

- Johns Manville

- Carlisle Companies Incorporated

- IKO Industries Ltd.

- Firestone Building Products Company, LLC

Frequently Asked Questions

The North America Roofing Market is projected to be valued at US$ 44.5 Bn in 2026.

The Asphalt Shingles segment is expected to account for approximately 45% of the North America Roofing Market by Material Type in 2026.

The market is expected to witness a CAGR of 5.3% from 2026 to 2033.

The North America Roofing Market growth is driven by rising U.S. and Canadian construction spending, federal infrastructure investment, climate-resilient building codes, and strong demand from residential, commercial, and industrial projects.

Key market opportunities in the North America Roofing Market lie in solar-integrated and energy-efficient roofing solutions, and in post-storm re-roofing driven by climate adaptation and disaster recovery programs.

Key players in the Roofing Market include CertainTeed Corporation, TAMKO Building Products, Atlas Roofing Corporation, GAF, Owens Corning, and Johns Manville.