- Home Care & Utilities

- Honeycomb Paperboard Packaging Market

Honeycomb Paperboard Packaging Market Size, Share, and Growth Forecast, 2026 – 2033

Honeycomb Paperboard Packaging Market by Material (Kraft Paper, Specialty Coated Paper, Others), Packaging type (Sheets, Boxes & Containers, Others), Application (Automotive, Consumer Goods, Others), and Regional Analysis 2026 – 2033

Honeycomb Paperboard Packaging Market Size and Trends Analysis

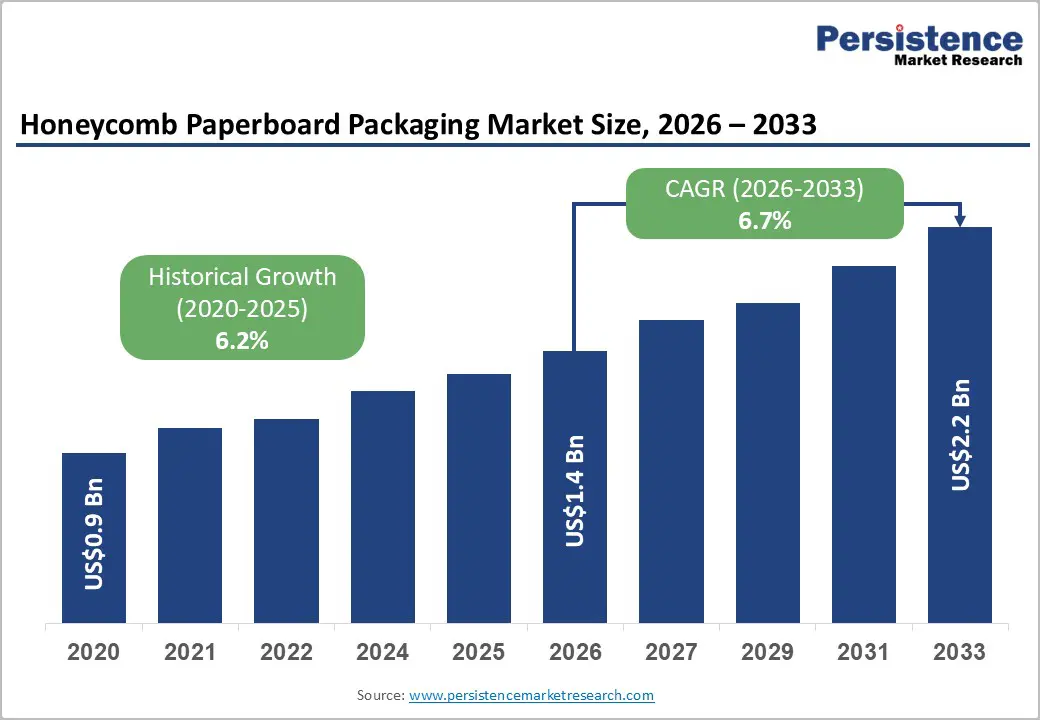

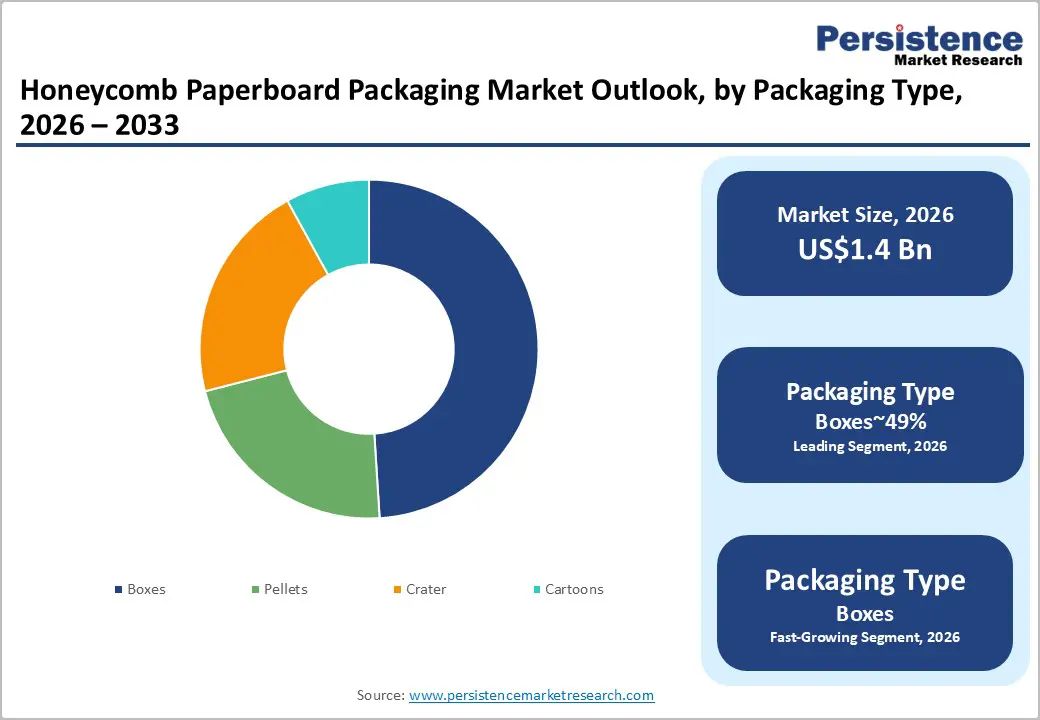

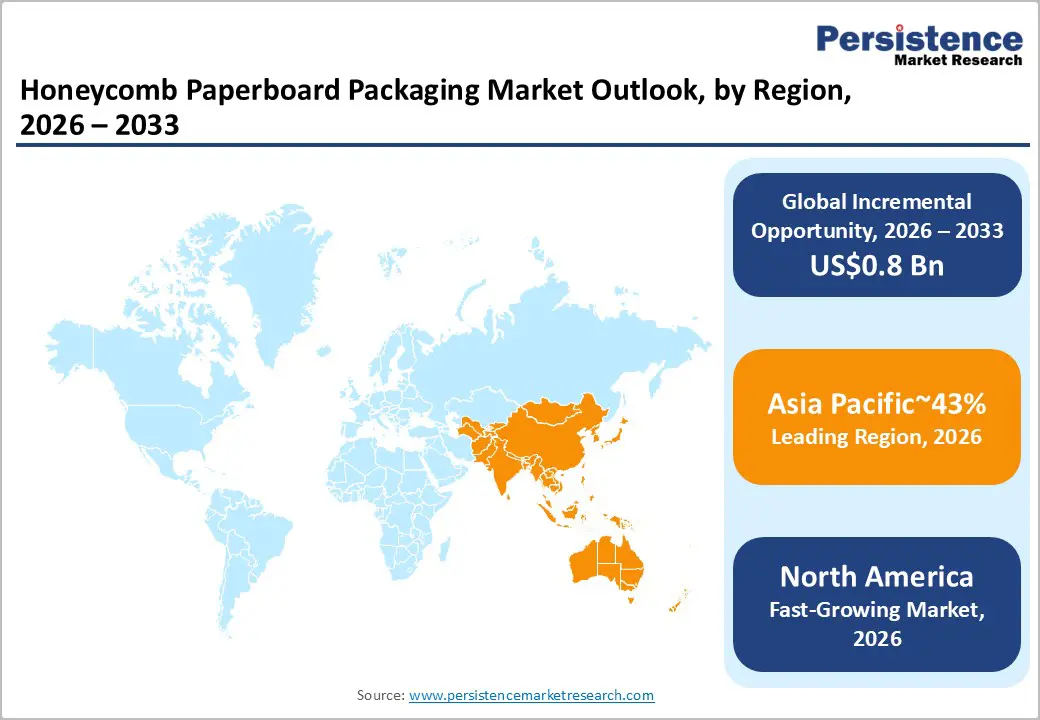

The global honeycomb paperboard packaging market size is likely to be valued at US$1.4 billion in 2026 and is expected to reach US$2.2 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033, driven by sustainable material adoption across global supply chains.

Manufacturers are anticipated to prioritize biodegradable configurations to optimize corporate carbon footprint metrics. Structural rigidity engineering is likely to displace traditional synthetic polymers within protective transit applications. Technological refinements in core density and linerboard integration are enabling broader adoption across high value automotive and consumer electronics shipments, which is expected to sustain mid single digit growth. Packaging optimization is expected to reduce dimensional logistics costs while ensuring premium product integrity.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to lead, accounting for approximately 43% share in 2026, supported by robust regional manufacturing ecosystems, expanding export volumes, and accelerating industrial modernization policies.

- Fastest Growing Region: North America is anticipated to grow the fastest, driven by aggressive e-commerce fulfillment expansion, stringent plastic reduction legislation, and localized supply chain resilience investments.

- Leading Material Type: Kraft paper is expected to lead, accounting for approximately 52% share in 2026, anchored by superior tensile strength, ubiquitous global availability, and optimal cost-to-performance recycling profiles.

- Leading Packaging Type: Boxes are projected to dominate, holding approximately 49% share in 2026, driven by universal shipping standardization, exceptional vertical stacking capabilities, and widespread automated handling compatibility.

| Key Insights | Details |

|---|---|

| Honeycomb Paperboard Packaging Market Size (2026E) | US$1.4 Bn |

| Market Value Forecast (2033F) | US$2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – E-commerce Logistics Intensification Driving Structural Shift toward Honeycomb Packaging

The rapid growth of digital retail is driving heightened demand for durable, impact-resistant transit packaging solutions. Distribution systems increasingly rely on materials that can withstand repeated handling and minimize product damage throughout the shipping process. Honeycomb paperboard offers enhanced cushioning performance, effectively absorbing multidirectional compression during transit. This capability helps reduce product returns and lowers reverse logistics costs across fulfillment networks. Its lightweight design also improves dimensional efficiency, positively impacting freight costs within carrier systems. The shift away from expanded polystyrene is gaining momentum due to stricter environmental regulations promoting recyclable alternatives. Engineered honeycomb packaging meets these sustainability requirements while maintaining strong structural performance over long-distance transportation. Collectively, these factors are elevating the role of paper-based structural packaging in high-volume e-commerce logistics.

Automated fulfillment environments increasingly require standardized packaging formats compatible with high-speed machinery operations. Honeycomb boards provide consistent rigidity, enabling efficient erecting, stacking, and sealing within automated lines. Retailers prioritize scalable packaging inputs capable of accommodating seasonal fluctuations in order volumes. Structural consistency enhances throughput efficiency while minimizing operational disruptions across distribution centers. Recyclable material composition strengthens brand perception during consumer-facing unboxing experiences. Advances in paperboard engineering improve puncture resistance under complex routing and variable load conditions. These attributes support inventory protection across fragmented last-mile delivery networks with rising service expectations. Consequently, honeycomb packaging integrates into both operational efficiency frameworks and sustainability-driven procurement strategies.

Aggressive Lightweighting Initiatives Optimizing Global Freight Economics

Escalating global transportation costs are expected to force enterprise shippers to minimize deadweight across logistics networks. Cellular geometric structures are projected to deliver maximum compressive strength utilizing minimal raw material mass. Smurfit Kappa with Hexacomb is anticipated to lower aviation and maritime freight expenditures through structural lightweighting. Freight optimization strategies are likely to demand high-strength-to-weight ratio materials to maximize volumetric payload efficiency. DS Smith with Honeycomb Cellpad is positioned to enhance palletized load stability without adding excessive gross tonnage. Reduced tare weight is expected to yield substantial financial savings across high-frequency intermodal shipping operations. Logistical efficiency metrics are anticipated to directly correlate with advanced honeycomb paperboard integration levels.

Fuel surcharge volatility is projected to drive continuous engineering investments in lightweight protective transit solutions. Supply chain architects are expected to replace heavy timber crating with advanced multi-layered paperboard alternatives. Packaging Corporation of America with Hexacomb Board is anticipated to facilitate seamless heavy-duty transit transitions. Ergonomic handling improvements are likely to reduce warehouse workplace injury rates through lighter material manipulation. Axxor with Axxor Core is positioned to improve manual loading velocities across decentralized distribution facilities. Structural optimization algorithms are expected to precisely calibrate cellular density to specific payload mass requirements. Intelligent material deployment is anticipated to maximize logistical yield while ensuring uncompromised asset protection.

Barrier Analysis – Structural Degradation Risk under High Moisture Exposure

Inherent hygroscopic material properties are expected to compromise structural integrity during prolonged high-humidity ambient exposure. Moisture absorption is projected to degrade cellular compressive strength and risk catastrophic palletized load failure. Honicel with Honicel Paper Core is anticipated to face adoption friction across unregulated tropical supply chain routes. Capillary action within unsealed paper edges is likely to draw ambient condensation into the core architecture. Dufaylite with Ultraboard is positioned to encounter deployment barriers within non-climate-controlled maritime shipping containers. Delamination of facing papers is expected to weaken crucial structural bonds under fluctuating dew point conditions. Environmental vulnerability is anticipated to restrict total addressable market penetration within the maritime and agricultural sectors.

Waterproofing chemical treatments are projected to negatively impact the fundamental recyclability profile of paperboard packaging. Converters are expected to struggle to balance moisture resistance requirements with strict environmental degradation standards. Lsquare Eco-Products with Lsquare Honeycomb Box is anticipated to navigate complex technical tradeoffs during product development. Secondary protective wrapping is likely to introduce unwanted plastic film back into the sustainable logistics loop. Corint Group with Corint Core is positioned to face pricing pressure when competing against naturally waterproof polymer alternatives. Perceived reliability deficits are expected to deter risk-averse procurement managers handling high-value sensitive equipment. Overcoming inherent cellulose moisture susceptibility is anticipated to demand significant ongoing chemical engineering capital investments.

Performance Perception Gaps Limiting Paper-Based Honeycomb Adoption

Persistent perception gaps continue to constrain the adoption of paper-based honeycomb across demanding industrial applications. End-use buyers often associate plastic and foam variants with superior durability under dynamic loading conditions. This bias persists despite comparable shock absorption performance demonstrated by engineered paperboard configurations. Risk-averse procurement practices reinforce reliance on incumbent materials within automotive and heavy logistics environments. Qualification protocols frequently prioritize historical material performance over emerging sustainability-aligned alternatives. Such inertia slows substitution cycles, particularly where failure risk carries high operational consequences. Regulatory encouragement for recyclable materials remains insufficient to fully offset entrenched performance perceptions. Consequently, paper-based solutions face delayed penetration within high-specification protective packaging segments.

Bridging these perception gaps requires extensive validation through application-specific testing and standardized performance benchmarks. Suppliers must demonstrate repeatable outcomes under real-world stress conditions to gain procurement confidence. Independent certification and peer-reviewed case studies become critical for influencing material selection frameworks. Without validated field data, buyers continue to favor legacy materials with established reliability records. This dynamic restricts access to premium segments within automotive and industrial logistics packaging. Cost advantages and sustainability benefits remain secondary to perceived operational risk mitigation priorities. As a result, market share expansion for paper-based honeycomb remains constrained by trust deficits. Overcoming this barrier necessitates systematic evidence generation across diverse high-impact use scenarios.

Opportunity Analysis – Specialized Protective Enclosures for EV Battery Transport

Explosive global electric vehicle production is expected to necessitate highly specialized dangerous goods transit packaging. Heavy lithium-ion battery modules are projected to demand rigorous impact resistance to prevent catastrophic thermal runaway. Smurfit Kappa with Hexacomb is anticipated to engineer proprietary multi-layered structural enclosures for critical automotive components. Cellular energy dissipation properties are likely to absorb kinetic transit shocks better than rigid wooden crating. DS Smith with Honeycomb Cellpad is positioned to capture automotive OEM contracts through UN-certified paperboard transit solutions. Die-cut core configurations are expected to immobilize sensitive battery cells precisely during complex international intermodal journeys. Sustainable automotive logistics are anticipated to represent a massive structural growth vector for advanced paperboard converters.

Automotive regulatory agencies are projected to mandate stringent vibration testing for all battery supply chain packaging. Advanced engineered paperboard is expected to pass critical drop-test compliance protocols while reducing gross vehicle weight. Packaging Corporation of America, with Hexacomb Board, is anticipated to develop customized platform solutions for tier-one suppliers. Elimination of splintering wooden crates is likely to drastically improve assembly line safety and ergonomic handling. Axxor with Axxor Core is positioned to integrate seamlessly into automated robotic automotive component unpacking workflows. End-of-life battery recycling logistics are expected to utilize single-use structural paperboard to prevent hazardous material contamination. Closed-loop automotive manufacturing ecosystems are anticipated to heavily leverage sustainable structural materials.

Expansion of Honeycomb Panels into Furniture and Interior Structural Applications

Engineered honeycomb panels are increasingly penetrating furniture and interior construction, requiring lightweight structural performance. Applications include ready-to-assemble furniture, partition systems, and load-bearing interior components. Paper-based cores offer favorable acoustical dampening alongside high stiffness-to-weight characteristics. These attributes align with the rising demand for modular, flat pack, and space-efficient interior solutions. Ease of machining and surface finishing support integration into diverse architectural and furniture designs. Material recyclability further strengthens alignment with sustainability standards across interior construction value chains. This transition expands functional relevance beyond protective packaging into semi-structural end-use applications. Consequently, honeycomb paperboard evolves into a versatile material platform within lightweight construction ecosystems.

Manufacturers are advancing into furniture segments through co-development with original equipment manufacturers. Customization of panel thickness, core geometry, and edge banding enhances application-specific performance. Integration within interior systems requires consistency in load distribution and dimensional stability. These requirements drive material engineering refinements across production and converting processes. Diversification into non-packaging applications broadens revenue streams and reduces dependence on logistics cycles. Supply chains increasingly adapt to serve both packaging and interior construction demand profiles. This convergence strengthens economies of scale while improving asset utilization across manufacturing operations. As adoption expands, honeycomb panels gain positioning within modular construction and interior systems markets.

Category–wise Analysis

Material Type Insights

Kraft paper is expected to lead, accounting for approximately 52% share in 2026, underpinned by its entrenched role in structural core formation and industrial packaging workflows. Adoption remains anchored by high tensile strength, recyclability, and cost-efficient raw material sourcing across logistics-intensive sectors. Smurfit Kappa with Hexacomb and DS Smith with Honeycomb Cellpad reinforce large-scale deployment across automated fulfillment and transport networks. Honicel Nederland B.V., with CompactCell Kraft and Helios Packaging with HoneyLock Kraft, further embeds kraft-based systems within OEM-aligned packaging specifications. Continuous-core forming and high-speed gluing technologies enhance throughput and structural consistency across production lines.

Specialty coated paper is expected to be the fastest-growing segment in the Honeycomb Paperboard Packaging Market, driven by increasing demand for barrier-enhanced and performance-optimized packaging solutions. Growth is catalyzed by coating technologies enabling moisture resistance, surface protection, and print-ready capabilities within single-material structures. Packaging Corporation of America, with Hexacomb Board and Axxor with Axxor Core, is advancing coated formats for sensitive and high-value shipments. EcoSense Coated Panel by Axxor and MultiGuard Coated Box by Lsquare Eco Products demonstrate integration of coatings within continuous forming systems. These innovations improve durability and branding functionality while maintaining recyclability advantages.

Packaging Type Insights

Boxes are expected to dominate, accounting for approximately 49% share in 2026, anchored by universal shipping standardization and widespread automated handling compatibility. Standardized cuboid geometries are projected to maximize volumetric efficiency across complex international intermodal shipping containers. Honicel with Honicel Paper Core is anticipated to supply high-compression structural boxes for heavy industrial machinery transport. Exceptional vertical load-bearing capabilities are likely to prevent lower-tier crushing during dense warehouse pallet stacking operations. Dufaylite with Ultraboard is positioned to deliver highly resilient transit cases for sensitive aerospace and automotive components. Integrated shock absorption is expected to eliminate the need for excessive secondary internal void-fill materials. Seamless integration into existing automated erecting machinery is anticipated to secure long-term enterprise-level procurement contracts.

Boxes are anticipated to be the fastest-growing segment, driven by aggressive e-commerce fulfillment expansion and direct-to-consumer digital retail models. Lightweight structural enclosures are projected to optimize dimensional freight costs for high-volume residential parcel delivery networks. Lsquare Eco-Products with Lsquare Honeycomb Box is anticipated to capture the rising demand for sustainable, plastic-free unboxing experiences. Custom-engineered internal cellular blocking is likely to securely immobilize fragile consumer goods during violent last-mile transit. Corint Group with Corint Core is positioned to support omnichannel retailers with scalable, flat-packed structural shipping solutions. Accelerated digital commerce penetration is expected to necessitate continuous upgrades to parcel impact resistance parameters. Sustainable structural boxes are anticipated to become the definitive standard for premium modern retail fulfillment.

Regional Insights

Asia Pacific Honeycomb Paperboard Packaging Market Trends

Asia Pacific is expected to remain the leading regional market, accounting for approximately 43% share in 2026, supported by robust regional manufacturing ecosystems and expanding export volumes. Massive industrial electronics production is projected to require immense quantities of sustainable, protective transit packaging. Smurfit Kappa with Hexacomb is anticipated to capitalize on regional supply chain modernization through localized structural manufacturing facilities. Aggressive state-sponsored plastic reduction policies are likely to force rapid enterprise transitions toward biodegradable cellulose architectures. DS Smith with Honeycomb Cellpad is positioned to support expanding cross-border e-commerce networks originating from Asian manufacturing hubs. Rapidly urbanizing consumer bases are expected to exponentially increase digital retail parcel delivery volumes. Regional logistics networks are anticipated to heavily leverage cellular lightweighting to optimize dense urban freight economics.

China is expected to serve as the structural anchor driving continuous Asia Pacific market momentum and technological scaling. Massive internal manufacturing capabilities are projected to lower the cost barrier for advanced paperboard conversion machinery. Packaging Corporation of America, with Hexacomb Board, is anticipated to navigate complex Chinese regulatory landscapes through strategic local partnerships. Dominant consumer technology exporters are likely to standardize honeycomb transit protection to comply with strict international sustainability mandates. Axxor with Axxor Core is positioned to capture immense volume through deep integration into Chinese electric vehicle supply chains. Rapidly advancing domestic material science is expected to continuously improve regional cellular compressive strength characteristics. Centralized industrial planning is anticipated to permanently establish biodegradable structural packaging across Asian trade networks.

North America Honeycomb Paperboard Packaging Market Trends

North America is expected to register the fastest growth trajectory, approximating its respective share, as aggressive e-commerce fulfillment expansion dictates advanced protective logistics. Stringent corporate ESG mandates are projected to aggressively penalize single-use plastic consumption across enterprise supply chains. Honicel with Honicel Paper Core is anticipated to capture lucrative procurement contracts through highly measurable carbon reduction profiles. Heavy investments in localized supply chain resilience are likely to drive demand for domestically sourced structural packaging. Dufaylite with Ultraboard is positioned to support regional nearshoring initiatives with scalable, high-performance transit protection solutions. Exploding direct-to-consumer retail models are expected to necessitate robust parcel impact resistance for complex transcontinental shipping. Advanced automated warehousing ecosystems are anticipated to seamlessly integrate standardized honeycomb materials for rapid throughput.

The U.S. is expected to architect the fundamental regulatory and commercial trajectory of the North American landscape. Massive domestic logistics networks are projected to financially incentivize structural lightweighting to combat volatile transportation fuel surcharges. Lsquare Eco-Products with Lsquare Honeycomb Box is anticipated to leverage American consumer preferences for transparently sustainable unboxing experiences. Strict state-level extended producer responsibility legislation is likely to aggressively tax non-recyclable corporate packaging waste streams. Corint Group with Corint Core is positioned to supply specialized protective configurations for expanding domestic aerospace manufacturing sectors. American automotive OEMs are expected to standardize cellular transit protection for heavy decentralized EV battery distribution.

Europe Honeycomb Paperboard Packaging Market Trends

Europe is expected to remain a mature and structurally stable regional market, approximating its respective share, with demand primarily anchored in aggressive circular economy legislation. Stricter environmental compliance frameworks are projected to permanently eliminate fossil-based transit packaging across the continental trade bloc. Smurfit Kappa with Hexacomb is anticipated to maintain formidable regional dominance through a deeply established sustainable manufacturing infrastructure. Sophisticated recycling ecosystems are likely to ensure highly efficient recovery and continuous remanufacturing of cellular paperboard assets. DS Smith with Honeycomb Cellpad is positioned to lead European premiumization trends through highly engineered, bespoke protective architectures. High-value automotive and industrial machinery exports are expected to rely heavily on advanced structural transit safeguards. Pan-European logistical harmonization is anticipated to sustain continuous, predictable demand for standardized honeycomb solutions.

Germany is expected to dictate the premium technological standards and regulatory compliance protocols shaping the European market. Uncompromising industrial engineering requirements are projected to demand the highest achievable cellular compressive strength and structural reliability. Packaging Corporation of America with Hexacomb Board is anticipated to secure lucrative contracts within the massive German automotive sector. German legislative mandates are likely to continuously push the boundary of mandatory supply chain material recyclability. Axxor with Axxor Core is positioned to support complex German heavy machinery exports with precision-engineered protective transit kits. German industrial leadership is anticipated to anchor the absolute premium tier of global structural packaging innovation.

Competitive Landscape

The global honeycomb paperboard packaging market is moderately consolidated, with leadership concentrated among integrated global suppliers such as Smurfit Kappa, DS Smith, Packaging Corporation of America, and Axxor. These players shape material standards, procurement frameworks, and qualification thresholds through vertically integrated pulp sourcing and engineered conversion capabilities. Their control over continuous cellular manufacturing and testing infrastructure anchors enterprise adoption across automotive, electronics, and industrial logistics workflows. Leaders differentiate through proprietary cushioning design, impact validation, and automated-line compatibility, while regional firms compete on responsiveness and localized supply. Industry behavior indicates sustained consolidation through targeted acquisitions and expansion of regional converting assets, alongside a shift toward consultative packaging design.

Competitive positioning favors standardized core-forming platforms combined with flexible, short-run conversion suited to fluctuating demand cycles. Regional players such as MAC PACK and YOJ Pack-Kraft gain relevance by embedding production close to automotive and consumer goods manufacturing clusters. Their influence stems from logistics-aware design capabilities, rapid turnaround, and alignment with localized procurement strategies. These firms differentiate through proximity advantages and cost-efficient raw material sourcing rather than large-scale integration. Industry dynamics reflect increasing decentralization of packaging production, with distributed mini-mill models and modular converting lines supporting resilient supply chains and reduced transit dependencies.

Key Industry Developments:

- In January 2026, Mondi secured nine WorldStar Awards for breakthrough packaging innovations. These awards highlight the industry's shift toward high-barrier paper mailers and transit protection, validating the commercial viability of "Sustainable by Design" honeycomb structures.

- In February 2026, Smurfit Westrock unveiled a medium-term plan to accelerate growth through specialized clinical packaging. By targeting high-margin sectors such as healthcare with dedicated honeycomb-insulated facilities, the company is diversifying away from commodity-grade shipping materials.

Companies Covered in Honeycomb Paperboard Packaging Market

- Smurfit Kappa

- DS Smith

- Packaging Corporation of America

- Axxor

- Sonoco Products Company

- Sealed Air Corporation

- Mondi Group

- Honicel Nederland B.V.

- Eltete TPM

- Dufaylite

- Cascades Inc.

- Tricor Packaging & Logistics

- Nidaplast

- Grigeo

- Lsquare Eco Products

- Greencore Packaging

Frequently Asked Questions

The global honeycomb paperboard packaging market size is projected to be valued at US$ 1.4 billion in 2026. The market is anticipated to subsequently reach US$ 2.2 billion by 2033.

The honeycomb paperboard packaging market is primarily driven by surging e-commerce fulfillment demand and stringent global plastic reduction mandates. These factors are expected to accelerate the transition toward sustainable, lightweight structural packaging.

The honeycomb paperboard packaging market is expected to expand at a compound annual growth rate of 6.7% during the forecast period. This growth trajectory is anticipated to span from 2026 through 2033.

Asia Pacific is projected to lead the global regional landscape. The region is anticipated to hold a dominant market share of approximately 43%.

Key players include Smurfit Kappa, DS Smith, Packaging Corporation of America, and Axxor.