- Industrial Goods & Service

- Metallographic Machine Market

Metallographic Machine Market Size, Share, and Growth Forecast 2026 - 2033

Metallographic Machine Market by Machine Type (Sectioning Machines, Mounting Machines (Hot Mounting, Cold Mounting), Grinding & Polishing Machines, Hardness Testing Machines, Microscopes, Image Analysis Machines), Industry (Metallurgy, Automotive & Transportation, Aerospace & Defense, Electronics & Semiconductor, Academic & Research Institutes, Healthcare & Medical Devices, Others), by Regional Analysis, 2026 - 2033

Metallographic Machine Market Size and Trend Analysis

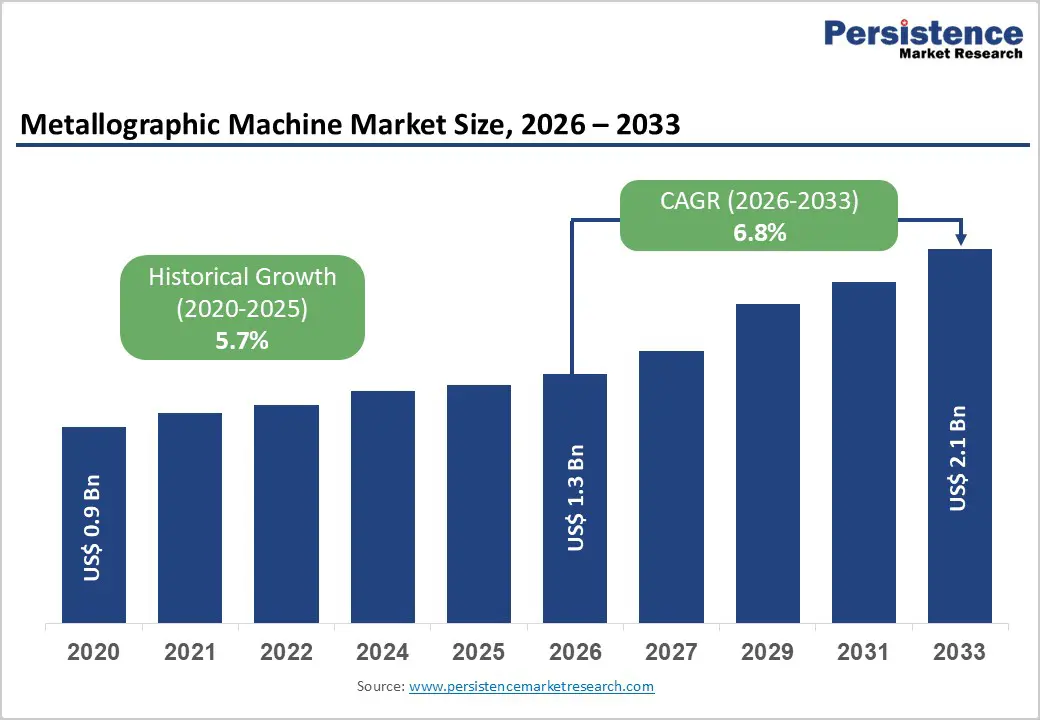

The global metallographic machine market size is expected to be valued at US$ 1.3 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

This robust growth is underpinned by accelerating global demand for precision materials characterization across a broadening range of advanced manufacturing and research-intensive end-use industries. The entire metallographic preparation workflow, encompassing sectioning, mounting, grinding, polishing, hardness testing, microscopic examination, and digital image analysis, is experiencing simultaneous demand expansion as quality standards tighten and semiconductor and additive manufacturing sectors create entirely new characterization requirements.

Regulatory mandates from ASTM International, ISO, and DIN, combined with multi-billion-dollar public research investments through programs including Horizon Europe and the U.S. CHIPS and Science Act 2022 is creating durable, multi-cycle equipment procurement demand that distinguishes this market’s growth profile from broader capital equipment trends.

Key Industry Highlights:

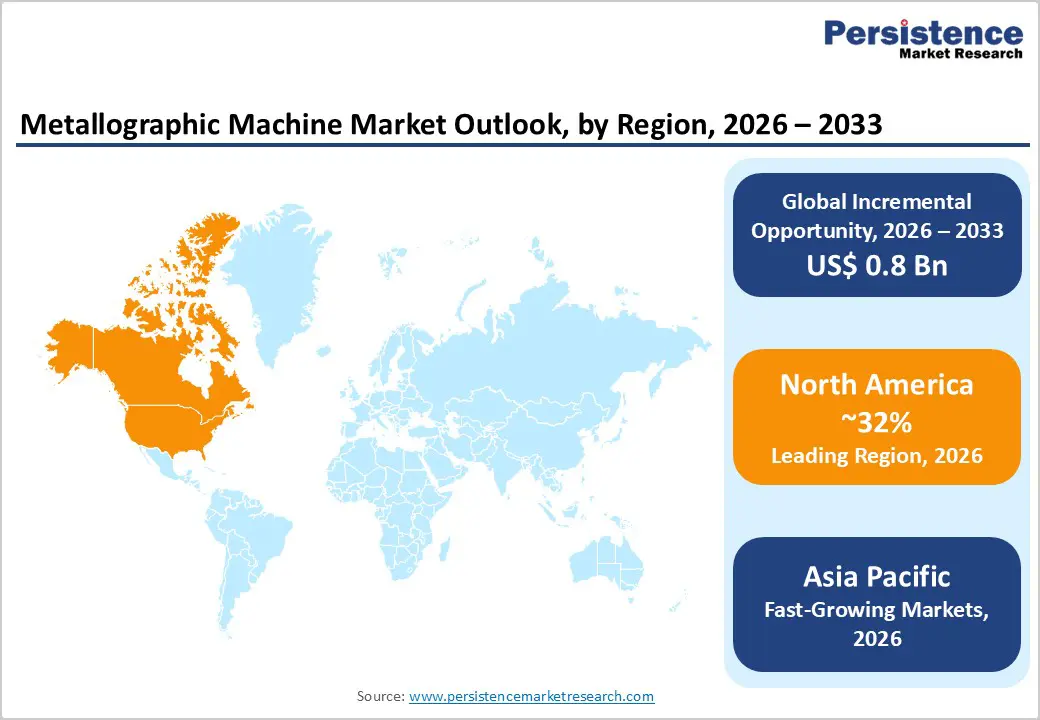

- Leading Region: North America leads the global Metallographic Machine market with 32% share in 2025, driven by the U.S. CHIPS and Science Act’s US$ 52 billion semiconductor investment, world-class national research laboratories, and the domestic presence of global leaders Buehler and LECO Corporation.

- Fastest Growing Region: Asia Pacific is the fastest growing region during 2026 - 2033, propelled by China’s 1.0 billion tonne annual steel output, semiconductor fab investment under the 14th Five-Year Plan, and India’s expanding metals and defense manufacturing base supported by the PLI scheme.

- Dominant Segment: Grinding & Polishing Machines dominate the machine type segment with approximately 28% market share in 2025, reflecting their multi-stage, high-frequency use in every metallographic workflow and strong adoption of automated polishing systems in industrial quality laboratories per ASTM E3 standards.

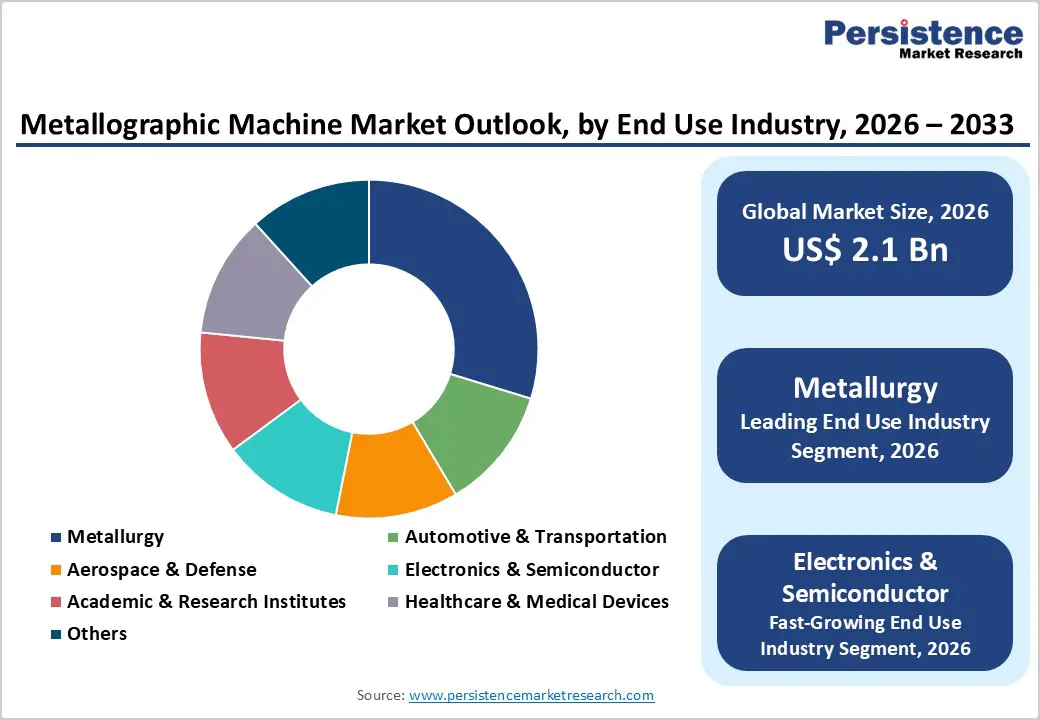

- Fastest Growing Segment: Electronics & Semiconductor is the fastest growing end-use industry segment during 2026 - 2033, driven by over US$ 200 billion in global fab construction under the U.S. CHIPS Act, EU Chips Act, and national semiconductor programs in South Korea, Japan, and Taiwan.

- Key Opportunity: The convergence of additive manufacturing scale-up, supported by ASTM F42 standards and America Makes quality initiatives, with maturing SLM, DED, and binder jetting platforms creates the most significant new characterization demand opportunity for the complete metallographic machine workflow through 2033.

| Key Insights | Details |

|---|---|

| Metallographic Machine Market Size (2026E) | US$ 1.3 Billion |

| Market Value Forecast (2033F) | US$ 2.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.8% |

| Historical Market Growth (2020 - 2025) | 5.7% |

Market Dynamics

Driver - Intensifying Quality Control Requirements Across Advanced Manufacturing Industries

The escalating complexity of engineered materials, spanning high-entropy alloys, next-generation superalloys, metal matrix composites, advanced ceramics, and multilayer semiconductor interconnects, is driving manufacturers across aerospace, automotive, energy, and electronics sectors to invest systematically in comprehensive metallographic machine workflows. In aerospace, compliance with AS9100 Rev D quality management and NADCAP materials testing accreditation programs mandates documented microstructural examination of safety-critical components. The automotive sector’s accelerating electrification trajectory generates new metallographic analysis demands for battery electrode cross-sections, copper busbar interconnects, and silicon carbide (SiC) power module packaging. According to the International Energy Agency (IEA), global EV sales exceeded 17 million units in 2023, with each vehicle platform incorporating dozens of metallurgically characterized material systems requiring ongoing quality verification and failure analysis support throughout the product lifecycle.

Expanding Public Research Infrastructure Investment Globally Driving Laboratory Equipment Procurement

Governments worldwide are making historically large investments in materials science and advanced manufacturing research infrastructure, directly generating demand for comprehensive metallographic laboratory equipment suites. The U.S. National Science Foundation (NSF) funds over US$ 1 billion annually in materials research through the Materials Research Science and Engineering Centers (MRSEC) program, supporting full metallographic preparation and characterization system procurement. Europe’s Horizon Europe framework (€95.5 billion, 2021-2027) designates advanced materials as a core research pillar. China’s 14th Five-Year Plan places advanced materials among the nation’s highest technology priorities, directing substantial state funding toward research laboratory upgrades that systematically include metallographic machine procurement as foundational equipment across universities and national research institutes.

Significant Capital Expenditure Requirements Creating Adoption Barriers for Smaller Laboratories

A primary restraint on the metallographic machine market growth is the substantial total cost of establishing or upgrading a fully equipped metallographic laboratory. When factoring in sectioning machines, mounting presses, automated grinding and polishing systems, hardness testers, high-resolution metallurgical microscopes, and image analysis software, the aggregate procurement cost for a comprehensive facility can exceed US$ 150,000-US$ 300,000 or more for research-grade configurations. According to the Organisation for Economic Co-operation and Development (OECD), capital expenditure constraints among small and medium-sized enterprises (SMEs) are a persistent structural challenge in industrial economies, directly moderating the pace at which smaller contract testing laboratories, independent foundries, and academic departments in resource-constrained institutions replace or expand metallographic equipment inventories.

Maintenance Complexity and Consumables Dependency Elevating Total Cost of Ownership

Beyond initial capital acquisition, the lifecycle economics of metallographic machines are meaningfully affected by recurring consumables costs, including abrasive sectioning wheels, mounting resins, grinding discs, polishing cloths, diamond suspensions, and calibration standards, representing significant ongoing operational expenditure. For high-throughput industrial laboratories processing hundreds of samples weekly, consumables budgets can approach or exceed annual equipment depreciation costs. The American Society for Metals (ASM International) has documented in its metallographic practice guides that consumable specification and procurement discipline is a substantial operational challenge for laboratory managers, particularly as automated grinding and polishing systems increase throughput and amplify consumables consumption rates. This total-cost-of-ownership complexity can deter procurement decisions among budget-constrained industrial customers and academic laboratories in developing economies.

Semiconductor Fab Investment Wave Creating Concentrated Near-Term Equipment Procurement Demand

The most immediately compelling growth opportunity for the Metallographic Machine market is the unprecedented wave of semiconductor fabrication facility construction funded through industrial policy programs. The U.S. CHIPS and Science Act (US$ 52 billion) has catalyzed over US$ 200 billion in total semiconductor facility investment announcements as of 2024, including new fabs from Intel, TSMC, Samsung, and Micron in Arizona, Ohio, Texas, and New York. The EU Chips Act (€43 billion) is driving analogous investments in Germany, Ireland, and France. Each new semiconductor facility requires a fully equipped failure analysis laboratory containing the complete metallographic machine workflow, sectioning, cold mounting, automated polishing, hardness testing, and high-resolution imaging, generating concentrated equipment procurement demand playing out across 2025-2030.

Additive Manufacturing Scale-Up Requiring New Metallographic Characterization Capabilities

The rapid industrial-scale adoption of additive manufacturing (AM) technologies, including selective laser melting (SLM), directed energy deposition (DED), electron beam melting (EBM), and binder jetting across aerospace, defense, medical, and energy sectors is creating substantial new demand for metallographic machines capable of characterizing AM-specific microstructural features. AM components exhibit complex, anisotropic grain structures, layer boundaries, and unique phase morphologies requiring the full metallographic characterization chain for regulatory qualification. The ASTM F42 Committee on Additive Manufacturing Technologies has published standards explicitly requiring microstructural characterization via standardized metallographic methods. The America Makes national AM institute and the European Powder Metallurgy Association (EPMA) actively promote metallographic best practice dissemination for AM quality systems, reinforcing the long-term structural demand generation this technology transition creates for metallographic machine manufacturers.

Category-wise Insights

By Machine Type

Grinding & polishing machines held the leading share in the machine type segment at approximately 28% in 2025, reflecting the central and highest-frequency role that grinding and polishing plays within the complete metallographic preparation workflow. Unlike sectioning or mounting, which are performed once per sample, grinding and polishing is a multi-stage process requiring sequential execution across coarse grinding, intermediate grinding, fine polishing, and final polishing steps, each demanding dedicated consumable media and machine time. Automated grinding and polishing systems from manufacturers including Struers, Buehler, and ATM GmbH are deployed in high-throughput industrial laboratories processing dozens to hundreds of samples per day. The ASTM E3 standard for metallographic specimen preparation explicitly defines grinding and polishing as the most technically critical preparation steps, directly influencing procurement priority in quality-certified industrial laboratories globally.

By Industry

The Metallurgy segment held the leading market share of approximately 26% in 2025, anchored by the universal and daily quality control role of metallographic machines across steel mills, foundries, non-ferrous metal producers, and specialty alloy manufacturers globally. Steel production, exceeding 1.8 billion tonnes annually per World Steel Association data, demands continuous metallographic monitoring of microstructure parameters including grain size, phase composition, inclusion ratings, and heat treatment response. Industry standards including ISO 643, ASTM E112 for grain size measurement, ASTM E45 for inclusion assessment, and ASTM E384 for microhardness testing are routinely executed on properly prepared metallographic specimens, creating codified, non-discretionary demand for the complete metallographic machine ecosystem across the global metallurgical manufacturing base.

Regional Insights

North America Metallographic Machine Market Trends and Insights

North America led the global Metallographic Machine market with a regional share of 32% in 2025, anchored by the United States’ combination of world-class materials research infrastructure, a highly regulated advanced manufacturing base, and the most concentrated ecosystem of metallographic instrument suppliers globally. The U.S. CHIPS and Science Act’s US$ 52 billion semiconductor manufacturing investment program is creating a structural wave of new laboratory equipment procurement as qualifying facilities build out failure analysis capabilities. The National Institute of Standards and Technology (NIST), Argonne National Laboratory, Oak Ridge National Laboratory, and Lawrence Berkeley National Laboratory maintain flagship metallographic characterization programs that influence procurement standards across the domestic industrial and academic community.

The U.S. market benefits from domestically headquartered global metallographic equipment leaders including Buehler (an Illinois Tool Works subsidiary based in Lake Bluff, Illinois) and LECO Corporation (St. Joseph, Michigan), which provide comprehensive machine portfolios reinforced by application engineering support and certified training through ASTM International and ASM International. Canada contributes demand through mining, primary metals processing, and aerospace manufacturing sectors, while Mexico’s expanding automotive manufacturing base is generating emerging demand for industrial-grade metallographic equipment tied to quality system compliance requirements.

Europe Metallographic Machine Market Trends and Insights

Europe held approximately 27% of the global Metallographic Machine market in 2025, supported by a deep tradition of precision instrument manufacturing and a highly developed materials research ecosystem. Germany is the dominant national market, home to world-class manufacturers including Volkswagen, BMW, Mercedes-Benz, Bosch, and ThyssenKrupp, all operating extensive metallographic quality control laboratories. Struers A/S, headquartered in Ballerup, Denmark, is the global market leader and maintains its primary R&D operations in Europe, reinforcing the region’s status as the world center of metallographic machine technology innovation.

The EU’s Horizon Europe program (€95.5 billion, 2021-2027) and EU Chips Act (€43 billion) are sustaining substantial equipment investment in academic and industrial R&D settings. France’s nuclear energy sector under EDF and aerospace industry centered on Airbus and Safran generate specialized demand for advanced metallographic systems. The United Kingdom’s National Physical Laboratory (NPL), Rolls-Royce materials R&D operations, and university research centers sustain meaningful equipment procurement volumes. Spain’s growing aerospace and renewable energy manufacturing base is emerging as an incremental demand contributor under EN 9100 and ISO 9001 quality certification frameworks.

Asia Pacific Metallographic Machine Market Trends and Insights

Asia Pacific is the fastest growing region in the Metallographic Machine market and is expected to register the highest CAGR through 2033, driven by the world’s largest steel and metals production base, the most rapidly expanding semiconductor manufacturing ecosystem, and government-led manufacturing upgrade programs. China dominates regional demand, operating the world’s largest steel industry at approximately 1.0 billion tonnes of annual production per World Steel Association, alongside a rapidly expanding semiconductor sector receiving state investment under the 14th Five-Year Plan. Domestic manufacturers including Laizhou Weiyi, Shanghai Minxin, and WHW are gaining domestic market share while international brands including Struers and Buehler maintain premium positions in high-precision applications.

Japan maintains a technically sophisticated metallographic machine market governed by JIS standards, with demand from precision manufacturing industries spanning automotive components, specialty steel, and advanced ceramics. India’s steel industry, now the world’s second-largest at over 140 million tonnes per the World Steel Association, combined with expanding aerospace and semiconductor manufacturing under the Production Linked Incentive (PLI) scheme, is driving new laboratory infrastructure investment. South Korea and Taiwan generate concentrated demand from world-leading semiconductor and display panel manufacturing sectors where metallographic failure analysis is critical for advanced node process development. ASEAN markets including Vietnam, Thailand, and Malaysia are emerging as secondary demand contributors as manufacturing investment diversification accelerates.

Competitive Landscape

The global metallographic machine market displays a moderately consolidated structure in the premium segment, where a small group of established manufacturers supply advanced laboratory systems to industrial testing facilities, research institutions, and semiconductor laboratories. At the same time, the broader market remains fragmented due to the presence of numerous regional suppliers offering cost-competitive equipment for routine metallographic preparation and analysis applications.

Competition is largely shaped by technological capability, reliability, and the ability to provide integrated laboratory solutions covering cutting, mounting, grinding, polishing, and imaging processes. Leading manufacturers focus on expanding digital capabilities such as automated sample preparation, AI-assisted image analysis, and IoT-enabled laboratory monitoring systems. At the same time, companies are investing in sustainable equipment designs that reduce chemical usage, water consumption, and energy requirements. Regional players continue to compete aggressively on pricing in emerging markets, encouraging premium suppliers to differentiate through high-precision instrumentation, strong application support, and global service networks.

Key Developments:

- May 2025: TESCAN announced an AI-driven failure analysis advancement for semiconductor advanced packaging, integrating automated microscopy and analytics to accelerate defect detection and improve reliability assessment for increasingly complex chip packaging architectures.

- September 2024: LECO Corporation launched the CX300 Series metallographic sectioning machines, a compact line offering manual to fully automated cutting capabilities designed to improve laboratory efficiency, safety, and precision in metallographic sample preparation workflows.

Companies Covered in Metallographic Machine Market

- Struers A/S

- Buehler (Illinois Tool Works)

- LECO Corporation

- PRESI

- Allied High Tech Products

- Laizhou Weiyi Experimental Instrument Co., Ltd.

- ATM GmbH

- Plusover

- BROT LAB

- Shanghai Minxin Precision Instruments

- WHW (Wuhan Huawei Technology)

- Metkon Instruments Inc.

- Kemet International Limited

- NextGen Material Testing, Inc.

- PACE Technologies Corporation

- QATM GmbH

- Qualitek International

- Extec Corp.

- Carl Zeiss AG

- Olympus Corporation (EVIDENT)

Frequently Asked Questions

The global Metallographic Machine market is estimated to reach US$ 1.3 billion in 2026, supported by growing demand from advanced manufacturing, semiconductor fabrication, and materials research laboratories.

Demand is driven by stricter quality control requirements in aerospace, automotive, semiconductor, and medical device manufacturing, along with increasing investment in materials research infrastructure.

North America leads the market due to its strong materials science research ecosystem, semiconductor fabrication investments, and advanced manufacturing base.

Key opportunities include expanding semiconductor fabrication facilities and increasing the adoption of metallographic testing in additive manufacturing quality assurance.

Key companies include Struers, Buehler, LECO Corporation, PRESI, Metkon Instruments, Allied High Tech Products, Carl Zeiss AG, Olympus (Evident), and QATM GmbH.