- Advanced Materials

- Hot Rolled Coil Steel Market

Hot Rolled Coil Steel Market Size, Share, and Growth Forecast 2026 - 2033

Hot Rolled Coil Steel Market by Product Type (Low Carbon Steel, Medium Carbon Steel, High Carbon Steel, Stainless Steel), by Thickness (≤ 3 mm, > 3 mm), by End Use (Construction & Infrastructure, Oil & Gas, Power & Energy, Automotive & Transportation, Industrial Equipment & Machinery, Shipbuilding & Marine, Pipes & Tubes, Home Appliances, Others), and Regional Analysis, 2026 - 2033

Hot Rolled Coil Steel Market Size and Trend Analysis

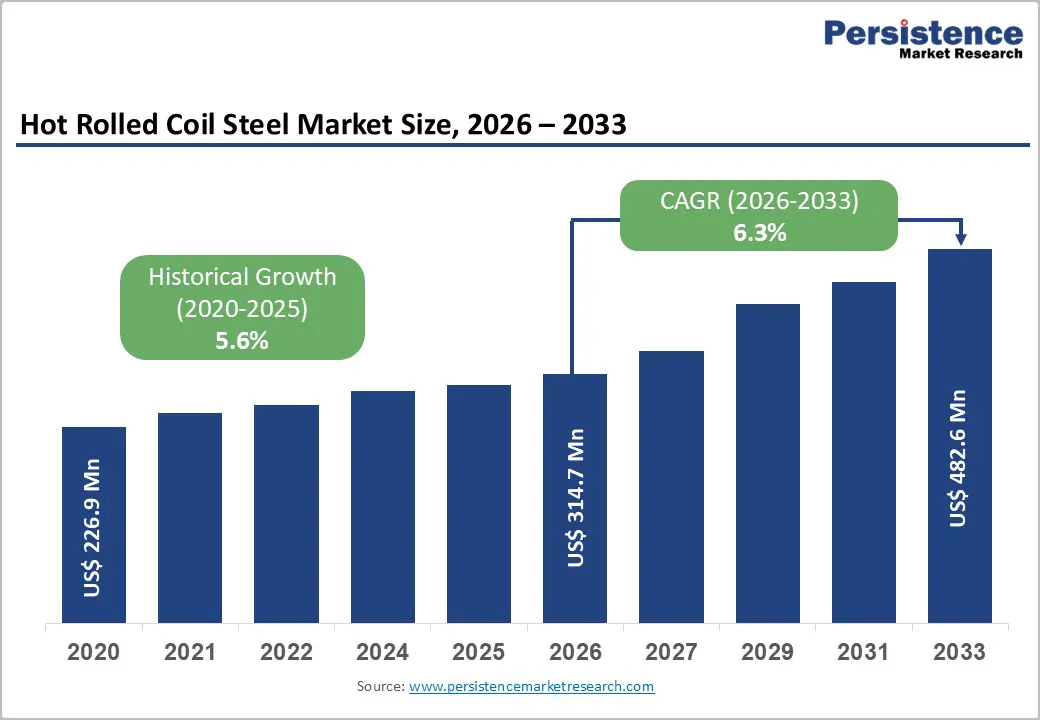

The global Hot Rolled Coil Steel market size is expected to be valued at US$ 314.7 billion in 2026 and likely to reach US$ 482.6 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

This robust growth trajectory is primarily fuelled by accelerating global infrastructure investment, rapid urbanization across emerging economies, and surging demand from the oil and gas, renewable energy, and automotive sectors. According to the World Steel Association (worldsteel), total world crude steel production reached 1,882.6 million tonnes (Mt) in 2024, underlining the foundational role of steel, and specifically Hot Rolled Coil (HRC) steel, in industrial supply chains. The widespread applicability of HRC steel across structural, pipe, automotive, and appliance manufacturing, combined with cost competitiveness versus alternative flat products, continues to sustain strong and diversified demand globally.

Key Industry Highlights:

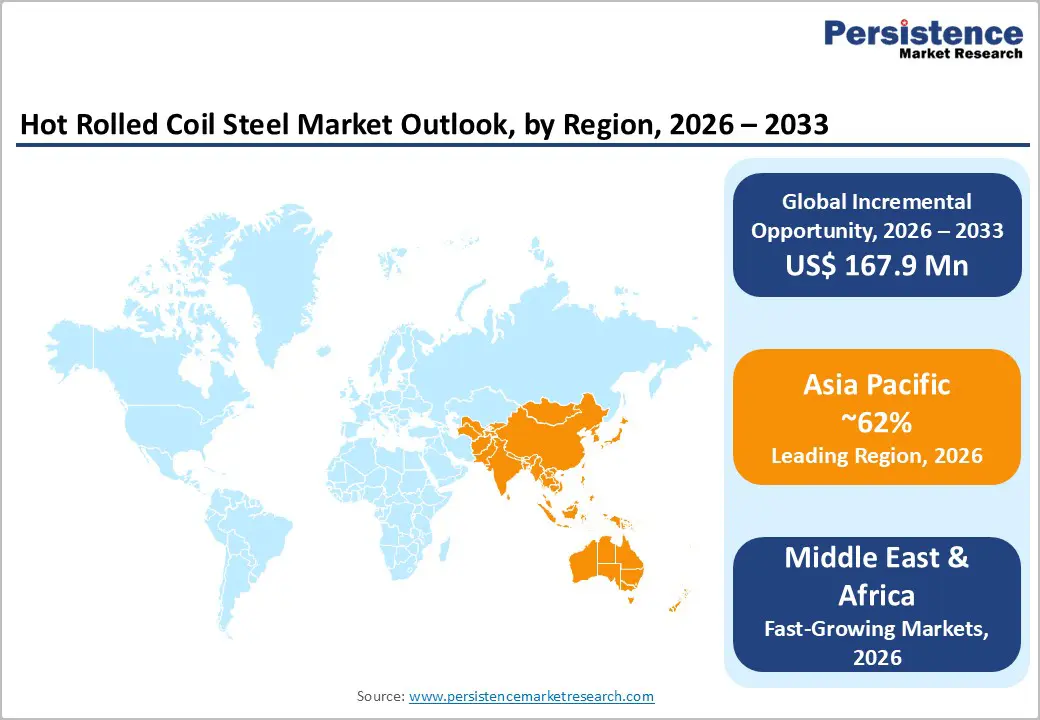

- Leading Region: Asia Pacific dominates the Hot Rolled Coil Steel market with over 62% share in 2025, underpinned by China's massive production base, India's 11.4% demand growth in 2024, and sustained infrastructure investment across ASEAN, Japan, and South Korea.

- Fastest Growing Region: Middle East & Africa is emerging as the fastest-growing regional market through 2033, fuelled by GCC Vision economic diversification programmes, expanding domestic steelmaking capacity, and large-scale energy and infrastructure projects driving HRC demand.

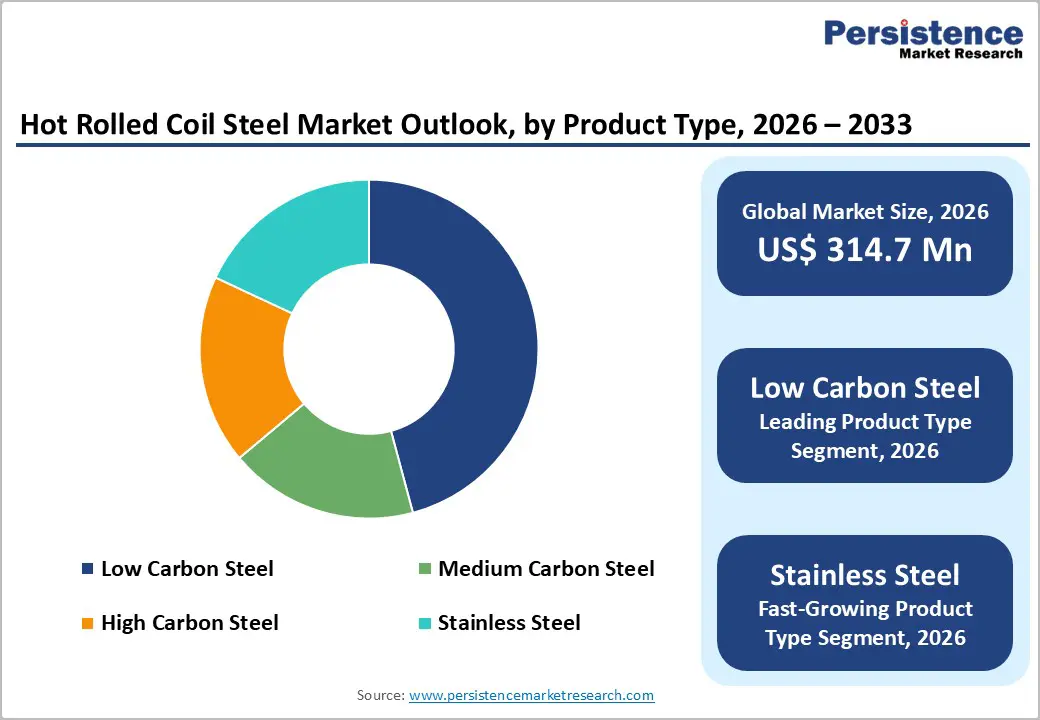

- Dominant Segment: Low Carbon Steel (mild steel) HRC holds approximately 47% market share in 2025, driven by its cost-efficiency, broad formability, and structural applicability across construction, automotive, pipes, and industrial equipment, the largest consuming end-use sectors globally.

- Fastest Growing Segment: Stainless Steel HRC is the fastest-growing product type segment, propelled by rising demand from corrosion-sensitive applications in food processing, chemical plants, oil and gas downstream, and architectural projects in Asia and the Middle East.

- Key Market Opportunity: Producers investing in hydrogen DRI and EAF-based low-carbon HRC output are positioned to capitalize on sustainability-driven premium procurement by automotive OEMs and infrastructure developers, unlocking significant value-added revenue streams through 2033.

| Key Insights | Details |

|---|---|

|

Hot Rolled Coil Steel Market Size (2026E) |

US$ 314.7 Billion |

|

Market Value Forecast (2033F) |

US$ 482.6 Billion |

|

Projected Growth CAGR (2026–2033) |

6.3% |

|

Historical Market Growth (2020–2025) |

5.6% |

DRO Analysis

Drivers - Robust Global Infrastructure Investment and Urbanization

Large-scale infrastructure investment remains one of the most powerful catalysts for HRC steel demand worldwide. In India, the government committed an outlay of INR 112 trillion (~US$ 1.35 trillion) for infrastructure development under initiatives such as Bharatmala, Gati Shakti, and the National Infrastructure Pipeline. The World Steel Association (worldsteel) confirms India registered 11.4% year-on-year steel demand growth in 2024 and forecasts a further 8.9% growth in 2025 and 9.1% in 2026, making it the fastest-growing major steel market globally.

In the United States, the Infrastructure Investment and Jobs Act drove an additional 6.8 million metric tonnes of incremental HRC demand in 2024 alone. Across the Asia Pacific, rapid urban expansion and rising construction orders, the UK Department for Business and Trade reported a 15.9% increase in total new construction orders in Q1 2024, collectively reinforcing sustained and growing demand for hot rolled coil steel throughout the forecast period.

Expanding Oil & Gas and Renewable Energy Sector Requirements

The oil and gas sector's dependence on HRC steel for pipelines, offshore drilling platforms, and high-pressure storage tanks constitutes a structural driver that remains resilient across commodity cycles. Simultaneously, the global energy transition is driving a new wave of HRC steel demand. According to World Steel's Short Range Outlook, steel demand for expanding global electricity grids is expected to double to approximately 20 million tonnes per year in the near term, with an estimated incremental demand of 40 million tonnes by end of the decade from renewable energy generation capacity expansion, encompassing wind turbine towers, solar mounting structures, and grid transmission infrastructure.

Furthermore, Nucor Corporation developed ultra-wide HRC coils (up to 2,400 mm) specifically for offshore wind tower bases in 2025, reflecting the specialized product innovation underway to serve this emerging high-growth end market. The convergence of capital expenditures for fossil fuels and renewable energy creates a broad, durable demand base for HRC steel over the forecast period.

Restraints - Raw Material Price Volatility and Input Cost Pressures

The Hot Rolled Coil Steel market remains highly exposed to fluctuations in iron ore and coking coal prices, the two primary raw material inputs. Iron ore prices exhibited significant volatility between 2022 and 2024, recording a pronounced declining trend from June 2024 through September 2024 before reversing upward through December 2024, according to data from India’s Ministry of Steel. Energy costs represent another persistent challenge, as in regions subject to stringent carbon regulations, manufacturing expenses increased by approximately 18% among affected producers. Approximately 35% of global steel producers reported raw material volatility as a primary operational constraint. These input cost pressures compress profit margins, complicate long-term pricing strategies, and may deter capacity investment, particularly among smaller and mid-tier producers, thereby acting as a meaningful restraint on market expansion.

Carbon Emission Regulations and Green Transition Compliance Costs

Tightening environmental regulations across key consuming regions pose a structural cost challenge for traditional blast-furnace-based HRC steel producers. The European Union's Carbon Border Adjustment Mechanism (CBAM) is progressively imposing carbon levies on imported steel, compelling overseas suppliers to either absorb costs or invest heavily in decarbonization. In Germany alone, €4.7 billion was earmarked for hydrogen-powered blast furnace construction, which substantially raises per-tonne production costs in the transition period. With over 59% of India's crude steel capacity still relying on emissions-intensive BF-BOF processes (emitting 3.83 tCO2 per tonne of crude steel), the compliance investment required is considerable and could constrain near-term capacity additions in developing regions, slowing potential market supply expansion.

Opportunities - Green Steel and Low-Carbon HRC Product Development

The rapid acceleration of global sustainability mandates is creating a significant first-mover opportunity for HRC producers who invest early in low-carbon steelmaking technologies. Over 36% of global steel mills had already incorporated electric arc furnaces (EAFs) by 2024, with scrap-based EAF steel contributing 43% of North American HRC supply. China Baowu Steel Group launched a hydrogen-based steelmaking pilot at its Baoshan facility in 2025, producing 300,000 metric tonnes of green hot-rolled coils during the pilot phase.

India's National Green Hydrogen Mission has allocated INR455 crore to the steel sector for green hydrogen projects through 2029–30, while Japan's government committed ¥1.3 trillion for AI-integrated rolling lines. As end-users, particularly automotive OEMs and infrastructure developers, increasingly embed low-carbon procurement criteria into supply chains, HRC producers offering certified green steel products will command premium pricing and expand addressable markets substantially through 2033.

Stainless Steel HRC Demand from Emerging Industrial & Specialty Applications

Stainless Steel HRC is the fastest-growing product type segment in the market, driven by increasing adoption in food processing, chemical processing, oil and gas downstream, and architectural applications that demand superior corrosion resistance and hygiene standards. The segment's growth is further reinforced by India's Production-Linked Incentive (PLI) 1.1 scheme for specialty steel, which offers producers incentives of 3–4% for investing in high-value grades.

Meanwhile, as ASEAN nations accelerate industrialization, Vietnam and Indonesia have expanded cold and hot rolling capacity specifically to serve regional downstream electronics and automotive assembly, demand for corrosion-resistant and high-purity HRC grades is structurally rising. India's domestic steel demand is forecast to grow from 136 million tonnes in 2024 to between 221–275 million tonnes by 2034, with an increasingly high-grade mix, creating a compelling growth runway for stainless steel HRC producers through 2033.

Category-wise Analysis

Product Type Insights

Low Carbon Steel (mild steel) is the dominant segment within the Hot Rolled Coil Steel market by product type, commanding approximately 47% of global HRC market share in 2025. This leadership stems from low carbon steel's unmatched combination of formability, weldability, cost-effectiveness, and broad applicability across construction, automotive, pipe manufacturing, and industrial equipment sectors. The mild steel (low carbon) HRC grade has retained dominance due to its widespread use as a structural input in bridges, highways, and commercial buildings globally. The lower alloy content reduces production costs relative to medium and high carbon grades, enabling competitive pricing in price-sensitive emerging markets. Low carbon steel HRC also serves as the primary feedstock for galvanizing, cold rolling, and pipe manufacturing downstream, further cementing its leading position in the global supply chain.

Thickness Insights

HRC steel with a thickness greater than 3 mm (> 3 mm) constitutes the leading segment by thickness, holding over 65% of global HRC market share in 2025. This dominant position reflects the extensive deployment of thick-gauge HRC in load-bearing, structural, and heavy-duty industrial applications, including beams, columns, heavy machinery frames, shipbuilding, and construction reinforcements, where tensile and yield strength requirements preclude thinner grades. Thick-gauge HRC steel's superior mechanical properties make it indispensable in pipeline manufacturing for the oil and gas sector, offshore platforms, and wind turbine tower bases. However, it is worth noting that the ≤ 3 mm segment is the fastest-growing thickness category, driven by growing demand from automotive body panels and lightweight industrial containers where formability is critical.

End-user Insights

Construction & Infrastructure is the leading end-use segment, accounting for approximately 42% of global HRC steel market share in 2025. This dominance is underpinned by massive multi-year infrastructure programmes in Asia, North America, and Europe. The World Steel Association estimates that renewable energy grid expansion alone will require an incremental 40 million tonnes of steel by end of the decade. Rapid urbanization, particularly in China, India, and Southeast Asia, is driving relentless demand for structural steel, reinforced concrete, and pipeline networks. In India, the Pradhan Mantri Awaas Yojana-Gramin (PMAY-G) programme aims to construct 49.5 million houses by March 2029, thereby boosting HRC demand. The construction sector's structural centrality in the value chain positions it as the primary end-use driver throughout the 2026–2033 forecast horizon. Fastest growth is expected from the Power & Energy segment, reflecting the global energy transition's steel intensity.

Regional Insights

Asia Pacific Hot Rolled Coil Steel Market Trends and Insights

Asia Pacific is the undisputed leading region in the global Hot Rolled Coil Steel market, accounting for over 62–63% of total global demand in 2025, driven by China, India, Japan, and South Korea. China remains the world's largest crude steel producer with 1,005.1 million tonnes in 2024 (per worldsteel), though domestic demand has moderated as the property sector contracts. India, now the second-largest global steel producer at 149.4 Mt in 2024, is simultaneously the fastest-growing major consumption market, with the World Steel Association projecting steel demand growth of 8.9% in 2025 and 9.1% in 2026. India's ambitious National Steel Policy targets crude steel capacity of 300 million tonnes by 2030.

Japan's public-private partnerships committed ¥1.3 trillion to AI-integrated rolling lines enhancing HRC quality, while South Korea's POSCO and JFE Steel Corporation continue investing in advanced high-strength steel grades for automotive and marine applications. In Southeast Asia, Vietnam and Indonesia are scaling HRC rolling capacity to capture growing downstream demand from electronics assembly and automotive manufacturing, extending the region's dominance across the forecast period. The Middle East & Africa sub-region is the fastest-growing globally in the forecast period, driven by GCC Vision programmes and rising domestic sources of steel production, reducing import dependency.

North America Hot Rolled Coil Steel Market Trends and Insights

North America represents the second-largest regional market, with the United States dominating at over 72% of regional revenue share in 2024. The U.S. domestic HRC steel market has been fundamentally reshaped by the Infrastructure Investment and Jobs Act, which drove an incremental 6.8 million metric tonnes of HRC demand in 2024 from bridge, highway, and railway construction. The automotive sector consumed approximately 10.5 million metric tonnes of HRC steel in 2024 across the U.S., supported by a structural shift toward electric vehicle production. Scrap-based EAF production contributed 43% of North American HRC supply in 2024, reinforcing the region's sustainability credentials.

Regulatory momentum continued with Representative Ro Khanna's Modern Steel Act proposing US$ 10 billion in grants and low-interest loans for new steel mills and facility upgrades in August 2024. A landmark conditional approval was granted in May 2025 for Nippon Steel's US$ 14.1 billion acquisition of U.S. Steel, targeting facility upgrades in Indiana and Pennsylvania and construction of a new steel mill, further underpinning North American HRC capacity investment. Nucor Corporation led domestic producers with 20.7 million metric tonnes of U.S. steel output in 2024, maintaining market leadership.

Europe Hot Rolled Coil Steel Market Trends and Insights

Europe's Hot Rolled Coil Steel market is navigating a complex transition, balancing near-term demand recovery with long-term decarbonization imperatives. The EU (27) recorded crude steel production of 9.6 million tonnes in December 2024, up 7.2% year-on-year (worldsteel), signalling a gradual recovery from 2023 lows. Germany, the continent's largest steel economy, has allocated €4.7 billion for hydrogen-powered DRI facilities, with ThyssenKrupp's Duisburg plant designed to cut HRC-related CO2 emissions by up to 64% versus conventional blast furnace routes, positioning Germany as a global leader in green steel manufacturing.

The EU Carbon Border Adjustment Mechanism (CBAM) is progressively raising the cost of imported steel, incentivising regional sourcing of low-carbon HRC among European automotive and construction OEMs. The automotive sector, particularly the electric vehicle transition, is a key demand driver across Germany, France, Spain, and the U.K., as EV body structures require high-strength HRC grades. Worldsteel forecasts EU steel demand to recover by 5.3% in 2025 and 4.6% in Germany specifically by 2026, reflecting improving conditions across both construction and manufacturing end markets after consecutive years of contraction.

Competitive Landscape

The global ot Rolled Coil (HRC) steel market is moderately consolidated, with a limited number of large producers accounting for a significant share of total output, supported by strong regional players in Asia and Europe. Market structure is characterized by high capital intensity, integrated value chains, and economies of scale, which create barriers to entry and reinforce the dominance of established manufacturers.

Key business strategies are centered on vertical integration from raw materials to finished coils, development of advanced high-strength steel (AHSS), and increasing adoption of electric arc furnace (EAF) routes. Companies are prioritizing decarbonization through investments in hydrogen-based direct reduction and carbon-certified “green steel” offerings. Additionally, digitalization, including AI-driven quality control and smart manufacturing, is being leveraged to enhance operational efficiency and product consistency. Strategic partnerships, capacity expansions, and sustainability-focused product differentiation are enabling players to secure long-term contracts and premium pricing from environmentally conscious end users.

Key Developments:

- May 2025: Nippon Steel received conditional approval from the U.S. government for its US$ 14.1 billion acquisition of U.S. Steel, with commitments to upgrade facilities in Indiana and Pennsylvania and construct a new greenfield steel mill.

- January 2026: Shyam Metalics and Energy Limited completed construction of a stainless steel hot rolled coil facility at its Sambalpur mill, enhancing downstream integration and enabling production of 200 and 400 series coils using captive raw materials.

Companies Covered in Hot Rolled Coil Steel Market

- ArcelorMittal

- Baowu Steel Group (China Baowu Steel Group Corporation Limited)

- Benxi Steel Group

- Hesteel Group

- JFE Steel Corporation

- Nippon Steel Corporation

- Nucor Corporation

- POSCO (Pohang Iron and Steel Company)

- Shougang Group

- Tata Steel

- Jindal Steel & Power Limited (JSPL)

- Gerdau S.A.

- SAIL (Steel Authority of India Limited)

- Ansteel Group Corporation

- HBIS Group

- JSW Steel Limited

- ThyssenKrupp AG

- Hyundai Steel

- Shagang Group

- United States Steel Corporation (U.S. Steel)

Frequently Asked Questions

The global Hot Rolled Coil Steel market is valued at US$ 314.7 billion in 2026 and is projected to reach US$ 482.6 billion by 2033 at a CAGR of 6.3%.

Demand is driven by infrastructure investments, rapid urbanization, energy sector expansion, and rising automotive production.

Asia Pacific leads the market with over 62% share due to strong steel production and infrastructure growth in China, India, and Southeast Asia.

The key opportunity lies in the development of low-carbon and green steel using hydrogen-based and EAF technologies.

Key players include China Baowu Steel Group, ArcelorMittal, Nippon Steel Corporation, POSCO, JFE Steel, Nucor, Tata Steel, JSW Steel, SAIL, and Gerdau.