- Bulk Chemicals

- Froth Flotation Chemicals Market

Froth Flotation Chemicals Market Size, Share, and Growth Forecast, 2026 - 2033

Froth Flotation Chemicals Market by Product Type (Collectors, Frothers, Others), End-Use Industry (Mining, Pulp & Paper, Others), Reagent Form, and Regional Analysis for 2026 - 2033

Froth Flotation Chemicals Market Size and Trends Analysis

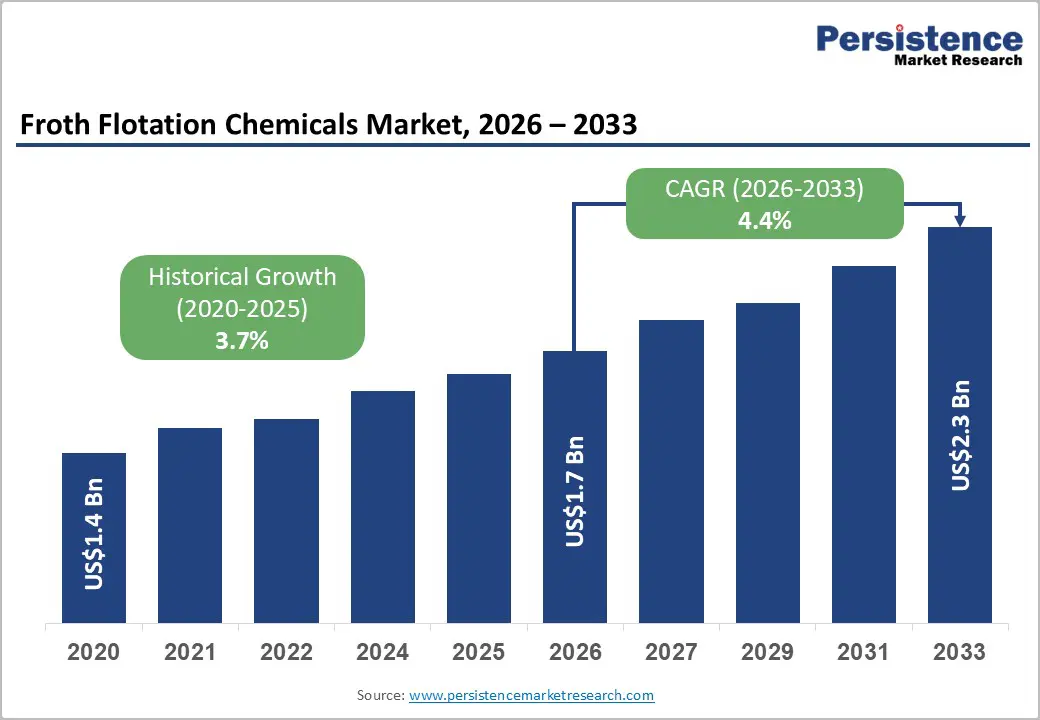

The global froth flotation chemicals market size is likely to be valued at US$1.7 billion in 2026 and is expected to reach US$2.3 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033, driven by increasing demand for critical minerals, tightening wastewater treatment regulations, and the expanding adoption of circular economy practices.

Additionally, a strong regulatory focus on sustainable chemical usage and enhanced recovery efficiency is boosting demand for high-performance, application-specific flotation reagents.

Key Industry Highlights:

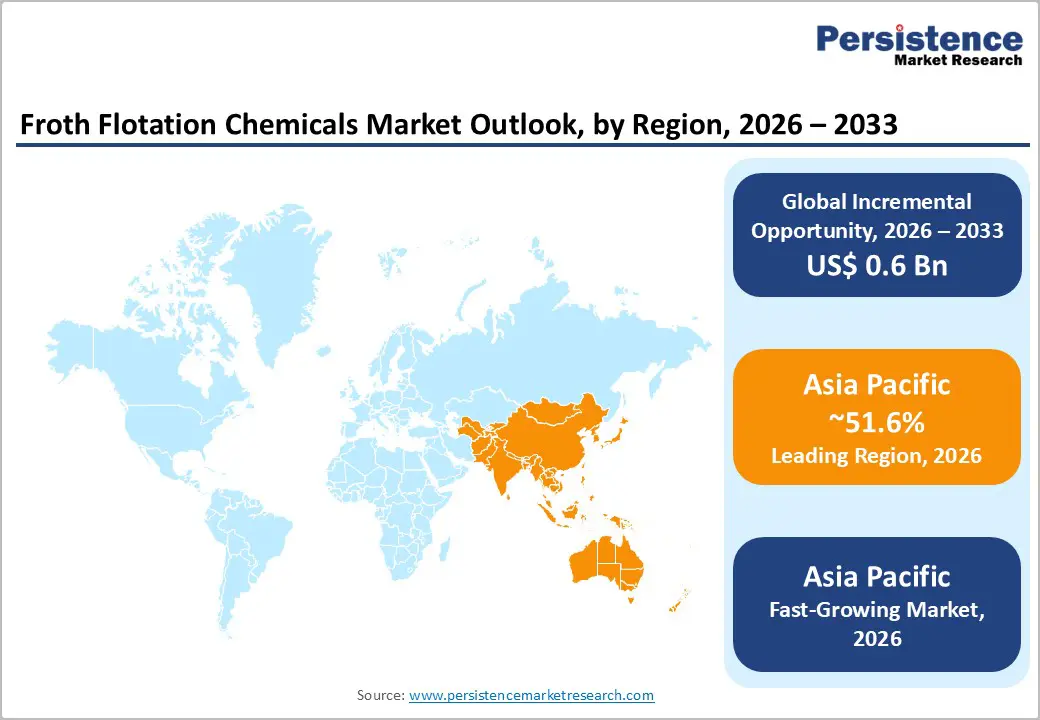

- Leading Region: Asia Pacific is projected to account for approximately 51.6% of market share, driven by large-scale mining operations and expanding industrial processing activities.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by increasing investments in mining infrastructure, water treatment, and recycling applications across China, India, and Australia.

- Investment Plans: Market investments are primarily focused on expanding mining projects, upgrading mineral processing facilities, and developing advanced flotation technologies, with companies increasing spending on R&D, digital optimization tools, and regional technical laboratories.

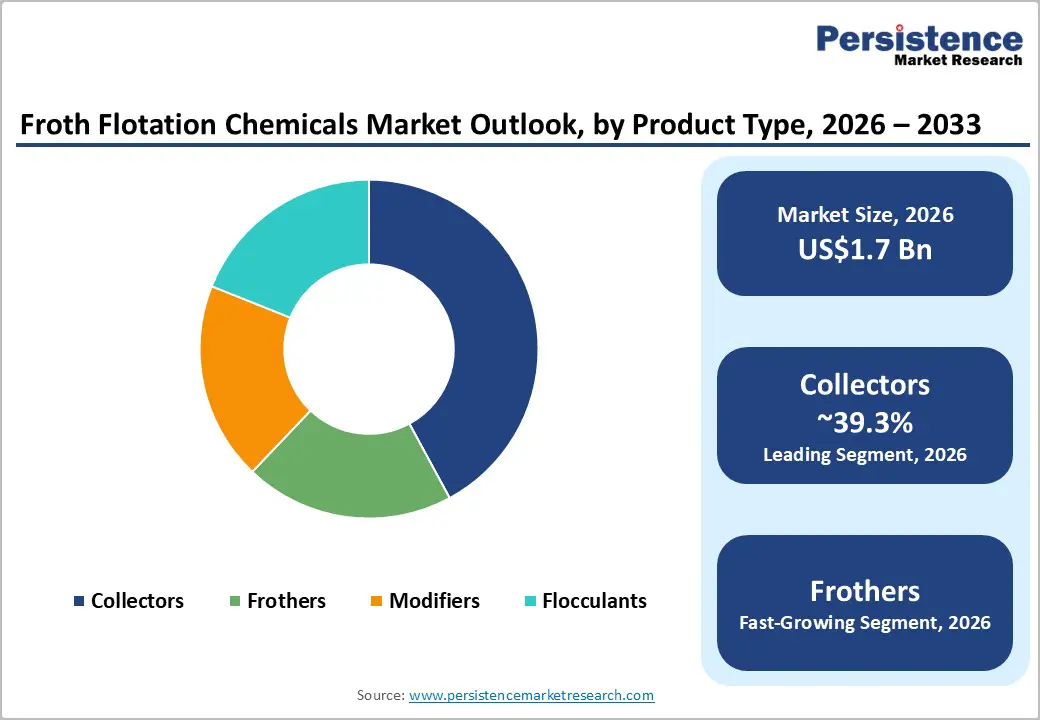

- Dominant Product Type: Collectors dominate, holding an anticipated 39.3% market share, due to their critical role in improving mineral recovery and flotation efficiency.

- Leading End-use Industry: Mining remains the leading end-use industry, accounting for an anticipated 41.2% market share, driven by rising demand for critical minerals and increasing processing of low-grade ores.

| Key Insights | Details |

|---|---|

| Froth Flotation Chemicals Market Size (2026E) | US$1.7 Bn |

| Market Value Forecast (2033F) | US$2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

DRO Analysis

Driver Analysis - Growing Demand for Critical Minerals Driving Flotation Chemical Consumption

The accelerating demand for critical minerals such as copper, lithium, nickel, cobalt, and rare earth elements is a major growth driver for the froth flotation chemicals market. These minerals are essential for electric vehicles, renewable energy systems, and power grid infrastructure. Long-term projections indicate copper demand alone is expected to increase significantly by 2040, requiring substantial investment in new mining capacity. As ore grades decline globally, mining operations increasingly depend on advanced flotation reagents to maintain recovery rates and concentrate quality. This trend directly boosts demand for collectors, frothers, and modifiers designed for complex ore processing, making flotation chemistry a critical enabler of resource efficiency.

Expansion of Water Treatment and Circular Economy Applications

The growing focus on wastewater reuse and resource recovery is expanding the application scope of flotation chemicals beyond mining. Industrial wastewater treatment, municipal sewage systems, and recycling operations are increasingly adopting flotation processes to separate contaminants, recover materials, and improve water quality. Regulatory frameworks in developed regions now mandate higher treatment efficiency and lower environmental impact, encouraging the use of specialized reagents. Flotation chemicals are widely used in deinking processes in paper recycling and in separating fine particles in industrial effluents. This diversification of end-use applications is strengthening market resilience and creating new revenue streams for chemical suppliers.

Advancements in Reagent Technology and Process Optimization

Technological innovation is transforming the flotation chemicals market from a commodity-based segment into a performance-driven solutions industry. Manufacturers are developing ore-specific formulations, advanced frothing systems, and digital dosing technologies to optimize flotation performance. The integration of process monitoring and real-time adjustment tools enables improved recovery rates, reduced reagent consumption, and enhanced operational efficiency. Companies are increasingly offering integrated solutions combining chemicals, technical services, and data analytics. This shift toward customized and high-value solutions allows suppliers to command premium pricing while improving customer retention.

Restraint Analysis - Volatility in Raw Material Costs and Supply Chain Disruptions

The production of flotation chemicals depends on petrochemical derivatives and specialty intermediates, which are subject to price volatility and supply chain disruptions. Fluctuations in raw material costs can significantly impact profit margins, particularly in a competitive market where price sensitivity is high. Mining companies often operate under strict cost controls, limiting the ability of suppliers to pass on increased costs. Long qualification cycles for new reagents further slow market responsiveness, creating operational and financial challenges for manufacturers.

Stringent Regulatory Compliance Requirements

Environmental and chemical safety regulations impose strict requirements on the production, use, and disposal of flotation reagents. Regulatory frameworks demand extensive testing, documentation, and compliance with environmental standards, increasing operational complexity and costs. Certain chemical compounds face restrictions due to toxicity concerns, requiring reformulation and additional investment in research and development. Smaller manufacturers face higher barriers to entry due to limited resources for compliance, which can constrain market competition and innovation.

Opportunity Analysis - Increasing Utilization of Low-Grade and Complex Ores

The global decline in high-grade ore reserves is creating strong demand for advanced flotation solutions capable of processing complex and low-grade deposits. These ores require highly selective reagents to achieve acceptable recovery and grade levels. Customized chemical formulations designed for specific mineral compositions are gaining traction, offering significant performance improvements without requiring major capital investment in processing infrastructure. Even marginal improvements in recovery rates can generate substantial economic benefits at scale, making this a highly attractive opportunity for reagent suppliers.

Growth in Recycling and Secondary Resource Recovery

The transition toward a circular economy is driving increased adoption of flotation technologies in recycling applications. Industries such as paper recycling, plastic recovery, and electronic waste processing are utilizing flotation methods to separate valuable materials from mixed waste streams. This trend is supported by regulatory initiatives promoting resource efficiency and waste reduction. As recycling volumes increase globally, the demand for flotation chemicals in non-mining applications is expected to grow steadily, creating a diversified and stable demand base.

Emerging Markets and Infrastructure Development

Rapid industrialization in emerging economies is creating new opportunities for flotation chemical suppliers. Expanding mining operations, increasing investments in water treatment infrastructure, and growing recycling initiatives are driving demand across Asia Pacific, Latin America, and parts of Africa. Governments in these regions are prioritizing resource security and environmental sustainability, leading to increased adoption of advanced separation technologies. Local production capabilities and strategic partnerships can further enhance market penetration in these high-growth regions.

Category-wise Analysis

Product Type Insights

Collectors are the leading segment, accounting for an anticipated 39.3% market share in 2026. Collectors play a critical role in flotation processes by selectively attaching to target mineral surfaces and enabling their separation from unwanted material. Their importance in determining recovery rates and concentrate quality makes them the most widely used reagent category. Mining operations rely heavily on tailored collector formulations for different mineral types, including sulfides (e.g., xanthates for copper and gold), oxides (fatty acid-based collectors for iron ore), and polymetallic ores. For instance, copper mining operations in Chile and Peru extensively use sulfide collectors to improve concentrate grades in complex ore systems. The dominance of collectors reflects their direct impact on process efficiency, recovery optimization, and overall project economics.

Frothers are likely to be the fastest-growing segment and are essential for stabilizing the froth layer and ensuring effective separation of mineral particles. Their demand is increasing due to the rising complexity of ore bodies and the need for improved flotation stability in high-throughput operations. Advanced frother formulations, such as alcohol- and glycol-based reagents, are being developed to enhance bubble formation, improve selectivity, and maintain consistent froth characteristics. For example, coal and iron ore beneficiation plants in Australia and China increasingly use customized frother blends to optimize throughput and reduce entrainment losses. As mining operations adopt more sophisticated flotation techniques, including coarse particle flotation, the role of frothers is becoming increasingly critical, driving their strong growth trajectory.

End-use Industry Insights

Mining is expected to be the dominant end-use industry, holding an anticipated 41.2% market share in 2026. Mining remains the largest consumer of flotation chemicals due to its reliance on flotation processes for mineral extraction. The industry’s focus on maximizing resource recovery and processing lower-grade ores is driving continuous demand for advanced reagents. Flotation chemicals are widely used in the extraction of copper, gold, zinc, nickel, and lithium, particularly in large-scale operations across regions such as Latin America, Australia, and Asia. For example, large copper mines in Chile and Indonesia depend on multi-stage flotation circuits using collectors, frothers, and modifiers to achieve high recovery rates from complex sulfide ores. The scale, operational intensity, and ongoing expansion of mining activities ensure sustained demand for flotation chemicals.

The pulp & paper segment is the fastest-growing segment, with an anticipated CAGR of 4.7%. The pulp and paper industry is increasingly using flotation chemicals for deinking and recycling processes, driven by the global shift toward sustainable packaging and circular material use. Flotation enables efficient removal of ink, adhesives, and other contaminants from recovered paper, improving the quality and usability of recycled fiber. For instance, large recycling facilities in Europe and North America utilize flotation deinking systems to process post-consumer paper waste into high-quality pulp for packaging and printing applications. The growing demand for recycled paper products, combined with stricter environmental regulations, is accelerating the adoption of flotation technologies. This segment is expected to expand steadily as industries prioritize resource efficiency and reduced environmental impact.

Regional Insights

North America Froth Flotation Chemicals Market Trends - Technology-Driven Mining Efficiency and Environmental Compliance Focus

North America represents a mature and technologically advanced market for froth flotation chemicals, with the U.S. playing a leading role due to its strong mining sector, particularly in copper, gold, and industrial minerals. The region is characterized by a high level of regulatory oversight, particularly in environmental protection and water treatment. This has led to increased adoption of advanced flotation reagents that improve efficiency while minimizing environmental impact. Regulatory bodies such as the U.S. Environmental Protection Agency continue to push for improved wastewater treatment standards, which have expanded the use of flotation technologies in industrial effluent management and municipal applications.

Innovation is a defining feature of the North American market. Major players such as Ecolab (Nalco Water division) and BASF SE are investing in high-performance reagents and digital optimization tools that integrate real-time process monitoring with chemical dosing. For example, Nalco Water’s flotation optimization platforms are widely used in copper and phosphate mining operations to enhance recovery while reducing reagent consumption. Similarly, BASF has been expanding its mining solutions capabilities, including advanced flotation and hydrometallurgical technologies, to support resource efficiency. The integration of automation and analytics is helping mining companies reduce operational variability and improve throughput.

Investment trends in North America are driven by the development of new mining projects and the modernization of existing processing plants. For instance, increased investments in copper mining projects in states such as Arizona and Nevada are supporting sustained demand for flotation chemicals. Partnerships between chemical suppliers and mining operators are becoming more strategic, focusing on long-term performance improvement rather than short-term cost reduction. This shift is strengthening demand for customized reagent programs and technical service offerings, reinforcing North America’s position as a high-value, innovation-driven market.

Europe Froth Flotation Chemicals Market Trends - Sustainability-Led Innovation in Recycling and Eco-Friendly Reagents

Europe is characterized by a strong regulatory framework and a pronounced focus on sustainability and environmental responsibility. Environmental regulations governing chemical usage and wastewater treatment are among the most stringent globally, particularly under frameworks such as REACH and updated wastewater directives. This regulatory environment has accelerated the development and adoption of environmentally friendly flotation reagents with reduced toxicity, improved biodegradability, and lower environmental impact.

Countries such as Germany, the U.K., France, and Spain contribute to regional demand through industrial processing, recycling, and water treatment applications. While large-scale mining activity is relatively limited, Europe’s strong emphasis on circular economy practices is creating new opportunities for flotation chemicals in recycling and waste management. For example, companies such as Clariant AG and Evonik Industries AG are actively developing sustainable flotation reagents tailored for both mining and industrial separation processes. These formulations are designed to meet strict environmental standards while maintaining high separation efficiency.

The region is also a hub for innovation in specialty chemicals, supported by advanced research infrastructure and strong collaboration between industry and academia. European chemical companies are investing in R&D facilities focused on mineral processing and water treatment technologies. For instance, Arkema continues to expand its specialty chemical portfolio, including solutions relevant to separation and processing applications. Europe’s commitment to sustainability, combined with regulatory harmonization across member states, is expected to drive continued demand for advanced flotation solutions, particularly in recycling and wastewater treatment segments.

Asia Pacific Froth Flotation Chemicals Market Trends - Mining Dominance with Rapid Industrial and Infrastructure Expansion

Asia Pacific is expected to be the leading region in the froth flotation chemicals market, accounting for approximately 51.6% of market share in 2026, and is also the fastest-growing market. The region’s dominance is driven by large-scale mining operations, particularly in China, India, and Australia, along with expanding industrial and recycling sectors. These countries possess significant reserves of key minerals and are investing heavily in mining and mineral processing infrastructure, which directly supports the demand for flotation chemicals.

China is a major contributor due to its extensive mining activities and strong industrial base, particularly in copper, coal, and rare earth elements. Domestic chemical manufacturers, along with global players such as Clariant AG and Syensqo, are strengthening their presence in the region to cater to growing demand. India is experiencing rapid growth driven by increasing mineral demand, infrastructure development, and expanding wastewater treatment capacity. Government initiatives focused on resource efficiency and water management are encouraging the adoption of flotation technologies in both mining and industrial applications.

Australia plays a critical role as a global mining hub, particularly for iron ore, gold, and lithium. Companies such as Orica Limited are actively expanding their flotation reagent portfolios and technical services to support mining operations. Recent developments, such as the establishment of new mining solution laboratories and regional partnerships by global chemical companies, are also enhancing local technical capabilities. These investments enable better ore-specific testing, faster product development, and improved customer support.

The region also faces significant environmental challenges, particularly related to water scarcity and pollution. This is driving increased adoption of flotation technologies in wastewater treatment, recycling, and industrial separation processes. With strong industrial demand, supportive government policies, and continuous investment in mining and infrastructure, Asia Pacific region remains the most dynamic and strategically important region in the global froth flotation chemicals market.

Competitive Landscape

The global froth flotation chemicals market is moderately fragmented, with a mix of global chemical companies and regional suppliers. Leading players hold significant market share due to their strong product portfolios, technical expertise, and global presence. Competition is based on product performance, cost efficiency, and the ability to provide customized solutions. Larger companies benefit from economies of scale and advanced research capabilities, while smaller players compete through niche offerings and regional specialization.

Key players are focusing on innovation, customization, and digital integration to differentiate their offerings. Strategic priorities include developing eco-friendly formulations, expanding regional presence, and providing integrated solutions that combine chemicals, technical services, and process optimization tools.

Key Industry Developments

- In June 2025, BASF SE entered into a strategic cooperation agreement with FUCHS in Australia to enhance the delivery of flotation and dewatering solutions, combining advanced chemistry with strong regional technical service capabilities to strengthen its presence in the mining sector.

Companies Covered in Froth Flotation Chemicals Market

- BASF SE

- Clariant AG

- Syensqo

- Ecolab Inc.

- Orica Limited

- Kemira Oyj

- Nouryon

- Arkema

- Evonik Industries AG

- Dow Inc.

- SNF Group

- Solenis

- ArrMaz

- Nasaco International LLC

- Huntsman Corporation

- Chevron Phillips Chemical Company

Frequently Asked Questions

The froth flotation chemicals market is estimated to be valued at US$1.7 billion in 2026.

The froth flotation chemicals market is projected to reach US$2.3 billion by 2033.

Key trends include rising demand for critical minerals, increasing use of flotation in wastewater treatment and recycling, and a shift toward customized, high-performance reagents integrated with digital process optimization tools.

Collectors are the leading product type segment, accounting for an anticipated 39.3% market share, due to their essential role in improving mineral recovery and separation efficiency.

The froth flotation chemicals market is expected to grow at a CAGR of 4.4% from 2026 to 2033.

Some of the major players include BASF SE, Clariant AG, Ecolab Inc., Orica Limited, and Syensqo.