- Pharmaceuticals

- Statins Market

Statins Market Size, Share, and Growth Forecast 2026 - 2033

Statins Market by Drug Class (Atorvastatins, Fluvastatins, Lovastatins, Pravastatins, Simvastatins, Others), Therapeutic Treatment (Obesity, Cardiovascular Disorders, Inflammatory Disorders, Others), End User (Hospitals, Clinics, Others), by Regional Analysis, 2026 - 2033

Statins Market Size and Trend Analysis

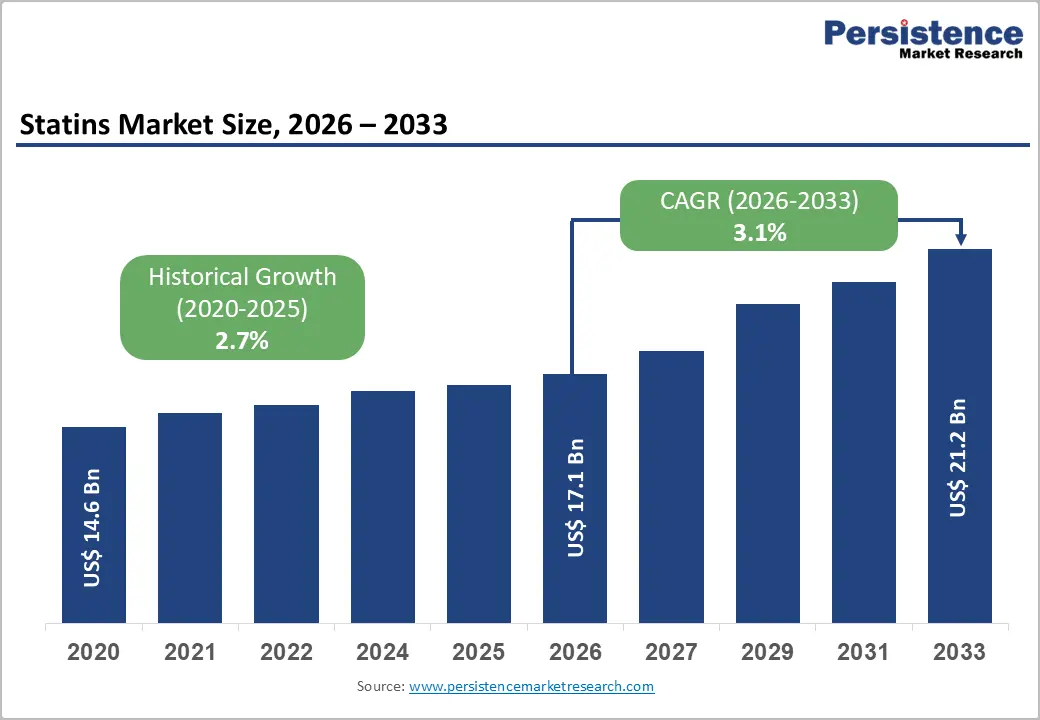

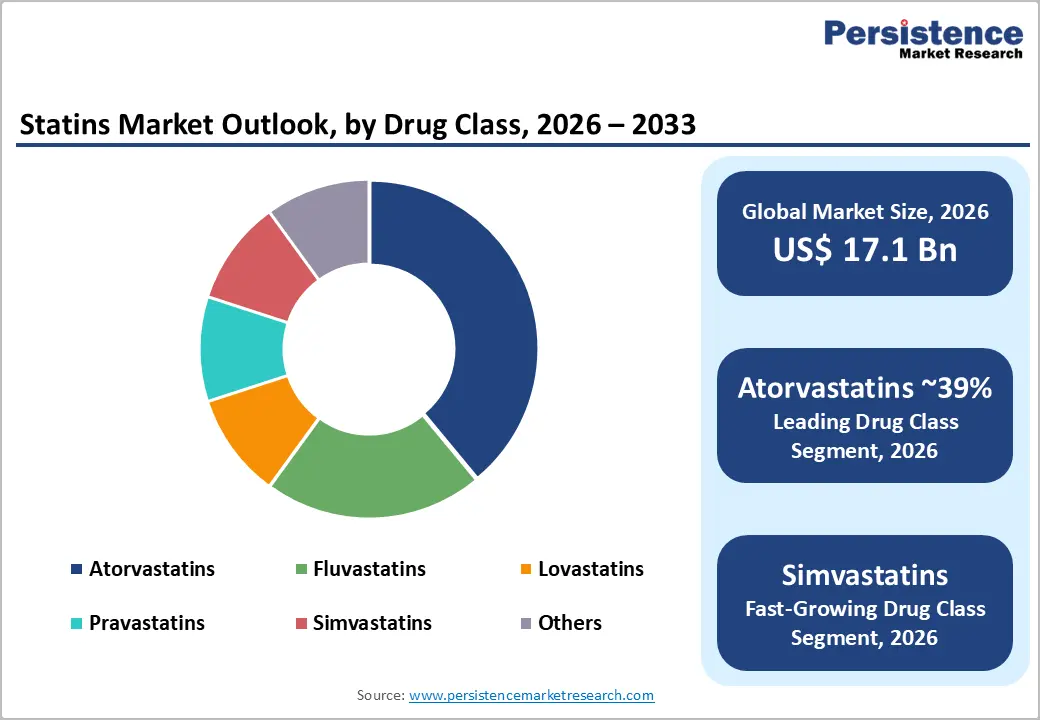

The global statins market size is expected to reach US$ 17.1 billion in 2026 and US$ 21.2 billion by 2033, growing at a CAGR of 3.1% between 2026 and 2033.

The statins market is experiencing steady growth driven by the rising prevalence of cardiovascular diseases such as atherosclerosis, coronary artery disease, and stroke. Increasing cases of hyperlipidemia and unhealthy lifestyle patterns are significantly boosting the demand for cholesterol-lowering medications worldwide.

According to the World Health Organization, more than 17 million people die from cardiovascular diseases annually, and this burden is expected to rise further with aging populations. Developed regions such as the U.S., Europe, and Japan are experiencing increased demand due to a growing elderly population that requires long-term lipid management. Statins remain among the most effective and widely prescribed therapies for reducing LDL cholesterol and preventing cardiovascular complications, supporting sustained market expansion in both developed and emerging healthcare systems.

Key Industry Highlights

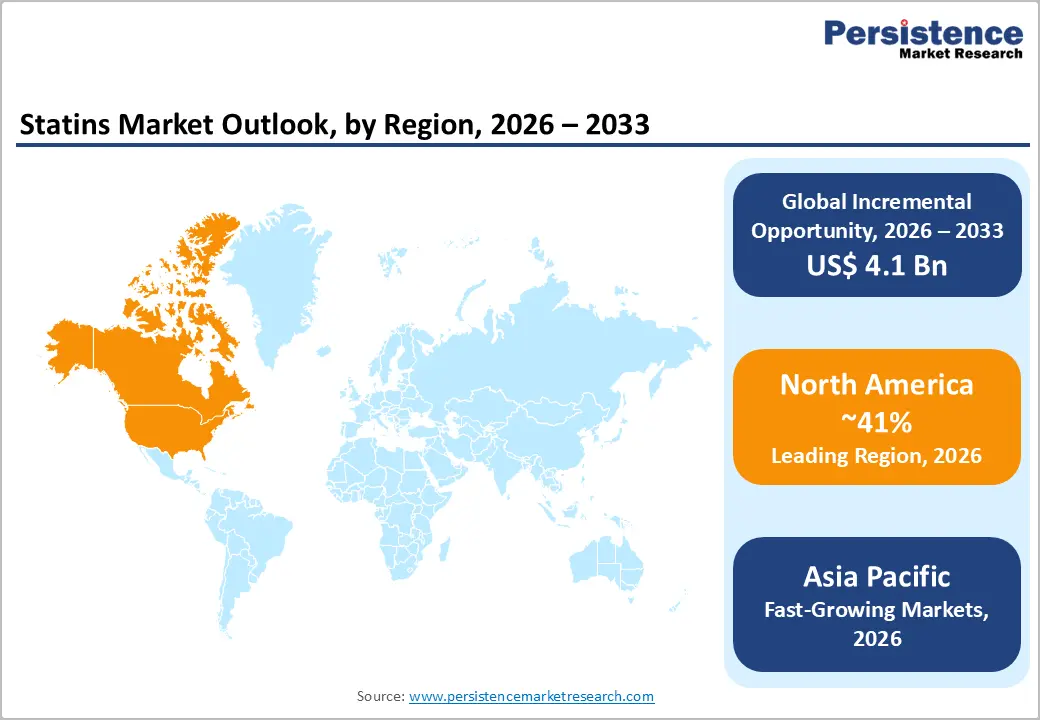

- Leading Region – North America leads the global market with ~41% revenue share, underpinned by the highest cardiovascular disease burden among developed nations, robust prescribing guidelines from the AHA/ACC, and over 200 million annual U.S. statin prescriptions.

- Fastest Growing Region – Asia Pacific grows fastest with rising cardiovascular risks, expanding healthcare access, generic statin availability, and improving hospital infrastructure.

- Dominant Segment – Atorvastatin dominates due to strong LDL cholesterol reduction, broad clinical guideline support, physician preference, and extensive generic availability.

- Fastest-Growing Segment – Simvastatin grows fastest due to demand for fixed-dose combinations, affordability, WHO inclusion, and rising adoption in emerging healthcare markets.

- Key Market Opportunity – Major opportunities exist in statin repurposing, inflammatory disease applications, and fixed-dose combination therapies, expanding treatment and commercial potential.

Market Dynamics

Drivers - Escalating Global Burden of Cardiovascular Disease and Dyslipidaemia

Cardiovascular disease (CVD) remains the world's foremost public health challenge and the single most compelling driver of demand for the statins market. According to the Global Burden of Disease (GBD) Study published in The Lancet, ischemic heart disease and stroke collectively contributed over 15 million deaths in 2022. The American Heart Association (AHA) estimates that nearly 86 million Americans are living with some form of cardiovascular disease or stroke, with dyslipidemia the primary indication for statin prescription affecting approximately 38% of U.S. adults.

The European Society of Cardiology (ESC) guidelines recommend high-intensity statin therapy as the first-line pharmacological intervention for LDL cholesterol reduction, ensuring continued institutional and clinical demand across all major market geographies.

Expanding Generic Statin Penetration in Emerging Markets

The widespread patent expirations of blockbuster statin molecules, including atorvastatin, rosuvastatin, and simvastatin, have enabled a robust generic pharmaceutical ecosystem to emerge, dramatically reducing treatment costs and broadening patient access globally. In India, the world's largest generic pharmaceutical producer, the Indian Pharmaceutical Alliance (IPA) reports that generics account for over 80% of total domestic pharmaceutical volumes. The WHO's Essential Medicines List includes simvastatin and atorvastatin as essential cardiovascular agents, facilitating government procurement and national formulary inclusion across low- and middle-income countries. This generic-driven volume expansion in Asia Pacific, Latin America, and Africa is creating sustained incremental demand, even as branded revenue faces pressure from biosimilar and generic competition in developed markets.

Restraints - Adverse Effect Profile and Statin Non-Adherence Among Patients

Despite their proven efficacy, statins are associated with a range of adverse effects, most notably statin-associated muscle symptoms (SAMS), including myalgia and, in rare cases, rhabdomyolysis, which contribute to high rates of therapy discontinuation. A meta-analysis published in the Journal of the American College of Cardiology found that approximately 10–15% of statin-prescribed patients discontinue therapy within the first year due to perceived or actual side effects.

This non-adherence problem reduces treatment effectiveness at the population level and constrains market volume growth, particularly in segments targeting long-term cardiovascular risk prevention.

Opportunities - Development of Combination Therapies to Spur Avenues due to Enhanced Outcomes

The development of combination therapies, in which statins are combined with other pharmacological agents, is a significant trend in the statin industry. These combination therapies offer improved therapeutic outcomes, better patient compliance, and enhanced cardiovascular risk management. Ezetimibe is a cholesterol-absorption inhibitor that reduces cholesterol absorption from the gastrointestinal tract. When combined with statins, it offers enhanced LDL cholesterol-lowering effects, particularly for patients who require additional lipid-lowering therapy despite statin therapy alone. For instance,

The IMPROVE-IT trial, one of the largest studies involving patients with acute coronary syndrome, found that combining simvastatin with ezetimibe resulted in a 6.4% reduction in major cardiovascular events compared with simvastatin alone. Introduction of PCSK9 inhibitors (like alirocumab and evolocumab) has revolutionized lipid-lowering therapy, offering a more potent way to lower LDL cholesterol levels. For example, the ODYSSEY trial demonstrated that combining alirocumab (a PCSK9 inhibitor) with statins reduced the risk of major adverse cardiovascular events (MACE) by 15% in patients with a history of heart attack, compared with placebo.

Category-wise Insights

Drug Class Analysis

Atorvastatins dominate the global statins market by drug class, accounting for approximately 39% of total market share in 2025. Atorvastatin's pre-eminence is rooted in its clinical pedigree as one of the most extensively prescribed cardiovascular drugs in pharmaceutical history. Lipitor by Pfizer Inc. was the best-selling drug globally for over a decade prior to patent expiry. Clinically, atorvastatin offers high-intensity LDL-C reduction (up to 50–60% dose-dependent reduction) and broad guideline endorsement from the AHA/ACC and ESC. The availability of affordable generic atorvastatin formulations through manufacturers including Teva Pharmaceuticals, Lupin, and Centrient Pharmaceuticals sustains high prescription volumes globally.

Statins are the fastest-growing segment, propelled by the development of combination therapies and strong generic market penetration across Asia Pacific and Latin America.

End User Analysis

Hospitals represent the leading end-user segment in the global Statins market, accounting for approximately 56% of total revenues in 2025. Hospitals serve as the primary point of diagnosis and initiation for statin therapy, particularly for high-risk and hospitalized cardiovascular patients, including those presenting with acute coronary syndrome (ACS), myocardial infarction, or post-surgical cardiovascular intervention. Institutional procurement through national formularies and hospital tender systems facilitates large-volume, consistent purchasing of statins.

The U.S. Centers for Medicare & Medicaid Services (CMS) quality metrics mandate statin prescribing for eligible cardiac patients at discharge, further entrenching hospital-based statin utilization. The clinics segment is the fastest-growing end-user category, driven by the expansion of outpatient cardiovascular risk management and preventive cardiology clinic models across both developed and developing health systems.

Regional Insights

North America Statins Market Trends and Insights

North America leads the global statins market with approximately 41% of total revenue share in 2025. The region's dominance is underpinned by the high prevalence of cardiovascular risk factors, including obesity, diabetes, and hypertension, robust health insurance coverage, strong guideline-driven prescribing practices, and a well-developed pharmaceutical distribution infrastructure. The transition to affordable generic formulations continues to expand patient access while sustaining volume growth.

U.S. Statins Market Size

The U.S. accounts for ~90% of North America's statin revenues, driven by the highest per-capita cardiovascular disease burden among developed nations and the AHA/ACC guideline mandate for broad statin use in eligible patients. The Centers for Disease Control and Prevention (CDC) reports that over 200 million statin prescriptions are dispensed annually in the U.S., reflecting the drug class's deep clinical penetration across all age groups above 40.

Europe Statins Market Trends and Insights

Europe is the second-largest regional market for statins, characterized by well-established national cardiovascular prevention programs, universal healthcare reimbursement frameworks, and strong generic statin penetration. The increasing use of the ESC guidelines' SCORE2 cardiovascular risk stratification tools is driving more systematic statin prescribing, while government reference pricing and mandatory generic substitution policies in major markets continue to shape volume and revenue dynamics.

Germany Statins Market Size

Germany is the largest statin market in Europe, contributing an estimated 22% of European regional revenues. The German Institute for Medical Documentation and Information (DIMDI) records statins among the most frequently prescribed drug classes in Germany. Strong institutional prescribing through hospital networks and general practitioner channels, combined with statutory health insurance (GKV) reimbursement, ensures consistent and high-volume statin utilization across all patient risk categories.

U.K. Statins Market Size

The U.K. statin market is among the most mature in Europe, accounting for ~16% of European regional revenues. The National Institute for Health and Care Excellence (NICE) guidelines recommend statin therapy for all adults with a 10% or greater 10-year cardiovascular risk, resulting in one of the highest statin prescription rates globally. NHS England data confirm statins as the most dispensed drug class in primary care.

Asia Pacific Statins Market Trends and Insights

Asia Pacific is the fastest-growing regional market for statins, driven by a rapidly expanding patient pool as cardiovascular risk factor prevalence, including hypertension, diabetes, and obesity, rises across the region's aging and urbanizing populations. China dominates regional statin revenues, with the National Healthcare Security Administration (NHSA) including multiple generic statin formulations in the National Reimbursement Drug List (NRDL), driving volume-based procurement and widespread clinical adoption across tier-1 and tier-2 hospital systems. Rising healthcare expenditure and expanding insurance coverage across India, Japan, and Southeast Asia further accelerate regional market growth.

India Statins Market Size

India is a high-growth statin market, accounting for ~14% of Asia Pacific regional revenues in 2025. India's statin market is driven by the dual burden of cardiovascular disease and a world-class generic pharmaceutical manufacturing base. The Indian Council of Medical Research (ICMR) identifies dyslipidemia as a major and under-treated cardiovascular risk factor across Indian adults, while domestic producers, including Lupin and AdvaCare Pharma, supply affordable statin formulations both domestically and to export markets.

Japan Statins Market Size

Japan accounts for ~20% of Asia Pacific statin revenues, reflecting a large, aging population with high cardiovascular risk awareness and a sophisticated healthcare system. The Japan Atherosclerosis Society (JAS) guidelines endorse statin therapy as the standard of care for dyslipidemia management. Kowa Pharmaceuticals, developer of pitavastatin, holds a notable domestic competitive position alongside global generics manufacturers that supply established statin molecules under Japan's regulated pharmaceutical pricing framework.

Competitive Landscape

The global statins market is moderately consolidated among originator innovators and large-scale generic manufacturers. Pfizer Inc., Merck & Co., Inc., AstraZeneca, and Novartis AG maintain strong brand equity through branded legacy products and ongoing lifecycle management strategies. Generic leaders including Teva Pharmaceuticals, Lupin, and Centrient Pharmaceuticals compete aggressively on volume and pricing.

Key competitive differentiators include manufacturing cost efficiency, global regulatory approvals, combination product pipelines, and formulary positioning. Emerging trends include patient adherence digital programmes, fixed-dose combination launches, and geographic expansion into high-growth emerging markets through local partnerships and volume-based procurement agreements.

Key Developments

- In October 2024, the National Institute for Health and Excellence revealed that 5.3 million people in England were given a NICE-recommended statin or ezetimibe by their GP to reduce their cholesterol during 2023 to 2024, the largest number on record.

- In October 2024, Amgen presented positive long-term real-world data for Repatha at the American Heart Association Scientific Sessions. The findings showed sustained LDL-C reduction and cardiovascular benefits when Repatha was used alongside statins, further strengthening the role of combination therapies for high-risk patients.

- In February 2024, Teva Pharmaceuticals received U.S. FDA approval for a once-daily fixed-dose combination statin tablet containing atorvastatin and ezetimibe. This new formulation was developed to simplify cholesterol management by combining two lipid-lowering agents into a single pill, improving patient adherence and treatment outcomes.

- In January 2024, a recent study by researchers at the Karolinska Institutet, published in Alzheimer's Research and Therapy, revealed an intriguing link between statins and Alzheimer’s progression.

- Patients diagnosed with Alzheimer’s dementia who received statin therapy showed slower cognitive decline compared to those who did not.

Global Statins Market – Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 14.6 Billion |

|

Current Market Value (2026) |

US$ 17.1 Billion |

|

Projected Market Value (2033) |

US$ 21.2 Billion |

|

CAGR (2026–2033) |

3.1% |

|

Leading Region |

North America, 41% market share (2025) |

|

Dominant Drug Class |

Atorvastatins, ~39% market share (2025) |

|

Top-ranking Therapeutic Treatment |

Cardiovascular Disorders, ~62% market share (2025) |

|

Incremental Opportunity |

US$ 4.1 Billion |

Companies Covered in Statins Market

- Pfizer Inc.

- Centrient Pharmaceuticals Netherlands B.V.

- CMP Pharma, Inc.

- AstraZeneca

- Salerno Pharma

- Kowa Pharmaceuticals America, Inc.

- Medicure Pharma

- Covis Pharma

- Novartis AG

- Teva Pharmaceuticals USA, Inc.

- Lupin

- AdvaCare Pharma®

- Arlak Corazon

- Merck & Co., Inc.

- CTX Lifesciences

- Biofield Pharma

- Organon group of companies

- Taj Pharmaceuticals Limited

- Aurobindo Pharma USA

- Biocon

Frequently Asked Questions

The global is estimated to be valued at US$ 17.1 billion in 2026.

Rising cardiovascular disease burden, strong global guideline support, and expanding generic statin access through government healthcare programs drive sustained market demand.

North America is the leading region with approximately 41% of global market share in 2025.

Major growth opportunities lie in statin repurposing for inflammatory disorders and fixed-dose combination therapies with ezetimibe and complementary agents.

Prominent players in the industry include Pfizer Inc., Centrient Pharmaceuticals Netherlands B.V., and CMP Pharma, Inc.