- Bulk Chemicals

- Humic Acid Market

Humic Acid Market Size, Share, and Growth Forecast 2026 - 2033

Humic Acid Market by Form (Powder, Granular, Liquid), Grade (Technical, Agricultural), Application (Soil Conditioner, Organic Fertilizer, Water Treatment, Animal Feed, Others), and Regional Analysis for 2026 - 2033

Humic Acid Market Size and Trend Analysis

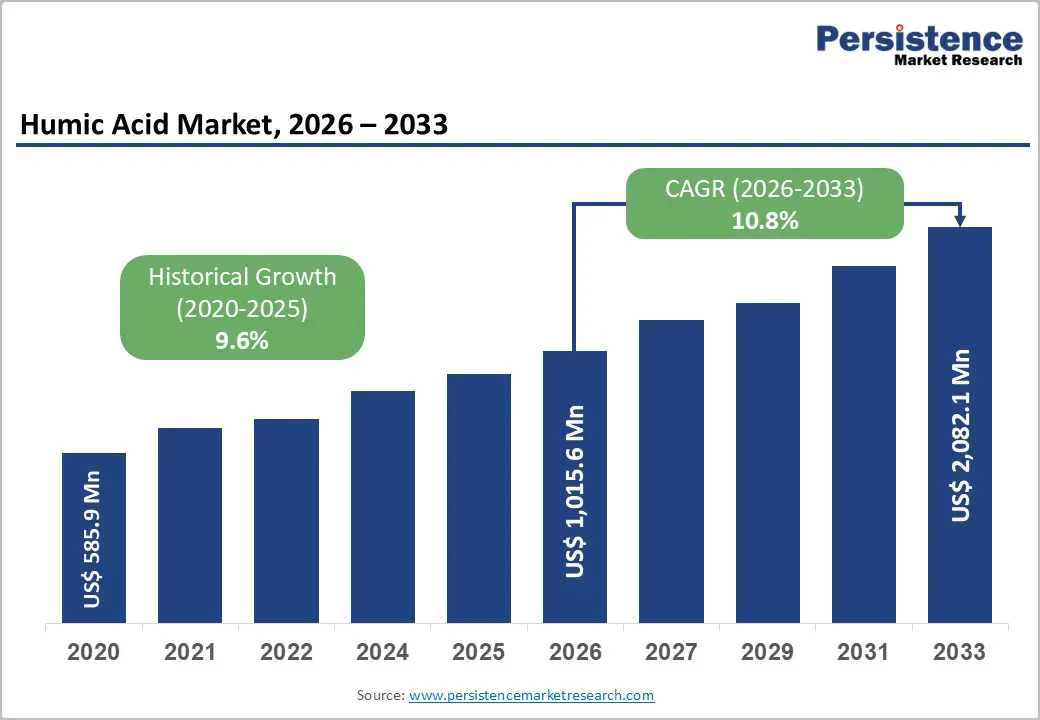

The global humic acid market size is valued at US$ 1.0 billion in 2026 and is projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 10.8% between 2026 and 2033. Rising global urgency around soil degradation, declining chemical fertilizer efficacy, and the accelerating transition toward sustainable and regenerative agriculture are collectively powering robust market expansion.

Governments across North America, Europe, and Asia-Pacific are deploying subsidy programs and regulatory mandates, including the European Green Deal and the U.S. Department of Agriculture (USDA) organic incentive frameworks, that are institutionalizing demand for bio-based soil inputs. The growing global organic food industry and the formalization of biostimulant regulations under the EU Fertilising Products Regulation (FPR) 2019/1009 are further anchoring the market's long-term growth trajectory.

Key Industry Highlights:

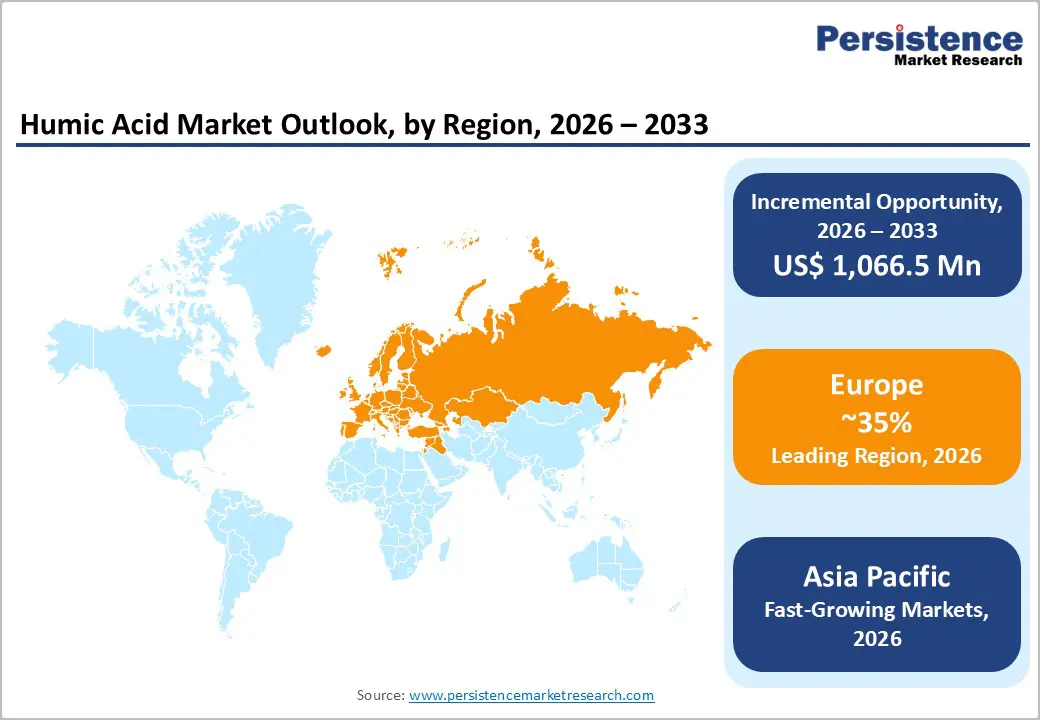

- Leading Region: Europe dominates the global humic acid market, with 35% market share, driven by the EU Green Deal, Farm to Fork Strategy, and formal biostimulant recognition under EU FPR 2019/1009, with Germany, France, Spain, and Italy as the largest national consumer markets fueling premium product demand.

- Fastest Growing Region: Asia-Pacific is the fastest-growing regional market, with China and India leading demand expansion supported by large smallholder farming populations, the PKVY organic farming program, and rapid scaling of aquaculture operations across ASEAN nations.

- Dominant Powder Segment: The powder form segment leads the global market with approximately 46% revenue share, preferred for large-scale soil conditioning and NPK fertilizer blending due to its cost efficiency, high concentration, and compatibility with automated precision agricultural spreading systems.

- Fastest Growing Segment: The liquid humic acid segment is the fastest-growing form, expanding at a CAGR of approximately 12%, driven by rising fertigation system adoption, precision irrigation investments, and high-value crop production expansion across Europe and Asia-Pacific.

- Key Market Opportunity: Enforcement of EU Regulation 2019/1009 formally recognizing biostimulants as a product category, combined with the Farm to Fork Strategy's binding 20% synthetic fertilizer reduction target by 2030, creates a transformative and well-funded commercial opportunity for premium humic acid biostimulant producers.

| Key Insights | Details |

|---|---|

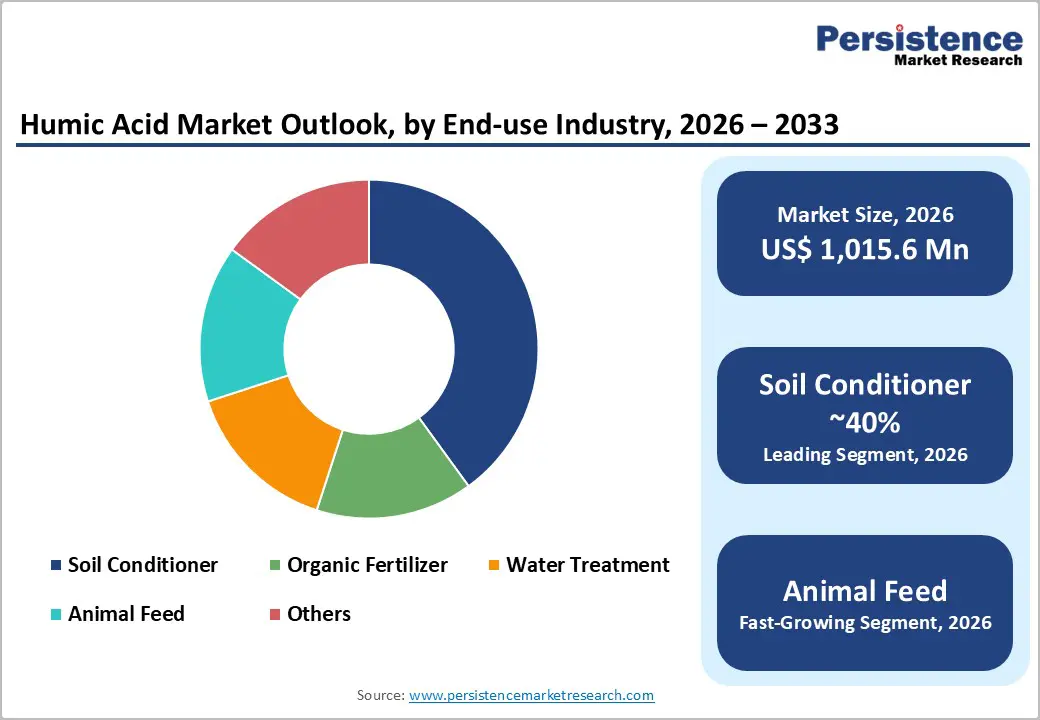

| Humic Acid Market Size (2026E) | US$ 1,015.6 Mn |

| Market Value Forecast (2033F) | US$ 2,082.1 Mn |

| Projected Growth CAGR (2026 - 2033) | 10.8% |

| Historical Market Growth (2020 - 2025) | 9.6% |

DRO Analysis

Drivers - Rising Adoption of Sustainable Agriculture and Organic Farming

Rising global awareness of soil degradation and the adverse impacts of synthetic fertilizers is compelling farmers and policymakers to pivot toward sustainable agricultural inputs, creating powerful demand tailwinds for humic acid. According to the Food and Agriculture Organization (FAO), over 33% of the world's soils are moderately to highly degraded, intensifying the urgency for organic soil amendments and biostimulants.

Governments across North America, Europe, and the Asia-Pacific are channeling subsidies toward eco-friendly farming through programs such as the European Common Agricultural Policy (CAP), institutionalizing demand for humic acid as a primary soil conditioner. The global organic food sector generated over USD 132 billion in sales as of recent industry estimates, further anchoring long-term structural demand for natural soil amendments.

Growing Demand for Soil Remediation and Environmental Applications

Beyond agriculture, humic acid is rapidly gaining traction in environmental remediation, a sector experiencing accelerated investment and policy momentum. Its capacity to bind heavy metals, reduce contaminants' bioavailability, and restore microbial ecosystems makes it a preferred tool for soil and water cleanup operations. The United Nations Environment Programme (UNEP) estimates that land degradation costs the global economy up to USD 10.6 trillion annually in lost ecosystem services, driving both public and private investment into bio-based remediation solutions.

Several government-funded remediation initiatives across Europe and North America are incorporating humic acid to reduce reliance on harsh chemical treatments. The European Soil Strategy for 2030 explicitly mandates the adoption of bio-based soil health solutions, while the U.S. Environmental Protection Agency (EPA) has recognized humic substances as effective agents within its contaminated land restoration programs, substantially broadening humic acid's addressable market beyond traditional agricultural applications.

Restraints - High Production Costs and Complex Extraction Processes

High extraction and processing costs remain a significant structural barrier to market penetration, particularly in price-sensitive emerging economies across South Asia and Sub-Saharan Africa. Humic acid is predominantly derived from leonardite, lignite, and peat, carboniferous deposits requiring specialized mining, chemical extraction, and multi-stage purification. According to the U.S. Geological Survey (USGS), lignite production costs have escalated materially due to tightening environmental compliance requirements, indirectly inflating humic acid production costs by approximately 10-15% over the past five years. These economic headwinds limit mainstream adoption among smallholder farmers who operate under constrained input budgets, restricting the market's full penetration potential in high-growth developing regions despite strong underlying agricultural fundamentals.

Lack of Quality Standardization and Regulatory Inconsistency

The humic acid market is hampered by the absence of internationally harmonized quality standards, resulting in significant variability in active compound concentration across commercial products. Concentrations of humic and fulvic acids in commercial formulations range from as low as 15% to over 90%, causing inconsistent agronomic outcomes and undermining farmer confidence. While the International Humic Substances Society (IHSS) has established scientific definitions, these do not translate into commercially enforceable product standards.

Although the EU Fertilising Products Regulation (FPR) 2019/1009 introduced minimum thresholds for biostimulants, enforcement across 27 EU member states remains uneven. This regulatory fragmentation increases compliance costs for multinational producers and deters new market entrants, constraining competitive dynamics and slowing the market's full commercial development.

Opportunities - Surging Demand in Aquaculture and Animal Feed Applications

The aquaculture and animal feed segments represent the fastest-growing end-use opportunity for humic acid, driven by converging regulatory and consumer demand dynamics. According to the Food and Agriculture Organization (FAO), global aquaculture production exceeded 87.5 million tonnes in 2022, with the sector expanding rapidly across Southeast Asia and generating substantial incremental demand for eco-friendly, natural feed additives.

Simultaneously, regulatory restrictions on antibiotic use in animal feed across the European Union and the United States, enforced under the EU's Veterinary Medicinal Products Regulation and the U.S. Veterinary Feed Directive (VFD), are accelerating the transition toward natural performance enhancers, including humic acid. Peer-reviewed studies published in journals affiliated with the American Society of Animal Science have confirmed that humic acid supplementation improves feed conversion ratios by 8-12%, substantially improving cost-per-unit productivity for livestock and aquaculture producers and underpinning its commercial scalability.

Biostimulant Regulatory Frameworks and the EU Green Deal

The formalization of biostimulant regulations across key global markets represents a landmark commercial opportunity for humic acid manufacturers seeking long-term revenue visibility and regulatory legitimacy. The enforcement of EU Regulation 2019/1009 (EU Fertilising Products Regulation) in July 2022 officially recognized plant biostimulants, including humic and fulvic acid, as a distinct regulatory product category, enabling standardized registration, labeling, and marketing across all 27 EU member states.

The European Green Deal's Farm to Fork Strategy further targets a 20% reduction in synthetic fertilizer use and a 50% reduction in pesticide dependency by 2030, directly benefiting bio-based inputs with established efficacy credentials. In North America, the USDA's Environmental Quality Incentives Program (EQIP) continues to channel federal incentives toward natural soil amendment adoption, providing market participants with a funded pathway to scale adoption among commercial farming operations.

Category-wise Analysis

Form Insights

The powdered form segment commands a significant share of the global humic acid market, representing approximately 46%. This dominance is due to its cost efficiency, operational versatility, and strong compatibility with NPK and micronutrient fertilizer blends, which enable the development of tailored soil rehabilitation programs. As reported by the American Society of Agronomy, powdered humic acid can enhance soil organic carbon levels by up to 25%, making it a preferred option for large-scale row crop farmers worldwide.

Its high concentration of active compounds facilitates precise dosage calibration, an advantage for precision agriculture utilizing automated spreading and fertigation equipment. Furthermore, lower storage and transportation costs compared to liquid and granular forms enhance its economic appeal. The growing utilization of powdered humic acid in degraded soils across India, China, and Brazil, leading agricultural nations, continues to solidify the segment’s market leadership.

Grade Insights

The technical grade segment represents approximately 68% of the global humic acid market, highlighting its critical role in industrial applications such as oil and gas drilling fluid formulation, municipal water treatment, and environmental remediation. Sourced mainly from high-quality leonardite deposits, technical-grade humic acid ensures consistent physicochemical properties essential for maintaining purity, viscosity, and efficacy in industrial uses.

The U.S. oil and gas industry significantly utilizes it as a cost-effective viscosity modifier, while increasing environmental regulations, including the U.S. Clean Water Act and EU Water Framework Directive, are fueling demand for its use in water quality management. In contrast, the agricultural grade segment is the fastest growing, driven by government mandates for sustainable soil inputs in European and Asia-Pacific markets, particularly within organic certification frameworks managed by the European Commission and national agricultural ministries.

Application Insights

The soil conditioner segment leads the global humic acid market, accounting for approximately 40% of total revenue. This dominance is driven by a significant global soil health crisis, as indicated by the Food and Agriculture Organization (FAO), which reports threats to soil biodiversity across over 60% of agricultural areas. Restoring soil organic matter and enhancing microbial activity has become essential for farming communities.

Humic acid as a soil conditioner provides critical agronomic benefits, including improved cation exchange capacity (CEC), water retention, and microbial diversity, directly addressing challenges in degraded farmland. The rise of regenerative agriculture, supported by initiatives like the European Common Agricultural Policy (CAP) and the U.S. Conservation Stewardship Program (CSP), is facilitating widespread adoption of humic acid-based inputs. Furthermore, increasing salinity-affected farmland in South Asia and the Middle East is generating new markets with strong demand for these solutions.

Regional Insights

North America Humic Acid Market Trends

The North American humic acid market is predominantly driven by the United States, which accounts for nearly 65% of regional revenues. The U.S. agricultural sector is experiencing a significant shift toward sustainable inputs, supported by federal programs such as the USDA’s Environmental Quality Incentives Program (EQIP) and the Conservation Stewardship Program (CSP), which promote the adoption of environmentally friendly soil amendments.

The expansion of certified organic farmland, exceeding 5.5 million acres under the USDA National Organic Program, has further reinforced demand for humic acid as a key organic input. Canada contributes approximately 25% of regional demand, supported by a CAD 200 million government investment in sustainable farming technologies. Geopolitical tensions affecting fertilizer supply chains and provisions under the Inflation Reduction Act are further accelerating market growth, alongside continued regional innovation and capacity expansion.

Europe Humic Acid Market Trends

Europe leads the global humic acid market by value, supported by one of the most advanced regulatory frameworks for sustainable agriculture worldwide. The European Green Deal and the Farm to Fork Strategy establish legally binding targets to reduce synthetic fertilizer use by 20% and pesticide dependency by 50% by 2030, thereby generating sustained demand for bio-based soil amendments. Germany, France, Spain, and Italy collectively account for more than 60% of regional consumption, with Germany’s advanced precision farming infrastructure driving strong demand for premium, certified biostimulant products.

Regional innovation is led by companies such as Humintech GmbH and Biolchim S.p.A., supported by R&D investments aligned with EU Horizon Europe programs. The implementation of EU Regulation 2019/1009 has harmonized national standards across all 27 member states, lowering entry barriers and expanding the unified European market.

Asia Pacific Humic Acid Market Trends

Asia-Pacific represents the fastest-growing regional market for humic acid, driven by strong demand across China, India, Japan, and the expanding agricultural economies of ASEAN. China dominates the region as both the largest producer and consumer, supported by abundant leonardite and lignite reserves that provide significant raw material cost advantages. The presence of more than 70 million smallholder farms sustains large-scale demand for affordable soil enhancement inputs.

Japan contributes premium demand through its advanced precision horticulture and high-value crop sectors, favoring concentrated liquid and granular formulations for protected cultivation. India is the fastest-growing country market, supported by the Paramparagat Krishi Vikas Yojana (PKVY), expanding organic farmland, and national soil health initiatives promoted by the Indian Council of Agricultural Research. ASEAN nations are rapidly scaling export-oriented aquaculture and horticulture operations, reinforcing the region’s long-term manufacturing and supply chain competitiveness through 2033.

Competitive Landscape

The global humic acid market exhibits a moderately fragmented competitive structure, characterized by a combination of multinational chemical conglomerates and specialized regional producers. Leading players, including Humintech GmbH, The Andersons Inc., HGS BioScience, and BASF SE, leverage vertically integrated supply chains, robust R&D capabilities, and expansive distribution networks to sustain competitive advantages. Key product differentiators include humic compound purity levels, EU biostimulant certifications under EU FPR 2019/1009, precision dispersing granule delivery technologies, and regulatory compliance depth. Emerging competitive trends include strategic M&A-led consolidation, direct-to-farmer digital distribution models, and the bundling of humic acid with microbial consortia and seaweed extracts to deliver multi-function biostimulant packages addressing complex soil health demands across diverse agronomic systems.

Key Developments:

- August 2025: The Andersons Inc. introduced MicroMark® DG MAX, integrating humic acid with micronutrients in a dispersible granular format. This innovation enhances nutrient efficiency, supports soil health, and reflects a shift toward value-added, sustainable, and multifunctional humic acid-based fertilizer solutions in modern agriculture.

- October 2025: HGS BioScience acquired NutriAg Ltd. to expand its humic acid-based portfolio and strengthen its position in the biostimulants market. The deal enhances product integration, R&D capabilities, and North American reach, supporting the shift toward advanced, multi-functional agricultural biological solutions.

- December 2024: PT Bukit Asam Tbk (PTBA) teamed up with Universitas Gadjah Mada (UGM) to spearhead a research and development (R&D) initiative aimed at transforming low-calorific value coal into humic acid. The launch of the humic acid prototype took place at IUP Peranap in Indragiri Hulu, Riau. The duo plans to advance this prototype into a full-fledged pilot project.

Top Companies in the Humic Acid Market

- Humintech GmbH (Grevenbroich, Germany) is one of Europe's foremost humic acid manufacturers, supplying premium humate and biostimulant products to over 80 countries worldwide. Its vertically integrated model, spanning leonardite mining through finished biostimulant formulations, ensures consistent high-quality output, supported by strong internal R&D infrastructure and full compliance with EU FPR 2019/1009 biostimulant certification requirements.

- The Andersons Inc. (Maumee, Ohio, USA) leverages one of North America's broadest farm retail and distribution networks. The 2023 commercial launch of MicroMark DG dispersing granule technology established innovation leadership in precision humate delivery for large-scale row crop farming applications.

- HGS BioScience (Billings, Montana, USA) has rapidly emerged as a high-growth consolidator within the global humate market. Two strategic acquisitions completed in 2025, Menefee Mining Corp. and NutriAg Ltd., materially expanded both upstream raw material access from premium domestic deposits and downstream specialty biostimulant product development capabilities.

Companies Covered in Humic Acid Market

- Humintech GmbH

- The Andersons Inc.

- HGS BioScience

- BASF SE

- Biolchim S.p.A.

- Black Earth Humic LP

- Mineral Technologies Inc.

- Cifo SRL

- Arctech Inc.

- Zhengzhou Shengda Khumic Biotechnology

- Sikko Industries Ltd.

- Grow More Inc.

Frequently Asked Questions

The global Humic Acid market is valued at US$ 1,015.6 Mn in 2026 and is projected to reach US$ 2,082.1 Mn by 2033, registering a CAGR of 10.8% during the forecast period.

The primary demand drivers include the rising global adoption of sustainable and organic farming practices, increasing soil degradation affecting over 33% of global farmland according to the FAO, government mandates for bio-based fertilizer usage under the EU Green Deal, and the growing global organic food sector. The enforcement of biostimulant regulations under EU FPR 2019/1009 and the Farm to Fork Strategy are additional pivotal structural catalysts driving long-term market growth.

The powder form segment leads the global Humic Acid market with approximately 46% of total market share. Powdered humic acid is the preferred choice of large-scale row crop farmers for its cost efficiency, high active compound concentration, compatibility with NPK and micronutrient fertilizer blends, and suitability for automated spreading systems. According to the American Society of Agronomy, it enhances soil organic carbon levels by up to 25%.

Europe currently leads the global Humic Acid market by value, driven by strong regulatory support from the EU Green Deal, the Farm to Fork Strategy, and the formal biostimulant recognition under EU FPR 2019/1009. Germany, France, Spain, and Italy are the largest national consumer markets, collectively accounting for over 60% of European humic acid demand. Meanwhile, Asia-Pacific is the fastest-growing region during the forecast period.

Key commercial opportunities include the fast-growing aquaculture and animal feed segments, driven by the regulatory phase-out of antibiotic growth promoters under the EU Veterinary Medicinal Products Regulation and the U.S. Veterinary Feed Directive (VFD), and the EU biostimulant regulatory framework under EU Regulation 2019/1009, which creates a unified legally recognized commercial platform across 27 EU member states for premium humic acid biostimulant products.

Leading market participants include Humintech GmbH, The Andersons Inc., HGS BioScience, BASF SE, Biolchim S.p.A., Black Earth Humic LP, Mineral Technologies Inc., Cifo SRL, Arctech Inc., Zhengzhou Shengda Khumic Biotechnology Co. Ltd., Sikko Industries Ltd., and Grow More Inc. These companies compete based on product purity levels, biostimulant certifications, geographic distribution reach, and proprietary formulation technologies.