- Advanced Materials

- Furfural Derivatives Market

Furfural Derivatives Market Size, Share, and Growth Forecast 2026 - 2033

Furfural Derivatives Market by Product Type (Furfuryl Alcohol, Tetrahydrofuran, Furoic Acid, 2-Methylfuran, Others), Application (Resins and Foundry, Solvents, Pharmaceuticals, Agrochemicals, Fuel Additives), End-use Industry (Chemicals and Materials, Plastics and Polymers, Pharmaceuticals, Agriculture, Food and Beverage, Other), and Regional Analysis for 2026 - 2033

Furfural Derivatives Market Size and Trend Analysis

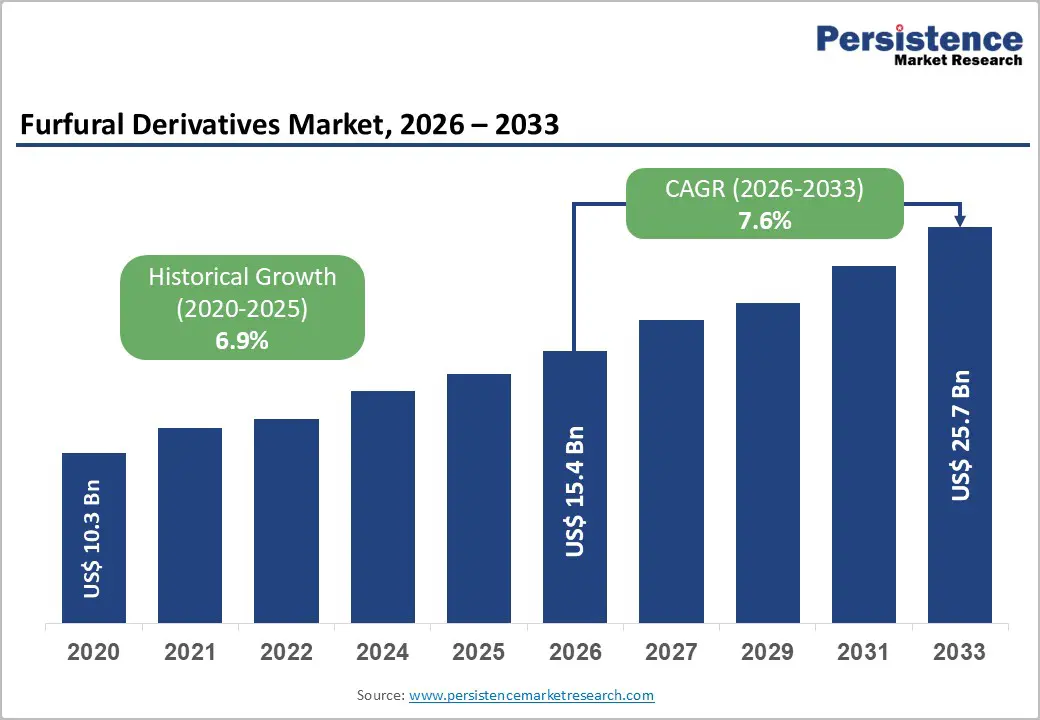

The global furfural derivatives market is valued at US$ 15.4 billion in 2026 and is projected to reach US$ 25.7 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

This robust growth is primarily fueled by accelerating global demand for bio-based, sustainable chemical alternatives to petrochemical-derived compounds, underpinned by stricter environmental regulations and rising adoption of circular economy principles across industries. The foundry and resin sector continues to absorb the largest share of furfuryl alcohol, driven by expanding construction and automotive metal-casting requirements, while diversified uptake in pharmaceuticals, agrochemicals, and advanced biofuels adds meaningful breadth to demand. Supporting this trajectory, government initiatives such as India's Global Biofuels Alliance (GBA), launched in 2024, and the European Union's Carbon Border Adjustment Mechanism (CBAM), entering its definitive phase in 2026, are structurally incentivizing bio-based chemical investment.

Key Industry Highlights:

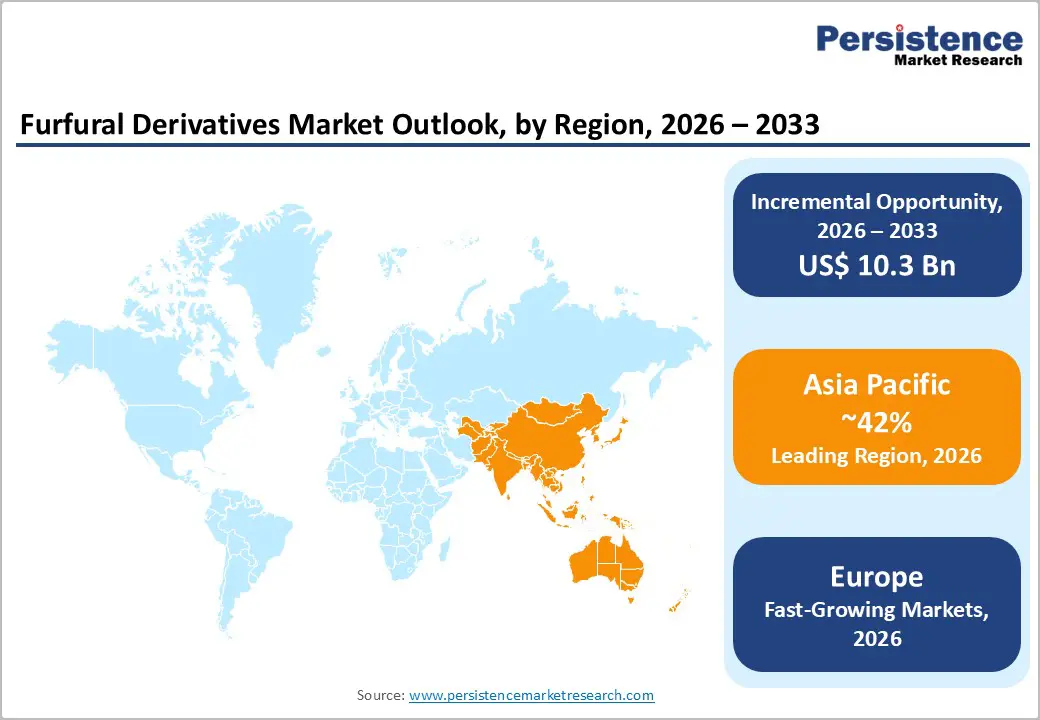

- Leading Region: Asia Pacific dominates the global furfural derivatives market with approximately 42% revenue share in 2025, driven by China's commanding furfural and furfuryl alcohol production capacity, abundant agricultural biomass feedstock, and rising industrial demand across chemicals, plastics, and agrochemicals verticals.

- Fastest Growing Region: Europe is projected to register the fastest regional CAGR through 2033, propelled by the CBAM definitive phase effective 2026, the European Green Deal mandates, and breakthrough investments such as Avantium's FDCA Flagship Plant in the Netherlands that are catalyzing a bio-based chemicals transition.

- Dominant Segment: Furfuryl alcohol leads by product type with approximately 62% revenue share, underpinned by its critical role in furan resin production for foundry mold-making, an application directly linked to global automotive manufacturing output exceeding 93 million vehicles annually.

- Fastest Growing Segment: The pharmaceuticals application segment is projected to expand at the fastest rate of approximately 8.4% CAGR through the forecast period, driven by growing utilization of furoic acid and furfuryl derivatives in antimicrobial drug candidates and eco-friendly crop protection formulations.

- Key Market Opportunity: The commercialization of FDCA and bio-based PEF plastic, led by Avantium's world-first Delfzijl plant targeting commercial sales from 2026, presents the most transformative near-term opportunity, creating an entirely new high-margin derivative category within the global furfural derivatives landscape.

| Key Insights | Details |

|---|---|

| Furfural Derivatives Market Size (2026E) | US$ 15.4 Bn |

| Market Value Forecast (2033F) | US$ 25.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 7.6% |

| Historical Market Growth (2020 - 2025) | 6.9% |

DRO Analysis

Drivers - Surging Demand for Bio-based Chemicals amid Decarbonization Mandates

The transition from fossil-based inputs to renewable chemical feedstocks constitutes the most significant structural driver of growth in the furfural derivatives market. Derived through the acid hydrolysis of lignocellulosic agricultural residues such as corn cobs, sugarcane bagasse, and rice husks, furfural-based compounds provide a commercially viable and scalable platform for bio-based chemical production. Governments across major economies are increasingly translating sustainability commitments into binding regulatory frameworks.

In the European Union, the implementation of Regulation (EU) 2023/956 establishing the Carbon Border Adjustment Mechanism from 2026 mandates carbon reporting for imported goods, thereby favoring low-carbon, bio-based alternatives. Similarly, the U.S. Inflation Reduction Act of 2022 allocates substantial funding to clean energy and sustainable industrial processes, directly supporting bio-based chemical manufacturers. Consequently, sustained investment across the furfural derivative value chain is accelerating.

Expanding Foundry and Advanced Resin Applications in Automotive and Construction Sectors

Furfuryl alcohol-based furan resins are integral to the global foundry industry, where they are widely utilized as high-performance binders for sand molds and cores in precision metal casting applications. These materials provide superior thermal resistance, dimensional accuracy, and low defect incidence, making them essential in the production of aluminum engine blocks and iron castings for automotive and heavy machinery markets. Sustained global automotive output continues to support stable baseline demand.

In parallel, furfuryl alcohol is gaining prominence as a feedstock for the synthesis of bio-based polyurethanes with enhanced thermal and chemical performance, as evidenced by recent academic research. Additionally, accelerated construction activity across Asia Pacific and the Middle East, particularly in large-scale infrastructure and smart-city developments, is driving increased demand for advanced composite materials incorporating furfural-derived resins, supporting long-term market growth.

Restraints - High Production Cost and Energy Intensity of Furfural Manufacturing

The production of furfural is an energy-intensive process requiring acid hydrolysis of biomass under high-temperature steam conditions, demanding significant capital investment in specialized reactors and distillation units. In North America, average furfural production costs ranged between US$ 1,600-US$ 1,800 per ton in 2024, compared to US$ 1,200-US$ 1,500 per ton in China, where abundant crop residue availability and lower energy costs provide a structural cost advantage. This cost disparity complicates market entry for producers in higher-cost regions and compresses margins, particularly when competing with established petrochemical pathways such as maleic anhydride-based furans. The 2022-2023 European energy crisis demonstrated how rapidly energy prices can erode the competitiveness of bio-based processes, creating uncertainty for capital-intensive investments.

Supply Chain Fragility and Seasonal Feedstock Volatility

The furfural derivatives supply chain is intrinsically tied to agricultural output cycles, exposing producers to feedstock price volatility linked to weather conditions, crop disease, and competing agricultural uses. Corn cob and sugarcane bagasse availability fluctuates seasonally, and competing bioenergy applications, such as pellet production and direct combustion, place additional pressure on these residue streams.

According to the Food and Agriculture Organization (FAO), global cereal production is subject to annual variability of ±5-8%, which can create supply disruptions and price spikes for furfural producers heavily reliant on consistent feedstock volumes. This raw material uncertainty constrains capacity utilization, increases procurement costs, and can delay delivery commitments, representing a meaningful barrier to expanding output in line with market demand.

Opportunities - A High-Growth Frontier in Circular Packaging demanding FDCA and PEF Bioplastics

2,5-Furandicarboxylic acid (FDCA), derived from furfural or HMF pathways, is emerging as a transformative platform molecule for the production of polyethylene furanoate (PEF), a 100% bio-based, recyclable plastic that outperforms conventional polyethylene terephthalate (PET) in barrier properties for oxygen and carbon dioxide, making it ideal for premium beverage packaging.

Avantium N.V. officially opened the world's first commercial FDCA plant at Chemie Park Delfzijl, Netherlands, in October 2024, designed to produce up to 5 kilotonnes of FDCA per year using its proprietary YXY® Technology. The company has secured offtake agreements with global brands including Henkel, Carlsberg, and Helios. As PEF scales commercially toward 2026, it is set to generate an entirely new high-margin derivative category within the furfural derivatives landscape, opening substantial licensing revenue streams and creating strong market pull for furfural platform chemicals at an industrial scale.

Biofuels Expansion and 2-Methylfuran as a Next-Generation Fuel Additive

The global biofuels sector represents a rapidly expanding opportunity for furfural derivative producers, particularly for 2-methylfuran (2-MF) as a high-octane, renewable transport fuel blending agent. 2-MF possesses a research octane number higher than that of ethanol and exhibits superior energy density, low water miscibility, and compatibility with existing fuel infrastructure, characteristics endorsed by peer-reviewed combustion studies and research from the U.S. Department of Energy (DOE).

The Global Biofuels Alliance (GBA), launched by India in 2024 and endorsed by 19 member governments, is catalyzing investments in sustainable aviation fuel (SAF) and road transport biofuels across Asia and Africa, markets with low current penetration but significant scale potential. With the International Energy Agency (IEA) projecting global biofuel demand to rise by over 30% between 2023 and 2028, the downstream pull for furfural-derived fuel components is expected to accelerate materially, rewarding early movers in the 2-MF production space.

Category-wise Analysis

Product Type Insights

Furfuryl alcohol (FA) represents the leading product type in the global furfural derivatives market, accounting for approximately 62% of total revenues in 2025. Its market dominance is primarily attributed to its critical function as a binder resin precursor in foundry casting applications, where it offers exceptional thermal stability, low shrinkage, and significantly lower volatile organic compound (VOC) emissions compared with conventional phenolic systems.

The principal end users include the automotive and heavy machinery industries, which rely extensively on sand casting for the manufacture of engine blocks, transmission components, and iron piping. According to the World Foundry Organization, global metal casting output exceeds 112 million metric tons annually, underscoring the scale of demand. Beyond foundry applications, furfuryl alcohol is increasingly utilized in the production of bio-based polyurethanes. Supported by capacity expansions in China and India, FA is expected to retain its market leadership through 2033.

Application Insights

Resins and foundry segment occupies a leading position within the furfural derivatives application landscape, accounting for over 55% of total consumption in 2025. Furan resins, produced from furfuryl alcohol, are extensively employed as high-performance binders for precision foundry molds and cores, owing to their exceptional thermal stability and ability to endure temperatures exceeding 1,200°C without structural deformation.

The global foundry sector remains closely aligned with the automotive industry, and increasing electric vehicle adoption is driving demand for lightweight aluminum components manufactured through advanced casting technologies. Additionally, furan resins are utilized in construction applications, particularly as acid-resistant linings for industrial storage tanks and chimneys. The segment’s long-term stability is supported by the lack of cost-effective substitutes at scale, alongside expanding research into bio-based adhesive systems for wood composites and insulation materials.

Industry Insights

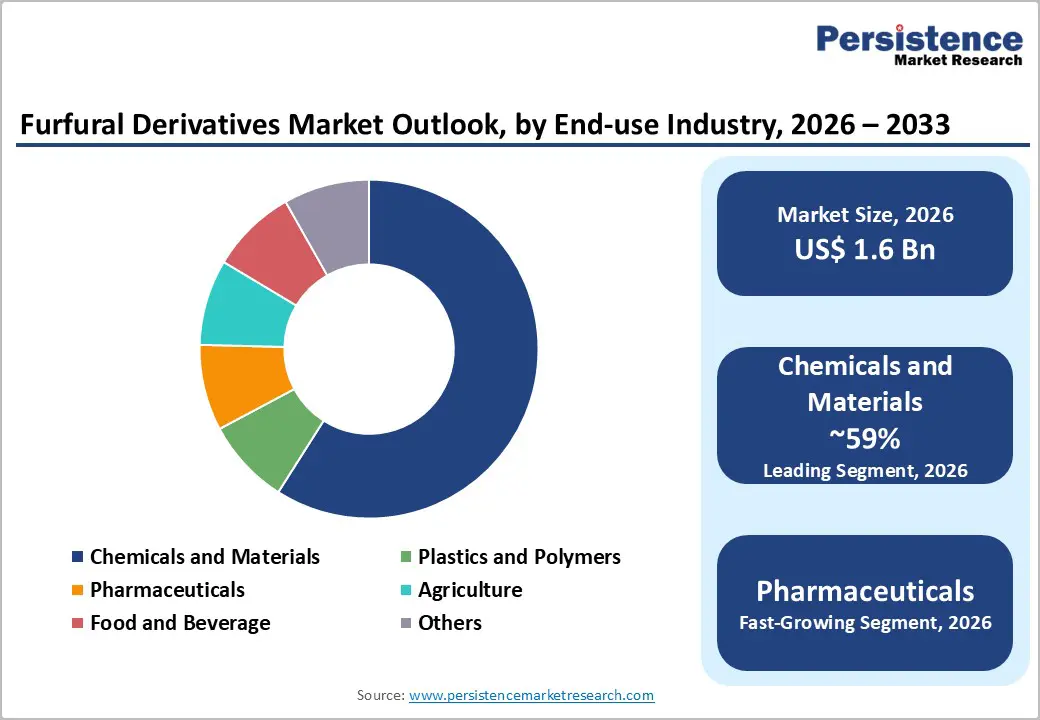

Chemicals and materials industry is the leading consuming vertical, accounting for over 59% of furfural derivatives market revenues in 2025. This dominance is underpinned by the extensive role of furfural derivatives as chemical intermediates across coating formulations, specialty solvents, adhesive resins, and composite binder systems. Furfuryl alcohol-based resins serve corrosion-resistant lining applications in the chemical process industry, and tetrahydrofuran (THF) is a critical solvent and monomer feedstock, particularly for polytetramethylene ether glycol (PTMEG), used in spandex fiber production under trademarks such as Lycra® and Elastane.

The chemical industry's pivot toward bio-based intermediates under Regulation (EU) 2023/956 and the U.S. Biopreferred Program actively incentivizes substitution of petroleum-derived solvents and resins with furfural-based alternatives, reinforcing the sector's pre-eminent share. Investments in continuous process improvement and catalyst innovation, such as BASF SE's copper hydrogenation catalysts for 2-MF synthesis, are further improving yield economics, sustaining the chemicals and materials segment as the cornerstone of market demand.

Regional Insights

North America Furfural Derivatives Market Trends

North America represents the second-largest regional market for furfural derivatives, underpinned primarily by the United States’ strong policy support for bio-based chemicals and its advanced industrial research and development ecosystem. The U.S. Inflation Reduction Act, with a clean-energy investment commitment of approximately US$ 369 billion, together with the continued expansion of the USDA BioPreferred Program, is reinforcing institutional demand for renewable chemical intermediates.

Pennakem, LLC, recognized as the world’s largest producer of furan, furfurylamine, and furfuryl alcohol, operates a flagship manufacturing facility in Memphis, Tennessee, leveraging more than six decades of expertise in furan chemistry. North America’s specialization in high-value derivatives, particularly pharmaceutical-grade furoic acid and specialty solvents, provides producers with a premium competitive positioning. Additionally, tightening EPA volatile organic compound emission standards are accelerating the adoption of furfuryl alcohol-based resins over conventional binder systems in foundry applications.

Europe Furfural Derivatives Market Trends

Europe is projected to record the fastest growth rate in the global furfural derivatives market in the forecast period, driven by an increasingly stringent regulatory and policy environment. Regulation (EU) 2023/956 establishing the Carbon Border Adjustment Mechanism (CBAM), which entered its definitive phase on 1 January 2026, requires importers of carbon-intensive goods to purchase carbon certificates, thereby shifting procurement preferences toward low-carbon, bio-based chemical alternatives.

Proposed extensions of CBAM coverage to organic chemicals and polymers beyond 2026 are expected to further reinforce this transition. Germany, France, and the Netherlands anchor regional demand, supported by Germany’s advanced chemical manufacturing base and France’s strong pharmaceutical sector. The Netherlands’ FDCA Flagship Plant operated by Avantium N.V. underscores Europe’s leadership in next-generation bio-based materials. Collectively, CBAM, the European Green Deal, and REPowerEU initiatives position Europe as a highly innovation-driven market through 2033.

Asia Pacific Furfural Derivatives Market Trends

Asia Pacific continues to dominate the global furfural derivatives market, accounting for approximately 42% of total revenues in 2025, with China serving as the primary production center. China controls more than 80% of global furfural and furfuryl alcohol manufacturing capacity, supported by abundant corn cob feedstock availability, comparatively lower energy costs, and well-established industrial infrastructure.

Leading domestic manufacturers, including Hongye Holding Group Corporation Ltd., Yuanli Chemical Group, and Xingtai Chunlei Furfuryl Alcohol Co., Ltd., continue to expand capacity and pursue downstream integration strategies. India is emerging as a significant growth market, driven by investments linked to the Global Biofuels Alliance, while Japan remains a high-value consumer of pharmaceutical-grade derivatives.

Competitive Landscape

The global furfural derivatives market exhibits a moderately consolidated competitive structure, with a handful of dominant players controlling significant production capacity, especially Pennakem, LLC in North America and multiple large-scale Chinese manufacturers in Asia Pacific, alongside a broader set of regional and specialty chemical producers. Competition is intensifying as leading companies invest in vertical integration from biomass feedstock procurement to high-value derivative production. Key strategies include capacity expansion in low-cost production regions, development of proprietary catalytic technologies (notably BASF SE's hydrogenation catalyst portfolio), and pioneering of novel bio-based derivative categories such as FDCA/PEF (Avantium N.V.). Cross-sector partnerships with automotive OEMs, pharmaceutical manufacturers, and biofuel blenders are becoming a differentiating business model trend, as are licensing strategies for proprietary production technologies.

Key Developments:

- February 2026: Avantium N.V., a pioneer in renewable and circular polymers, and Will & Co B.V., a distributor of specialty (bio-based) chemicals, have launched a collaboration to accelerate the use of FDCA (furandicarboxylic acid) in Coatings, Adhesives, Sealants, and Elastomers (CASE).

- January 2026: Avantium N.V., a pioneer in renewable and circular polymer materials, today provides an update on the start-up of its FDCA Flagship Plant in Delfzijl, the Netherlands. Avantium now expects to complete start-up by mid-2026 and to commence sales of product under its existing offtake agreements in the second half of 2026.

- November 2025: Avantium N.V., a leader in renewable and circular polymer materials, announces that its innovative plant-based plastic PEF (polyethylene furanoate), branded as releaf®, has received official approval for recycling within the Japanese PET (polyethylene terephthalate) bottle stream by the Council for PET Bottle Recycling (CPBR).

Top Companies in the Furfural Derivatives Market

- Pennakem, LLC (Memphis, U.S.) is recognized as the world's largest producer of furan, furfurylamine, and furfuryl alcohol, with over six decades of specialty and fine chemicals manufacturing experience. Affiliated with the MINAFIN Group, the company operates full-scale R&D and pilot plant facilities and serves pharmaceutical, agricultural, and rubber additive markets globally. Its proprietary Viridisol M renewable solvent, approved for use in natural detergent formulations since 2019, exemplifies Pennakem's commitment to green chemistry.

- Avantium N.V. (Amsterdam, Netherlands) is a pioneering commercial-stage company at the intersection of furfural derivative chemistry and advanced bio-based polymer materials. Its proprietary YXY® Technology converts plant-based sugars into FDCA, the key building block for PEF plastic branded Releaf®. The commissioning of its Delfzijl FDCA Flagship Plant in 2024 and offtake agreements with Henkel, Carlsberg, and Helios position Avantium as a transformative force in sustainable packaging materials globally.

- BASF SE (Ludwigshafen, Germany) engages with the furfural derivatives market primarily through its world-class hydrogenation catalyst portfolio, which is the technology backbone for converting furfural into furfuryl alcohol, 2-MF, and tetrahydrofurfuryl alcohol at commercial scale. Its copper catalyst Cu 0203 T is widely regarded as the industry standard for selective 2-MF synthesis, offering high selectivity, mechanical robustness, and resistance to multiple regeneration cycles, making it indispensable to bio-refinery operators globally. BASF's participation reinforces the market's technological infrastructure.

Companies Covered in Furfural Derivatives Market

- Pennakem, LLC

- BASF SE

- Central Romana Corporation, Ltd.

- Avantium N.V.

- Lenzing AG

- Silvateam S.p.A.

- Yuanli Chemical Group

- Hongye Holding Group Corporation Ltd.

- Xingtai Chunlei Furfuryl Alcohol Co., Ltd.

- Pyran

- UBE Corporation

- International Furan Chemicals B.V.

- TransFurans Chemicals bvba

- DynaChem Inc.

- Chempolis Oy

- Corbion N.V.

Frequently Asked Questions

The global furfural derivatives market is projected to reach US$ 25.7 Bn by 2033, growing from US$ 15.4 Bn in 2026 at a CAGR of 7.6% over the forecast period, driven by the expansion of bio-based chemical adoption and rising demand in foundry, pharmaceutical, and biofuel applications.

The key demand drivers include accelerating global adoption of bio-based chemicals as sustainable alternatives to petrochemicals, bolstered by policy frameworks such as the EU CBAM (Regulation (EU) 2023/956) and the U.S. Inflation Reduction Act. Rising foundry resin requirements linked to global automotive production and expanding applications in pharmaceuticals, agrochemicals, and biofuels are also key accelerators.

Furfuryl alcohol (FA) holds the dominant share of approximately 62% of total revenues in 2025. Its pre-eminence is driven by its indispensable role in furan resin production for foundry casting, its direct link to the global automotive and machinery manufacturing sectors, and its growing applications in bio-based polyurethane synthesis.

Asia Pacific leads the global furfural derivatives market with approximately 42% revenue share in 2025. China's dominant production infrastructure, accounting for over 80% of global furfural output, combined with rising industrial demand in India and Southeast Asia, makes this the definitive production and consumption hub for furfural derivatives globally.

The most transformative market opportunity lies in the commercialization of FDCA (2,5-furandicarboxylic acid) and bio-based PEF (polyethylene furanoate) plastics. With Avantium N.V.'s Delfzijl FDCA Flagship Plant targeting commercial sales from 2026 and a pipeline of offtake agreements with global brands, FDCA/PEF represents an entirely new, high-margin derivative category set to attract substantial licensing and investment activity.

Leading companies include Pennakem, LLC, Avantium N.V., BASF SE, Hongye Holding Group Corporation Ltd., Yuanli Chemical Group, International Furan Chemicals B.V., TransFurans Chemicals bvba, Central Romana Corporation, Ltd., and UBE Corporation, among others.