- Pharmaceuticals

- Hyponatremia Treatment Market

Hyponatremia Treatment Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Hyponatremia Treatment Market by Treatment Type (Intravenous (IV) Fluids, Medications, Others), End-User (Hospitals, Clinics, Homecare Settings, Others), Route of Administration (Oral, Parenteral, Subcutaneous), and Regional Analysis for 2026-2033

Hyponatremia Treatment Market Share and Trends Analysis

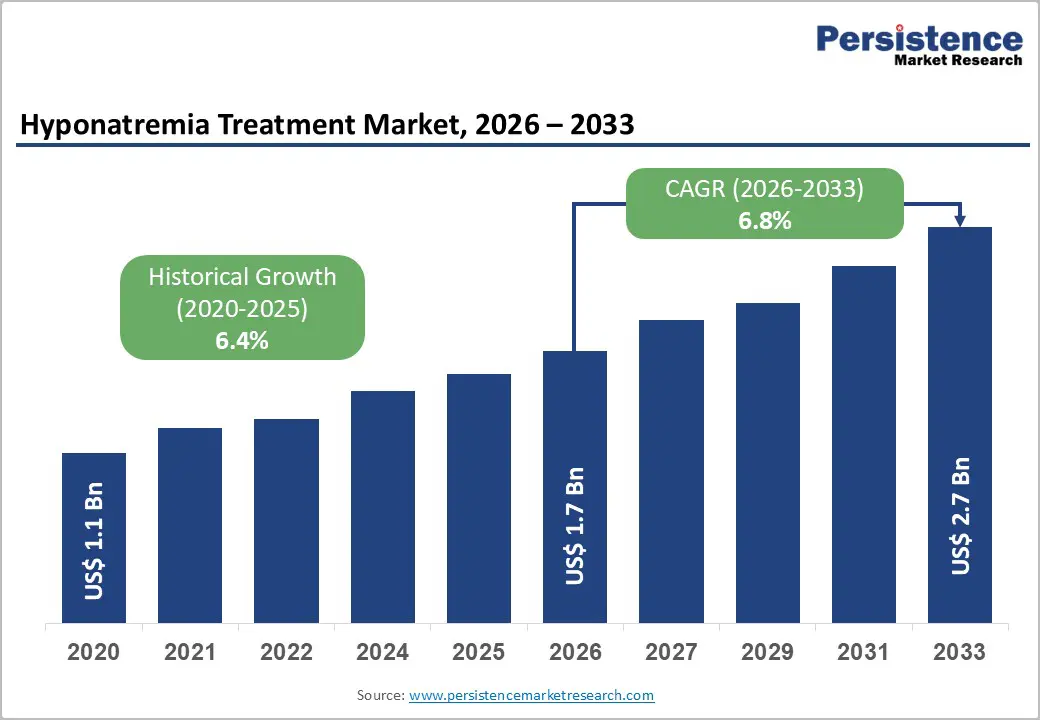

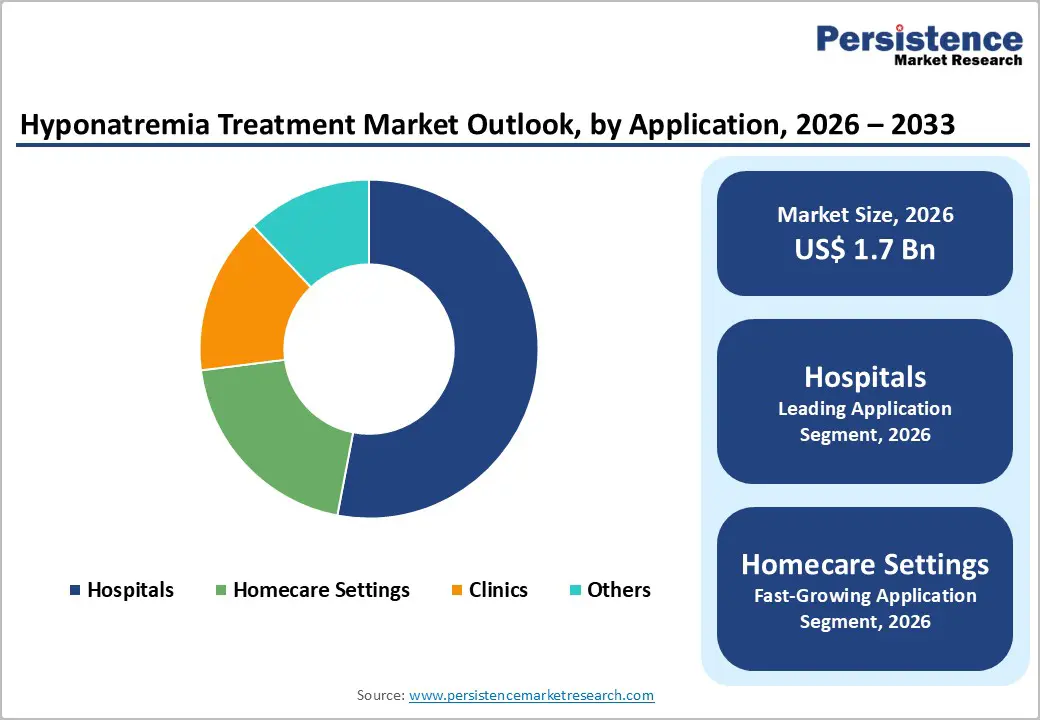

The global hyponatremia treatment market size is likely to be valued at US$ 1.7 billion in 2026, and is projected to reach US$ 2.7 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026−2033.

The rising incidence of chronic conditions such as heart failure, liver cirrhosis, and kidney disorders, all of which commonly contribute to the development of hyponatremia. The expanding elderly population further amplifies this trend, as older individuals are more vulnerable to such health issues. Increased hospitalization rates, particularly for surgical procedures, also play a role, since hyponatremia can emerge as a postoperative complication. Together, these factors are steadily boosting the need for effective treatment solutions and supporting overall market expansion.

Key Industry Highlights

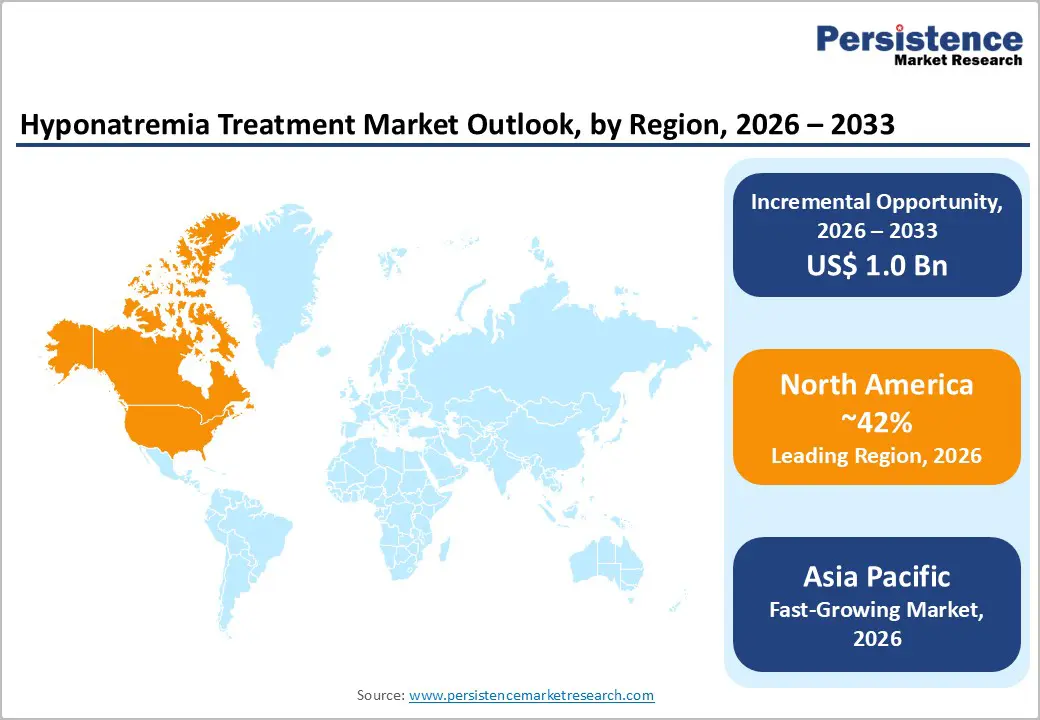

- Dominant Region: North America is expected to command about 42% market share in 2026, supported by well-established healthcare infrastructure, high healthcare expenditure.

- Fastest-growing Region: The Asia Pacific market is slated to be the fastest-growing through 2033, fueled by the increasing healthcare investments and improving healthcare infrastructure.

- Dominant & Fastest-growing Treatment Type: Medication is poised to dominate with approximately 48% market revenue share in 2026, with intravenous (IV) fluids likely to grow the fastest during the 2026-2033 forecast period.

- Leading & Fastest-growing End-User: Hospitals are poised to represent the leading end-user segment, capturing approximately 53% revenue share in 2026, while homecare settings are expected to be the fastest-growing over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

| Hyponatremia Treatment Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 2.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

DRO Analysis

Rising Prevalence of Hyponatremia Across Aging Populations

Hyponatremia, defined as a low concentration of sodium in the blood, is emerging as one of the most commonly managed electrolyte disorders in clinical practice. It is increasingly affecting patients across diverse care settings, particularly those with underlying conditions such as cardiovascular disorders, renal impairment, and endocrine imbalances. Healthcare providers are recognizing its clinical significance due to its association with neurological complications, reduced functional capacity, and higher risk of morbidity. The condition is frequently being identified during routine diagnostics, and clinicians are prioritizing timely intervention to prevent deterioration. Treatment protocols are evolving with a focus on controlled sodium correction and patient-specific management approaches, which is strengthening the adoption of targeted therapies.

A notable demographic transition is reshaping the treatment landscape, as the global elderly population is expanding and is becoming more susceptible to electrolyte imbalances. This shift is driving higher hospital admissions and prolonged patient monitoring, particularly in acute and post-operative care environments. Medical systems are responding by integrating advanced diagnostic tools and optimized fluid management strategies to improve outcomes. Pharmaceutical and biotechnology companies are developing novel osmotic agents and vasopressin receptor antagonists, which are enhancing treatment precision and safety. Demand for effective therapies is expected to remain strong, as healthcare infrastructure is continuing to adapt to the growing burden of chronic and age-related conditions.

Expanding Regulatory Approvals and Pipeline Development

Regulatory progress is shaping the pharmacological pipeline for hyponatremia treatment, as authorities are continuing to approve and evaluate targeted therapies. The United States Food and Drug Administration (FDA) is having established a strong base with approvals of vasopressin receptor antagonists such as tolvaptan and conivaptan, which are improving sodium balance through precise mechanisms. These approvals are guiding current research directions and encouraging companies to focus on safer and more effective correction strategies. Pharmaceutical developers are actively submitting Investigational New Drug (IND) applications and New Drug Applications (NDA), which are undergoing structured review under Prescription Drug User Fee Act (PDUFA) timelines. This process is ensuring faster assessment while maintaining safety standards, and it is supporting a steady flow of innovative candidates entering late-stage development.

Across international markets, regulatory alignment is playing a crucial role in expanding access to new therapies. The European Medicines Agency (EMA) is streamlining approvals through its centralized procedure, which is allowing companies to enter multiple countries with a single authorization. This approach is reducing administrative delays and is helping manufacturers scale commercialization efforts more efficiently. Shorter approval cycles are enabling quicker product launches, and companies are strengthening their market positioning through early entry strategies. Investors are responding positively, as the pipeline is becoming more predictable and commercially viable, which is driving sustained interest and competitive advancement within the sector.

Potential Side Effects and Complications Associated with Treatments

Vasopressin receptor antagonists are playing an important role in correcting sodium imbalance, yet their safety profile is requiring close clinical attention. These agents are influencing water excretion without significant electrolyte loss, which is making them effective in targeted therapy. Despite this benefit, concerns around liver toxicity are limiting broader adoption. Healthcare professionals are carefully evaluating liver function before initiating treatment and are continuing to monitor patients throughout therapy. This cautious approach is helping reduce adverse outcomes while maintaining therapeutic effectiveness. Clinical guidelines are increasingly emphasizing patient selection criteria, which is ensuring that only suitable individuals are receiving these medications under controlled conditions.

Ongoing research is focusing on improving the safety and tolerability of these therapies, as developers are working to minimize hepatic risks while preserving efficacy. Pharmaceutical companies are exploring modified formulations and alternative mechanisms of action, which are expected to enhance treatment outcomes over time. Physicians are also considering combination strategies and dose adjustments to balance safety with clinical benefits. Regulatory authorities are maintaining strict oversight, which is encouraging transparent reporting of adverse events and long-term effects. This evolving landscape is shaping more refined treatment pathways, where risk management is becoming a central component of therapeutic decision-making in hyponatremia care.

Generic Competition and Pricing Pressure

Branded drugs are facing growing competition from generic alternatives, particularly for vasopressin receptor antagonists such as tolvaptan and conivaptan. This shift is compelling originator companies to reposition their offerings by focusing on clinical value, treatment outcomes, and patient support programs rather than relying on patent protection. Generic manufacturers are expanding their presence by offering cost-effective options, which is increasing accessibility while simultaneously driving down price levels. Competition intensifies, average selling prices are declining, and companies are adjusting their strategies to maintain market relevance while managing reduced margins per unit.

Procurement practices within healthcare systems are further amplifying these pricing pressures, especially in publicly funded environments. Government-led purchasing frameworks are prioritizing cost efficiency, which is favoring suppliers that can meet large-scale demand at lower prices. Hospital networks are increasingly adopting tender-based models, where contracts are awarded based on competitive bidding processes. This environment is placing additional strain on branded manufacturers, as they are striving to justify premium pricing through differentiation and innovation. Companies are responding by optimizing production costs and strengthening distribution efficiency, while also exploring value-based agreements that align pricing with therapeutic outcomes in clinical settings.

Development of Novel Therapeutic Agents and Advanced Formulations

The development of novel therapeutic agents is creating a strong growth pathway within the hyponatremia treatment landscape. Pharmaceutical companies are increasing their focus on research and development (R&D) to identify drug candidates that are delivering improved efficacy while reducing adverse effects. Scientists are exploring targeted mechanisms that regulate water balance and sodium levels with greater precision, which is enhancing clinical outcomes. Advanced drug design is supporting better pharmacokinetics and patient compliance, especially in long-term management scenarios. Companies are also prioritizing differentiated formulations that are addressing unmet medical needs across diverse patient groups, which is strengthening their competitive positioning in evolving healthcare environments.

Innovation is extending beyond conventional therapies, as next-generation intravenous solutions and refined delivery systems are entering development pipelines. These approaches are improving the speed and control of sodium correction, particularly in acute care settings where rapid intervention is critical. Healthcare providers are increasingly adopting therapies that are offering predictable responses and reduced monitoring burden. Strategic collaborations between pharmaceutical firms and research institutions are accelerating product development timelines and expanding technological capabilities. This momentum is expected to enhance treatment standards, while companies are positioning themselves to capture emerging opportunities through continuous innovation and value-driven therapeutic advancements.

Label Expansion and Off-Label Clinical Use

Clinical research is increasingly focusing on expanding the therapeutic scope of vasopressin receptor antagonists, commonly known as vaptans. These drugs are being evaluated for broader applications such as pediatric care, specific forms of heart failure, and hyponatremia following surgical procedures. Researchers are conducting advanced clinical trials to determine safety and effectiveness across these patient groups, while healthcare providers are anticipating more flexible treatment options. Regulatory pathways are supporting this approach, as companies are pursuing supplemental approvals based on existing clinical data. This strategy is reducing development complexity, since manufacturers are building on already approved molecular frameworks rather than creating entirely new compounds.

Label expansion is emerging as a practical and cost-efficient route for growth within the pharmaceutical sector. Companies are leveraging established manufacturing systems, distribution channels, and regulatory familiarity to accelerate market entry for new indications. This approach is strengthening return on investment, as fewer resources are required compared to developing new drugs from early stages. Physicians are expected to adopt these expanded uses as clinical evidence is becoming more robust and widely accepted. Market participants are positioning themselves to capture additional value through lifecycle management strategies, while ongoing research is continuing to refine treatment protocols and improve patient outcomes across a broader clinical spectrum.

Category-wise Analysis

Treatment Type Insights

Medication is expected to command approximately 48% of the hyponatremia treatment market revenue share in 2026, driven by ongoing advancements in targeted drug therapies. Pharmaceutical companies are developing improved formulations such as vasopressin receptor antagonists that are offering precise regulation of sodium levels. These treatments are gaining traction due to their ability to address underlying causes rather than providing temporary correction. Physicians are increasingly prescribing these drugs for long-term management, particularly in patients with chronic conditions. R&D efforts are accelerating innovation, while regulatory support is enabling quicker approvals, which is expanding access and driving sustained growth in this segment.

Intravenous Fluids are likely to be the fastest-growing segment during the 2026-2033 forecast period. Hospitals are relying on these solutions to stabilize patients quickly, especially in emergency and post-surgical scenarios where rapid intervention is critical. Their ease of administration and predictable response are supporting consistent clinical use. Healthcare systems are continuing to prioritize intravenous therapy due to its effectiveness in controlled environments. Standard treatment protocols are reinforcing their dominance, as physicians are preferring established approaches that deliver reliable and measurable outcomes in both inpatient and critical care situations.

End-User Insights

Hospitals are likely to be the dominant end-users, capturing roughly 53% of the hyponatremia treatment market share in 2026. A major factor supporting this dominance is the widespread occurrence of hyponatremia among patients receiving hospital care. Clinical conditions such as heart failure, liver cirrhosis, and post-surgical complications are frequently observed in inpatient settings and are contributing to electrolyte imbalances. Medical teams are actively monitoring sodium levels as part of routine care, which is increasing early detection and timely intervention. Hospitals are continuously managing complex cases where fluid imbalance is common, which is strengthening the need for reliable treatment options. This environment is driving consistent demand for effective therapies, as providers are prioritizing rapid stabilization and improved patient outcomes.

Homecare settings are expected to be the fastest-growing segment over the 2026-2033 forecast period. Healthcare systems are shifting toward decentralized and patient-centric care models. Patients are increasingly receiving treatment and monitoring in home environments, supported by portable medical devices and telehealth services. This approach is improving convenience while reducing the burden on hospitals. Care providers are offering customized treatment plans that allow ongoing management of mild to moderate cases outside clinical facilities. Technological advancements are enabling remote monitoring of electrolyte levels, which is supporting timely interventions and driving the expansion of home-based hyponatremia care solutions.

Regional Insights

North America Hyponatremia Treatment Market Trends

North America is set to command a significant portion of the hyponatremia treatment market value at approximately 42% in 2026, with the United States leading regional performance. The country is benefiting from a well-structured regulatory environment governed by the U.S. FDA, which is ensuring timely approvals and strong compliance standards. A highly developed private insurance system is supporting access to advanced therapies, while an extensive hospital network is enabling efficient diagnosis and treatment. Clinical organizations such as the American Society of Nephrology and the Endocrine Society are establishing standardized guidelines, which are improving treatment consistency and supporting physician decision-making across healthcare settings.

Healthcare demand in the region is rising due to increasing cases of chronic conditions such as cardiovascular and liver disorders, which are contributing to electrolyte imbalances. An expanding elderly population is requiring continuous medical attention, which is strengthening treatment adoption. The market is also benefiting from high pharmaceutical spending, which is enabling the use of advanced drug therapies. Canada is contributing through its publicly funded healthcare system, where procurement strategies are emphasizing cost efficiency and accessibility. Major companies such as Otsuka Pharmaceutical and Teva Pharmaceutical Industries are maintaining a strong presence, which is supporting innovation and competitive development across the region.

Europe Hyponatremia Treatment Market Trends

Europe is holding a strong position as the second-largest regional market for hyponatremia treatment, with key contributions from Germany, United Kingdom, France, and Spain. The region is benefiting from the centralized approval framework of the European Medicines Agency, which is enabling pharmaceutical companies to access multiple markets through a single authorization process. This system is reducing administrative complexity and accelerating product availability. Germany is leading adoption due to its advanced hospital infrastructure and strong clinical workforce, while policy guidance from the National Institute for Health and Care Excellence is shaping treatment access decisions in the United Kingdom through structured evaluation of clinical and economic value.

Market dynamics across Europe are evolving under a framework of regulatory coordination and cost control measures. Post-Brexit adjustments are influencing trade and approval pathways in the United Kingdom, although ongoing agreements are maintaining supply continuity. France and Spain are experiencing increasing demand as aging populations are requiring more specialized care, and healthcare systems are strengthening nephrology services. Health Technology Assessment (HTA) bodies are actively evaluating pricing and reimbursement, which is ensuring that therapies deliver measurable value. This environment is supporting stable treatment volumes, while collaborative clinical research efforts are generating real-world evidence that is improving reimbursement decisions and expanding patient access.

Asia Pacific Hyponatremia Treatment Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing hyponatremia treatment market. supported by rapid healthcare expansion and policy-driven reforms. China is leading regional growth, as government initiatives such as Healthy China 2030 are strengthening hospital infrastructure and improving access to nephrology services. Japan is contributing a stable and high-value market, where physicians are actively adopting advanced therapies and managing a large elderly population with higher susceptibility to electrolyte disorders. Meanwhile, India and emerging economies across Southeast Asia are expanding healthcare delivery through private sector participation and broader insurance coverage, which is improving treatment accessibility across urban and semi-urban populations.

Cost efficiency and manufacturing strength are shaping the regional competitive landscape. China and India are serving as major hubs for active pharmaceutical ingredient (API) production, which is enabling large-scale manufacturing of affordable generic therapies. This capability is increasing treatment penetration while creating pricing pressure on branded products. Governments are implementing procurement programs and expanding national formularies, which is improving drug availability in public healthcare systems. Regional medical associations are promoting awareness and early diagnosis, which is supporting timely intervention. Pharmaceutical companies are strengthening their presence through local partnerships and infrastructure investments, which is enhancing distribution networks and accelerating long-term market development.

Competitive Landscape

The global hyponatremia treatment market structure is moderately consolidated, dominated by leading players such as Otsuka Pharmaceutical Co., Ltd., Teva Pharmaceutical Industries Ltd., Fresenius Kabi AG, Baxter International Inc. and Pfizer Inc. These players collectively capture 35-40% of the market share. The competitive landscape is evolving through the presence of global pharmaceutical companies alongside regional generic drug manufacturers. Branded innovation is remaining concentrated among a limited number of established players, while the generics segment is becoming increasingly fragmented, especially across Asian markets.

Furthermore, companies are actively entering the space as patent expirations are opening new pathways for market participation. This shift is increasing competitive pressure, as manufacturers are focusing on pricing strategies and broader distribution. Firms involved in generics and biosimilar-adjacent development are strengthening their positions, which is driving market share shifts and encouraging continuous strategic adaptation.

Key Industry Developments

- In February 2026, Northern California researchers conducted a study on nearly 14,000 hospitalized patients with severe hyponatremia, and found that faster 24-hour sodium correction rates were associated with a lower risk of 90-day death or delayed neurologic events compared to slow correction, reducing standardized risk by 5.6-9.0 percentage points.

- In June 2025, a Medical Surveillance Monthly Report (MSMR) published by the U.S. Armed Forces Surveillance Center highlighted that exertional hyponatremia, caused mainly by excessive fluid intake during intense physical activity, remains a persistent risk among U.S. military personnel, particularly in hot environments.

Companies Covered in Hyponatremia Treatment Market

- Otsuka Pharmaceutical Co., Ltd.

- Teva Pharmaceutical Industries Ltd.

- Fresenius Kabi AG

- Baxter International Inc.

- Pfizer Inc.

- B. Braun Melsungen AG

- ICU Medical, Inc.

- Mylan N.V.

- Sun Pharmaceutical Industries Ltd.

- Hikma Pharmaceuticals PLC

- Lupin Limited

- Cipla Limited

- Aurobindo Pharma Ltd.

- Siegfried Holding AG

Frequently Asked Questions

The global hyponatremia treatment market is projected to reach US$ 1.7 billion in 2026.

Rising prevalence of hyponatremia in aging populations, hospitalized patients, and those with comorbidities such as heart failure is driving the market.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Major opportunities lie in emerging markets with expanding healthcare infrastructure and rising diagnosis rates.

Otsuka Pharmaceutical Co., Ltd., Teva Pharmaceutical Industries Ltd., Fresenius Kabi AG, Baxter International Inc. and Pfizer Inc. are some of the key players in the market.