- IT and Telecommunication

- Industry 4.0 Market

Industry 4.0 Market Size, Share, and Growth Forecast 2026 – 2033

Industry 4.0 Market by Component (Hardware, Software, Services), Technology (IIoT, Robotics and Automation, AI and ML), Industry Vertical (Manufacturing, Petrochemicals, Automotive), and Regional Analysis, 2026 – 2033

Industry 4.0 Market Size and Trends Analysis

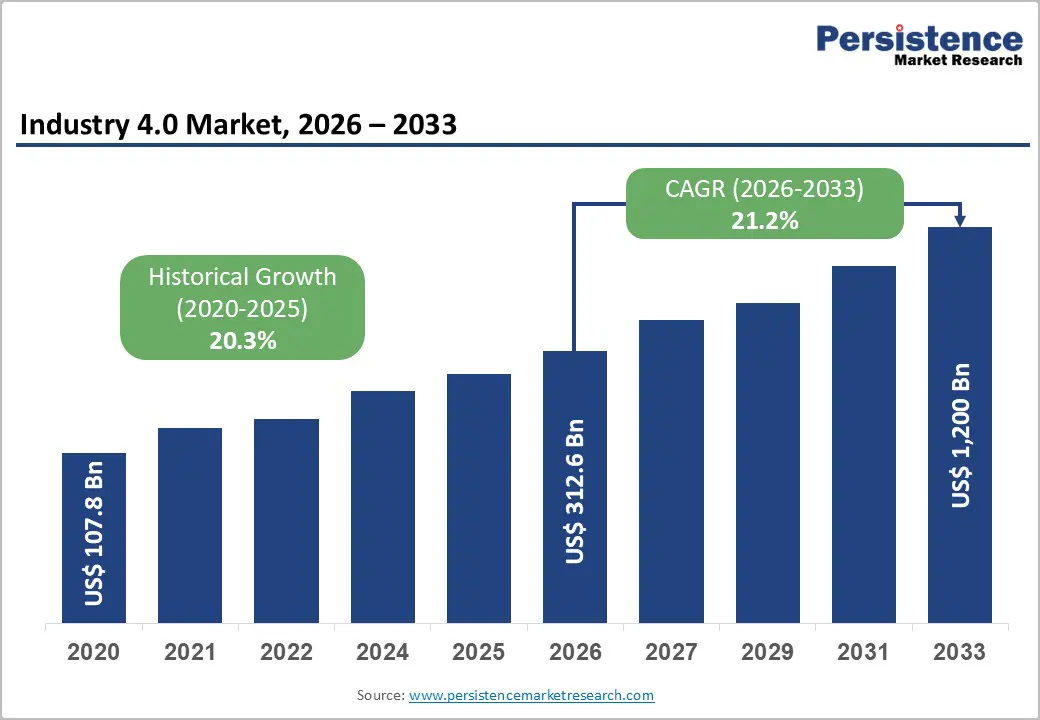

The global Industry 4.0 market size is likely to be valued at US$312.6 billion in 2026 and is expected to reach US$1,200 billion by 2033, growing at a CAGR of 21.2% during the forecast period from 2026 to 2033, driven by the ongoing adoption of industrial automation and smart manufacturing practices across the key sectors. Increasing use of AI, machine learning, and digital twins is enabling real-time decision-making and predictive maintenance in factories. Government support through smart manufacturing programs is also projected to boost the market.

Key Industry Highlights:

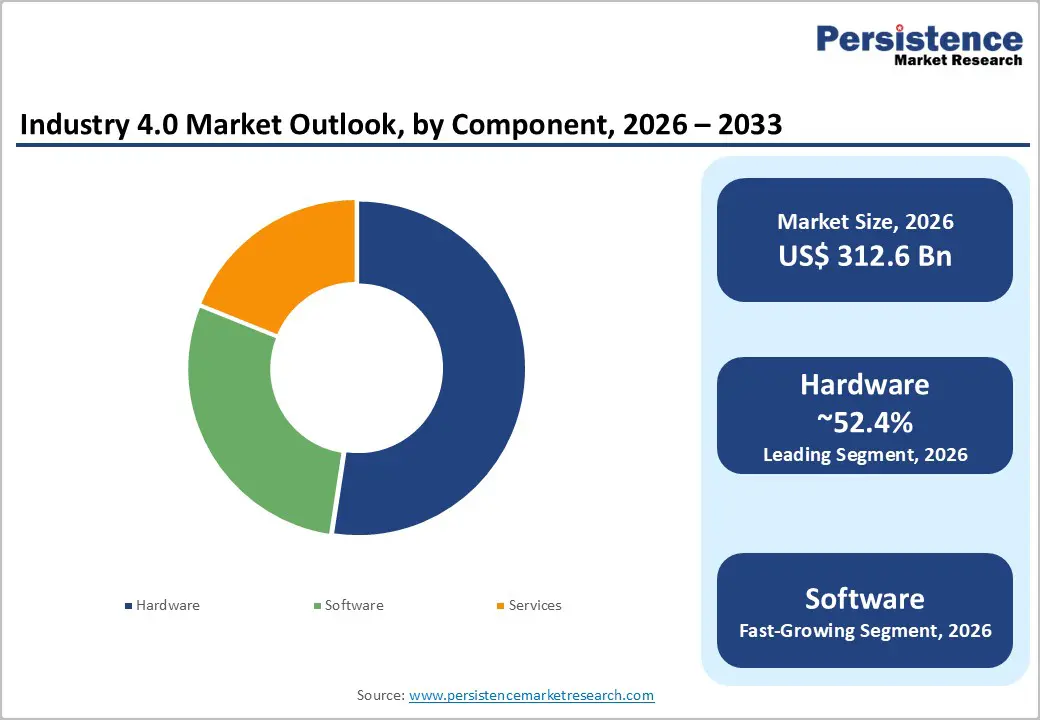

- Leading Component: Hardware, approximately 52.4% share in 2026, as manufacturers invest heavily in upgrading legacy production equipment with connected automation systems.

- Dominant Technology: Industrial Internet of Things (IIoT), with a nearly 29.6% share in 2026, as it serves as the foundation of Industry 4.0.

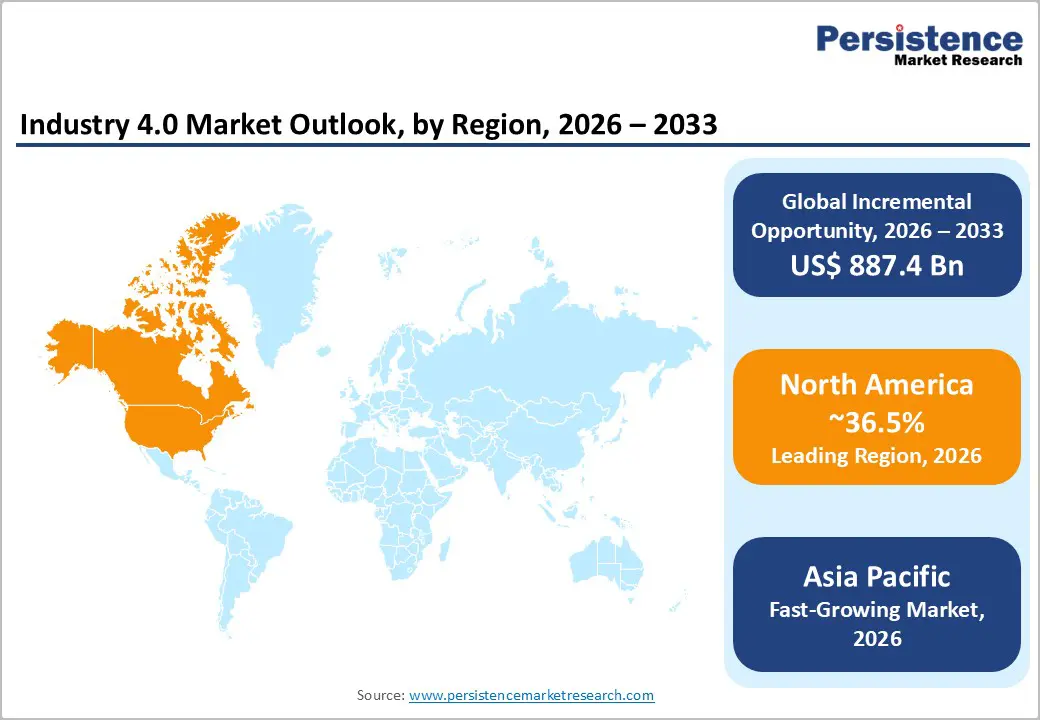

- Leading Region: North America, with about a 36.5% share in 2026, due to its early adoption of industrial automation.

- Fast-growing Region: Asia Pacific, fostered by modernization of factories through government-backed digitalization and automation programs.

- Latest Spin-Off: In April 2025, ABB announced plans to spin off its robotics division into an independent company by the second quarter of 2026. The firm stated that this move would allow both businesses to sharpen their focus on automation, robotics, and electrification opportunities while improving operational agility.

DRO Analysis

Driver - Policy Push and Cross-Sector Collaborations

Coordinated policy action is one of the key catalysts for Industry 4.0 adoption. Germany's Manufacturing-X program, backed by €140 million (nearly US$162.5 million) in federal funding, launched its first projects in early 2024 and runs through 2026, building a decentralized data network for Industry 4.0. At the EU level, the Made in Europe Partnership is co-funding Factory 4.0-focused projects such as RE4DY.

It creates data hubs for resilient and data-backed manufacturing environments with tools for improved production continuity and sustainable decision-making. These are not standalone grants. They require industry, academia, and government to collaborate under shared frameworks. This multi-stakeholder design ensures that technologies developed in research settings are tested and expanded across real production environments, fueling time to deployment across member states.

Rising Demand for Industrial and Human-Collaborative Robotics

The shift toward flexible and human-compatible automation is changing factory floors globally. According to the International Federation of Robotics’ (IFR) updated position paper (December 2024), cobots reached a market share of 10.5% of all industrial robots installed worldwide in 2023. The deployment numbers are skyrocketing. In 2024, companies deployed a record 64,542 collaborative robots globally, a 12% increase from the previous year.

Unlike traditional caged robots, cobots use force-torque sensing and vision systems to work alongside workers, making them accessible to small-scale manufacturers. The IFR's 2023 report noted a remarkable 50% growth in cobot installations across industrial applications. As Industry 4.0 frameworks prioritize adaptive and reconfigurable production lines, cobots have become the most practical entry point for manufacturers that cannot yet commit to full-scale automation.

Restraint - Unclear Returns May Discourage Tier-2 and Tier-3 Supplier Adoption

For small-scale suppliers deeper in the value chain, the financial case for Industry 4.0 investment remains difficult to prove. Industrial IoT, robotics, AI, and cyber-physical systems require significant capital expenditure on hardware, software, infrastructure, and training, something several SMEs cannot afford, especially when ROI is not obvious or immediate. This problem is compounded by the absence of standardized measurement tools.

A lack of a standardized framework for assessing digital transformation ROI in SMEs hinders the ability to provide precise quantitative analyses of its impact. Integration further complicates decisions. Barriers such as financial challenges, lack of management support, absence of regulatory clarity, and insufficient workforce skills remain among the most significant obstacles to adoption in manufacturing supply chains. Until OEMs or industry bodies establish transparent benchmarks for measuring returns at the supplier tier, hesitation is predicted to persist among manufacturers operating on thin margins.

Opportunity - Green Manufacturing Incentives to Push Low-Carbon Factories

Regulatory pressure to cut emissions is turning energy optimization into a competitive advantage for smart factories. Siemens cut its CO2 emissions by 60% since 2019, exceeding its 2025 target a year early, while Schneider Electric helped customers avoid 679 million tons of CO2, both through digital manufacturing systems. Research published in Humanities and Social Sciences Communications (2024) examined 144 China-based manufacturers and found that the country has prioritized smart factories in key policies, including Made in China 2025 and the 14th Five-Year Intelligent Manufacturing Development Plan.

It is directly linking industrial digitalization to carbon reduction goals. As carbon border taxes become enforceable, particularly in the EU, manufacturers that invest in self-optimizing, AI-backed energy systems stand to gain both a compliance edge and cost savings. This creates a commercial incentive that extends beyond sustainability goals.

Private 5G and Edge Networks to Provide Real-Time Factory Control

Reliable and low-latency connectivity is becoming the backbone of advanced manufacturing. Standalone private 5G networks are well-positioned to become the predominant wireless connectivity medium for Industry 4.0 applications in manufacturing and process industries. The numbers reflect this shift. Edge AI is cutting inference latency from over 100ms to under 15ms, and 50% of enterprises are anticipated to adopt edge computing by 2025, up from 20% in 2024.

Real deployments are already underway. NTT Data is rolling out a private 5G network across Hyster-Yale Group's manufacturing operations, integrating asset tracking, materials visibility, and real-time communication across production lines. As more manufacturers require millisecond-level decision-making for robotics and quality control, private 5G and edge computing together remove the cloud dependency that previously limited real-time automation on a large scale.

Category-wise Analysis

Component Insights

Hardware is predicted to lead with a share of approximately 52.4% in 2026, as it forms the physical backbone of Industry 4.0 systems. Factories still depend on machines, sensors, Programmable Logic Controllers (PLCs), robotics, and edge devices to collect and transmit data. Without these, digital systems cannot function. Governments continue to invest heavily in smart manufacturing infrastructure, which boosts hardware demand. For example, Germany’s Industrie 4.0 program, supported by the Federal Ministry for Economic Affairs and Climate Action, has funded large-scale deployment of smart sensors and cyber-physical systems in manufacturing plants.

Software is estimated to be the fastest-growing segment over the forecast period, as it converts raw machine data into actionable insights. Industry 4.0 is not just about collecting data; it is about using it for decisions. Software platforms enable predictive maintenance, digital twins, and real-time analytics. These tools help reduce downtime and improve efficiency. For instance, Siemens uses its Xcelerator platform to create digital twins of factories, allowing companies to simulate production before actual deployment.

Technology Insights

The Industrial Internet of Things (IIoT) segment is anticipated to dominate with a share of nearly 29.6% in 2026, as it connects all parts of the manufacturing network. IIoT enables machines, sensors, and systems to communicate in real time. This connectivity is essential for automation and data-driven decisions. Governments and industry bodies strongly promote IIoT adoption. For example, India’s Smart Advanced Manufacturing and Rapid Transformation Hub (SAMARTH Udyog), supported by the Ministry of Heavy Industries, focuses on IIoT-enabled smart factories.

The blockchain and secure data exchange segment is expected to remain in the second position in 2026, as trust and data integrity are becoming important in connected factories. As more devices and partners share data, the risk of tampering and cyberattacks increases. Blockchain helps create secure, tamper-proof records of transactions and machine data. This is especially useful in supply chains and multi-vendor environments. For example, the European Commission has supported blockchain-based industrial data sharing projects under its digital innovation programs. In 2024, IBM and Maersk continued broadening blockchain-based supply chain platforms to improve transparency and traceability.

Regional Insights

North America Industry 4.0 Market Trends

North America is predicted to dominate in 2026 with a share of approximately 36.5%, as it blends a superior industrial base with advanced digital capabilities. The region has early adoption of automation, AI, and cloud technologies. Companies invest heavily in smart factories and digital twins. Government-backed programs also support this shift. For example, the National Institute of Standards and Technology leads smart manufacturing frameworks and cybersecurity standards for connected factories. Firms, including General Electric and Rockwell Automation, actively deploy IIoT platforms across industries. North America also benefits from a well-established cloud infrastructure led by Microsoft and Amazon Web Services, which allows quick expansion of Industry 4.0 solutions.

U.S. Industry 4.0 Market Trends

A share of nearly 68.4% is expected to be held by the U.S. in 2026, owing to policy support and reshoring of manufacturing. The U.S. government is pushing domestic production through laws such as the CHIPS and Science Act. This has triggered new semiconductor and advanced manufacturing plants. According to official releases from the U.S. Department of Commerce, billions of dollars are being invested in smart fabs that rely on AI and automation. Companies such as Intel are building new facilities with fully automated production lines. The adoption of AI-backed predictive maintenance is further rising across sectors such as aerospace and energy, which keeps demand for Industry 4.0 solutions consistent.

Asia Pacific Industry 4.0 Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026 with a share of nearly 29.4%, backed by swift industrialization and government-led digitization. Countries in this region are upgrading factories to remain globally competitive. Governments are actively funding smart manufacturing. For instance, China’s Made in China 2025 policy focuses on robotics, automation, and smart equipment. Similarly, Japan and South Korea are investing in AI-based production systems. A report from the International Federation of Robotics shows that Asia accounts for the majority of global industrial robot installations, with China alone contributing a large share. This push toward automation is boosting speedy Industry 4.0 adoption.

China Industry 4.0 Market Trends

China will likely lead Asia Pacific in 2026 with a share of around 42.2%, spurred by large-scale automation and domestic technology development. The country is focusing on reducing reliance on foreign technology. It is investing in local robotics, chips, and industrial software. The government continues to support smart factories through subsidies and pilot projects. For example, the Ministry of Industry and Information Technology has identified hundreds of smart manufacturing demonstration factories. Companies such as Huawei are providing industrial cloud and IIoT platforms for factories.

India Industry 4.0 Market Trends

In 2026, India is projected to account for a share of approximately 12.7%. The country is focusing on digital manufacturing through initiatives such as SAMARTH Udyog and Make in India. These programs aim to upgrade MSMEs with smart technologies. The Ministry of Heavy Industries has set up smart manufacturing demo centers to train industries. Companies such as Tata Motors and Mahindra & Mahindra are adopting robotics and IoT in production lines. However, challenges such as skill gaps and infrastructure issues still limit speedy adoption. Growth is visible, but it is not yet at the level of China or the U.S.

Europe Industry 4.0 Market Trends

Europe will likely see decent growth in the forecast period, with a share of nearly 18.1% in 2026, backed by superior industrial heritage and a structured digital transition. Several countries focus on precision manufacturing and sustainability. The region follows a planned approach through policies and standards. The European Commission supports Industry 4.0 through programs such as Horizon Europe and Digital Europe. Companies are also adopting energy-efficient automation and circular manufacturing models. Firms such as Siemens and Schneider Electric lead innovation in smart factories. This structured approach ensures stable and long-term growth.

Germany Industry 4.0 Market Trends

Germany will likely register a substantial share of approximately 40.1% in 2026, fueled by its leadership in advanced manufacturing. The country is the origin of the Industry 4.0 concept. It has strong integration of automation, engineering, and digital tools. The Federal Ministry for Economic Affairs and Climate Action continues to fund smart factory projects and industrial AI research. Local manufacturers such as BMW and Bosch use digital twins and connected production systems. Several factories in Germany now operate with high levels of automation and real-time data exchange. This keeps it at the center of Europe’s Industry 4.0 growth.

U.K. Industry 4.0 Market Trends

A share of around 26.3% is predicted to be held by the U.K. in 2026, backed by innovation and digital strategy. The country focuses on advanced manufacturing and digital innovation rather than large-scale production. Programs such as Made Smarter, backed by the U.K. Government, support SMEs in adopting digital tools. This initiative has helped thousands of manufacturers adopt robotics and data analytics. Companies are also using AI and digital twins in the aerospace and automotive sectors. Research institutions and universities play a key role in innovation. While growth is slower compared to Asia Pacific, the U.K. is building a well-established network for future expansion.

Competitive Landscape

The global Industry 4.0 market is moderately fragmented, with no single company holding a dominant share. Key automation and digitalization vendors such as Siemens, Schneider Electric, ABB, Rockwell Automation, Honeywell, Emerson Electric, and Microsoft lead the market. However, the top players collectively account for only a limited portion of total industry revenue.

Competition is increasingly shifting from standalone automation hardware to integrated digital networks. Leading vendors are building end-to-end platforms that combine industrial IoT, AI, digital twins, edge computing, cloud analytics, and cybersecurity. Strategic partnerships and acquisitions have also become a prominent competitive tool. Another defining feature of the competitive landscape is the convergence of Operational Technology (OT) and Information Technology (IT).

Key Industry Developments:

- In May 2026, Lattice Semiconductor announced a definitive agreement to acquire AMI from THL Partners. The companies noted that the transaction would create a more comprehensive, secure management and control platform for AI, cloud, and industrial infrastructure applications, supporting increasingly connected Industry 4.0 environments.

- In May 2026, SAP announced an agreement to acquire Dremio. The companies stated that combining Dremio’s open data lakehouse platform with SAP Business Data Cloud would help manufacturers and industrial enterprises unify SAP and non-SAP data, enabling more effective real-time analytics and agentic AI workloads.

- In February 2026, Siemens acquired Canopus AI to improve AI-based metrology and inspection capabilities for semiconductor manufacturing. Siemens noted that the acquisition would extend its semiconductor digital thread and improve precision in wafer manufacturing through advanced AI and machine-learning technologies.

Companies Covered in Industry 4.0 Market

- ABB LTD.

- Cisco Systems Inc.

- Cognex Corporation

- Denso Corporation

- Emerson Electric

- Fanuc Corporation

- General Electric Company

- Honeywell International Inc.

- Intel Corporation

- Johnson Controls International

- Kuka Group

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Others

Frequently Asked Questions

The global Industry 4.0 market is projected to be valued at US$312.6 billion in 2026.

The Industry 4.0 market is expected to reach US$1,200 billion by 2033.

Key market trends include the rising adoption of industrial AI and the launch of sustainability-focused smart manufacturing solutions.

Hardware is expected to be the leading component with a share of nearly 52.4% in 2026, as smart factories require large-scale deployment of sensors, industrial robots, and PLCs.

The Industry 4.0 market is expected to grow at a CAGR of 21.2% from 2026 to 2033.

ABB LTD., Cisco Systems Inc., and Cognex Corporation are a few key market players.