- Home Care & Utilities

- Flushable Nonwovens Market

Flushable Nonwovens Market Size, Share, and Growth Forecast 2026 - 2033

Flushable Nonwovens Market by Product Type (Flushable Wipes, Flushable Diapers, Flushable Towels, Flushable Feminine Hygiene Products, Flushable Medical Supplies), Material Type (Wood Pulp, Cellulose Fibers, Cotton, Rayon, Polypropylene, Natural Fibers, Synthetic Fibers), Application, End-user, and Regional Analysis, 2026 - 2033

Flushable Nonwovens Market Size and Trend Analysis

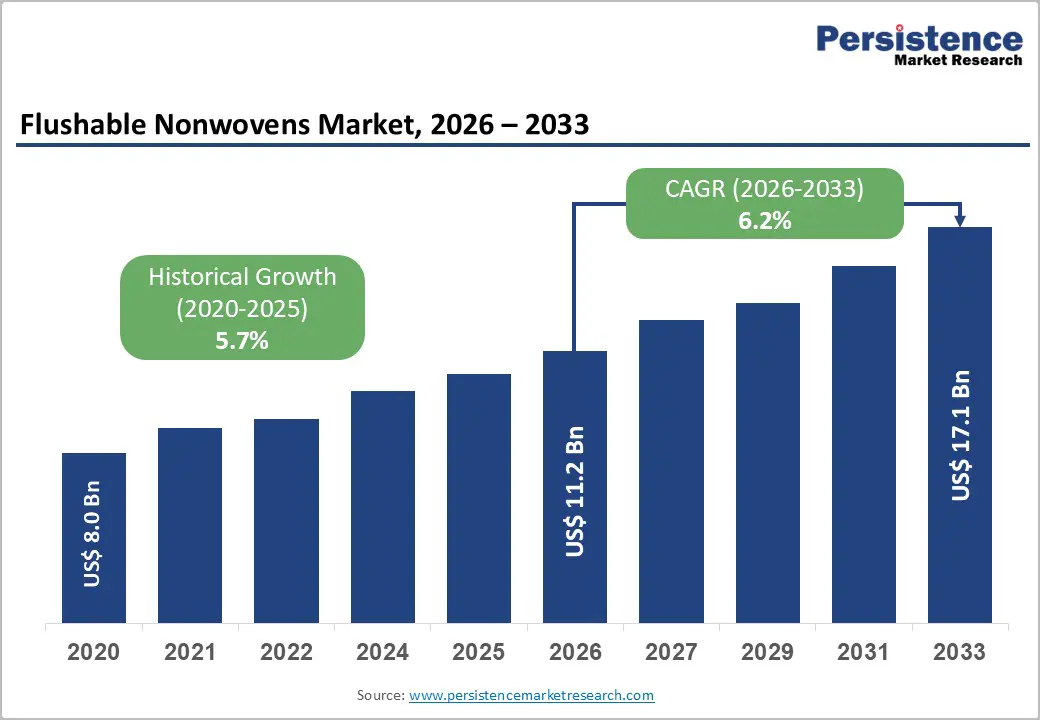

The global flushable nonwovens market size is likely to be valued at US$ 11.2 billion in 2026 and is expected to reach US$ 17.1 billion by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033.

The flushable nonwovens market is experiencing accelerating growth driven by rising consumer demand for convenient, hygienically superior personal care products, expanding healthcare infrastructure globally, and a critical regulatory shift toward genuine standards that elevate the needs for product quality.

Key Industry Highlights:

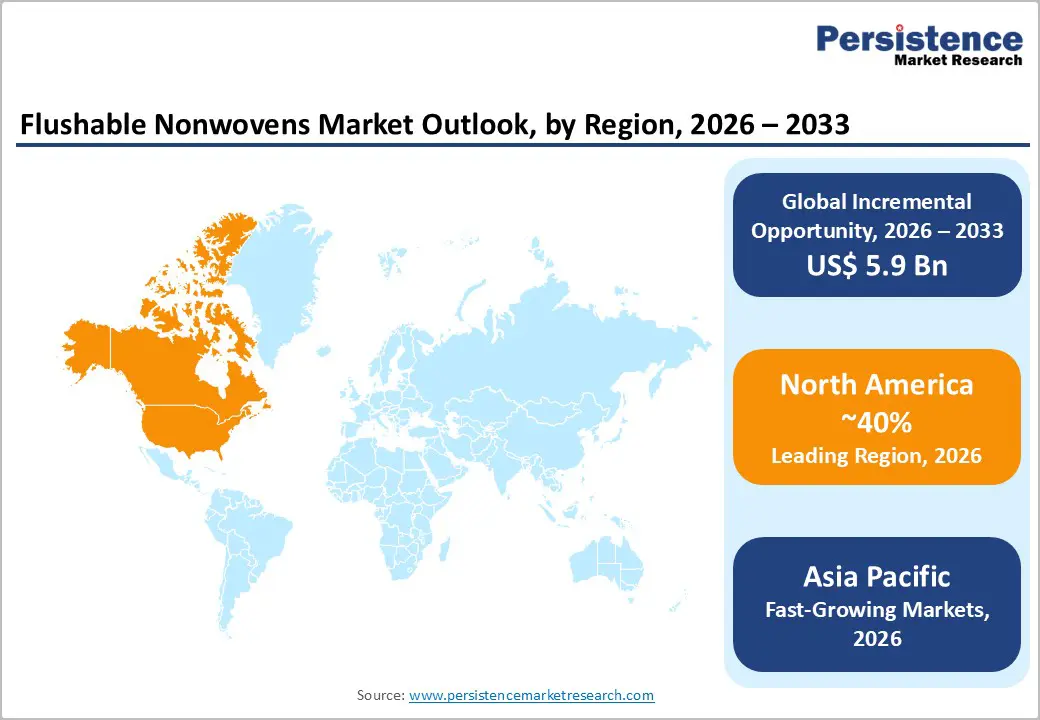

- Leading Region: North America leads the flushable nonwovens market, holding 40% share, driven by the U.S.’s highest global per-capita consumption of moist toilet tissue, FTC flushability claim regulations, and state-level legislation in California and New York mandating certified flushability testing for labeled products.

- Fastest Growing Market: Asia Pacific is the fastest growing region with a CAGR of 8.1%, propelled by China’s booming personal care market, India’s Swachh Bharat Mission-driven hygiene improvement, Japan’s mature moist toilet tissue culture, and ASEAN’s rapidly expanding baby care and personal hygiene wipe adoption.

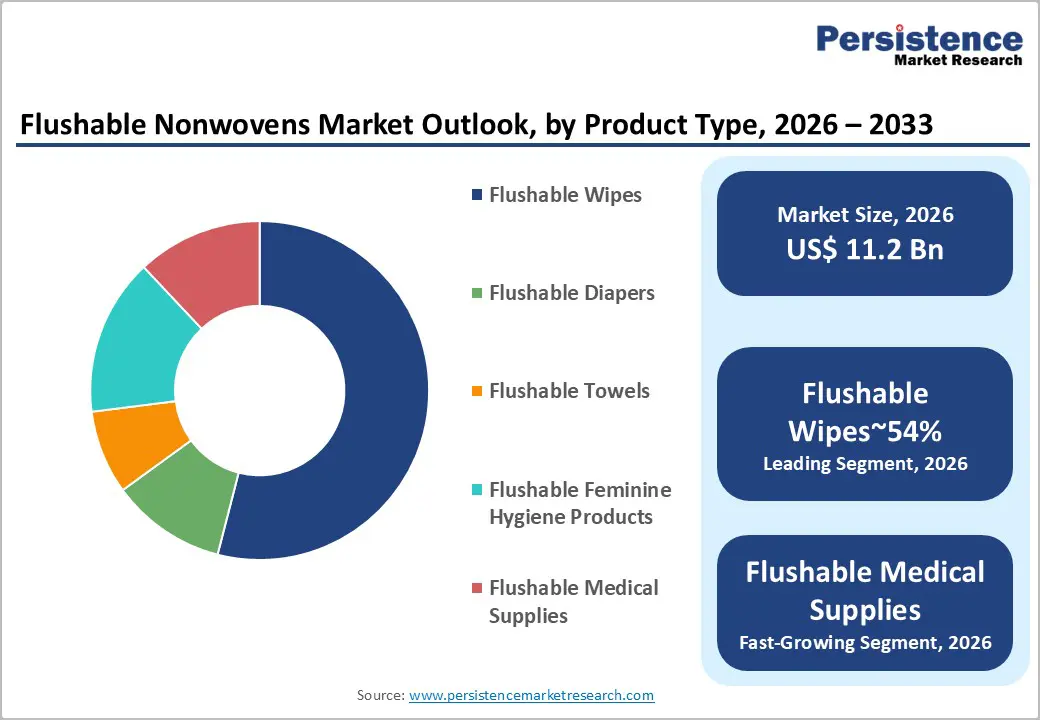

- Dominant Product Segment: Flushable wipes are likely to lead with approximately 64% market share, anchored by Kimberly-Clark’s Cottonelle and P&G’s Charmin brands, consistent repurchase frequency, and INDA/EDANA-documented fastest growth within the broader wet wipes market.

- Fastest Growing Product: Flushable medical supplies are the fastest growing, driven by WHO-validated infection control hygiene requirements, expanding global healthcare infrastructure, and hospital procurement preferences for certified flushable patient care wipes meeting ISO 11135 standards.

- Key Opportunity: Next-generation biodegradable, flushable substrates made with TENCEL lyocell, hemp, and FSC-certified wood pulp, targeting EU Ecolabel certification, can command 25% price premiums in sustainability-driven European retail channels, with BEUC documenting 70%+ consumer preference for sustainable personal care products.

Market Dynamics

Drivers - Rising Consumer Hygiene Awareness and Personal Care Product Premiumization

Consumer hygiene consciousness, significantly elevated by the COVID-19 pandemic, has created a structural, lasting expansion in demand for personal care nonwoven products including flushable wipes. The Global Hygiene Council documented sustained increases in hand hygiene and personal sanitation product consumption in the post-pandemic period, with moist toilet tissue and personal care wipes experiencing particularly strong demand growth.

In North America alone, the American Cleaning Institute (ACI) noted consistent year-on-year growth in retail sales for the wet wipe and personal hygiene categories. The aging global population is also a powerful demographic demand driver, with the United Nations projecting that persons aged 65+ will represent 16% of the global population by 2050, as elderly care requirements increasingly rely on flushable incontinence products, personal care wipes, and adult diapers. These intersecting demographic and behavioral trends are sustaining long-term, structurally growing demand for certified flushable nonwoven products across personal and healthcare applications.

Growing Regulatory Pressure for Certified Flushability and Sewer Protection

Water utilities and municipal governments worldwide are increasingly enacting regulations and awareness campaigns to address the persistent problem of non-flushable wipes clogging sewage infrastructure. The Water UK association estimated that the UK sewer system handles over 300,000 sewer blockages annually, with a significant proportion attributed to non-flushable wipes, costing water companies over £100 million per year.

Similar issues have been documented in the U.S., Australia, and Canada. In response, Water UK launched the ‘Fine to Flush’ certification scheme, and INDA and EDANA (European Disposables and Nonwovens Association) developed the GD4 (Code of Practice for Flushable Products) framework. These certification-driven demand signals are compelling manufacturers to invest in genuinely biodispersible nonwoven substrates that pass recognized flushability tests, creating a premium, compliance-differentiated market segment that drives both product innovation and higher average selling prices.

Restraints - High Raw Material and Processing Costs for Biodispersible Nonwovens

Developing genuinely flushable nonwoven substrates using wood pulp, lyocell, or cotton-based fibers, with hydroentanglement or wet-laid processing, involves significantly higher material and manufacturing costs than conventional polypropylene or polyester nonwovens used in non-flushable wet wipes.

Premium cellulose-based flushable substrates can cost 40% more per unit area than conventional alternatives, creating price points that deter mass-market consumer adoption, particularly in price-sensitive developing market consumer segments. This cost differential constrains the pace of market conversion from non-flushable to genuinely flushable products.

Consumer Confusion and Greenwashing Concerns

A persistent challenge in the flushable nonwovens market is consumer confusion between genuinely certified flushable products and products marketed as “safe to flush” that do not meet recognized standards such as INDA’s GD4 protocol or Water UK’s Fine to Flush scheme.

Multiple class action lawsuits in the U.S. and regulatory investigations in the UK and Australia have targeted manufacturers of non-compliant products marketed as flushable, creating reputational risk for the entire category. This consumer trust deficit reduces category growth velocity, as negative media coverage of blockage incidents discourages broader adoption of even genuinely flushable certified products.

Opportunities - Development of Certified Bio-dispersible Wipes in the Healthcare Domain

Expanding healthcare infrastructure in emerging economies across Asia Pacific, Africa, and Latin America is creating a significant growth opportunity for certified flushable medical-grade nonwovens used in patient hygiene, surgical preparation, and infection control applications. Hospitals and long-term care facilities in these regions are adopting disposable hygiene products at an accelerating rate as healthcare standards improve.

The World Health Organization (WHO) has documented the critical role of patient hygiene practices in preventing hospital-acquired infections, a market valued globally at over US$ 1 billion annually for clinical hygiene products. Healthcare facilities are prioritizing certified flushable medical wipes because they reduce waste-handling requirements and improve infection-control workflows. Manufacturers with ISO 11135 (sterilization) and EN 14885 (disinfectant efficacy) compliant product lines incorporating genuinely flushable substrates can differentiate strongly and build premium hospital procurement relationships in these fast-growing healthcare markets.

Next-Generation Biodegradable and Sustainable Flushable Substrate Innovation

The intersection of flushability regulation and consumer sustainability preferences is driving significant R&D investment in next-generation bio-based, biodegradable nonwoven substrates that combine genuine flushability with environmental performance credentials. Lyocell (TENCEL) fibers, hemp-based nonwovens, and seaweed-derived cellulose substrates are among the emerging materials being evaluated for flushable wipe applications by leading nonwoven producers, including Ahlstrom-Munksjö, Glatfelter Corporation, and Suominen Corporation.

Consumer research by the European Consumer Organization (BEUC) consistently finds that 70%+ of European consumers prefer sustainable personal care products. Manufacturers that achieve EU Ecolabel certification or equivalent for their flushable nonwoven products, confirming both genuine flushability and reduced environmental impact, can command 15–25% price premiums in eco-conscious retail channels, representing a significant and growing revenue opportunity through the forecast period.

Category-wise Analysis

By Product Type Insights

Flushable wipes dominate the product type segment, commanding approximately 64% of total market share. Flushable wipes, encompassing moist toilet tissue, personal care wipes, baby wipes marketed for flushability, and feminine hygiene wipes, represent the core and most commercially established product category within the flushable nonwovens market.

Their convenience advantages over dry toilet paper, particularly in terms of hygiene, cleansing efficacy, and comfort for elderly and sensitive skin users, have driven consistent category growth for over a decade. The INDA and EDANA collectively report that flushable wipes are the fastest-growing subcategory of the broader wet wipes market, both in volume and value. Premium moist toilet tissue brands from Kimberly-Clark (Cottonelle) and Procter & Gamble (Charmin) anchor the retail category with certified flushable claims.

By Material Type Insights

Wood pulp is the leading material type segment, representing approximately 38% of total market share. Wood pulp-based nonwoven substrates, produced through wet-laid or airlaid processing techniques, offer the optimal combination of genuinely biodispersible performance, competitive raw material costs, and processing versatility, making them the dominant substrate choice for certified flushable nonwoven products.

Wood pulp fibers disintegrate rapidly in water, meeting the rapid disintegration requirements of international flushability protocols, including INDA GD4 and Water UK Fine to Flush standards. The availability of FSC (Forest Stewardship Council)-certified wood pulp from sustainably sourced forests further enhances the environmental credentials of wood pulp-based flushable products, aligning with consumer sustainability expectations and supporting premium brand positioning in eco-conscious retail channels.

By Application Insights

Personal care is the dominant application segment, accounting for approximately 47% of the market. Personal care applications, encompassing moist toilet tissue, personal hygiene wipes, feminine care wipes, and adult incontinence management products, represent the foundational and largest-volume application for flushable nonwovens. Consumer adoption of moist toilet tissue has been particularly strong in North America and Europe, where the Association of the Nonwoven Fabrics Industry (INDA) documents consistent market penetration growth.

The personal care segment benefits from high repurchase frequency, generating recurring retail demand, and from demographic tailwinds, including aging populations requiring incontinence products and growing consumer awareness of intimate hygiene. Premium product positioning supported by clinical hygiene claims and certified flushability labeling drives above-average category value growth.

By End-user Insights

Residential is the dominant end-use segment, accounting for approximately 58% of the market. The residential segment encompasses all household personal care, baby care, and household cleaning flushable nonwoven product consumption, the most voluminous and geographically distributed demand category in the market. Household penetration of flushable wipes continues to grow across mature markets in North America, Europe, and Australia, driven by product innovation, improvements in retail availability, and shifting hygiene norms.

The U.S. Census Bureau reports that U.S. households number over 130 million, each representing a potential recurring consumer of personal care flushable products. The residential segment also benefits from the strongest direct consumer marketing investment by category leaders, including Kimberly-Clark and Procter & Gamble, reinforcing category awareness and trial conversion.

Regional Insights

North America Flushable Nonwovens Market Trends & Analysis

North America leads the global flushable nonwovens market, supported by high hygiene awareness, strong premium product penetration, and robust regulatory oversight of flushability claims. Innovation in biodegradable substrates and strict wastewater compliance standards are driving product evolution, while brand competition and retail accessibility are sustaining steady demand growth.

- U.S. Flushable Nonwovens Market Size

The U.S. dominates the regional market, accounting for approximately USD 8.2 billion by 2026, driven by high consumption of moist toilet tissue and flushable wipes. Regulatory pressure from environmental agencies and state legislation is accelerating investment in certified flushable materials.

Europe Flushable Nonwovens Market Trends, Drivers & Insights

Europe represents a mature, regulation-driven market characterized by strict wastewater standards and strong environmental consciousness. The transition toward plastic-free substrates is accelerating due to regulatory frameworks such as the SUP Directive. Continuous innovation in sustainable nonwoven technologies and certification schemes is shaping product development across the region.

- Germany Flushable Nonwovens Market Size

Germany holds a significant share, estimated at USD 1.4 billion by 2026, driven by a strong personal care industry and sustainability focus. The demand is driven by environmentally conscious consumers and advanced wastewater infrastructure.

- U.K. Flushable Nonwovens Market Size

The U.K. market is valued at approximately USD 1.1 billion by 2026, led by stringent flushability standards such as “Fine to Flush.” Regulatory leadership and water utility advocacy are driving adoption of certified products.

- France Flushable Nonwovens Market Size

France is projected to reach USD 950 million by 2026, supported by strict consumer protection laws and labeling requirements. Growth is driven by increasing awareness around environmental impact and sustainable hygiene products.

Asia Pacific Flushable Nonwovens Market Drivers & Analysis

Asia Pacific is the fastest-growing market, driven by rising disposable incomes, urbanization, and expanding hygiene awareness. Growth is particularly strong in baby care, personal hygiene, and healthcare sectors. Government sanitation initiatives and rapid e-commerce expansion are further accelerating product penetration and regional manufacturing capabilities.

- China Flushable Nonwovens Market Size

China is expected to reach USD 2.3 billion by 2026, driven by rapid expansion in personal care and baby wipe markets. Increasing urbanization and digital retail growth are key drivers, with strong domestic and international competition supporting a high CAGR of ~7.0%.

- India Flushable Nonwovens Market Size

India’s market is estimated at USD 850 million by 2026, supported by rising hygiene awareness and government sanitation programs like Swachh Bharat. Urban middle-class expansion and healthcare demand are accelerating adoption, with a projected CAGR of ~7.5%, among the highest globally.

- Japan Flushable Nonwovens Market Size

Japan is a mature yet innovative market, projected at USD 1.7 billion by 2026. High penetration of moist toilet tissue and advanced hygiene practices drive steady demand. Technological leadership in nonwoven materials supports a stable growth rate of ~5.0%.

Competitive Landscape

The global flushable nonwovens market is moderately consolidated at the finished product level, with large consumer goods companies including Kimberly-Clark and Procter & Gamble dominating retail flushable wipe brand sales, while the nonwoven substrate supply tier is served by a mix of large industrial nonwovens producers and specialty substrate manufacturers.

Key competitive differentiators include certified flushability compliance, substrate biodispersibility technology, raw material sustainability credentials, and private label supply capabilities for retailer brands. Emerging business model trends include sustainability co-branding between substrate manufacturers and finished goods brands, EU Ecolabel-targeted product development, and investments in marine biodegradability certification to address microplastic concerns that are increasingly influencing European regulatory and consumer trends.

Key Developments:

- March 2025: Suominen Corporation launched a new 100% plant-based flushable wipe substrate using Nordic FSC-certified wood pulp and lyocell fibers, targeting Water UK Fine to Flush certification for retail and healthcare customers across European markets.

- October 2024: Kimberly-Clark Corporation announced reformulation of its Cottonelle Flushable Wipes range to achieve INDA GD4 protocol compliance, transitioning to a plant-based cellulose substrate that disintegrates rapidly in water and sewer systems while maintaining cleansing performance.

- June 2024: Glatfelter Corporation introduced a new airlaid wood pulp substrate platform specifically engineered for flushable medical wipes, achieving both certified flushability and antimicrobial performance for hospital hygiene and patient care applications in healthcare facility markets.

Global Flushable Nonwovens Market- Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 8.0 Bn |

|

Current Market Value (2026) |

US$11.2 Bn |

|

Projected Market Value (2033) |

US$ 17.1 Bn |

|

CAGR (2026-2033) |

6.2% |

|

Leading Region |

North America, 40% share |

|

Dominant Product Type |

Flushable Wipes, 64% share |

|

Top-ranking Application |

Personal Care, 47% |

|

Incremental Opportunity |

US$ 5.9 Bn |

Companies Covered in Flushable Nonwovens Market

- Kimberly-Clark Corporation

- Procter & Gamble Co.

- Berry Global Group, Inc.

- Ahlstrom-Munksjö Oyj

- Glatfelter Corporation

- Georgia-Pacific LLC

- Suominen Corporation

- Fitesa S.A.

- Freudenberg Group

- Johns Manville Corporation

- TWE Group GmbH

- Hollingsworth & Vose Company

- Pegas Nonwovens SA

- Toray Industries, Inc.

- Avgol Nonwovens Ltd.

- Lenzing AG

- Essity AB

Frequently Asked Questions

The global Flushable Nonwovens Market is projected to reach US$ 17.1 Billion by 2033, growing from US$ 11.2 Billion in 2026 at a CAGR of 6.2% during the 2026–2033 forecast period.

The primary drivers are rising consumer hygiene awareness, with the UN projecting 16% of the global population to be 65+ by 2050 driving elderly care flushable product demand, and Water UK’s documentation of £100M+ annual UK sewer blockage costs from non-compliant wipes driving INDA GD4 and Fine to Flush certification mandates that are compelling genuine biodispersible product development.

Flushable Wipes lead the By Product Type category with approximately 64% market share. As the most commercially established flushable nonwoven product, anchored by Kimberly-Clark’s Cottonelle and Procter & Gamble’s Charmin brands with certified flushability claims, they generate the highest repurchase frequency and broadest retail distribution of any flushable nonwoven product category.

North America leads the global Flushable Nonwovens Market, underpinned by the U.S.’s world-leading moist toilet tissue per-capita consumption, FTC flushability claim regulatory oversight, and state-level legislation in California and New York requiring certified flushability testing, compelling brand owners including Kimberly-Clark and P&G to invest in genuinely biodispersible certified product formulations.

The highest-value opportunities are next-generation sustainable flushable substrates using FSC-certified wood pulp, TENCEL lyocell, and hemp achieving EU Ecolabel certification, commanding 25% price premiums with BEUC’s 70%+ eco-preference consumers, and certified flushable medical wipes for emerging market healthcare infrastructure growth validated by WHO infection control guidelines.

The key participants include Kimberly-Clark Corporation, Procter & Gamble Co., Berry Global Group Inc., Ahlstrom-Munksjö Oyj, Glatfelter Corporation, Georgia-Pacific LLC, Suominen Corporation, Fitesa S.A., Freudenberg Group, Toray Industries Inc., Pegas Nonwovens SA, Avgol Nonwovens Ltd., TWE Group GmbH, and Hollingsworth & Vose Company, spanning consumer brand owners and nonwoven substrate manufacturers.