- Energy Storage Solutions

- Graphite Felt Market

Graphite Felt Market Size, Share, and Growth Forecast, 2026 - 2033

Graphite Felt Market by Product Type (Carbon Felt, Graphitized, Others), Form (Polyacrylonitrile (PAN) based Felt, Rayon‑Based Felt, Others), Application, and Regional Analysis for 2026 - 2033

Graphite Felt Market Size and Trends Analysis

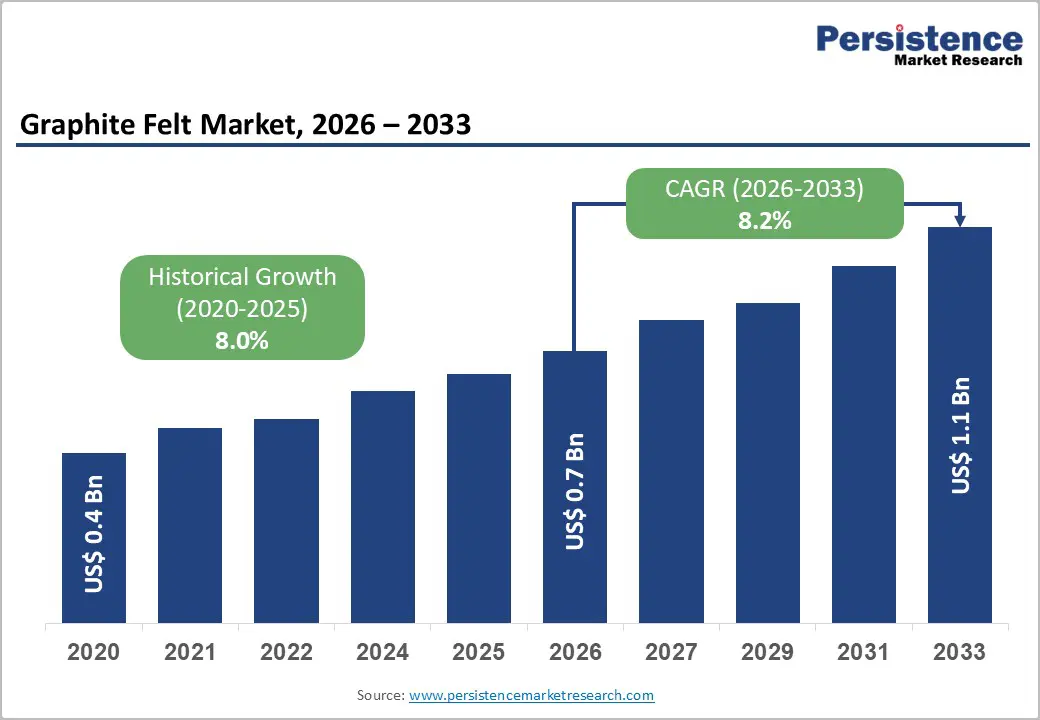

The global graphite felt market size is likely to be valued at US$0.7 billion in 2026 and is expected to reach US$1.1 billion by 2033, growing at a CAGR of 8.2% during the forecast period from 2026 to 2033, driven by increasing demand for high-performance thermal insulation and electrochemical materials across industrial and energy-storage applications.

The industry remains strongly specification-oriented, with procurement decisions increasingly based on factors such as material purity, thermal conductivity, and electrochemical efficiency rather than volume alone.

Furnace insulation and heat-treatment applications continue to account for the largest share of market revenue, while battery-grade graphite felt is emerging as the fastest-growing segment due to expanding adoption of redox flow batteries, fuel cells, and advanced energy-storage technologies. In addition, rising semiconductor manufacturing investments and broader industrial decarbonization initiatives are driving global demand for premium-grade graphite felt products.

Key Industry Highlights:

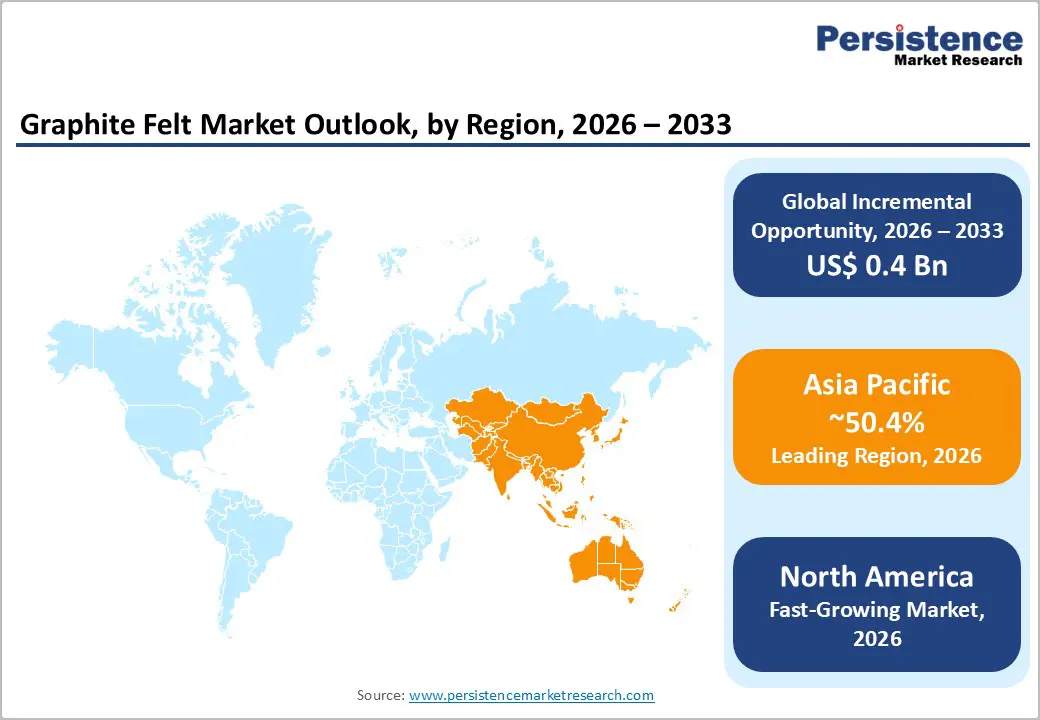

- Leading Region: Asia Pacific is projected to account for an anticipated 50.4% of market share in 2026, supported by China’s dominance in semiconductor manufacturing, solar PV production, battery materials, and large-scale industrial furnace operations.

- Fastest-growing Region: North America is projected to register the fastest growth during the forecast period, driven by semiconductor localization programs, expansion of silicon carbide manufacturing, and rising investments in utility-scale energy storage systems.

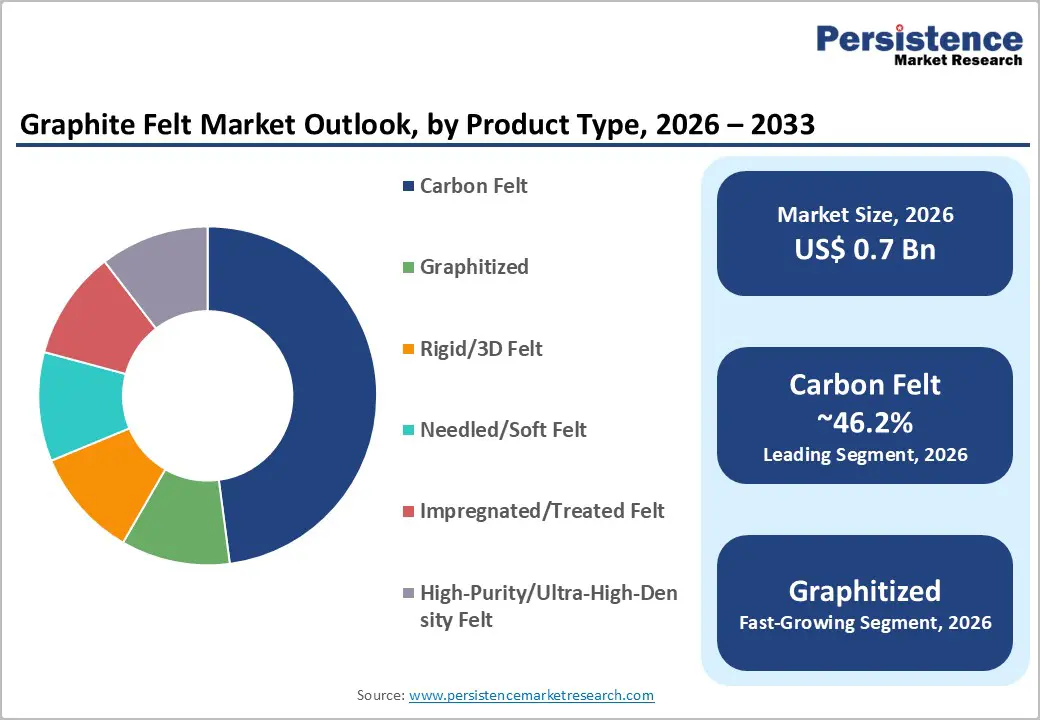

- Dominant Product Type: Carbon felt is anticipated to hold approximately 46.2% market share in 2026, due to its broad use in vacuum furnaces, metallurgical processing, and industrial thermal insulation applications.

- Leading Form: PAN-based felt is expected to account for nearly 55.9% of the market share in 2026, owing to its strong mechanical strength, oxidation resistance, scalable manufacturing, and cost-performance balance.

DRO Analysis

Drivers - Semiconductor and High-Temperature Manufacturing Expansion

The increasing scale of semiconductor fabrication and advanced high-temperature manufacturing is significantly driving demand for graphite felt. Graphite felt is widely used in furnace hot zones, thermal shielding systems, silicon crystal growth equipment, and polysilicon processing due to its low thermal conductivity, chemical stability, and resistance to extreme temperatures. Semiconductor fabrication facilities require highly purified insulating materials that maintain process consistency during crystal growth and wafer manufacturing.

Global semiconductor capital expenditure continues to rise as countries expand domestic chip manufacturing capabilities. The U.S. has made major investments through semiconductor manufacturing support programs, while Asia-Pacific economies continue to scale up advanced wafer production capacity. These investments directly support graphite felt consumption because high-temperature processing equipment requires premium insulation systems with extremely low ash content and controlled thermal performance.

Growth of Renewable Energy Storage and Electrochemical Systems

The expansion of renewable energy generation is creating a strong growth environment for graphite felt used in electrochemical energy storage systems. Graphite felt is a critical electrode material in vanadium redox flow batteries, fuel cells, and advanced stationary storage systems because of its electrical conductivity, chemical resistance, and structural stability.

As renewable energy penetration increases globally, utility operators and grid infrastructure providers require large-scale storage systems capable of balancing intermittent solar and wind generation. Long-duration storage technologies, especially redox-flow batteries, are attracting greater commercial attention for their operational lifespans, scalability, and suitability for utility-scale applications.

Battery-grade graphite felt is therefore transitioning from a specialized industrial material into a strategically important component within energy storage infrastructure. Material suppliers are responding by introducing products with improved surface area, lower electrical resistance, and enhanced electrochemical performance.

Restraint - High Production Costs and Qualification Barriers

Despite strong growth potential, the graphite felt market faces structural limitations related to production complexity, purification requirements, and customer qualification standards. Graphite felt manufacturing requires energy-intensive heat-treatment processes that reach extremely high temperatures, increasing operational costs and capital investment requirements.

High-purity graphite felt used in semiconductor and battery applications must meet strict contamination-control standards with very low ash content. Achieving these specifications requires additional purification stages, advanced process controls, and extensive quality assurance procedures. These factors increase production costs while also extending customer approval and qualification timelines.

Demand volatility in the semiconductor and advanced manufacturing industries also creates utilization risks for suppliers. Production capacity expansion may temporarily outpace end-market demand during cyclical slowdowns, creating pricing pressure and margin challenges. As a result, smaller manufacturers often struggle to compete in premium applications that require substantial technical investment and long-term customer validation.

Opportunities - Expansion of Redox-Flow Battery Infrastructure

Redox-flow battery deployment represents one of the strongest long-term opportunities for graphite felt manufacturers. Although the installed global base for vanadium redox-flow systems remains relatively limited compared with lithium-ion technologies, deployment is expanding steadily across utility-scale renewable integration projects and industrial backup systems.

Graphite felt serves as a core electrode material in these systems because it provides high conductivity, structural durability, and resistance to corrosive electrolyte environments. As demand for long-duration storage increases, suppliers capable of producing optimized battery-grade felt with consistent porosity and electrochemical efficiency are expected to benefit from premium pricing.

Premiumization in Semiconductor and Silicon Carbide Manufacturing

Expanding semiconductor and silicon carbide manufacturing activities are generating substantial opportunities for premium-grade graphite felt products. Advanced crystal-growth furnaces, silicon wafer fabrication lines, and high-temperature semiconductor processing systems require ultra-pure insulation materials that can maintain consistent thermal stability at temperatures above 2,000°C.

The rising adoption of silicon carbide semiconductors across electric vehicles, renewable energy systems, and industrial power electronics is further driving demand for high-purity graphite insulation solutions. In addition, every new semiconductor fabrication plant and crystal-growth installation creates demand for specialized insulation systems, while ongoing maintenance and replacement cycles continue to support recurring consumption of graphite felt materials.

For graphite felt suppliers, this trend supports a transition toward higher-margin engineered products rather than standardized industrial insulation materials. Long-term growth will likely favor manufacturers capable of combining purification expertise, process engineering, and collaborative development relationships with semiconductor equipment producers.

Category-wise Analysis

Product Type Insights

Carbon felt is anticipated to account for approximately 46.2% of the global graphite felt market share in 2026, supported by its cost-effectiveness, broad industrial applicability, and dependable thermal insulation performance. Carbon felt is widely used in vacuum furnaces, annealing systems, and metallurgical heat-treatment equipment where high-temperature stability is required without the need for ultra-high purity.

For example, steel heat-treatment facilities and industrial sintering furnaces often use carbon-felt insulation to improve thermal efficiency and reduce energy loss. Its strong commercial position also comes from established supply chains and easier qualification compared with premium graphite grades. Recurring replacement demand from furnace refurbishment cycles further supports steady consumption across industrial manufacturing sectors.

Graphitized is anticipated to register the fastest growth rate through 2033, driven by rising demand from advanced batteries, semiconductor processing, and electrochemical applications. Compared with carbon felt, graphite felt offers higher thermal stability, improved conductivity, lower impurity levels, and stronger chemical resistance. These advantages make it highly suitable for vanadium redox-flow batteries, fuel cells, silicon carbide crystal-growth systems, and semiconductor wafer manufacturing.

For instance, battery manufacturers increasingly use purified graphite felt electrodes in large-scale energy storage systems, while semiconductor fabs rely on graphite felt insulation for crystal-growth furnaces requiring contamination control. The segment is also benefiting from the expansion of renewable energy, electrification trends, and increasing investment in semiconductor localization programs globally.

Form Insights

PAN-based felt is anticipated to hold approximately 55.9% of the market share in 2026, making it the dominant form segment due to its strong mechanical strength, oxidation resistance, and scalable production characteristics. PAN-based materials are widely used in industrial furnace insulation, thermal shielding, and battery backing systems because they provide a balanced cost-to-performance ratio.

For example, PAN-based felt is commonly deployed in vacuum heat-treatment furnaces and energy-storage insulation systems where durability and stable thermal performance are required. The segment also benefits from broad supplier availability, allowing industrial buyers to diversify sourcing and simplify qualification procedures. Its reliable processability and moderate production costs continue to support widespread adoption across both standard and advanced thermal management applications.

High-purity and graphitized grades are anticipated to witness the highest CAGR during the forecast period, supported by increasing demand from semiconductor, silicon carbide, and high-end battery manufacturing applications. These grades provide extremely low ash content, superior thermal consistency, and improved conductivity under high-temperature operating conditions.

For example, silicon carbide crystal-growth systems and semiconductor wafer-processing furnaces increasingly require graphitized felt capable of operating in highly controlled environments. Similarly, advanced redox-flow battery systems use purified graphite felt electrodes to improve energy efficiency and electrochemical stability. Manufacturers are expanding investments in purification technologies and advanced graphitization processes as industrial customers prioritize operational consistency, contamination control, and long-term performance reliability.

Regional Insights

North America Graphite Felt Market Trends

North America represents a strategically important graphite felt market driven by semiconductor manufacturing, aerospace applications, and advanced energy storage investments. The region benefits from strong R&D capabilities, high-value industrial production, and increasing government support for domestic semiconductor and clean-energy supply chains.

U.S. Graphite Felt Market Trends

The U.S. dominates the North American graphite felt market due to large-scale semiconductor fabrication activity and rising investment in advanced manufacturing infrastructure. Demand is particularly strong for high-purity graphite felt used in silicon wafer processing, crystal-growth furnaces, and silicon carbide semiconductor production.

The country is also witnessing increased deployment of utility-scale battery storage and renewable energy infrastructure, supporting demand for graphite felt electrodes in redox-flow batteries and fuel cells. The aerospace and defense industries also contribute to consumption through thermal shielding and high-temperature insulation applications.

Canada Graphite Felt Market Trends

Canada represents a smaller but steadily growing market, supported by clean-energy initiatives, metallurgical processing, and advanced materials research. Industrial furnace applications remain the primary driver of graphite felt demand, particularly in metal processing and specialty manufacturing.

The country’s focus on sustainable energy infrastructure and on developing the battery-material supply chain is expected to create additional opportunities for premium graphite felt products used in energy storage systems and thermal management applications.

Europe Graphite Felt Market Trends

Europe remains a major premium market characterized by advanced industrial manufacturing, strict environmental regulations, and strong energy-efficiency standards. Demand is supported by semiconductor processing, industrial decarbonization initiatives, and investments in renewable energy technologies.

Germany Graphite Felt Market Trends

Germany is the leading graphite felt market in Europe due to its strong industrial base, advanced furnace manufacturing industry, and high concentration of automotive and semiconductor-related production facilities. Demand is particularly strong for vacuum furnace insulation, silicon carbide processing, and precision thermal management systems.

German manufacturers continue investing in energy-efficient industrial technologies, supporting the adoption of high-performance graphite felt materials across metallurgy, specialty ceramics, and advanced manufacturing sectors.

U.K. Graphite Felt Market Trends

The U.K. is an important regional market driven by aerospace engineering, advanced materials research, and clean-energy investments. Graphite felt demand is supported by thermal processing applications, industrial furnace systems, and growing interest in hydrogen and fuel-cell technologies.

Research collaborations between universities, material suppliers, and industrial manufacturers are also supporting innovation in electrochemical and high-temperature insulation materials.

France Graphite Felt Market Trends

France benefits from strong participation in aerospace, nuclear energy, and advanced industrial manufacturing sectors. The country’s focus on low-carbon energy systems and industrial efficiency improvements supports demand for graphite felt used in thermal insulation and energy-storage applications. Semiconductor-related investments and advanced engineering capabilities are also contributing to growth in high-purity graphite felt consumption.

Asia Pacific Graphite Felt Market Trends

Asia Pacific is the largest regional market for graphite felt, supported by extensive manufacturing capacity, integrated supply chains, and dominant semiconductor and solar production ecosystems. The region benefits from lower production costs, strong feedstock availability, and expanding renewable energy infrastructure.

China Graphite Felt Market Trends

China represents the largest graphite felt market globally due to its massive industrial manufacturing base, semiconductor production capacity, and renewable energy expansion. The country dominates solar photovoltaic manufacturing and battery-material processing, both of which require high-temperature insulation systems using graphite felt. China also benefits from large-scale graphite processing infrastructure and strong domestic supplier networks, allowing competitive production of both standard and high-purity graphite felt products.

Japan Graphite Felt Market Trends

Japan remains a technologically advanced market focused on precision thermal processing, semiconductor manufacturing, and specialty materials engineering. Demand is concentrated in high-purity graphite felt applications used in semiconductor wafer processing, electronics manufacturing, and advanced industrial furnaces. Japanese manufacturers also play a major role in developing engineered graphite materials for fuel cells and advanced energy-storage systems.

India Graphite Felt Market Trends

India is emerging as a promising growth market supported by industrial expansion, renewable energy investments, and increasing semiconductor manufacturing initiatives. Demand is rising in metallurgical processing, industrial furnace insulation, and solar manufacturing applications. Government-led manufacturing programs and investments in energy infrastructure are expected to support long-term demand for graphite felt across industrial and clean-energy sectors.

Competitive Landscape

The global graphite felt market is moderately consolidated, with a small group of multinational specialty carbon-material manufacturers controlling a significant share of premium applications. Leading suppliers compete primarily through purification capability, process engineering expertise, technical customization, and long-term customer qualification.

Leading companies are focusing on purification technologies, application-specific product development, and regional manufacturing expansion. Innovation, premiumization, and customer co-development remain the primary competitive strategies. Suppliers are also emphasizing long-term qualification partnerships and localized technical support to strengthen relationships with semiconductor, battery, and industrial equipment manufacturers.

Key Industry Developments:

- In June 2025, SGL Carbon SE announced the launch of its new SIGRACELL® GFX4.8 EA battery felt for redox-flow batteries, designed with low electrical resistance and enhanced surface area to improve electron exchange and long-cycle energy storage performance in stationary renewable energy systems.

Companies Covered in Graphite Felt Market

- Mersen

- SGL Carbon SE

- Morgan Advanced Materials plc

- Nippon Carbon Co., Ltd.

- Toray Industries, Inc.

- Kureha Corporation

- Schunk Carbon Technology

- Graphite India Limited

- Beijing Great Wall Co., Ltd.

- CM Carbon Co., Ltd.

- Chemshine Carbon Co., Ltd.

- Gansu Haoshi Carbon Fiber Co., Ltd.

- CFC Carbon Co., Ltd.

- Sinotek Materials Co., Ltd.

- Kejing Carbon Fiber Technology Co., Ltd.

- AvCarb Material Solutions

Frequently Asked Questions

The global graphite felt market is anticipated to be valued at approximately US$0.7 billion in 2026.

The graphite felt market is projected to reach nearly US$1.1 billion by 2033.

Key market trends include growing adoption of graphite felt in vanadium redox-flow batteries, increasing semiconductor fabrication investments, expansion of renewable energy storage infrastructure, rising demand for high-purity insulation materials, and advancements in graphitization and purification technologies.

Carbon felt remains the leading product segment, accounting for an anticipated 46.2% share of the market in 2026 due to its extensive use in vacuum furnaces, metallurgical processing, and industrial thermal insulation systems.

The graphite felt market is projected to grow at a CAGR of 8.2% between 2026 and 2033.

Major companies include Mersen, SGL Carbon SE, Morgan Advanced Materials plc, Nippon Carbon Co., Ltd., and Toray Industries, Inc.