- Display Technologies

- Flexible Display Market

Flexible Display Market Size, Share, and Growth Forecast 2026 – 2033

Flexible Display Market by Display Technology (LCD, OLED, E-Paper Display (EPD), Micro-LED, Others), Panel Size (Up to 6 Inch, 6 to 20 Inch, 20 to 50 Inch, Above 50 Inch), Substrate Material (Glass, Plastic/Polymer, Metal Foil), Application (Smartphones, Tablets & Laptops, Smartwatches, Wearables, Television & Digital Signage, Automotive Displays, E-readers, Gaming & Entertainment Devices, Others), and Regional Analysis for 2026–2033

Flexible Display Market Size and Trend Analysis

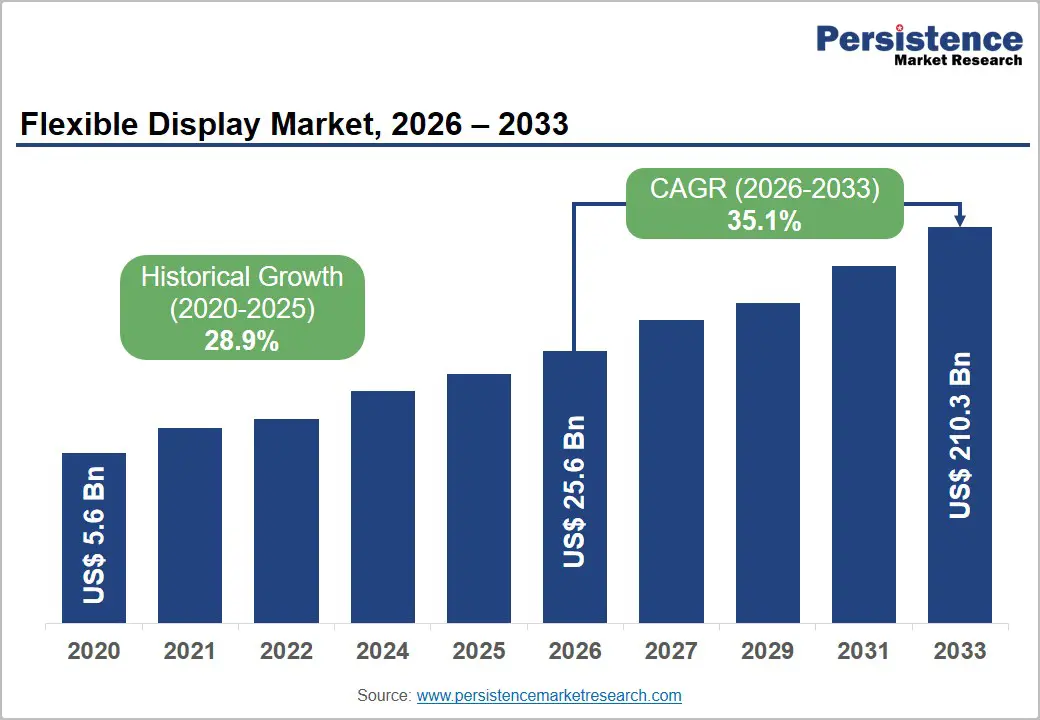

The global Flexible Display market is valued at US$ 25.6 Bn in 2026 and is projected to reach US$ 210.3 Bn by 2033, growing at a CAGR of 35.1% between 2026 and 2033. A flexible display is an advanced electronic display technology engineered to bend, fold, curve, or roll without compromising performance or durability. Unlike traditional rigid glass-based screens, flexible displays are manufactured using bendable substrates such as polyimide films and ultra-thin flexible glass, enabling innovative product designs across foldable smartphones, curved televisions, wearable electronics, automotive cockpit displays, and rollable digital devices.

The technology is transforming the consumer electronics landscape by offering lightweight structures, enhanced portability, improved design flexibility, and immersive viewing experiences. The market is witnessing strong growth driven by the rapid adoption of foldable smartphones, increasing demand for wearable electronic devices, and expanding integration of flexible displays in automotive infotainment systems and digital signage applications.

Key Industry Highlights:

- OLED Technology Dominance: OLED technology dominates the market with approximately 65% revenue share in 2026 due to its superior flexibility, ultra-thin structure, power efficiency, and strong deployment in foldable smartphones and automotive displays.

- Micro-LED Growth Surge: Flexible Micro-LED displays are expected to witness the fastest growth at nearly 52% CAGR , supported by rising investments in AR/VR devices, smart wearables, and ultra-high brightness display applications.

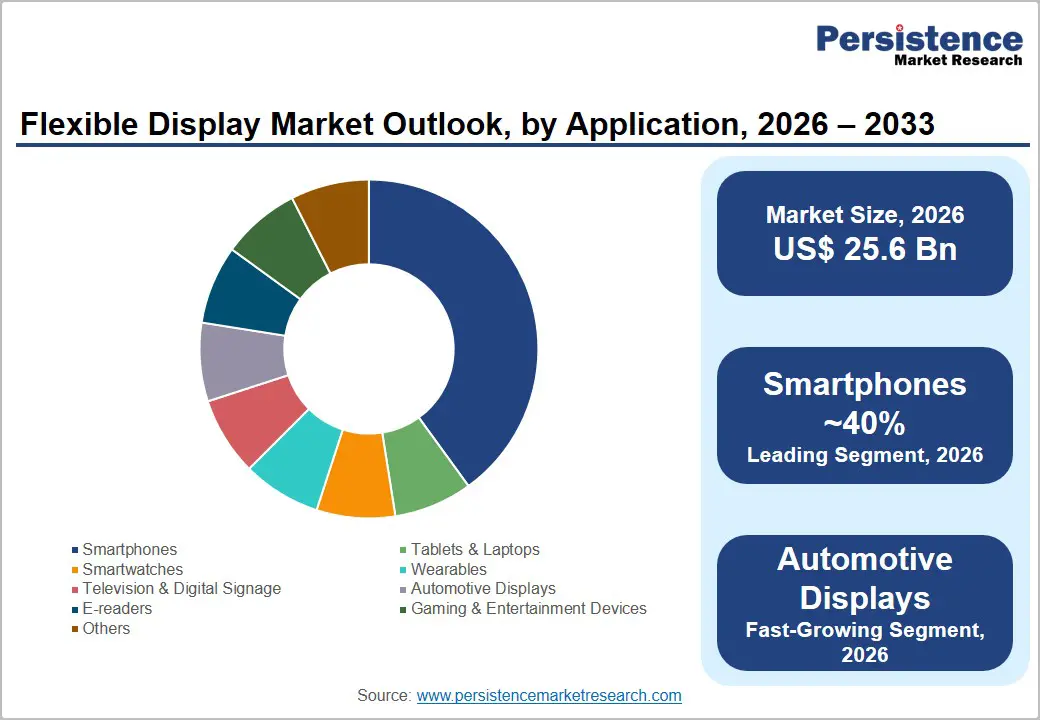

- Smartphone Demand Leadership: Smartphones account for nearly 42% of total market revenue in 2026, fueled by growing adoption of foldable OLED smartphones from global brands including Samsung, Apple, Huawei, Xiaomi, and OPPO.

- Automotive Display Acceleration: Automotive displays represent the fastest-growing application segment with approximately 48% CAGR as vehicle manufacturers increasingly integrate curved and multi-screen digital cockpit systems into electric and premium vehicles.

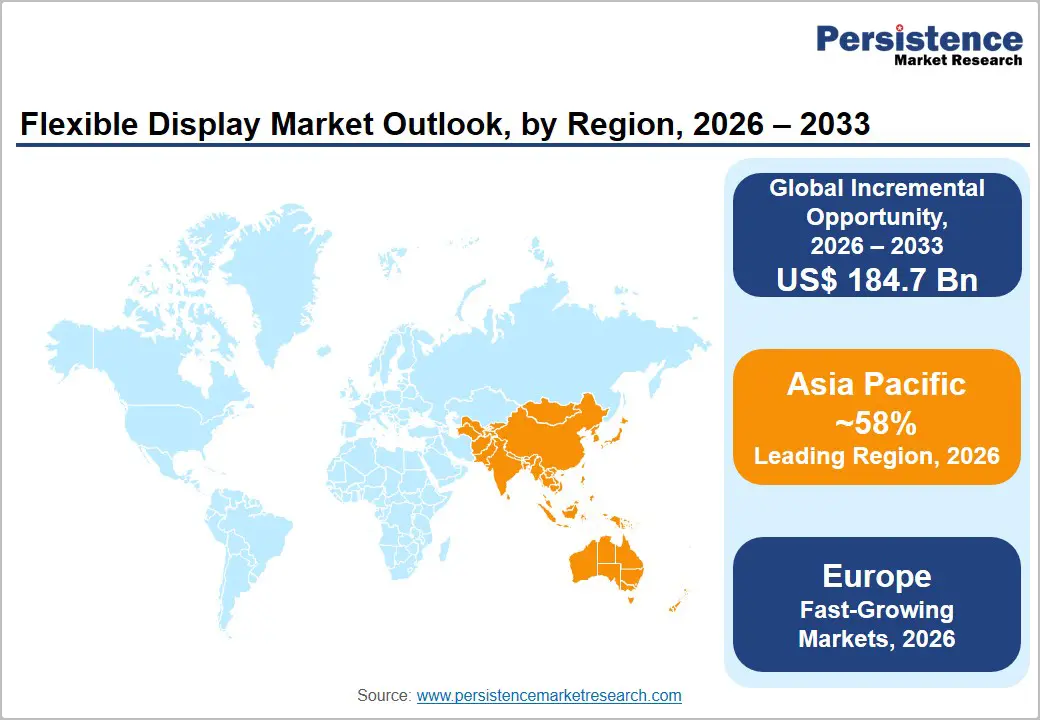

- Asia Pacific Dominance: Asia Pacific leads the global market with nearly 58% revenue share in 2026, supported by advanced manufacturing infrastructure, strong consumer electronics production, and extensive investments across China and South Korea.

- Substrate Material Leadership: Plastic and polymer substrates hold approximately 58% market share in 2026 due to their superior thermal stability, lightweight properties, mechanical flexibility, and extensive use in flexible OLED manufacturing processes.

- Foldable Device Momentum: Rapid commercialization of foldable smartphones and wearable electronic devices is accelerating flexible OLED panel production, lowering manufacturing costs, and expanding adoption across mainstream consumer electronics markets.

- Manufacturing Investment Expansion: Continuous investments by Samsung Display, LG Display, and BOE Technology Group are strengthening global flexible OLED manufacturing capacity and supporting long-term market expansion.

Market Dynamics

Drivers - Mass-Market Foldable Smartphone Adoption and OLED Panel Proliferation

Foldable smartphones have transitioned from niche luxury devices to mainstream consumer electronics between 2022 and 2025, catalyzing explosive demand for flexible OLED display panels. According to IDC (International Data Corporation), global foldable smartphone shipments exceeded 20 million units in 2023, with the growth trajectory projected to accelerate fivefold by 2028. Samsung Electronics' Galaxy Z Fold and Z Flip series, Huawei's Mate X line, and Motorola's Razr models have collectively established consumer acceptance of foldable form factors while competitive dynamics have driven entry prices progressively lower.

Flexible OLED panels valued for their superior contrast, power efficiency, and unmatched form-factor versatility are the enabling technology for foldable devices, creating a direct demand linkage between consumer adoption curves and panel production investment. Samsung Display, LG Display, and BOE Technology have collectively committed hundreds of billions in capacity investment to capture this structural demand shift.

Automotive Digital Transformation and Display-Centric Cockpit Design

The automotive industry's accelerating transition to software-defined vehicle architectures has elevated flexible displays from optional premium features to essential components of next-generation vehicle interiors. Modern vehicles increasingly incorporate curved dashboard panels, flexible center console screens, and pillar-integrated information displays, all requiring flexible OLED or advanced LCD panels.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global automobile production exceeded 90 million units in 2023, with display content per vehicle expanding rapidly as digital cockpit systems replace traditional analog instrument clusters. Automotive industry analysts project that by 2030, the average vehicle will incorporate 3–5 display screens versus 1–2 in current models, a secular increase that creates a massive and structurally expanding demand base for flexible display panels engineered to meet automotive-grade durability, wide-temperature operation, and long service life requirements.

Restraints - High Manufacturing Costs and Yield Challenges in Flexible OLED Production

Flexible OLED panel manufacturing, particularly for foldable-grade substrates, remains significantly more capital-intensive and yield-constrained than conventional rigid display production. Depositing OLED organic layers on ultra-thin polyimide substrates, combined with stringent thin-film encapsulation requirements to prevent moisture and oxygen ingress, results in substantially higher per-panel cost structures. Industry estimates indicate that flexible OLED panel rejection rates can run 2–3 times higher than those for rigid OLED panels during new product ramp-up phases, constraining supply availability and sustaining price premiums that limit penetration in mid- and lower-tier consumer electronics markets.

Display Durability and Long-Term Reliability Consumer Perception Challenges

Consumer and enterprise concerns regarding the long-term durability of foldable flexible displays, specifically crease formation, delamination risk, and brightness degradation after sustained folding cycles continue to represent a meaningful demand restraint. While Samsung Display's Ultra-Thin Glass (UTG) and LG Display's advanced encapsulation technologies have made material progress, independent durability assessments and consumer reports highlight remaining reliability gaps versus rigid display alternatives. These perceptions suppress willingness-to-pay premiums and may slow enterprise adoption of flexible display devices in rugged industrial, field service, and high-duty-cycle commercial applications where long-term reliability is paramount.

Opportunities - Flexible Micro-LED Displays Enabling Next-Generation Wearables and AR/VR Devices

The convergence of flexible substrate technology with Micro-LED display architectures represents the most technically ambitious and commercially transformative opportunity in the flexible display market. Micro-LED displays offer an unprecedented combination of luminance exceeding 100,000 nits, zero burn-in risk, and dramatically superior operational lifetime compared to OLED panels, while flexible substrate integration would enable revolutionary form factors for smartwatches, augmented reality (AR) glasses, and next-generation foldable devices. Apple Inc., Samsung, and Taiwanese manufacturers AUO and Innolux are actively investing in flexible Micro-LED development programs.

The U.S. Department of Energy's Solid-State Lighting Program projects Micro-LED display technology achieving commercial production readiness for smartwatch applications by 2026–2027, implying a near-term inflection point. The integration of GaN-on-Sapphire-derived LED chips into Micro-LED panel architectures also creates a direct technology linkage with upstream synthetic sapphire substrate demand.

Rollable and Stretchable Display Innovation Creating New Device Categories

Beyond foldable smartphones, the next technological frontier encompasses rollable, slideable, and stretchable flexible display configurations that are defining entirely new device categories. LG Electronics demonstrated rollable OLED television technology with its Signature OLED R series, while LG, Oppo, and TCL have prototyped rollable smartphone concepts targeting commercial launch. Stretchable display technology where the substrate physically elongates and conforms to irregular surfaces is being actively developed for wearable health monitoring patches, smart clothing, and conformable IoT sensor interfaces.

The EU's Horizon Europe research program has allocated dedicated funding to flexible and stretchable electronics research, recognizing their transformative potential. Market participants investing early in rollable and stretchable display intellectual property and manufacturing process development are positioned to capture substantial first-mover advantages in product categories that have not yet reached commercial scale, representing a multi-billion-dollar blue-ocean opportunity.

Category-wise Insights

Display Technology Insights

OLED technology dominates the flexible display market, commanding approximately ~65% of total flexible display market revenue in 2026. OLED's structural advantages for flexible applications zero backlight requirement, ultra-thin panel architecture, self-emissive pixels enabling perfect black levels and infinite contrast, and superior power efficiency on plastic substrates make it the technology of choice for premium foldable smartphones, smartwatches, and automotive displays.

Samsung Display and LG Display collectively account for a substantial majority of global flexible OLED production capacity, while BOE Technology is rapidly expanding its share through government-supported capital investment. The high degree of vertical integration among Korean and Chinese panel makers covering substrate preparation, backplane deposition, OLED evaporation, and thin-film encapsulation has progressively reduced flexible OLED panel costs, steadily expanding the addressable market. Market maturity in smartphone applications and rapid penetration of new categories, including automotive and wearable electronics sustain OLED's dominant market position.

Micro-LED is the fast-growing display technology, at an estimated 52% CAGR. While currently at an early commercialization stage, Micro-LED's extraordinary performance advantages including unmatched brightness, zero burn-in risk, and dramatically longer operational lifetime, are attracting massive R&D investment from Apple, Samsung, and Sony. The use of GaN-on-Sapphire-derived LED chips in Micro-LED panels creates a critical supply chain linkage with sapphire substrate materials.

Panel Size Insights

Up to 6 Inch panel size segment is the market leader, commanding approximately ~48% of flexible display revenue in 2026, driven by the overwhelming volume of flexible OLED panels deployed in premium and foldable smartphones and smartwatches. This segment benefits from the highest manufacturing maturity across the flexible display value chain, the broadest OEM customer base, and the most advanced yield optimization, translating to the most competitive cost structures within the ecosystem. Samsung's Galaxy S and Z series, Apple's iPhone OLED lineup, and the full spectrum of Android flagship smartphones collectively consume billions of sub-6-inch flexible OLED panels annually. The smartwatch segment led by Apple Watch, Samsung Galaxy Watch, and Garmin adds further high-volume consumption to this size category, ensuring its sustained revenue leadership through the forecast period.

The 6 to 20 Inch segment is the fastest growing at approximately 42% CAGR, driven by rapid adoption of flexible OLED in foldable large-screen smartphones, tablets, laptop displays, and automotive cockpit panels. Rising consumer willingness to pay for premium flexible display experiences in productivity and entertainment devices is fuelling above-average growth in this size category.

Substrate Material Insights

Plastic/Polymer substrates, primarily polyimide (PI) film, are the dominant substrate material for flexible displays, accounting for approximately ~58% of market revenue in 2026. Polyimide's exceptional thermal stability (withstanding OLED deposition temperatures up to 450°C), chemical resistance, optical clarity, and inherent mechanical flexibility make it the substrate of choice for flexible OLED manufacturing. Key substrate suppliers, including Kolon Industries (South Korea) and DuPont (USA) provide high-performance PI films to leading panel manufacturers globally. The adoption of colorless polyimide (CPI) as a flexible cover window material in foldable smartphones replacing conventional glass in the folding zone further expands plastic substrate content per device. Advances in barrier coating deposition have largely resolved earlier moisture perm veation concerns, cementing polyimide's market-leading position in flexible display substrate materials through the forecast period.

Metal foil substrates are the fast-growing material segment at approximately 38% CAGR. Superior thermal conductivity beneficial for high-luminance Micro-LED panel applications, combined with excellent dimensional stability and hermeticity make metal foil increasingly attractive for industrial flexible displays and next-generation Micro-LED panels. Growing R&D investment by leading panel manufacturers in metal foil processing is accelerating commercialization.

Application Insights

Smartphones dominate flexible display applications, accounting for approximately ~42% of total market revenue in 2026. The universal adoption of flexible OLED panels in premium smartphones by Samsung, Apple, Huawei, Xiaomi, and OPPO, combined with the rapidly growing foldable smartphone subsegment, make smartphones the largest flexible display application by a substantial margin. According to IDC, global smartphone shipments reached 1.17 billion units in 2023, with OLED penetration in flagship models approaching 100% and expanding progressively into mid-tier price bands.

The foldable smartphone subsegment requiring two full-size flexible OLED panels per device amplifies per-unit panel consumption and revenue versus conventional smartphones, providing a structurally value-accretive growth vector within the largest application category. Television & Digital Signage, Automotive Displays, and Smartwatches collectively represent the next tier of application demand, with Automotive Displays emerging as the fast-growing individual application segment.

Automotive displays are the fast-growing application in the forecast period. The automotive sector's sweeping transition to digital cockpit architectures featuring curved, multi-screen flexible display arrays and the proliferation of electric vehicles with display-centric interiors are the primary growth catalysts. BMW, Mercedes-Benz, Tesla, and BYD are integrating increasingly sophisticated flexible display systems as standard features in new vehicle programs, amplifying panel demand.

Regional Insights

North America Flexible Display Market Trends

North America is a technologically advanced and high-value flexible display market, characterized by strong premium smartphone adoption, robust demand from the automotive display sector, and early adoption of flexible display technologies in defense and industrial applications. The United States as the home of Apple Inc., the world's largest single consumer of premium flexible OLED panels is the region's primary and defining demand driver. The sustained commitment of the U.S. National Science Foundation (NSF) and DARPA to flexible electronics research, combined with the FlexTech Alliance's industrial development programs, provides a robust innovation foundation for next-generation flexible display technologies.

North America's automotive sector including Ford, General Motors, and Tesla represents a fast-growing demand channel for automotive-grade flexible displays, driven by vehicle electrification and the digital cockpit transformation accelerated by Tesla's industry-setting touchscreen-centric interior designs. The region's enterprise and defense procurement represents an additional high-value demand tier for ruggedized flexible display solutions.

- U.S. Flexible Display Market Trends

The United States accounts for approximately 38% of North America's flexible display market revenue and is projected to grow at approximately 32% CAGR reflecting the country's high per-capita premium device spending and first-mover enterprise adoption. Apple Inc.'s iPhone lineup all utilizing flexible OLED displays sourced from Samsung Display and LG Display since 2017, represents one of the largest single procurement streams for flexible OLED panels globally, establishing quality standards that propagate across the industry.

DARPA and the FlexTech Alliance are driving development of next-generation flexible electronics for defense wearables, conformal sensor arrays, and field communications systems. Domestic EV production expansion by Ford, GM, and Tesla is simultaneously accelerating automotive-grade flexible display demand, establishing the U.S. as a multi-vector growth market for flexible display technology through the forecast period.

Europe Flexible Display Market Trends

Europe's flexible display market is driven by premium automotive display demand, progressive sustainability regulations favoring energy-efficient display technologies, and a research-intensive photonics and electronics ecosystem. Germany's automotive OEMs including BMW, Mercedes-Benz, and Volkswagen represent Europe's premier demand center for automotive-grade flexible displays, driving strategic OEM partnerships with Asian panel manufacturers. The EU Chips Act, committing €43 billion to semiconductor and advanced display technology investments, is expected to stimulate European R&D and production capacity in flexible display technologies over the forecast period.

The EU's Energy Labeling Regulation favors flexible OLED displays for their superior energy efficiency compared to LCD, providing a regulatory tailwind for market growth. European consumers demonstrate elevated willingness to pay for premium foldable and flexible OLED smartphones, supporting healthy adoption across the region's key national markets.

- Germany Flexible Display Market Trends

Germany holds approximately 25% of Europe's flexible display market share and is projected to grow at approximately 30% CAGR, making it the region's largest and fast-growing market. Germany's global automotive leadership through BMW, Mercedes-Benz, and Volkswagen creates premium demand for automotive-grade flexible displays in curved cockpit panels, heads-up display (HUD) systems, and multi-zone pillar displays. Fraunhofer IPMS and other research institutes conduct frontier flexible display processing research, supporting application development and commercialization. Germany's well-developed electronics manufacturing supply chain and growing EV production, driven by substantial government incentives further accelerate flexible display module integration into next-generation vehicle platforms and industrial automation systems.

- U.K. Flexible Display Market Trends

The UK's globally renowned flexible electronics research base anchored by the University of Cambridge's Centre for Advanced Photonics and Electronics and the Plastic Electronics Foundation has generated substantial intellectual property in organic semiconductor and flexible display processing. UK defense procurement through the Ministry of Defence (MoD) and QinetiQ is an established early adopter of flexible display technologies for soldier wearables, vehicle-mounted situational awareness systems, and field communications devices. The UK's dynamic fintech, retail, and hospitality sectors are emerging consumers of flexible OLED point-of-sale and interactive signage solutions, adding commercial breadth to the country's flexible display demand profile.

- France Flexible Display Market Trends

France's world-renowned digital retail and luxury brand ecosystem centered on Paris as the global capital of fashion and luxury consumer goods drives premium demand for flexible OLED signage, interactive retail displays, and custom-shaped display applications in haute couture and luxury wearables. French automotive manufacturer Stellantis (Peugeot, Citroën, DS Automobiles brands) is actively integrating flexible display technologies in new vehicle cockpits, supported by substantial French government EV transition incentives. France's high-tech industrial sector and government-supported innovation programs through Bpifrance and the French Tech initiative provide additional momentum for flexible display technology adoption.

- Italy Flexible Display Market Trends

Italy's distinguished tradition in premium consumer goods, high-end automotive design, and precision engineering creates a distinctive demand base for flexible OLED displays across luxury products. Italian automotive brands Ferrari and Alfa Romeo (Stellantis Group) are adopting curved and flexible digital cockpit displays in flagship vehicle models, while Italian consumer electronics design studios are integrating flexible display elements in premium lifestyle products. Italy's growing fashion-tech sector, where wearable technology intersects with luxury design, represents an emerging and high-margin application niche for custom-form flexible OLED displays in the Italian market.

Asia Pacific Flexible Display Market Trends

Asia Pacific dominates the global Flexible Display market, accounting for approximately 58% of total revenue in 2026, representing simultaneously the world's primary manufacturing hub and largest consumption market for flexible display panels. South Korea hosts the world's most advanced flexible OLED manufacturing capabilities through Samsung Display and LG Display, while China's BOE Technology, CSOT, and Visionox have made rapid strides in expanding production capacity. Japan's indispensable materials and equipment supply chain including Nitto Denko, Sumitomo Chemical, and Canon Tokki underpins global flexible display manufacturing quality and efficiency.

India and the broader ASEAN region represent emerging high-growth consumption markets driven by rising smartphone penetration and government electronics manufacturing incentives. China's domestic flexible display demand fuelled by Huawei, Xiaomi, Vivo, and OPPO foldable device launches is the second-largest national consumption market globally, reinforcing Asia Pacific's dual role as manufacturer and consumer of flexible display panels.

- China Flexible Display Market Trends

China holds approximately 40% of Asia Pacific's flexible display market share and is projected to reach ~36% CAGR, making it the world's most dynamic national market for flexible display production and consumption. BOE Technology has emerged as a formidable global competitor in flexible OLED manufacturing, supplying panels to Huawei, Xiaomi, and increasingly to Apple. China's massive domestic smartphone market with annual shipments exceeding 280 million units per IDC provides unmatched manufacturing scale for flexible display consumption. National programs including Made in China 2025 and the National Integrated Circuit Development Plan are channeling substantial government support into advanced display technology investment, supporting China's ambition to achieve flexible OLED technology parity with Korean incumbents.

- India Flexible Display Market Trends

India's flexible display market is projected to expand at approximately 42% CAGR the region's fastest national growth rate from a current base of approximately 5% of Asia Pacific revenues, reflecting enormous untapped penetration potential. India is the world's second-largest smartphone market by unit volume, and is rapidly transitioning toward OLED and flexible display handsets driven by rising middle-class incomes and competitive product launches from Samsung, Xiaomi, Vivo, and domestic brands.

The Government of India's PLI Scheme for mobile phones and electronics has attracted Samsung, Foxconn, and Tata Electronics to establish large-scale manufacturing operations, accelerating flexible display component integration at national scale. The imminent deployment of domestic semiconductor and display manufacturing capacity under India's semiconductor incentive programs will further structurally entrench the country's position as a long-term high-growth flexible display market.

- South Korea – Samsung Display and LG Define Global Flexible OLED Benchmarks

South Korea commands approximately 32% of Asia Pacific's flexible display market share and is projected to grow at ~33% CAGR, anchored by its position as the global technology and quality leader in flexible OLED manufacturing. Samsung Display the world's largest flexible OLED panel producer and LG Display collectively define industry benchmarks for flexible OLED performance, durability, and manufacturing yield.

South Korea's government-backed Display Industry Development Strategy, announced in 2021, committed US$ 65 billion in display manufacturing investments, explicitly targeting next-generation flexible and Micro-LED display technologies. The country's world-class semiconductor and display equipment supply chain including Samsung Electronics Semiconductor, SK Hynix, and Dongwon Systems makes South Korea the most innovation-intensive flexible display market globally, with first-to-market advantages in foldable, rollable, and stretchable display applications.

Competitive Landscape

The global flexible display market is moderately concentrated at the panel manufacturing level, with Samsung Display, LG Display, and BOE Technology collectively accounting for the substantial majority of global flexible OLED production capacity. However, the broader value chain spanning flexible substrate suppliers, OLED material producers, display driver IC developers, and OEM device manufacturers is considerably more fragmented, with hundreds of companies competing across specialized sub-segments.

Market leaders differentiate through continuous capital investment in advanced flexible OLED manufacturing lines, proprietary encapsulation technologies, and co-development of display driver ICs with OEM partners. Chinese panel makers are aggressively challenging Korean leadership through government-backed capacity expansion and technology licensing strategies, while Japanese materials and precision equipment companies maintain indispensable positions throughout the global supply chain.

Key Developments:

- In May 2026, Samsung Electronics globally launched its latest Odyssey gaming monitors and ViewFinity S8 displays featuring DisplayPort 2.1 technology, enhancing high-resolution visual performance across gaming and professional display applications.

- In March 2026, Samsung Display showcased AI-optimized OLED technologies at MWC26, featuring Flex Magic Pixel privacy displays, ultra-durable foldable OLEDs, and 5,000 PPI RGB OLEDoS-enabled mixed reality experiences.

- In August 2025, Samsung Display introduced its new foldable display brand “MONT FLEX™” at K-Display 2025, highlighting advanced durability, ultra-thin design, narrow bezels, and premium foldable display innovation.

- January 2025: Samsung Display announced the mass production launch of a new generation of ultra-thin flexible OLED panels with enhanced fold durability rated up to 400,000 fold cycles, targeting next-generation foldable smartphones from multiple global OEM brands.

- October 2024: BOE Technology completed commissioning of its 8.6-generation flexible OLED production line in Chengdu, China, significantly expanding capacity to supply flexible OLED panels to Apple, Huawei, and other major domestic OEM customers.

- April 2024: LG Display announced a strategic supply partnership with BMW to provide curved flexible OLED display panels for next-generation vehicle cockpit systems, marking a landmark milestone in premium automotive flexible display adoption.

Companies Covered in Flexible Display Market

- Samsung Display

- LG Display

- BOE Technology Group

- AUO Corporation

- Innolux Corporation

- Japan Display Inc.

- Visionox Technology

- Tianma Microelectronics

- Royole Corporation

- E Ink Holdings

- Sharp Corporation

- CSOT (China Star Optoelectronics Technology)

- EverDisplay Optronics

- HannStar Display

- Konica Minolta

Frequently Asked Questions

The global Flexible Display market is valued at US$ 25.6 billion in 2026 and is projected to reach US$ 210.3 billion by 2033, expanding at an exceptional CAGR of 35.1% over the 2026–2033 forecast period. The market grew from US$ 5.6 billion in 2020 at a historical CAGR of 28.9%, driven by rapid foldable smartphone adoption and flexible OLED panel proliferation across consumer electronics.

The primary growth drivers include mass-market adoption of foldable and rollable smartphones with global foldable shipments exceeding 20 million units in 2023 per IDC the automotive industry's transition to multi-screen flexible display cockpits across 90+ million vehicles annually (OICA data), and sustained capital investment by Samsung Display, LG Display, and BOE Technology in expanding flexible OLED production capacity to reduce per-panel costs and broaden addressable market scope.

OLED is the dominant display technology segment, accounting for approximately ~65% of total flexible display market revenue in 2026. OLED's structural advantages for flexible applications including self-emissive pixels, zero backlight requirement, ultra-thin form factor, and superior power efficiency on polyimide substrates make it the enabling technology for premium foldable smartphones, smartwatches, and automotive cockpit displays produced by Samsung, Apple, Huawei, and leading automotive OEMs.

Asia Pacific leads the global Flexible Display market with approximately 58% revenue share in 2026, functioning simultaneously as the world's primary manufacturing hub and largest consumption market. South Korea's Samsung Display and LG Display define global flexible OLED technology benchmarks, while China is the world's largest national consumer of flexible display panels through its dominant smartphone market and BOE Technology's rapidly expanding production capacity.

The development of Micro-LED flexible displays combining the extraordinary performance advantages of Micro-LED technology with the form-factor versatility of flexible substrates represents the most transformative near-term opportunity. Apple, Samsung, and Sony are accelerating flexible Micro-LED development for next-generation smartwatches and AR devices, with commercial deployment projected within the 2026–2027 timeframe per the U.S. Department of Energy's Solid-State Lighting Program, implying a near-term inflection point for the market.

The leading companies include Samsung Display Co., Ltd. (South Korea) the world's largest flexible OLED producer LG Display Co., Ltd. (South Korea), BOE Technology Group Co., Ltd. (China), AUO Corporation (Taiwan), Innolux Corporation (Taiwan), Japan Display Inc. (Japan), Visionox Technology (China), E Ink Holdings Inc. (Taiwan), and Universal Display Corporation (USA), among others. These companies compete on manufacturing scale, technology innovation, OEM relationships, and supply chain integration depth.